|

市場調査レポート

商品コード

1444069

スマート兵器(スマートウェポン):市場シェア分析、業界動向と統計、成長予測(2024~2029年)Smart Weapons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマート兵器(スマートウェポン):市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

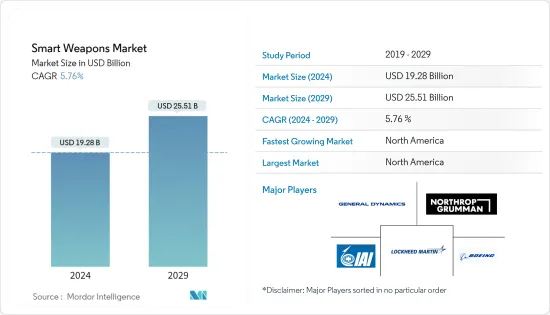

スマート兵器(スマートウェポン)市場規模は2024年に192億8,000万米ドルと推定され、2029年までに255億1,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.76%のCAGRで成長します。

主なハイライト

- スマート兵器市場は、新型コロナウイルス感染症(COVID-19)のパンデミックにより、前例のない課題に直面しました。パンデミックの急速な拡大は市場に大きな影響を与えました。世界中のさまざまな国によるロックダウンの実施は、サプライチェーンに影響を与え、重要な原材料の移動や物流上の課題に混乱をもたらしました。さらに、必須原材料の移動に関連した課題、さまざまな防衛企業による大量解雇、および世界中のさまざまな防衛関係者によるスマート兵器の注文の減少により、スマート兵器システムの生産が減少しました。

- 一方で、防衛システムの製造業者やサービスプロバイダーは、防衛産業の収益と営業成績の低下に耐えるために、拡張や研究開発への投資を削減する必要がありました。この指標は、スマート兵器の取得に関して世界中のさまざまな防衛関係者による需要の増加により、新型コロナウイルス感染症後の力強い回復を示しています。さらに、さまざまな防衛メーカーによる高度な機能を備えたスマート兵器の研究開発への投資の増加により、予測期間中に市場の成長が促進されると予想されます。

- さらに、戦争の変化と高精度の武器と弾薬の需要が、スマート兵器市場を推進する2つの主な要因です。現在、世界中で起こっている紛争により、精密攻撃と作戦攻撃の重要な必要性が浮き彫りになっています。巻き添え被害を回避するための重要な必要性は、世界中の国々のための高度なスマート兵器の調達の必要性においても強調されています。

- さらに、新興国の軍事支出の増加は、新しい先進的なスマート兵器の開発に貢献しており、予測期間中にスマート兵器市場の成長につながると予想されます。

スマート兵器市場動向

法執行部門は予測期間中に最高のCAGRで成長すると予想される

- 法執行部門は、予測期間中に大幅な成長を示すと予想されます。世界中で銃乱射事件に関連した事件が増加しており、銃による暴力の増加による死者数の増加を減らす必要性が高まっていることが、近い将来、法執行機関向けのスマート兵器の成長に寄与する主な要因となると思われます。未来。

- 現在、銃による暴力の増加により、死亡に関わる事件が増加しています。近年、世界中で銃器による負傷や死亡が増加しており、多くの子供や青少年に悪影響を及ぼしています。信頼できるビジネス情報源からのデータによると、2020年には銃器が主な死因となっています。米国では、2021年に銃による負傷で48,830人が死亡しました。

- さらに、疾病管理予防センター(CDC)のデータによると、2021年の米国の銃関連死亡のうち54%が自殺(26,328人)で、43%が殺人(20,958人)で、残りは銃による死亡です。事故(549件)、法執行機関が関与したもの(537件)、または未確定の状況によるもの(458件)。現在、銃暴力による死亡者数を減らすために、世界中のさまざまな法執行機関が必要な措置を講じる必要性が高まっています。

- 銃をより安全かつスマートにする必要性が高まっています。近年、法執行機関向けのスマート銃に関してさまざまな大きな開発が行われていますが、無線や超音波を介して作動するものなど、真のスマート銃に適した技術はまだ初期段階にあり、開発には何年もかかります。未来。一方で、指紋スキャンや顔認識システムなどの技術の進歩により、法執行部門向けのスマート兵器の成長が促進されています。

- 現在のシナリオでは、パーソナライズされたスマートガンが世界中の法執行機関に利用可能になります。 2022年1月、LodeStar Works社は法執行機関向けの9mmスマートハンドガンの発表を発表しました。さらに、現在、望ましくない死亡事故を防ぐために、顔認識などの高度な技術を備えたスマートガンが開発されています。さらに、スマートガンは自殺を減らし、紛失または盗難された銃を無用にし、銃の強奪を恐れる警察官や刑務所の看守に安全を提供することにも貢献しています。

- したがって、スマートガンの技術進歩と世界中で望ましくない死亡事故を防ぐためのスマートガンの使用量の増加は、予測期間中の法執行部門におけるスマート兵器の市場のプラスの成長につながります。

北米は予測期間中に目覚ましい成長を示すと予想

- 北米は、予測期間中に最も高い成長を示すと予測されています。防衛予算の増加は、この地域のさまざまな主要企業による技術進歩の増加と相まって、市場の成長を促進します。

- 2023年の米国の国防予算は7億7,300万米ドルに達しました。この予算は、2022年度制定の基準レベルである7,423億米ドルと比べて307億米ドルまたは4.1%増加し、2022年度の要求レベルからは8.1%増加します。 2021年度のレベルと比較して、2023年度の要求は2年間で700億米ドル(9.8%)近く増加しました。

- ここ数年、北米地域における銃乱射事件の件数は増加しています。 Gun Violence Archivesのデータによると、2023年 5月の時点で、米国では少なくとも13,959人が銃暴力により死亡しています。さらに、死亡者のうち491人が10代、85人が子供でした。2023年の銃暴力による死者の大部分は自殺によるものでした。2023年の自殺による死者数は1日あたり平均約66人でした。これが米国のさまざまな防衛メーカーによるスマート兵器の開発の増加につながりました。

- 一方で、軍事用のスマート兵器に関しては成長が見られ、米国はこの点で大幅な成長を目の当たりにしています。現在のシナリオでは、米国国防軍のスマート兵器に関して技術の進歩が見られます。現代の戦場では、地上、海上、空中を問わず、電子機器とデータがあふれています。レーダー、ソナー、LiDARなどの確立されたシステムや技術から得られるデータの量は、戦士が処理するには多すぎるため、意思決定を共有できる半自律型または「スマート」兵器の開発が奨励されています。現在、兵器には人工知能(AI)や機械学習(ML)技術が搭載されており、これらの兵器の多くは光、音、電磁波(EM)によって誘導され、選択した標的に高精度で到達するようになっています。さらに、スマート兵器は、複数の信号環境で不要な信号をフィルタリングし、潜在的なターゲットが多数存在する戦場で特定のターゲットを見つけるようにプログラムできます。この点に関して、米国は現在、壁越しに敵の位置を正確に特定することができ、武装勢力が隠れていると思われる場所に到達すると爆発する弾丸を発射できる新しいスマート兵器の開発に取り組んでいます。

- したがって、法執行機関と軍事分野の両方で先進技術を活用した先進的なスマート兵器の開発は、予測期間中に北米で大幅な成長を遂げるスマート兵器市場につながるでしょう。

スマート兵器業界の概要

スマート兵器市場は本質的に細分化されており、さまざまな企業が市場で大きなシェアを占めています。著名な市場企業には、General Dynamics Corporation、Israel Aerospace Industries Ltd.、Lockheed Martin Corporation、Northrop Grumman Corporation、The Boing Companyなどが挙げられます。

市場の主要企業は、世界中のさまざまな防衛要員が軍事作戦を実行するために使用する高度なスマート兵器システムの開発に焦点を当てています。さらに、先進的なスマート兵器システムの製造に向けた研究開発への支出の増加は、近い将来により良い機会の創出につながるでしょう。現在、さまざまなメーカーが、そのような武器の誤使用や誤用を防ぐ指紋認識などの技術を統合しており、これが予測期間中のスマート兵器市場の成長を支えることが期待されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高度な精密攻撃兵器に対する需要の高まり

- 市場抑制要因

- 武器輸送に関する規制

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品

- ミサイル

- 弾薬・その他

- 技術

- 衛星誘導

- レーダー誘導

- 赤外線誘導

- レーザー誘導

- プラットフォーム

- 陸上

- 海上

- 空中

- エンドユーザー別

- 法執行機関

- 軍事

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- General Dynamics Corporation

- Israel Aerospace Industries Ltd.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Rafael Advanced Defense Systems Ltd.

- Rheinmetall AG

- The Boeing Company

- MBDA

- BAE Systems plc

- Raytheon Technologies Corporation

- Safran

第7章 市場機会と将来の動向

The Smart Weapons Market size is estimated at USD 19.28 billion in 2024, and is expected to reach USD 25.51 billion by 2029, growing at a CAGR of 5.76% during the forecast period (2024-2029).

Key Highlights

- The smart weapons market witnessed unprecedented challenges due to the COVID-19 pandemic. The rapid spread of the pandemic had a significant impact on the market. Implementation of lockdowns by various countries worldwide led to affecting the supply chain and disruption in the movement of essential raw materials and logistics challenges. Moreover, the challenges related to the movement of essential raw materials, mass layoffs by various defense companies, as well as a reduction in terms of orders for smart weapons by various defense personnel worldwide led to a decline in the production of smart weapon systems.

- On the other hand, the defense systems manufacturers and service providers had to reduce expansion and R&D investments to withstand the decline in revenue and operating performance of the defense industry. The marker showcased a strong recovery post-covid due to an increase in demand by various defense personnel worldwide in terms of acquiring smart weapons. Moreover, the growing investments in research and development of smart weapons having advanced capabilities by various defense manufacturers are expected to propel the growth of the market during the forecast period.

- In addition, a change in warfare and demand for high-precision arms and ammunition are the two major factors that are driving the smart weapons market. Current conflicts which are taking place all over the world have spotlighted the critical need for precision attacks and operational strikes. A crucial need for avoiding collateral damage has also been stressed in the need for the procurement of advanced smart weapons for countries across the world.

- In addition, the increasing military spending of emerging countries is helping in terms of the development of new and advanced smart weapons and is expected to lead to the growth of the smart weapons market during the forecast period.

Smart Weapons Market Trends

Law Enforcement Segment is Anticipated to Grow with the Highest CAGR During the Forecast Period

- The law enforcement segment is anticipated to show significant growth during the forecast period. The increasing number of incidents related to mass shootings around the world and the growing need to cut down on the increasing number of deaths due to growing gun violence will be the major factors that will contribute to the growth of smart weapons for law enforcement in the near future.

- Currently, there has been an increasing rise in the number of incidents related to deaths due to growing gun violence. Firearm injuries and deaths around the world have increased in recent years and adversely affect many children and adolescents. According to data from a trusted business source, in 2020, firearms became the leading cause of death. In the US, in 2021, 48,830 people died from gun-related injuries.

- Moreover, according to data from the Centers for Disease Control and Prevention (CDC), in 2021, 54% of all gun-related deaths in the US were suicides (26,328), while 43% were murdered (20,958) while the remaining gun deaths were accidental (549), involved law enforcement (537) or had undetermined circumstances (458). Currently, there is a growing need for various law enforcement agencies across the globe to take the necessary steps in order to reduce the number of fatalities related to gun violence.

- There has been an increasing need to make guns safer and smarter. Although there have been various major developments with regard to smart weapons for law enforcement in recent times still, proper technology for a true smart gun, such as one that operates via radio or ultrasonic waves, is still in the fledgling stage and is many years in the future. On the other hand, advancements in technologies such as fingerprint scanning and facial recognition systems are propelling the growth of smart weapons for the law enforcement segment.

- In the present scenario, personalized smart guns are being made available to law enforcement agencies worldwide. In January 2022, LodeStar Works company announced the unveiling of their 9mm smart handgun for law enforcement agencies. Moreover, smart guns are now being developed with advanced technologies such as facial recognition in order to help prevent unwanted fatalities. In addition, smart guns are also helping to reduce suicides, render lost or stolen guns useless, and offer safety for police officers and jail guards who fear gun grabs.

- Thus, technological advancement for smart guns and the increasing growth of the usage of smart guns to prevent unwanted fatalities worldwide will lead to positive market growth for smart weapons in the law enforcement segment during the forecast period.

North America Will Showcase Remarkable Growth During the Forecast Period

- North America is projected to show the highest growth during the forecast period. The increasing defense budget, coupled with increasing technological advancements by various major players in the region, will foster market growth.

- In 2023, the defense budget for the US amounted to USD 773 million. This budget represents a USD 30.7 billion or 4.1 percent increase over the FY 2022 enacted base level of USD 742.3 billion and an 8.1 percent increase from the FY 2022 requested level. Compared to the FY 2021 level, the FY 2023 request has grown by nearly USD 70 billion (9.8 percent) over a 2-year period.

- There has been a growth with regard to the number of incidents regarding mass shootings in the North American region over the past few years. As of May 2023, according to data from Gun Violence Archives, at least 13,959 people have died from gun violence in the US. Moreover, of those who died, 491 were teens, and 85 were children. Deaths by suicide have made up the vast majority of gun violence deaths in 2023. There's been an average of about 66 deaths by suicide per day in 2023. This has led to an increase in the development of smart weapons by various defense manufacturers in the US in recent years. Making use of advanced technology such as fingerprint sensors has enabled the development of smart guns which do not fire other than when it is in the hands of the fingerprinted user. Smart guns have been a notoriously quixotic category for decades. The weapons carry the hope that an extra technological safeguard might prevent a wide range of gun-related accidents and death.

- On the other hand, there has been a growth with regard to smart weapons for the military, and the US is witnessing significant growth in this regard. In the present scenario, there have been technological advancements with regard to smart weapons for the United States defense forces. Modern battlefields are immersed in electronic devices and data, whether on the ground, at sea, or in the air. The amounts of data from well-established systems and technologies such as radar, sonar, and LiDAR are becoming too much for any warrior to process, encouraging the development of semi-autonomous or 'smart' weapons that can share in decision-making. Currently, weapons are now being equipped with artificial intelligence (AI) and machine learning (ML) technologies, and many of these weapons are being guided by light, sound, or electromagnetic (EM) waves to reach a selected target with high accuracy. In addition, smart weapons can be programmed to filter unwanted signals in multiple-signal environments and find a specific target on a battlefield with many potential targets. The US, in this regard, is now engaged in the development of new smart weapons which can pinpoint an enemy's location through a wall, and rounds can be fired, which explode upon reaching the place where the insurgent is believed to be hiding.

- Thus, developments in advanced smart weapons that make use of advanced technology both in the law enforcement and military sector will lead to the market of smart weapons witnessing significant growth in North America during the forecast period.

Smart Weapons Industry Overview

The smart weapons market is fragmented in nature, with various players holding significant shares in the market. Some prominent market players are General Dynamics Corporation, Israel Aerospace Industries Ltd., Lockheed Martin Corporation, Northrop Grumman Corporation, and The Boeing Company, amongst others.

The key players in the market are focusing on the development of advanced smart weapons systems, which will be used by various defense personnel around the world to carry out their military operations. Moreover, growing expenditure on research and development towards manufacturing advanced smart weapon systems will lead to creating better opportunities in the near future. Various manufacturers are now currently integrating technologies such as fingerprint recognition which will prevent accidental use and misuse of such weapons, and this is expected to support the growth of the smart weapons market during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for advanced precision strike weapons

- 4.3 Market Restraints

- 4.3.1 Regulations on arm transport

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product

- 5.1.1 Missiles

- 5.1.2 Ammunition and Other Products

- 5.2 Technology

- 5.2.1 Satellite Guidance

- 5.2.2 Radar Guidance

- 5.2.3 Infrared Guidance

- 5.2.4 Laser Guidance

- 5.3 Platform

- 5.3.1 Land

- 5.3.2 Sea

- 5.3.3 Air

- 5.4 By End-User

- 5.4.1 Law Enforcement

- 5.4.2 Military

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 Latin America

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 Rest of Latin America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 Israel Aerospace Industries Ltd.

- 6.2.3 Lockheed Martin Corporation

- 6.2.4 Northrop Grumman Corporation

- 6.2.5 Rafael Advanced Defense Systems Ltd.

- 6.2.6 Rheinmetall AG

- 6.2.7 The Boeing Company

- 6.2.8 MBDA

- 6.2.9 BAE Systems plc

- 6.2.10 Raytheon Technologies Corporation

- 6.2.11 Safran

7 Market Opportunities and Future Trends

- 7.1 Advancement in terms of weapons technology