|

市場調査レポート

商品コード

1432575

オルソキシレン:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Ortho-Xylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オルソキシレン:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

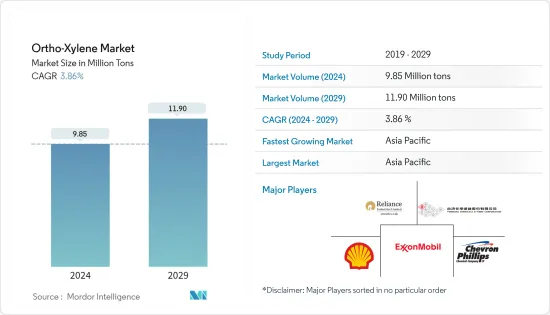

オルソキシレンの市場規模は2024年に985万トンと推定され、2029年には1,190万トンに達すると予測され、予測期間(2024-2029年)のCAGRは3.86%で成長すると予測されます。

市場を牽引する主な要因は、PVC製造の中間体としてのオルソキシレン需要の増加、塗料や接着剤の製造におけるオルソキシレンの広範な使用です。

主なハイライト

- オルソキシレンの神経学的悪影響と、無水フタル酸(PA)生産におけるナフタレンの使用が市場成長の妨げになると予想されます。

- アジア太平洋地域が世界市場を独占し、中国やインドなどの国々が最大の消費量を記録しました。

オルソキシレン市場動向

市場を独占する無水フタル酸(PA)

- 無水フタル酸は工業的にはアントラキノン製造のための重要な原料です。また、アリザリンやアリザリン誘導体だけでなく、多くの浴用染料の製造にも使用されます。フルオレセイン、エオシン、ローダミン染料にも直接使用されます。

- 無水フタル酸からはいくつかのエステルが作られ、主にプラスチック産業で可塑剤として使用されています。アルキド樹脂、グリプタール樹脂、レジル樹脂、フタル酸ジオクチル、ポリビニル樹脂の製造にも使用されます。

- 無水フタル酸の需要が増え続けているため、代替原料の探索が活発化しています。石油精製所から大量に入手できるオルソキシレンが最も適していると思われます。

- オルソキシレンには、無水フタル酸の製造原料としていくつかの利点があります。オルソキシレンの酸化は、オルソキシレンが液体であるため、ナフタレンの酸化よりも単純な供給システムを可能にします。

- オルソキシレンの酸化に必要な空気の理論量は、ナフタレンの酸化に必要な量のわずか3分の2です。反応中に放出される熱量は、ナフタレンのそれよりも121kcal少ないです。生成物は純度が高く、理論収率もナフタレンより高いです。さらに、オルソキシレンは常温で液体であるため、よりシンプルな供給システムが可能です。

- したがって、無水フタル酸の需要増加に伴い、オルソキシレンの消費量は予測期間中に増加する可能性が高いです。

アジア太平洋地域が市場を独占する

- アジア太平洋地域では、中国がGDPで最大の経済大国です。オルトキシレンの主な割合は、フタル酸系PVC可塑剤の製造に使用される無水フタル酸の製造に使用されます。中国は可塑剤の唯一最大の市場であり、世界の消費量の40%以上を占めています。

- PVCは自動車産業で広く使用されています。PVCの熱可塑性特性は、金属に比べて重量が軽いです。また、他の製造方法と比較して低コストです。外装部品や自動車内装部品に最適です。PVCは、軽量で耐久性があり、成形が容易で、外観が魅力的なため、外装部品に好まれています。

- 代替材料の代わりにPVCを使用することで、部品全体のコストを20~60%下げることができます。PVCで作られる自動車部品には、インストルメントパネル、フロアカバー、マッドフラップ、シール、サンバイザー、石害防止などがあります。

- 中国は2009年以来、世界最大の自動車メーカーであり、現在の生産シェアは約29.06%です。

- 内需の減少と自動車メーカーの他国への浸透により、2018年の生産量は4.2%減少しました。需要はまだ増加しているため、減少は一時的なものと予想されます。

- そのため、前述の要因から無水フタル酸の消費量は多いです。このため、予測期間中にオルソキシレンの需要が増加する可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- PVC製造の中間体としての需要の増加

- 塗料および接着剤産業におけるオルソキシレンの広範な使用

- 抑制要因

- オルソキシレンの神経学的悪影響

- 無水フタル酸(PA)製造におけるナフタレンの使用

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途

- 無水フタル酸

- 殺菌剤

- 大豆除草剤

- 潤滑油添加剤

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析

- 主要企業の戦略

- 企業プロファイル

- China Petroleum & Chemical Corporation

- Exxon Mobil Corporation

- Flint Hills Resources

- Formosa Chemicals and Fibre Corporation

- KP Chemical Corp.

- Nouri Petrochemical Company

- Reliance industries Ltd

- Royal Dutch Shell PLC

- SK Global Chemical Co. Ltd

第7章 市場機会と今後の動向

The Ortho-Xylene Market size is estimated at 9.85 Million tons in 2024, and is expected to reach 11.90 Million tons by 2029, growing at a CAGR of 3.86% during the forecast period (2024-2029).

The major factors driving the market studied are the increasing demand for ortho-xylene as an intermediate for PVC production, and extensive usage of ortho-xylene in the production of paints and adhesive.

Key Highlights

- Detrimental neurological effects of ortho-xylene and usage of naphthalene for the production of phthalic anhydride (PA) areexpected to hinder the growth of the market studied.

- Asia-Pacific dominated the global market, with the largest consumption recorded from the countries, such as China and India.

Ortho-Xylene Market Trends

Phthalic Anhydride (PA) to Dominate the Market

- Phthalic anhydride is industrially an important raw material for the production of anthraquinone. Itis also used in the manufacture of many vat dyes, as well as in alizarin and alizarin derivatives. It is used directly for the fluorescein, eosin, and rhodamine dyes.

- Several esters are made from phthalic anhydride, and are largely used in the plastics industry, as plasticizers. It is also used to manufacture alkyd resins, the glyptal and rezyl resins, dioctyl phthalate, and the poly-vinyl resins.

- The ever-increasing demand for phthalic anhydride has stimulated a search for alternative raw materials. Ortho-xylene, which is available in abundant quantities from the petroleum refineries, appears to be the most suitable.

- O-xylene has several advantages as a raw material for the production of phthalic anhydride. The oxidation of o-xylene permits a simpler feed system than that of the oxidation of naphthalene, due tothe liquid state of o-xylene.

- The theoretical amount of air required for oxidizing o-xylene is only two-thirdof the amount required for the oxidation of naphthalene. The heat emitted off during the reaction is 121 kcal less than that of naphthalene. The product is of higher purity, and the theoretical yield percentage is higher than that of naphthalene. Furthermore, as o-xylene is a liquid at ordinary temperature, its use permits a simpler feed system.

- Thus, with increasing demand for phthalic anhydrade, the consumption of o-xylene is likely to increase during the forecast period.

Asia-Pacific to Dominate the Market

- In the Asia-Pacific region, China is the largest economy in terms of GDP. The major proportion of ortho-xylene is used in the manufacture of phthalic anhydride that is used in the production of phthalate-based PVC plasticizers. China is the single largest market for plasticizers, with more than 40% of the global consumption. Some of the manufacturers of PVC in the country are Shin-Etsu Chemical Co. Limited, Xinjiang Zhongtai Chemical Co. Ltd, Lubrizol, Hanwha Chemical, Formosa Plastics, etc.

- PVC is widely used in the automotive industry. PVC's thermoplastic properties have lesser weight compared to metals. It has a lower cost of manufacturing methods compared to the cost of other methods. It is an ideal choice for exterior and automotive interior parts. PVC is favored for exterior parts, owing to its light weight, durability, easily shapeable quality, and attractive appearance.

- The overall cost of a component can be brought down to 20-60%, by using PVC instead of alternative materials. Some of the automotive components made with PVC include instrument panels, floor coverings, mud flaps, seals, sun visors, and anti-stone damage protection.

- China is by far the largest automotive manufacturer in the world, since 2009, with a current share of production of about 29.06%.

- The production decreased by 4.2% in 2018, owing to the decrease in domestic demand and penetration of automotive manufacturers to other countries. The decline is expected to be temporary, as the demand is still increasing.

- Therefore, owing to the aforementioned factors, the consumption of phthalic anhydride is high. This may lead to an increase in demand for ortho-xylene, during the forecast period.

Ortho-Xylene Industry Overview

The ortho-xylene market is fragmented in nature. The major companies includeRoyal Dutch Shell PLC,Reliance Industries Limited,China Petroleum & Chemical Corporation, andExxon Mobil Corporation, and Formosa Chemicals & Fibre Corp.among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand as an Intermediate for PVC Production

- 4.1.2 Extensive Usage of Ortho-xylene in Paints and Adhesive Industries

- 4.2 Restraints

- 4.2.1 Detrimental Neurological Effects of Ortho-xylene

- 4.2.2 Usage of Naphthalene for the Production of Phthalic Anhydride (PA)

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Phthalic Anhydride

- 5.1.2 Bactericides

- 5.1.3 Soybean Herbicides

- 5.1.4 Lube Oil Additives

- 5.1.5 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East & Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East & Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 China Petroleum & Chemical Corporation

- 6.4.2 Exxon Mobil Corporation

- 6.4.3 Flint Hills Resources

- 6.4.4 Formosa Chemicals and Fibre Corporation

- 6.4.5 KP Chemical Corp.

- 6.4.6 Nouri Petrochemical Company

- 6.4.7 Reliance industries Ltd

- 6.4.8 Royal Dutch Shell PLC

- 6.4.9 SK Global Chemical Co. Ltd