|

市場調査レポート

商品コード

1686665

産業用モーター:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Industrial Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用モーター:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

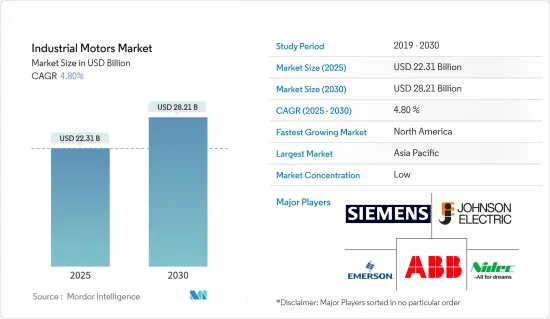

産業用モーター市場規模は2025年に223億1,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは4.8%で、2030年には282億1,000万米ドルに達すると予測されます。

産業用モーターは、電気エネルギーを機械エネルギーに変換し、産業環境でさまざまなタスクを実行する電気機械です。産業用モーターは、製造、石油・ガス、建設、輸送などで使用されるさまざまな機器や機械に動力と運動を提供するように設計されています。これらのモーターは通常、住宅や商業用アプリケーションで使用されるモーターよりも頑丈で強力であり、高負荷に耐え、厳しい環境で動作する必要があるためです。

主なハイライト

- モーターは工業生産の原動力モータの監視、調整、試験、接続における革新的な方法は、時間とコストを節約し、安全性を高める。同時に、省エネモーターとインテリジェント・ドライブが効率と性能を高め、トラブルシューティングを簡素化します。

- 世界のエネルギー効率と持続可能性の推進に伴い、メーカーはエネルギー効率の高いモーターを選択するようになっています。これらの選択は、エネルギー消費と運転コストの削減を目的としており、IE4効率モーターは、旧モデルよりも大幅にエネルギーを節約できる点で際立っています。

- 世界の工業化により、エネルギー効率の高いモーターへの需要が高まっています。産業が確立し拡大するにつれて、エネルギー消費と運転コストを削減するモータの必要性が最も重要になります。こうしたエネルギー効率の高いモーターは効率を高め、エネルギー損失を最小限に抑えるため、長期にわたって顕著なコスト削減につながります。この需要の高まりは、製造業、農業、建設業、運輸業など、さまざまな分野に及んでいます。

- オートメーション・システムは、製造、エンジニアリング、建設、発電にとって極めて重要であり、効率と生産性の向上を推進しています。産業オートメーションは、人工知能(AI)、クラウド・コンピューティング、ビッグデータ、モノのインターネット(IoT)に後押しされ、急速な進歩を遂げています。

- このような利点があるにもかかわらず、エネルギー効率の高いモーターの普及を妨げている課題がいくつかあります。基本的な制約には、エネルギー、メンテナンス、初期購入といった関連コストが含まれます。さらに、エネルギー効率の高いモーターを製造するには、優れた材料、高度な製造技術、厳格な試験と認証が必要です。これらの要件は、メーカーの製造コストを押し上げ、消費者価格の上昇につながる可能性があります。

産業用モーター市場の動向

石油・ガス部門が成長する見込み

- 石油・ガス部門は、掘削、採掘、精製、輸送など、さまざまなプロセスに電力を供給する産業用モーターの必要性から、現在市場をリードしています。気候変動に対する意識の高まりとCO2排出量削減の必要性から、石油・ガス業界はエネルギー効率の高いモーターの重要性を認識しつつあります。

- ポンプ、コンプレッサ、タービンにAC誘導モータが多用されているほか、石油・ガスの採掘、処理、採掘現場から精製所への輸送に応用され、消費者に販売されているため、石油・ガス業界ではこれらのモータが流行すると推定されます。さらに、低電圧誘導モータは、原油をガソリン、ディーゼル、ジェット燃料などの複数の製品に変換するためのポンプ、コンプレッサ、攪拌機の駆動用として製油所で使用されています。

- 開発途上国における急速な都市化は、エネルギー需要の大幅な増加を伴います。その結果、液体燃料や天然ガスの消費量が増加します。例えばBP社によると、2023年の天然ガス生産量は4兆800億立方メートルに達します。電力と燃料に対する世界のニーズの高まりが、石油・天然ガスの需要を増大させています。

- 石油・ガス需要の増加に伴い、E&P機械・装置・部品の市場も拡大しています。その結果、石油・ガス産業の下流および上流セグメントでさまざまな容量に使用されるACモーターのニーズも増加しています。

- Baker Hughes社によると、北米は世界的に石油・ガスのリグを受け入れています。2024年8月現在、この地域には781基の陸上リグと23基の海上リグがあります。2023年には、世界の石油リグ数は平均1,800基を突破しました。

北米が大きな市場シェアを占める見込み

- 産業用モーター市場は主に、米国内でインダストリー4.0に注力する産業が増加していることが要因となっています。産業オートメーションは、メーカーがより効果的な製品を生産することを促し、予測期間を通じて堅調な成長が見込まれます。このようなパターンにより、新しい産業用モーター機械の開発が望まれることになります。産業オートメーションのあらゆる分野への普及は、均等になると予想されます。その結果、産業オートメーションの成長に対応するため、産業用モーター市場は米国で発展すると予測されます。

- 産業界や消費者がエネルギー消費を削減し、二酸化炭素排出量を最小限に抑えようとする中、エネルギー効率の高いソリューションに対する需要が高まっています。産業用電気モーターは、従来のモーターよりも高効率でエネルギー損失が少ないことで知られています。

- 石油・ガスは、掘削装置を使って貯留層から原油や天然ガスを抽出する掘削作業を行う産業です。電気モーターは、掘削装置の一般的な動力源です。ベーカー・ヒューズ社によると、北米は石油・ガス掘削装置の保有で世界をリードしています。2024年8月現在、この地域には781基の陸上リグがあり、さらに23基の海上リグがあります。2023年末までに、米国では500基の石油・ガス用ロータリー・リグと120基のガス用ロータリー・リグが稼動しており、合計622基のロータリー・リグが稼動しています。

- カナダはエネルギー効率規制を実施し、非効率なモーターを市場から排除しています。NEMA MG-1が提供するモータ効率のガイドラインは、この性能基準を通じてカナダの企業が利用できます。これらの規制は、出力が1~500馬力の三相誘導モータを対象としています。これらの性能基準は、製造および産業用途で使用されるほとんどのモータを対象としています。これらのエネルギー基準の遵守は、事業主にとって必須です。

- カナダ政府は、カナダの製造業を育成するために、新規投資に対する減税、さまざまな国との貿易協定、新技術への投資、多くの技能訓練プログラムなど、いくつかのイニシアチブをとってきました。カナダ政府はまた、地元企業や起業家が成功に必要な手段を確保できるよう、投資も行ってきました。

- 例えば、2024年7月、日立エナジーカナダはカナダ政府から3,000万カナダドル(2,154万米ドル)の資金を確保しました。この資金は、モントリオールに新しいHVDCシミュレーションセンターを設立し、ヴァレンヌにある電力変圧器工場を近代化するのに役立てられます。これらの取り組みは、持続可能なエネルギーに対する北米の急増する需要を満たすことを目的としています。

産業用モーター市場の概要

競合の度合いは、ブランド・アイデンティティ、強力な競争戦略、透明性の度合いなど、市場に影響を与える様々な要因によって決まる。

産業用モーター市場には、ABB社、Emerson Electric Co.社、Nidec Industrial Solutions社、Johnson Electric Holdings Limited社、Siemens AG社など、様々な著名企業が参入しています。この市場では、各社のブランド・アイデンティティが大きな影響力を持っています。強力なブランドは好業績の代名詞であるため、老舗企業が優位に立つと予想されます。

イノベーションによる持続可能な競争優位性がかなり高い市場では、鉱業、石油・ガス、エネルギーといったエンドユーザー業界の新規顧客からの需要急増が予想されることから、競合は激化する一方です。大規模な既存企業の存在により、市場浸透度も高いです。

市場への浸透度と高度な製品を提供する能力により、競争企業間の敵対関係は今後も高水準で推移すると予想されます。市場は様々な企業で構成されているが、その高い水準と優れた品質で市場で突出しているのはほんの一握りです。

統合技術の進歩や地政学的シナリオの拡大に伴い、調査された市場は変動を目の当たりにしています。これに加えて、主要な業界企業は、彼らの収入から生じる投資能力を考慮し、原料ベンダーのための彼らの関連会社に依存しています。

技術革新のレベル、市場投入までの時間、業績は、調査した市場において企業が自らを差別化する重要な条件です。

全体として、調査市場間の競争企業間の敵対関係は激化しており、業界の成長により予測期間中も高水準になると予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 政府規制によるエネルギー効率化需要

- スマートモーターへのシフトの高まり

- 市場の課題

- 可搬性の問題

- 新しい機器の購入と既存機器のアップグレードのための高額な初期投資

第6章 市場セグメンテーション

- モータータイプ別

- 交流(AC)モーター

- 直流(DC)モーター

- その他のモーター(サーボモーターと電子整流モーター(ECモーター))

- 電圧別

- 高電圧

- 中電圧

- 低電圧

- エンドユーザー別

- 石油・ガス

- 発電

- 鉱業・金属

- 上下水道管理

- 化学・石油化学

- ディスクリート製造

- その他のエンドユーザー

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- ABB Ltd.

- Emerson Electric Co.

- Siemens AG

- Nidec Industrial Solutions

- Johnson Electric Holdings Limited

- Arc Systems Inc.

- Ametek Inc.

- Toshiba Electronic Devices and Storage Corporation

- Wolong Industrial Motors

- Allen-Bradly Co. LLC(Rockwell Automation Inc.)

- Maxon Motor AG

- Franklin Electric Co. Inc.

- Fuji Electric Co. Ltd

- ATB Austria Antriebstechnik AG

- Menzel Elektromotoren GmbH

第8章 投資分析

第9章 市場の将来

The Industrial Motors Market size is estimated at USD 22.31 billion in 2025, and is expected to reach USD 28.21 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

An industrial motor is an electrical machine that converts electrical energy into mechanical energy to perform various tasks in industrial settings. Industrial motors are designed to provide power and motion to different equipment and machinery used in manufacturing, oil and gas, construction, transportation, etc. These motors are typically more robust and powerful than motors used in residential or commercial applications, as they need to withstand heavy loads and operate in demanding environments.

Key Highlights

- Motors drive industrial production. Innovative methods in motor monitoring, alignment, testing, and connections save time and costs and enhance safety. Concurrently, energy-saving motors and intelligent drives elevate efficiency and performance and simplify troubleshooting.

- With a global push towards energy efficiency and sustainability, manufacturers are increasingly opting for energy-efficient motors. These choices aim to reduce energy consumption and operating costs, with IE4 efficiency motors standing out for their significant energy savings over older models.

- Global industrialization has heightened the demand for energy-efficient motors. As industries establish and expand, the need for motors that curtail energy consumption and operating costs becomes paramount. These energy-efficient motors enhance efficiency and minimize energy loss, leading to notable cost savings over time. This growing demand spans multiple sectors, including manufacturing, agriculture, construction, and transportation.

- Automation systems are pivotal for manufacturing, engineering, construction, and power generation, driving enhanced efficiency and productivity. Industrial automation is witnessing rapid advancements fueled by artificial intelligence (AI), cloud computing, Big Data, and the Internet of Things (IoT).

- Despite the advantages, several challenges hinder the widespread adoption of energy-efficient motors. Fundamental limitations include the associated costs: energy, maintenance, and initial purchase. Furthermore, producing energy-efficient motors demands superior materials, advanced manufacturing techniques, and rigorous testing and certification. These requirements can inflate production costs for manufacturers, leading to higher consumer prices.

Industrial Motors Market Trends

The Oil and Gas Segment is Expected to Witness Growth

- The oil and gas sector is currently leading the market due to its need for industrial motors to power a range of processes, including drilling, extraction, refining, and transportation. Due to increasing awareness of climate change and the necessity of decreasing CO2 emissions, the oil and gas industry is progressively acknowledging the significance of energy-efficient motors.

- Due to the significant use of AC induction motors in pumps, compressors, and turbines, as well as their application for extraction, processing, and transport of oil and gas from drilling sites into refineries, which are sold to consumers, it is estimated that these motors will be trendy within the oil and gas industry. In addition, low-voltage induction motors are used in refineries for drive pumps, compressors, and agitators to convert crude oil into multiple products such as gasoline, diesel, and jet fuel.

- Rapid urbanization in developing nations accompanies a considerable increase in energy demand. Consequently, the consumption of liquid fuels and natural gas rises. For instance, according to BP, natural gas production amounted to 4.08 trillion cubic meters in 2023. The escalating global need for electricity and fuel has increased the demand for oil and natural gas.

- With rising oil and gas demand, the market for E&P machines, equipment, and components is growing. As a result, the need for AC motors used in different capacities within the downstream and upstream segments of the oil and gas industry is also increasing.

- According to Baker Hughes, North America hosts oil and gas rigs globally. As of August 2024, the region boasted 781 land rigs and 23 offshore rigs. In 2023, the global count of oil rigs surpassed 1,800 units on average.

North America is Expected to Hold Significant Market Share

- Industrial motor markets are mainly driven by the increasing focus of industries on Industry 4.0 within the United States. Industrial automation encourages manufacturers to produce more effective products, with solid growth expected throughout the projection period. This pattern would result in a desire to develop new industrial motor machines. The spread of industrial automation across all sectors is expected to be evenly distributed. Consequently, to cope with industrial automation's growth, the market for industrial motors is predicted to develop in the United States.

- As industries and consumers seek to reduce energy consumption and minimize their carbon footprint, there is a growing demand for energy-efficient solutions. Industrial electric motors are known for their higher efficiency and lower energy losses than traditional motors.

- Oil and gas is an industry in which drilling operations are carried out to extract crude oil and natural gas from reservoirs using drilling rigs. Electric motors are a common source of power for drilling equipment. According to Baker Hughes, North America leads the world in hosting oil and gas rigs. As of August 2024, the region boasted 781 land rigs and an additional 23 offshore. By the end of 2023, the United States had 500 active rotary oil rigs and 120 gas rigs, contributing to a total rotary rig count of 622.

- Canada has implemented energy efficiency regulations to remove inefficient motors from the market. The guidelines for motor efficiency, provided by NEMA MG-1, are available to Canada's businesses through these performance standards. These regulations cover three-phase induction motors with power between 1 and 500 horsepower. These performance standards cover most motors used in manufacturing and industrial applications. Compliance with these energy standards is mandatory for business owners.

- The Government has taken several initiatives to foster Canada's manufacturing sector, including tax reductions on new investments, various trade agreements with different countries, investment in new technologies, and many skill training programs. The Canadian Government has also invested in local companies and entrepreneurs to ensure they have the tools necessary for success.

- For instance, in July 2024, Hitachi Energy Canada secured CAD 30 million (USD 21.54 million) in funding from the Government of Canada. This funding will help set up a new HVDC simulation center in Montreal and modernize the power transformer factory in Varennes. These initiatives aim to meet North America's surging demand for sustainable energy.

Industrial Motors Market Overview

The degree of competition depends on various factors affecting the market, such as brand identity, powerful competitive strategy, and degree of transparency.

The industrial motors market comprises various prominent players such as ABB Ltd., Emerson Electric Co., Nidec Industrial Solutions, Johnson Electric Holdings Limited, and Siemens AG, among others. The brand identity associated with the companies has a major influence in this market. As strong brands are synonymous with good performance, long-standing players are expected to have the upper hand.

In a market where the sustainable competitive advantage through innovation is considerably high, the competition is only going to increase, considering the anticipated surge in demand from new customers from the end-user industries like mining, oil and gas, energy. With the presence of large market incumbents, market penetration levels are also high

Owing to their market penetration and the ability to offer advanced products, the competitive rivalry is expected to continue to be high. Although the market comprises various players, only a handful are prominent in the market for their high standards and excellent quality.

With the growing consolidation technological advancement, and geopolitical scenarios, the studied market has been witnessing fluctuation. In addition to this, the major industry player depends on their affiliates for raw materials vendors, considering their ability to invest, which result from their revenues.

The level of innovation, time-to-market, and performance are the key terms by which the players differentiate themselves in the market studied.

Overall, the intensity of the competitive rivalry in the studied market is growing and expected to be high during the forecast period owing to the growth of the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Energy Efficiency Owing to Government Regulations

- 5.1.2 Growing Shift towards Smart Motors

- 5.2 Market Challenges

- 5.2.1 Portability Issues

- 5.2.2 High Initial Investment for Procuring New Equipment and Upgrading Existing Equipment

6 MARKET SEGMENTATION

- 6.1 By Type of Motor

- 6.1.1 Alternating Current (AC) Motors

- 6.1.2 Direct Current (DC) Motor

- 6.1.3 Other Types of Motors (Servo and Electronically Commutated Motors (EC))

- 6.2 By Voltage

- 6.2.1 High Voltage

- 6.2.2 Medium Voltage

- 6.2.3 Low Voltage

- 6.3 By End User

- 6.3.1 Oil & Gas

- 6.3.2 Power Generation

- 6.3.3 Mining & Metals

- 6.3.4 Water & Wastewater Management

- 6.3.5 Chemicals & Petrochemicals

- 6.3.6 Discrete Manufacturing

- 6.3.7 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd.

- 7.1.2 Emerson Electric Co.

- 7.1.3 Siemens AG

- 7.1.4 Nidec Industrial Solutions

- 7.1.5 Johnson Electric Holdings Limited

- 7.1.6 Arc Systems Inc.

- 7.1.7 Ametek Inc.

- 7.1.8 Toshiba Electronic Devices and Storage Corporation

- 7.1.9 Wolong Industrial Motors

- 7.1.10 Allen - Bradly Co. LLC (Rockwell Automation Inc.)

- 7.1.11 Maxon Motor AG

- 7.1.12 Franklin Electric Co. Inc.

- 7.1.13 Fuji Electric Co. Ltd

- 7.1.14 ATB Austria Antriebstechnik AG

- 7.1.15 Menzel Elektromotoren GmbH