|

市場調査レポート

商品コード

1906897

産業用モノのインターネット(IIoT):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Industrial Internet Of Things (IIoT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用モノのインターネット(IIoT):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

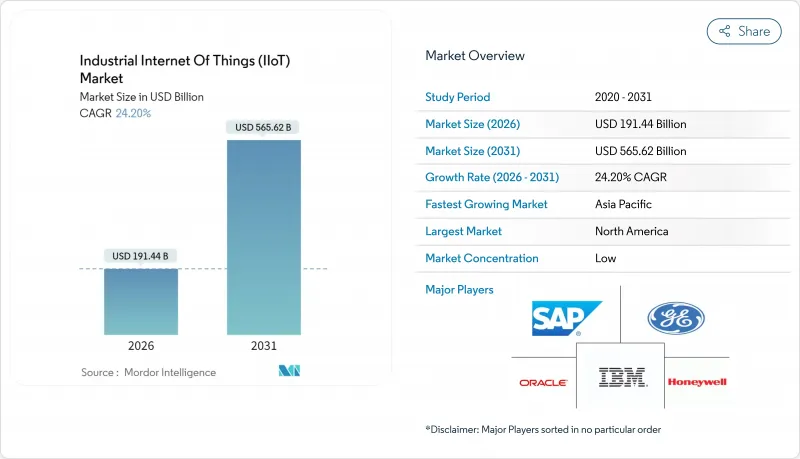

産業用モノのインターネット(IIoT)市場は、2025年の1,541億4,000万米ドルから2026年には1,914億4,000万米ドルへ成長し、2026年から2031年にかけてCAGR24.2%で推移し、2031年までに5,656億2,000万米ドルに達すると予測されています。

この成長軌道は、センサー価格の急激な低下、プライベート5Gの広範な展開、および運用現場でのリアルタイム分析を可能にするチップレットベースのエッジAI設計を反映しています。製造業者は、反応型から予知保全への移行、総合設備効率(OEE)の向上、サプライチェーンの衝撃緩和を目的として、導入を加速しています。フリート全体の分析にはクラウドリソースが依然として重要ですが、遅延に敏感な制御ループにはハイブリッドエッジクラウドアーキテクチャが好まれています。競合環境においては、成果ベースのサービスモデルが標準化するにつれ、運用技術ベンダーとクラウドハイパースケーラー間の連携強化が明らかになっています。

世界の産業用モノのインターネット(IIoT)市場の動向と洞察

高度なセンサーの統合とデバイスコストの低下

ユニットレベルのセンサー価格は低下を続けており、一方、組み込みプロセッサにはニューラルアクセラレーション機能が追加され、STマイクロエレクトロニクスのSTM32N6 MCUのように、ディスクリートアクセラレータなしでオンサイト推論を実行できるAI対応デバイスが可能となっています。製造業者は、特に既存プラントにおいて、システム全体の交換ではなく、非侵襲型センサーでレガシー資産を網羅するようになりました。LoRaWANなどの低電力広域通信オプションにより遠隔資産へのカバレッジが拡大し、スマートセンサーの自己診断機能によりライフタイムイベントログが分析ハブへ集約されます。可視性の向上は投資対効果の強化を促し、改修コストにより停滞していたプロジェクトを加速させます。その結果、産業用IoT市場はコスト意識の高い中堅工場において、より広範な潜在顧客基盤を獲得しています。

予知保全とOEE改善の推進

運用責任者は計画外のダウンタイムを戦略的リスクと捉えています。継続的な状態データは機械学習モデルを強化し、数週間前から異常を検知することで、予定外の停止を二桁パーセント削減します。振動・熱・音響の特性を基に、保守チームは優先順位付けされた作業に集中でき、限られた労働力を高付加価値業務に振り向けられます。デジタルツインによるオーバーレイは複数ラインにわたるサービスシナリオをシミュレートし、予備部品の在庫管理や技術者の派遣を最適化します。プロセス産業では、1回の停止回避が数百万米ドルの生産量損失を防止するため、資本支出の抑制が求められる中でも予測システムに優先予算が割り当てられる理由がここにあります。

OTサイバーセキュリティとレガシーシステムの脆弱性

インターネット以前の産業制御機器が現在、統合ネットワーク上に存在し、攻撃対象領域を拡大しています。機器のライフサイクル延長により、パッチが提供されないままPLCが脆弱な状態に晒されるケースも生じています。部門が未検証のIoTノードを設置し、中央セキュリティ管理を迂回する「シャドーOT」を構築する事例も見受けられます。ローコード開発プラットフォームはアプリケーション展開を加速しますが、ガバナンスがなければ不安全なコードが拡散する恐れがあります。運用担当者は生産性向上とサイバーリスクを天秤にかけ、多層防御とゼロトラストフレームワークが整備されるまで、インターネット接続型アップグレードを遅らせるケースが少なくありません。

セグメント分析

2025年時点で産業用IoT市場シェアの46.15%をハードウェアが占め、センサー、ゲートウェイ、産業用PCが中核を形成しています。センサーとアクチュエーターは状態監視の基盤を構成し、エッジゲートウェイはテレメトリを前処理して帯域幅を管理します。しかしながら、サービスと接続性は25.12%のCAGRを記録しており、統合上の課題が調達決定を再構築している実態を浮き彫りにしています。プロフェッショナルサービスチームは既存設備を最新プロトコルに改修し、管理型サービスは社内にOT-IT人材を欠く中堅工場を引き付けています。

実際のところ、ハードウェアベンダーはデバイス管理ポータルや遠隔監視サブスクリプションをバンドルする傾向が強まり、製品とサービスの境界が曖昧になりつつあります。システムインテグレーターは、かつて導入したインフラの運用から継続的な収益を得ています。ローコードダッシュボードが主流となる中、運用チームはコーディングなしでカスタム可視化を構築できるようになり、企業IT部門への依存度が低下しています。こうした背景から、産業用IoT市場は単発の設備投資ではなく、ライフサイクルを通じたパートナーシップへと移行しつつあります。

クラウドプラットフォームは、初期コストを抑えた弾力的な分析機能を提供することで、2025年の産業用IoT市場規模の52.91%を占めました。しかしながら、純粋なクラウド環境では10ミリ秒未満の制御要件を満たせません。このため、ハイブリッド型エッジクラウド展開がCAGR25.28%で拡大しています。製造業者は振動スペクトルやマシンビジョンのフレームを現地で処理し、集約された知見をクラウドに転送することで、設備群全体の最適化を実現しています。

プライベート5Gバックボーンは、確定的で低遅延のアップリンクを提供することで、この融合を加速します。コンテナ化されたマイクロサービスにより、エンジニアはコンピューティング連続体の任意の場所にAIモジュールを配置でき、製薬や防衛分野のデータ主権ルールに準拠します。オンプレミス専用モデルは規制の厳しいニッチ分野で存続しますが、産業用IoT市場における次世代展開では、ハイブリッドアーキテクチャが標準となる見込みです。

地域別分析

北米が2025年に38.36%のシェアを占める背景には、先進的な製造基盤、強力なベンチャー資金調達、プライベート5Gパイロットの早期導入があります。国内回帰とレジリエンスを促進する連邦プログラムは、国内サプライチェーン全体の可視化需要を拡大しています。規制枠組み、特にFDAのプロセス監視規則は、ライフサイエンス工場におけるリアルタイム品質記録を推進しています。

アジア太平洋地域は24.98%のCAGRで成長し、世界最大の電子機器生産クラスターと初期導入コストを低減する政府補助金から恩恵を受けています。中国の一線都市は大規模スマート工場を主導し、インドのテクノロジーセンターは近隣のASEAN輸出国へ低コスト統合サービスを拡大しています。越境部品取引は相互運用可能なソリューションを促進し、産業用IoT市場をさらに拡大させます。

欧州では厳格なデータプライバシー法と持続可能性指令のバランスが取られています。GDPRはアーキテクチャをローカルエッジ処理へ導き、2050年カーボンニュートラル目標は詳細なエネルギー計測を義務付けています。ドイツの自動車大手はIT-OT基盤統合のためOPC UA over TSNを採用し、欧州経済領域全体で複製される参照モデルを提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高度なセンサーの統合とデバイスコストの低下

- 予知保全とOEE改善の推進

- 政府主導のスマート製造イニシアチブ

- 重工業向けプライベート5Gキャンパスネットワーク

- ESGに基づくエネルギー消費量ベンチマーク

- チップレットベースの産業用エッジAIアクセラレータ

- 市場抑制要因

- OTサイバーセキュリティとレガシーシステムの脆弱性

- クロスベンダー相互運用性基準の不足

- 既存システム向けデジタルツイン人材の不足

- ローコードIoTアプリケーションによるシャドーITリスクの高まり

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 投資と資金調達分析

第5章 市場規模と成長予測

- コンポーネント別

- ハードウェア

- センサーおよびアクチュエーター

- エッジゲートウェイおよび産業用PC

- 産業用ロボットおよびコントローラー

- ソフトウェア

- デバイス管理プラットフォーム

- 分析と可視化

- MES/SCADAおよびデジタルツインソフトウェア

- サービスと接続性

- プロフェッショナルおよび統合

- マネージドサービス

- 接続サービス(移動体通信事業者、LPWAN、衛星通信)

- ハードウェア

- 展開モデル別

- オンプレミス

- クラウド

- ハイブリッド/エッジクラウド

- コネクティビティテクノロジー別

- 有線(イーサネット、PROFINET、Modbus-TCP)

- 短距離無線通信(BLE、Wi-Fi 6/6E)

- セルラー通信(4G LTE-M、プライベート5G)

- LPWAN(LoRa WAN、Sigfox、NB-IoT)

- エンドユーザー業界別

- 個別生産

- プロセス製造業

- 石油・ガス

- 公益事業(電力、水道)

- 運輸・物流

- 鉱業・金属

- 医療・医薬品

- その他のエンドユーザー業種

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amazon Web Services Inc.

- Telefonaktiebolaget LM Ericsson

- Fujitsu Ltd.

- Mitsubishi Electric Corporation

- SAP SE

- Siemens AG

- Honeywell International Inc.

- Emerson Electric Co.

- OMRON Corporation

- International Business Machines Corporation

- Robert Bosch GmbH

- Oracle Corporation

- PTC Inc.

- Telit IoT Platforms Limited

- NXP Semiconductors N.V.

- Cisco Systems Inc.

- Infineon Technologies AG

- Rockwell Automation Inc.

- Advantech Co. Ltd.

- Schneider Electric SE

- ABB Ltd.

- Hitachi Ltd.

- General Electric Company

- Intel Corporation

- Arm Ltd.