|

市場調査レポート

商品コード

1939163

ウェアラブルテクノロジー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Wearable Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ウェアラブルテクノロジー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 161 Pages

納期: 2~3営業日

|

概要

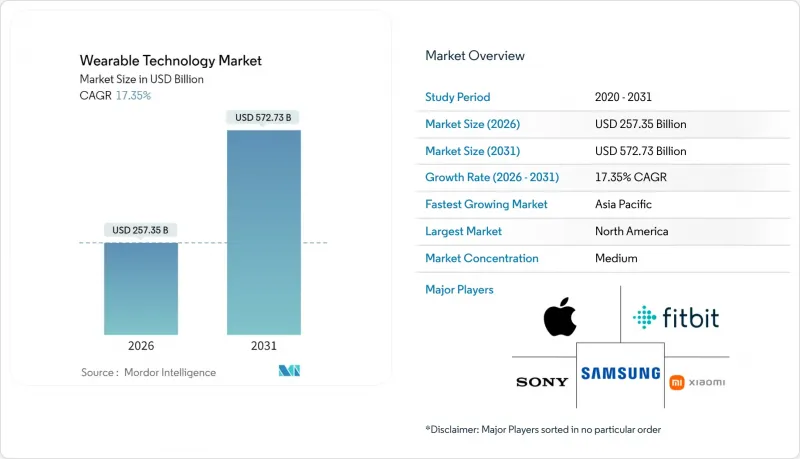

ウェアラブルテクノロジー市場は、2025年の2,193億米ドルから2026年には2,573億5,000万米ドルへ成長し、2026年から2031年にかけてCAGR17.35%で推移し、2031年までに5,727億3,000万米ドルに達すると予測されています。

これは同セクターの急速な規模拡大と、センサーを豊富に搭載した接続デバイスの商業的実現可能性を裏付けるものです。この勢いは、AI搭載医療用ウェアラブル機器のFDA認可、拡張現実ヘッドセットへの企業支出、長年の電力密度制約を緩和する固体電池のブレークスルーに起因しています。北米が最大の収益源を占めておりますが、部品製造の現地化や政府による医療提供のデジタル化が進むアジア太平洋地域が最も急速に拡大しております。デバイス分野ではスマートウォッチが主導的地位を維持しておりますが、最前線での従事者への導入を背景に、ヘッドマウントディスプレイの普及率が最も急激に伸びております。競合はハードウェアの差別化からエコシステム支配へと移行しており、チップ、ソフトウェア、サービスを最も緊密に統合する企業が、価値の過半数を獲得しております。

世界のウェアラブルテクノロジー市場の動向と洞察

AI搭載臨床グレードセンサー

規制当局はAI駆動型バイオセンサーの承認を迅速化しており、ウェアラブルを予防医療における意思決定支援ツールとして位置付けています。FDAのデジタルヘルスセンター・オブ・エクセレンスは審査プロセスを効率化し、トリニティ・バイオテックなどの革新企業は代謝データと予測分析を融合した持続血糖モニターを発売しました。韓国科学技術院(KAIST)や香港大学の学術グループは、カフレス血圧測定モジュールや有機トランジスタアレイの商用化を進めています。これらはデータをローカルで処理するため、遅延を低減しプライバシーを保護します。こうした進歩により、消費者向けフィットネス機器と臨床診断機器の差が縮まり、保険者も遠隔モニタリングサービスの償還に自信を持てるようになりました。病院は、この技術を早期介入とコスト回避の手段と捉えており、ウェアラブルテクノロジー市場の潜在顧客基盤をさらに拡大しています。

現場作業員向けエンタープライズAR

産業用拡張現実(AR)ヘッドセットは、危険な環境や分散型環境における効率性を向上させます。コルゲート・パルモリーブ社は63件の仮想コラボレーションを実施し、出張費とダウンタイムを削減。シェル社は12カ国で本質安全防爆型ARウェアラブルを導入し、爆発危険区域でのメンテナンスを支援しました。富士通はARガイダンス導入により組立作業を19%削減。鉄鋼メーカーKSP社はヘルメット装着型可視化技術で生産性を40%向上させました。投資回収期間は1年未満となることが多く、運用チームによる導入判断を容易にしております。遠隔専門家アプリケーションの拡大に伴い、企業は規模を伴った発注を進めており、ウェアラブルテクノロジー市場の成長を後押ししております。

データプライバシーコンプライアンスの負担

ウェアラブル端末は生体認証データを収集するため、GDPRやイリノイ州BIPAなどの厳格な規制の対象となります。メーカーは同意管理機能や端末内匿名化技術を組み込む必要があり、開発コストの増加や発売スケジュールの遅延を招いています。国境を越えたデータ転送の制限は、クラウド分析をさらに複雑化させています。法的リソースが不足する小規模ベンダーはコンプライアンスコストの障壁が高く、新規参入率を抑制し、ウェアラブルテクノロジー市場の成長を鈍化させています。

セグメント分析

ヘッドマウントディスプレイは2026年から2031年にかけて19.02%という最速のCAGRを記録しましたが、2025年時点ではスマートウォッチがウェアラブルテクノロジー市場シェアの45.60%という最大の割合を維持しました。この勢いは、企業がメンテナンス、トレーニング、物流管理にハンズフリーディスプレイを導入するにつれ、ウェアラブルテクノロジー市場全体を押し上げています。Metaは2023年後半から200万台のRay-Banスマートグラスを販売し、年間1,000万台まで規模を拡大しており、目立たないアイウェアに対する消費者の需要を裏付けています。GoogleがWarby Parkerと1億5,000万米ドルで提携し、スタイルの選択肢を拡大することで、ファッション面での導入障壁が低くなっています。

多様化はイヤウェアラブルにも見られ、Appleの特許は、手首装着型デバイスへの依存度を低減できるインイヤー型健康診断装置を示唆しています。スマート衣類はまだ発展段階ですが、ジョンズ・ホプキンズ大学のファイバー電池は、電子繊維を主流にする可能性のある、洗濯可能なエネルギー貯蔵装置を示唆しています。スマートウォッチの平均販売価格が下落する中、リストバンドはコモディティ化のリスクに直面していますが、神経入力バンドはAR制御のニッチな需要を維持しています。これらの変化が相まって、ウェアラブルテクノロジー市場はさらに充実したものとなっています。

第2世代のスマートグラスには、携帯電話の無線機能とマイクロLEDディスプレイが統合されており、携帯電話に接続することなく、通知の優先順位付け、ナビゲーションのオーバーレイ、リアルタイムの翻訳が可能になります。OEMは、対象ユーザー層を拡大するために、軽量化と処方レンズのサポートに注力しています。このカテゴリーの急速な規模拡大により、デバイスの多様性は高く維持され、ウェアラブルテクノロジー市場は成長を続けていくでしょう。

2025年時点のウェアラブルテクノロジー市場規模において、センサーが最大の28.70%を占めました。これはマルチモーダルデータストリームへの需要を反映しています。同時に、固体電池は19.85%のCAGRで全コンポーネントを上回る成長が見込まれ、高度な使用事例を支えるエネルギー基盤を提供します。TDKのチップスケール電池やサムスンの1週間持続型プロトタイプは、より安全な化学組成が薄型筐体の実現を可能にする好例です。プロセッサとメモリは3D積層技術の波に乗り、TSMCはCPU、GPU、メモリを単一基板に統合するパネルレベルパッケージングを計画しています。

ディスプレイはフレキシブルOLEDやマイクロLED形式へ移行し、曲面や透明表面を実現することでアイウェアとの融合を可能にします。接続用ICはBluetooth、Wi-Fi、UWBを共封装し、基板レイアウトの簡素化とアンテナ設置面積の縮小を図ります。ソフトウェアとサービスは最高利益率の層であり、プラットフォーム所有者はサブスクリプションによる機能制限を強化することでエコシステムを固め、乗り換えコストを高めています。したがって、ウェアラブルテクノロジー市場では利益率と販売数量の両方が拡大を続けています。

地域別分析

北米は2025年の収益の31.70%を占め、研究開発の主導権、ベンチャー資金の厚み、有利な償還政策を反映しています。FDAは2023年に124の新規デバイスを承認し、年間最多記録を更新、商品化までの期間を短縮しました。米国多国籍企業による企業向けARパイロット事業は、ハードウェアの更新サイクルを安定させる一因となっています。しかしながら、高い離脱率は、消費者導入と価値提供における継続的な課題を示しています。

アジア太平洋地域は2026年から2031年にかけてCAGR20.25%で拡大し、ウェアラブルテクノロジー市場の主要な数量牽引役となる見込みです。中国のデジタルヘルス政策支援と韓国の3nmファウンドリ・固体電池分野におけるリーダーシップが、地域のサプライチェーン自立化を加速させております。インドの健康意識の高い中産階級と日本の高齢化人口が需要曲線をさらに押し上げております。TSMCのアリゾナ州および熊本県における新工場は耐障害性を高めつつ、主要プロセスノウハウを地域内に留保しております。

欧州では厳格なプライバシー・持続可能性規制と、強力な産業自動化需要が均衡しています。GDPRやWEEE指令はコンプライアンス負担を増大させますが、強固なガバナンスを有するベンダーには競争上の優位性も生み出します。ドイツのスマートファクトリー計画や英国の国民保健サービス(NHS)による遠隔モニタリング試験運用は、安定した企業向けパイプラインを提供します。中東・アフリカ・南米の小規模市場はインフラと可処分所得で遅れを取っていますが、接続コストの低下と現地アプリエコシステムの成熟に伴い、オプション価値を有しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- AI搭載の臨床グレードセンサー

- 現場従業員向けエンタープライズAR

- 医療用ウェアラブル機器の保険適用範囲拡大

- エッジAIおよび低消費電力チップセット

- 固体マイクロ電池

- 没入型ゲームおよびeスポーツの需要

- 市場抑制要因

- データプライバシーコンプライアンスの負担

- 高度なパッケージングの供給ボトルネック

- 電子廃棄物と持続可能性への圧力

- ユーザーの疲労感/デバイスの放棄

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- デバイスタイプ別

- スマートウォッチ

- 耳装着型デバイス

- ヘッドマウントディスプレイ

- スマート衣類

- リストバンド

- コンポーネント別

- プロセッサおよびメモリ

- センサー

- ディスプレイ

- バッテリー

- 接続用集積回路(コネクティビティIC)

- ソフトウェアおよびサービス

- コネクティビティテクノロジー別

- BluetoothおよびBLE

- セルラー(LTE/5G)

- Wi-Fi

- NFCおよびUWB

- 衛星通信およびLP-WAN

- エンドユーザー業界別

- 民生用電子機器

- 医療・ヘルスケア

- 産業・企業

- 防衛・公共安全

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他のアジア

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Alphabet Inc.(Google LLC)

- Meta Platforms, Inc.(Oculus)

- Sony Group Corporation

- Xiaomi Corporation

- Huawei Technologies Co., Ltd.

- Garmin Ltd.

- Fitbit LLC(Google)

- Microsoft Corporation

- HTC Corporation

- BOE Technology Group Co., Ltd.

- Qualcomm Technologies, Inc.

- Corning Incorporated

- Valencell, Inc.

- Zepp Health Corporation

- Fossil Group, Inc.

- Vuzix Corporation

- Magic Leap, Inc.

- Mobvoi Information Technology Co. Ltd.