|

市場調査レポート

商品コード

1852159

キシレン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Xylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| キシレン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年09月10日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

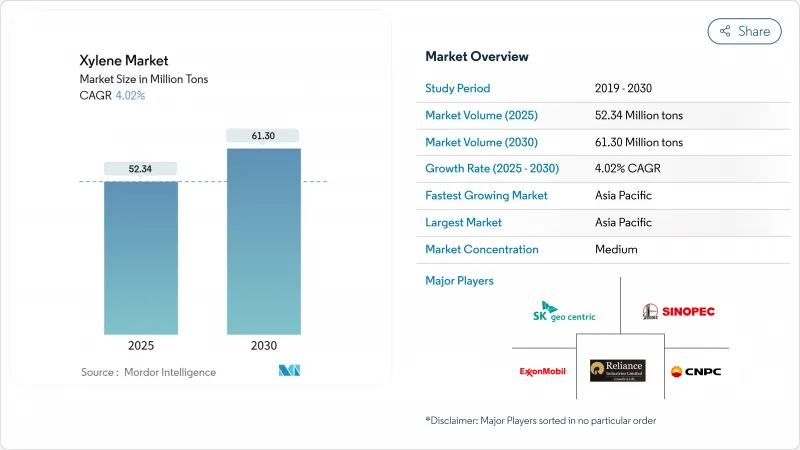

キシレンの市場規模は2025年に5,234万トンとなり、2030年には6,130万トンに達すると予測され、CAGRは4.02%です。

成長の背景には、ポリエステル生産におけるパラキシレンの支配的な役割、アジアと中東における大規模な総合芳香族プロジェクト、北米におけるエンジニアリングプラスチック需要の増加があります。中国とインドのコンビナートにおける急速な設備投資が地域の自給率を引き上げる一方、規制とブランドオーナーからの圧力が強まる中、バイオベースの化学物質が初期段階で勢いを増しています。マージンの見通しはナフサ価格の変動に左右されるが、後方統合型メーカーは精製、芳香族、誘導品の各チェーンで価値を獲得しています。競争優位性は、原料の柔軟性、デジタルの最適化、信頼できる脱炭素化ロードマップを兼ね備えた企業に傾きつつあります。

世界のキシレン市場の動向と洞察

PET樹脂需要の急増がアジアのパラキシレン消費を促進

ポリエステルの大量生産が原料の流れを再編成しています。中国は、2024年から2028年の間にパラキシレンの大量生産能力を計画しています。この増設により、急成長するPETフィルムとボトルの生産に対応するPTA供給が確保されます。生産者はコストとロジスティクスを管理するために垂直統合を進めており、一方、ナフサ輸入の増加はアジアの不足を補うものです。

中東とアジア全域の統合型芳香族コンプレックスにおける能力拡張

サウジアラムコのアミラル・コンプレックスのようなプロジェクトは、精製と下流のアロマティクスを組み合わせることで、原料の節約と高いパラーキシレン収率を実現しています。共用ユーティリティ、先進触媒、リアルタイムの最適化により、単位コストを削減し、地域の輸出競争力を強化します。これらのメガサイトは、供給バランスをシフトさせ、古い単独プラントに合理化やアップグレードを迫っています。

欧州と北米で芳香族系溶剤の使用を制限する厳しいVOC規制

規制当局はVOC規制を消費者向け塗料、クリーナー、室内製品にまで拡大しています。この規制を遵守するために、改質業者は化学物質全体の添加量を削減したり、再設計したりしなければならず、成熟した経済圏での成長が制約されます。生産者は市場アクセスを維持するため、低芳香族またはバイオベースブレンドに軸足を移します。

セグメント分析

パラキシレンは、PTAおよびPETチェーンにおける不可欠な役割により、2024年のキシレン市場シェアの90%を占める。川下への強固な統合により、大手精製業者はマージンの変動をヘッジし、旺盛な需要を確保しています。Ortho-キシレンは、はるかに小さいもの、無水フタル酸の柔軟な可塑剤需要を背景に、CAGR 4.09%で成長をリードしています。Meta-キシレンはニッチコーティングと特殊樹脂に対応し、混合キシレンは異性体分離の供給オプション性を提供します。触媒の進歩と異性化装置により、事業者は価格シグナルに合わせて生産量を微調整することができ、コモディティ化した製品群の中で収益性を高めることができます。この適応能力は、デリバティブ取引の流れが再編成されても、パラキシレンの中心性を維持します。

生産者は、アジアでパラキシレン抽出装置のデボトルネックを続け、規模の経済を利用し、拡大するPETボトル注文に対応しています。北米の供給業者は、低アセトアルデヒド生成を要求するフィルム用途の付加価値グレードを重視します。欧州の精製業者は、排出規制の強化に対応するため、混合溶媒を水素化溶媒に向ける傾向を強めており、この動向は2030年まで各異性体に特化した需要を開拓することになります。

2024年のキシレン市場の85%を占めるのはテクニカルグレードであり、これはコーティング剤配合業者、接着剤配合業者、工業用洗浄業者がコスト、入手性、中間レンジの溶解性を優先しているためです。リフォーメートとBTXプールからの単純な製造ルートは、豊富な供給量と競合価格をもたらします。新興国の大量消費者は、インフラや製造の急増期にこの量を吸収し、その中心的役割を強化しています。

逆に、高純度99.9%材料は、半導体、医薬品、高機能樹脂用途でCAGR 4.7%で成長しています。その厳格な仕様を満たすには、高度な晶析、蒸留、オンストリーム分析が要求され、高い参入障壁と魅力的な利幅を生み出しています。統合されたラボ・サービスと強固な品質システムを持つ生産者は、この特殊なレーンを活用し、汎用品と比較してトン当たりEBITDAを高めています。

地域分析

アジア太平洋地域は2024年にキシレン市場の55%を占め、2030年まで年率4.51%の成長を続ける。中国のパラキシレン能力は2028年まで年産2,500万トン拡張され、地域の自給率を下支えし、インドのPETラインは旺盛な飲料需要を供給します。ASEAN主要国は不足分を補うために混合キシレンを輸入し、アジア域内貿易の流れを維持しています。競争の激化はスプレッドを縮小させ、提携と川下PTAの連結に拍車をかけています。

北米は低成長ながら安定しています。頁岩ベースの原料経済により、精製業者は有利なBTX収率を得る。自動車の軽量化規制はエンジニアリングプラスチックの使用を増加させ、塗料における厳しいVOC規制にもかかわらず、誘導体需要を強化しています。規制の明確化と確立されたロジスティックスが相俟って、新工場建設よりもむしろデボトルネックの増加を促します。

欧州の成熟した需要環境は、持続可能性指令の下で再構築されつつあります。ドイツの化学クラスターは高効率プロセスに磨きをかけ、英国とフランスは循環型溶剤回収装置を導入し、EU全体のREACH分類は低芳香族ブレンドへの再製造を促しています。政策的なインセンティブに支えられたバイオベースのパイロット事業は、再生可能な芳香族で早期の足がかりを築くことを目指しており、ニッチグレードは高級塗料やエレクトロニクス市場をターゲットにしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- PET樹脂需要の急増がキシレンを促進する

- 中東とアジアにおけるアロマティクス・コンプレックスの能力拡張

- 自動車の軽量化が北米のエンジニアリングプラスチックスを牽引する

- キシレン使用量の増加

- サプライチェーンが乱高下する中での製薬会社による溶剤の戦略的備蓄

- 市場抑制要因

- 欧州と北米で芳香族溶剤の使用を制限する厳しいVOC規制

- 健康毒性への懸念が酸素系溶剤へのシフトを促す

- 揮発性ナフサ価格が生産者マージンを圧縮する

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- オルソキシレン

- メタキシレン

- パラキシレン

- 混合キシレン

- グレード別

- テクニカルグレード

- 高純度グレード(99.9)

- 供給源別

- 石油ベースキシレン

- バイオベースキシレン

- 用途別

- 溶剤

- モノマー

- その他の用途

- エンドユーザー業界別

- プラスチック・ポリマー

- 塗料・コーティング

- 接着剤

- その他のエンドユーザー業界

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- ENEOS Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- GS Caltex Corporation

- Indian Oil Corporation Ltd

- INEOS AG

- LOTTE Chemical Corporation

- Mangalore Refinery and Petrochemicals limited

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Mitsui Chemicals, Inc.

- Petro Rabigh

- PTT Global Chemical Public Company Limited

- QatarEnergy

- Reliance Industries Limited

- SK Geocentric Co., Ltd.

- S-OIL CORPORATION

- TotalEnergies