|

|

市場調査レポート

商品コード

1907228

ニッケル:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Nickel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ニッケル:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

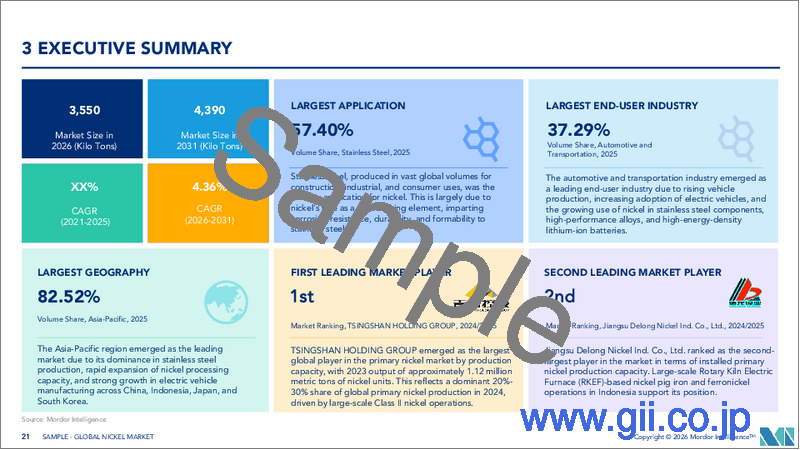

ニッケル市場は2025年に340万トンと評価され、2026年の355万トンから2031年までに439万トンに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは4.36%と見込まれます。

中国とインドネシアにおけるステンレス鋼生産の急増、電池グレード精錬への持続的な投資、低炭素サプライチェーンへの選好の高まりが数量成長を支えております。一方で、持続的なクラスIIの供給過剰が基準価格を圧迫しております。コスト優位性を持つインドネシアのニッケル銑鉄および高圧酸浸出拠点は、現在供給量の60%以上を占めており、貿易の流れを再構築するとともに、中国のステンレス鋼複合施設への垂直統合を加速させております。電池セクターの需要は依然として少数派ながら、低品位素材の過剰供給と電池用原料の不足が同時に生じる中、電気自動車用カソード供給が可能なクラスIプロジェクトへの戦略的資本配分を牽引しています。フィリピンがインドネシアの2014年鉱石輸出禁止令をモデルとした輸出規制を検討していることから政策リスクは依然として高く、深海ノジュールプロジェクトはニッケル市場における長期的な不確定要素として浮上しています。

世界のニッケル市場の動向と展望

中国とインドネシアにおけるステンレス鋼生産量の急増

中国の粗ステンレス鋼生産量は2025年第1四半期に前年比10.6%増加し、3月単月では358万トンに達しました。生産量の増加に伴い、ニッケル含有原料の輸入需要が高まっています。一方、インドネシアのニッケル銑鉄生産拡大は、製錬所を価格変動から保護する統合的な供給ルートを形成しています。この相乗効果により、ニッケル市場への原料供給が確保され、高コストの欧米鉱山が操業停止となる不況期においても、中国・インドネシア合弁事業が稼働を継続することが可能となっています。しかしながら、この集中化は政策、天候、物流などあらゆる混乱要因が世界の供給逼迫を急速に招きかねないため、システミックリスクを増幅させる要因となっています。

EV用電池グレード硫酸ニッケル精製所の急速な拡張

ヴァーレ社は2024年12月にヴォイジーズ・ベイ拡張計画を完了させ、年間4万5千トンの生産能力を追加しました。フル稼働は2026年下半期を予定しています。カナダ・ニッケル社のクロフォードプロジェクトは2027年末までに初生産を達成し、41年間の操業で160万トンの生産を見込んでいます。BASFとエラメットによる26億米ドル規模のインドネシア合弁事業は中止となりましたが、カナダと米国における新たな精錬所計画の発表は、地域のギガファクトリー向けに、現地調達可能なバッテリー対応原料をニッケル市場が求めていることを示しています。生産各社は、高水準のESG認証と炭素回収技術を組み合わせることで、潜在的な税額控除や価格プレミアムの獲得を目指しています。

持続的なクラスII供給過剰が基準価格を押し下げる

インドネシア産ニッケル銑鉄の供給量は、2018年の世界供給量の6%から2025年には50%以上に急増し、価格を押し下げ、高コストの欧米鉱山を保守・維持状態に追い込んでおります。BHP社はクウィナナ精錬所、カルグーリー製錬所、マウントキース鉱山、レインスター鉱山の操業を2027年まで停止し、約1,600名の従業員に影響が及んでおります。グレンコア社の2024年生産量9%減およびコニアムボ鉱山の操業停止は、ニッケル市場が新たなコストリーダーに適応する中で、既存資産が直面する圧力をさらに浮き彫りにしております。

セグメント分析

2025年、ステンレス鋼生産はニッケル市場の69.20%を占め、建設・消費財・産業分野における耐食性合金の基幹素材としての地位を再確認しました。中国の製鋼所は2025年初頭に生産量を10.6%増加させ、経済成長が鈍化する中でも大量需要を支えました。鋳造・合金セグメントは航空宇宙部品や耐熱部品向けに安定した(ただし減少傾向の)供給量を維持し、めっき用途は装飾仕上げで高付加価値マージンを獲得しています。

電池分野はシェアこそ小さいもの、2031年までCAGR4.96%で最も急速に拡大するセグメントです。電気自動車用パックや大規模蓄電設備の需要が牽引役となり、ヴァーレ社のヴォイジーズ・ベイ鉱山拡張やカナダ・ニッケル社の炭素回収機能付き精錬所などへの投資を促進しています。電池向けニッケル市場規模は2031年までに61万トンに達し、2024年基準値の倍増が見込まれます。LFP(リン酸鉄リチウム)電池やナトリウムイオン電池の普及が成長を抑制する一方、高級車向け高エネルギー正極材では、クラスIプレミアム価格を実現するニッケル高含有化学組成が引き続き優位性を保ちます。

本ニッケル市場レポートは、用途別(ステンレス鋼、鋳造、合金、電池、めっき、その他用途)、エンドユーザー産業別(自動車・輸送機器、金属加工製品、耐久消費財、建設、産業機械、その他エンドユーザー産業)、地域別(アジア太平洋、北米、欧州、その他)に分類されています。市場予測は数量(トン)単位で提供されます。

地域別分析

アジア太平洋地域は2025年に世界のニッケル市場需要の71.10%を占め、2031年までCAGR5.10%で拡大すると予測されています。中国のステンレス鋼需要急増とインドネシアの垂直統合型サプライチェーンが地域の成長を牽引しており、フィリピンの鉱石輸出規制の可能性がASEAN域内での加工集中をさらに促進する可能性があります。日本と韓国は高度な合金生産を維持し、インドの産業基盤が着実に消費を押し上げています。

北米では、カナダ・ニッケルのクロフォード鉱山プロジェクトやヴァーレ社のヴォイジーズ・ベイ拡張計画を筆頭に、供給の現地化に向けた取り組みが強化されています。米国におけるギガファクトリー建設計画がインフレ抑制法の調達規則に準拠したクラスI原料を必要とするため、北米のニッケル市場規模は拡大が見込まれます。メキシコは米国自動車工場への地理的近接性から物流面で優位性を有しますが、関税変動が不確実性を生んでいます。

欧州では厳格なESG基準とコスト圧力とのバランスが図られています。自動車メーカーが認証済みグリーンメタルを求める動きが、域内および隣接ノルウェーにおける低炭素精錬への投資を促進しています。ブラジルが世界の埋蔵量の約12%を保有する南米は、物流面の課題があるにもかかわらず、ブラジル・ニッケルのピアウイプロジェクトが示すように資本を集めています。中東・アフリカ地域は新興市場ながら、将来性のある鉱物への投資機会を求める湾岸投資ファンドの関心を集めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 中国とインドネシアにおけるステンレス鋼生産量の急増

- EV用電池グレード硫酸ニッケル精製所の急速な増設

- グリーンニッケルプレミアムとOEMサプライチェーンの現地化

- 全体的な供給過剰にもかかわらずクラスIニッケル不足

- 複数の新興深海ノジュールプロジェクト

- 市場抑制要因

- 持続的なクラスIIの供給過剰が基準価格を引き下げる

- LFPおよびナトリウムイオン電池化学の採用

- インドネシアのHPALおよびNPIプロジェクトに対するESG反発

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 用途別

- ステンレス鋼

- 鋳造

- 合金

- 電池

- メッキ

- その他の用途

- エンドユーザー業界別

- 自動車および輸送機器

- 金属加工製品

- 耐久消費財

- 建設

- 産業機械

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- Anglo American

- Antam

- BHP

- Canada Nickel Company

- Eramet

- Glencore

- Jinchuan Group International Resources Co., Ltd.

- Nickel Asia Corporation

- Norilsk Nickel

- PACIFIC METALS CO., LTD.

- PT Vale Indonesia

- Sherritt International Corporation

- Sibanye-Stillwater

- South32

- Sumitomo Metal Mining Co., Ltd.

- TSINGSHAN HOLDING GROUP

- Vale