真空断熱パネル-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Vacuum Insulation Panel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639374

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

真空断熱パネル市場規模は2025年に88億1,000万米ドルと推定され、2030年には112億4,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5%を超えると予測されます。

COVID-19パンデミックは、封鎖や規制による製造施設や工場の操業停止により、市場に悪影響を与えました。サプライチェーンと輸送の混乱はさらに市場に障害をもたらしました。しかし、産業は2021年に回復を示し、その結果、調査された市場の需要は回復しました。

主要ハイライト

- 短期的には、建設産業からの旺盛な需要と自動保管・検索用真空断熱パネルの世界の採用が、調査対象市場の成長を促進する要因となっています。

- 反面、非標準サイズに対する高コストとパネルの重さが市場成長の妨げになる可能性が高いです。

- しかし、エネルギー効率の高い材料を推進する規制がますます厳しくなっていることや、真空断熱パネルのコストを削減する自動化パネルを導入する研究開発イニシアティブは、予測期間中に調査した市場に機会を提供する可能性が高いです。

真空断熱パネルの市場動向

建設セグメントが力強い成長を遂げる

- 真空断熱パネル(VIP)は、最も高い断熱能力を持つ有望な断熱材の一つであり、建設産業で広く受け入れられています。

- 真空断熱パネルは、建築部材の薄型化、室内空間の拡大と土地利用の最適化、耐用年数後の構成材料のリサイクル可能性など、建設セグメントにおけるその他の利点も備えています。

- 米国国勢調査局によると、米国における2022年の商業建築額は1,147億9,000万米ドルで、前年比17.63%の増加を示しました。

- さらに、アジア太平洋、中東・アフリカなどの地域では、産業ユニット、病院、モール、劇場、ホテル、ITセクターの設立のために国内外から巨額の投資が集まっており、真空断熱パネルの需要に拍車がかかる可能性があります。

- サウジアラビアでは、不動産開発の増加、住宅需要の増加、社会経済インフラ整備のための政府の取り組みが、同国の真空断熱パネル市場を牽引しています。サウジアラビアのMajid Al-Hogail住宅相によると、サウジアラビア王国は今後5年間で30万戸の住宅建設を計画しています。ビジョン2030」におけるサウジアラビアの重要なイニシアチブのひとつが住宅です。今後数年間、同国の建設産業から真空断熱パネル市場への需要が生まれる可能性が高いです。

- Institution of Civil Engineers(ICE)の調査によると、世界の建設産業は2030年までに8兆米ドルに達すると予想されており、主に中国、インド、米国が牽引しています。

- さらに、エネルギー効率の高い構造を義務付ける建築基準法や施策が増加していることも、建設部門による環境に優しくエネルギー節約につながる材料の使用増加を促進しています。

- したがって、建設産業における上記の動向は、予測期間中の真空断熱パネル市場の成長を促進すると予想されます。

市場を独占するアジア太平洋

- アジア太平洋が世界市場シェアを独占。インド、中国、フィリピン、ベトナム、インドネシアでは、住宅や商業施設の建設活動への投資が増加しており、市場は今後数年間で成長すると予想されます。

- 2011~2022年までの中国における建設生産額は、この産業の成長が進んでいることを示しています。例えば、中国国家統計局によると、2022年の中国の建設生産額はピーク時で約27兆6,300億人民元(4兆1,000億米ドル)に達します。

- 在宅所得率の上昇と農村部から都市部への人口移動により、中国では住宅建設需要が増加すると予想されます。公共部門と民間部門の両方で手頃な価格の住宅が重視されるようになれば、住宅建設部門の開発に拍車がかかると考えられます。

- 中国では現在、開発中または計画中の空港建設プロジェクトがいくつかあります。例えば、新疆ウイグル自治区は、近代的な空港ネットワークシステムを形成するため、新たに8つの空港の建設を計画しています。新疆空港グループは、2023~2025年にかけて、バヤンブラク、バルコル、ウス、ホボクサル、チエモに空港を建設する計画を発表しました。

- さらに、2021年に建設産業で新たに締結された契約額は1,345億人民元(195億2,000万米ドル)で、前年同期比2.5%増、伸び率は7.1%縮小しました。中国は2022年1月、第14次5カ年計画(2021~2025年)期間中に建設産業を発展させる計画を発表し、より環境に優しく、よりスマートで、より安全な道を歩む同国経済の柱を打ち立てた。そのため、建設からの契約増は真空断熱パネル市場にとってプラスに働くと予想されます。

- さらにインドでは、政府が2022年1月に国内21カ所のグリーンフィールド空港の開発を承認しました。国内最大の空港は、ウッタル・プラデーシュ州のガウタム・ブッダ・ナガル地区に建設されます。民間航空省は、今後数年間でインド全土に21の空港を追加建設する意向です。

- さらに、インド空港公団(AAI)は今後4~5年の間に、3億3,800万米ドルで新空港の建設と多くの既存空港の拡大・改良を計画しています。これは、既存ターミナルの拡大・変更、新ターミナルの建設、既存滑走路、技術ブロック、エプロン、空港ナビゲーションサービスの管制塔の拡大・強化で構成されます。

- さらに、2025年までに、デリー、ベンガルール、ハイデラバードの3つのPPP(官民パートナーシップ)空港が、拡大計画に3,000億インドルピー(38億1,000万米ドル)を投資する予定です。そのため、真空断熱パネル市場に上昇需要が生まれます。

- インドでは、政府が27の産業クラスターの開発に1,205億米ドルを投資するという目標を掲げており、国内の商業建設が活発化すると期待されています。

- したがって、アジア太平洋諸国におけるこのような投資や計画されたプロジェクトはすべて、同地域における建設活動を後押ししており、予測期間中、真空断熱パネルの需要を促進すると予想されます。

真空断熱パネル産業概要

真空断熱パネル市場は細分化されています。この市場の主要企業(順不同)には、Evonik Industries AG、Panasonic Corporation、Dow、Knauf Insulation、OCI Company Ltdなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設産業からの旺盛な需要

- 真空断熱パネルの自動保管・検索への採用

- その他の促進要因

- 抑制要因

- 非標準サイズのVIPの高コスト

- 真空断熱パネルの重い重量

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 芯材

- シリカ

- ガラス繊維

- その他

- 構造タイプ

- フラット

- 特殊形態

- 用途

- 建築

- 冷却・冷凍装置

- 物流

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AVERY DENNISON CORPORATION

- Chuzhou Yinxing Electric Co. Ltd

- Csafe

- Dow

- Etex Group

- Evonik Industries AG

- KCC CORPORATION

- Kevothermal

- Kingspan Group

- Knauf Insulation

- Morgan Advanced Materials

- Panasonic Corporation of North America

- Recticel Insulation

- TURNA d.o.o

- Vaku-Isotherm GmbH

- Va-Q-Tec AG

第7章 市場機会と今後の動向

- 自動化パネル導入に向けた研究開発の取り組み

- サステイナブル建築用真空断熱パネル

目次

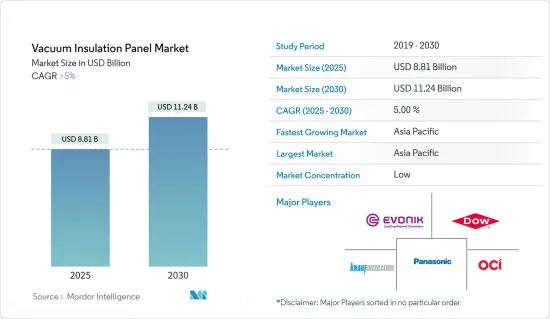

The Vacuum Insulation Panel Market size is estimated at USD 8.81 billion in 2025, and is expected to reach USD 11.24 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market due to the shutdown of manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, robust demand from the construction industry and the adoption of vacuum insulation panels for automated storage and retrieval worldwide are factors driving the studied market's growth.

- On the flip side, the high cost for non-standard sizes and the heavy weight of the panels will likely hinder the studied market's growth.

- However, increasingly stringent regulations promoting energy-efficient materials and R&D initiatives to introduce automated panels to reduce vacuum insulation panel costs will likely provide opportunities for the market studied during the forecast period.

Vacuum Insulation Panel Market Trends

Construction Segment to Witness Strong Growth

- Vacuum insulation panels (VIPs) are one of the most promising insulation materials with the highest thermal insulating capacity and are widely accepted in the construction industry.

- Vacuum insulation panels also offer other advantages in the construction sector, like the reduced thickness of building components, increased indoor space and land use optimization, and recyclability of constitutive materials after their service life.

- According to the US Census Bureau, the value of commercial construction in the United States amounted to USD 114.79 billion in 2022, which showed an increase of 17.63% compared to the previous year.

- Additionally, regions like Asia-Pacific, the Middle East, and Africa are attracting huge domestic and foreign investments for setting up industrial units, hospitals, malls, theaters, hotels, and the IT sector, which may add to the demand for vacuum insulation panels.

- In Saudi Arabia, the growing number of real estate developments, increasing demand for residential property, and governmental initiatives to develop socio-economic infrastructure drive the vacuum insulation panel market in the country. According to Majid Al-Hogail, the Saudi Housing Minister, the Kingdom of Saudi Arabia plans to construct 300,000 extra housing units over the next five years. One of Saudi Arabia's significant initiatives under Vision 2030 is housing. It will likely create demand for the vacuum insulation panel market from the country's construction industry in the upcoming years.

- According to a study by the Institution of Civil Engineers (ICE), the global construction industry is expected to reach USD 8 trillion by 2030, primarily driven by China, India, and the United States.

- Furthermore, the rising number of building codes and policies mandating energy-efficient structures is further facilitating an increase in the construction sector's usage of eco-friendly and energy-conserving materials.

- Hence, the trends above in the construction industry are expected to drive the growth of the vacuum insulation panel market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market share. With growing investments in residential and commercial construction activities in India, China, the Philippines, Vietnam, and Indonesia, the market is expected to grow in the coming years.

- The output value of construction in China from 2011 to 2022 indicates progressive growth in the industry. For instance, according to the National Bureau of Statistics of China, in 2022, the construction output value in China peaked at around CNY 27.63 trillion (USD 4.10 trillion).

- Rising household income rates and population migration from rural to urban areas are expected to increase demand for residential construction in China. Increased emphasis on both public and private sector affordable housing would fuel development in the residential construction sector.

- There are currently several airport construction projects in China, either in the development or planning stage. For instance, the Xinjiang Uygur autonomous region plans to construct eight new airports to form a modern airport network system. Xinjiang Airport Group announced its plan to build airports in Bayanbulak, Barkol, Wusu, Hoboksar, and Qiemo from 2023 to 2025.

- Moreover, in 2021, the value of newly signed contracts in the construction industry was CNY 134.5 billion (USD 19.52 billion), an increase of 2.5% year-on-year, and the growth rate narrowed by 7.1% compared with the same period last year. In January 2022, China unveiled plans to develop its construction industry during the 14th Five-Year Plan (2021-2025), paving a pillar of the country's economy on a greener, smarter, and safer path. Therefore, increasing contracts from construction is expected to include an upside for the vacuum insulation panel market.

- Moreover, in India, the government approved the development of 21 greenfield airports in the country in January 2022. The country's largest airport will be built in Uttar Pradesh's Gautam Buddha Nagar area. The Ministry of Civil Aviation intends to build 21 additional airports across India in the next few years.

- Furthermore, in the next four to five years, the Airports Authority of India (AAI) plans to create new airports and expand and upgrade many existing airports for USD 338 million. It comprises the expansion and alteration of existing terminals, the construction of new terminals, and the expansion or strengthening of existing runways, technical blocks, aprons, and the control towers of the Airport Navigation Services.

- In addition, by 2025, three PPP (Public-Private Partnership) airports in Delhi, Bengaluru, and Hyderabad will invest INR 30,000 crore (USD 3810 million) in expansion plans. Therefore, creating an upside demand for the vacuum insulation panel market.

- In India, the government's target for investing USD 120.5 billion in developing 27 industrial clusters is expected to boost commercial construction in the country.

- Hence, all such investments and planned projects in the Asia-Pacific countries are boosting construction activities in the region, which are anticipated to drive the demand for vacuum insulation panels during the forecast period.

Vacuum Insulation Panel Industry Overview

The vacuum insulation panel market is fragmented in nature. The major players in this market (not in any particular order) include Evonik Industries AG, Panasonic Corporation, Dow, Knauf Insulation, and OCI Company Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Robust Demand from Construction Industry

- 4.1.2 Adoption of Vacuum Insulation Panel for Automated Storage and Retrieval

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of VIPs for Non-standard Sizes

- 4.2.2 Heavy Weight of Vacuum Insulation Panels

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Core Material

- 5.1.1 Silica

- 5.1.2 Fiberglass

- 5.1.3 Other Core Materials

- 5.2 Structure Type

- 5.2.1 Flat

- 5.2.2 Special Shape

- 5.3 Application

- 5.3.1 Construction

- 5.3.2 Cooling and Freezing Devices

- 5.3.3 Logistics

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AVERY DENNISON CORPORATION

- 6.4.2 Chuzhou Yinxing Electric Co. Ltd

- 6.4.3 Csafe

- 6.4.4 Dow

- 6.4.5 Etex Group

- 6.4.6 Evonik Industries AG

- 6.4.7 KCC CORPORATION

- 6.4.8 Kevothermal

- 6.4.9 Kingspan Group

- 6.4.10 Knauf Insulation

- 6.4.11 Morgan Advanced Materials

- 6.4.12 Panasonic Corporation of North America

- 6.4.13 Recticel Insulation

- 6.4.14 TURNA d.o.o

- 6.4.15 Vaku -Isotherm GmbH

- 6.4.16 Va-Q-Tec AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 R&D Initiatives to Introduce Automated Panels

- 7.2 Vacuum Insulated Panels for Sustainable Buildings

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日