|

市場調査レポート

商品コード

1639390

ボトルウォーターパッケージング:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Bottled Water Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ボトルウォーターパッケージング:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

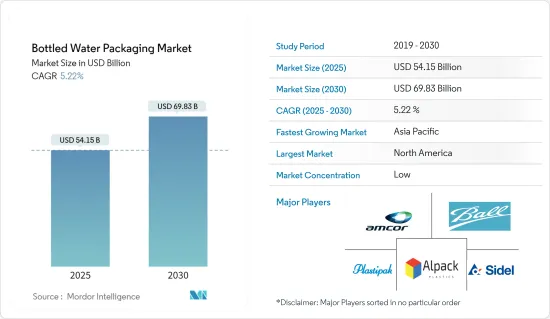

ボトルウォーターパッケージング市場規模は2025年に541億5,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは5.22%で、2030年には698億3,000万米ドルに達すると予測されます。

包装水業界、ひいてはボトルウォーターパッケージング業界は、清潔な飲料水の重要性に対する人々の意識が高まるにつれて急成長しています。さらに、ボトルの製造にリサイクル可能なポリマーを使用することで、消費者に良い影響を与えています。

主なハイライト

- 飲料業界は、大幅な事業拡大と技術近代化投資を行っているパイオニアのひとつです。水の包装は、業界の複雑な技術分野です。純粋な飲料水の必要性に対する一般消費者の意識が高まるにつれ、包装水・ボトル入り飲料水産業は急成長を遂げています。

- ボトル入り飲料水は、その利便性から最も消費される飲料のひとつと考えられています。ボトル包装は水の長距離輸送にも適しています。家庭でお湯を沸かすのは時間がかかり、エネルギー効率も悪いです。ボトル入り飲料水パッケージ市場の成長に大きく貢献すると予想されます。新興市場では、水は健康的なライフスタイルの象徴となった。健康的な生活のために安全な水を消費しようという意識が高まり、水道水が汚染されるようになったことで、ボトル入り飲料水には大きな市場機会が生まれています。ひいては、ボトル入り飲料水のパッケージ市場に明るい展望をもたらすと思われます。

- さらに、ボトル入りミネラルウォーターは精製され、溶存ミネラルで強化されているため、消費者にさらなる健康上のメリットを提供します。革新的なデザインと新しいパッケージング・ソリューションは、パッケージングと軽量化の改善に貢献しました。したがって、ボトルウォーターパッケージング市場の促進要因となっています。

- しかし、ペットボトルの不適切な廃棄に起因する政府による環境規制は、予測期間中にボトルウォーターパッケージング市場規模を抑制する可能性が高いです。

- さらに、ロシアとウクライナの戦争はボトル入り飲料水市場に大きな影響を与えました。同地域と経済的に密接な関係を持つ同地域で事業を展開する企業は、長期的に自社の事業にどのような影響を及ぼす可能性があるかを検討しながら、戦争を考慮しています。

ボトルウォーターパッケージング市場の動向

市場を独占するプラスチック包装

- プラスチックは水筒の製造に最もよく使われる素材です。世界のボトル入り包装市場の97.3%を占めており、残りはガラスです。プラスチック容器は、安価で軽量、耐久性に優れた容器製造用素材です。ポリエチレンテレフタレート(PET)は最も一般的に使用されているプラスチックの一種で、100%リサイクルも可能です。

- 革新的なパッケージング技術により、軽量で耐久性のあるプラスチック製ウォーターパックボトルが開発され、市場にプラスの影響を与えています。さらに、カーボンフットプリントが低く、リサイクル可能な素材を使用した包装容器は、世界のボトルウォーターパッケージング市場の成長をさらに促進すると思われます。

- さらに、製造の先進化と運用コスト、樹脂、パッケージングの低下が業界の成長を加速させています。低原料コストは、ペットボトル包装の利用と採用を促進しています。

- さらに、ブランドオーナーは顧客に焦点を当てることで、輸送や製造における軽量化など、他の包装分野では類を見ないプラスチックボトル包装のデザイン革新を推し進めています。このような要因が、ボトル入り飲料水のプラスチック包装市場に拍車をかけています。

- Indorama Venturesによると、PETは飲料やその他頻繁に使用されるものプラスチックボトルを作るのに使用されます。PETの需要は2020年に2,700万トンに達しました。PETの需要は2030年には4,200万トンに達すると予想されています。PET需要の増加は、ペットボトル生産能力の増加を示しています。生産者は需要の増加を満たすために生産能力の拡張に資金を費やし、ボトル入り飲料水やその他の用途に使用されるプラスチックボトルの利用可能性を高めると思われます。

北米が圧倒的なシェアを占める

- 国際ボトルウォーター協会(IBWA)と飲料マーケティング・コーポレーション(BMC)によると、アメリカ人は他のどのパッケージ飲料よりもボトル入り飲料水を飲んでいます。健康意識、生活水準の向上、ボトル入り飲料水の需要と消費の増加は、北米におけるボトルウォーターパッケージングの主な促進要因です。

- 米国やカナダのような新興経済諸国では、利用可能な水は健康志向の消費者にとって魅力的な選択肢であるため、主要な商業的人気飲料カテゴリーになりつつあります。したがって、この要因はボトル入り飲料水市場を増大させています。

- シングルサーブのスパークリングウォーター製品、バルク水、製造された氷は、カナダのボトル入り飲料水製造部門の主要製品です。顧客のボトル入り飲料水購入への関心の高まりにより、業界収入は調査期間を通じて増加しました。これは、顧客の健康志向の高まりと、ソーダやジュースのような糖分の多い飲料の摂取を控えたいという願望によるものです。このような健康観の変化により、業界にはあまり含まれていない水道水フィルターのような、ボトル入り飲料水に代わる家庭用飲料水の需要が急増しました。

- さらに、国際ボトルウォーター協会(IBWA)の委託でハリス・ポールが18歳以上の米国成人2,000人以上を対象にオンラインで実施した最近の全国調査によると、米国人の88%が飲料の選択肢としてボトル入り飲料水に好印象を抱いていると答えています。

ボトルウォーターパッケージング業界の概要

ボトルウォーターパッケージング市場は、主要企業により細分化され、競争が激しいです。ボトルウォーターパッケージング市場の主要企業は、Amcor Ltd、Plastipak Holdings、Ball Corporation、Sidel Internationalです。ボトルメーカーはまた、より多くの顧客ベースと高い業界シェアを獲得するために広告やマーケティングキャンペーンに投資しています。

- 2022年10月-Sidelは、デリケートな飲料用の環境に優しいパッケージの未来形である1SKINボトルを発表します。Sidelは、ラベルのない唯一無二のリサイクルPETボトルを開発。1SKINは、サイデルの顧客が持続可能性の目標を達成するのを支援し、卓越した棚へのアピールと最高のエコ認証を融合させることで、ハイエンド商品の売上を押し上げるために作られました。

- 2022年7月-Amcor Limitedは、米国税務貿易局(TTB)が新たに承認したサイズに適合するリサイクル可能なポリエチレンテレフタレート(PET)製のスピリッツボトルのサンプルを発売しました。Amcorの新しい製品は、お客様が新しい市場を開拓するための自由と柔軟性を提供するために開発されました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- ボトルウォーター消費量の増加

- ボトルウォーター機器の技術革新

- 市場抑制要因

- プラスチックボトルの使い捨てに関する厳しい環境規制

- バリューチェーン/サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 材料別

- プラスチック

- 金属

- ガラス

- その他の材料

- 製品別

- ボトルウォーター

- 炭酸入りボトルウォーター

- フレーバーボトルウォーター

- 機能性ボトルウォーター

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Alpack Packaging

- Alpha Packaging(Protective Packaging Solutions)

- Amcor Limited

- Ball Corporation

- Exo Packaging

- Graham Packaging Company

- Greif Inc.

- Plastipak Holdings Inc.

- Rpc Group PLC

- Sidel International

- Silgan Holdings Inc.

- Tetra Pak International SA

第7章 投資展望

第8章 市場機会と今後の動向

The Bottled Water Packaging Market size is estimated at USD 54.15 billion in 2025, and is expected to reach USD 69.83 billion by 2030, at a CAGR of 5.22% during the forecast period (2025-2030).

The packaged water industry, and by extension, the bottled water packaging industry, is growing quickly as public awareness of the importance of clean drinking water rises. Additionally, the use of recyclable polymers in the production of bottles is making a good impact on consumers.

Key Highlights

- The beverage industry is one of the pioneers with considerable expansion and technology modernization investments. Packaging water is a complex technical area of the industry. The packaged and bottled water packaging industries are experiencing rapid growth as public awareness of the need for pure drinking water increases.

- Bottled water is considered one of the most consumed beverages due to its convenience. The bottle packaging is also suitable for long-distance transportation of water. Boiling water at home is time-consuming and energy inefficient. It is anticipated to contribute significantly to the growth of the bottled water packaging market. In emerging markets, it became a symbol of a healthy lifestyle. The rise in awareness about consuming safe water for a healthy life and contaminated tap water is creating a huge market opportunity for bottled water. It, in turn, will create a positive outlook on the bottled water packaging market.

- Moreover, bottled mineral water is purified and fortified with dissolved minerals, providing added health benefits to consumers. The innovative designs and new packaging solutions contributed to packaging and weight reduction improvements. Hence, acting as the driver for the bottled water packaging market.

- However, environmental regulations imposed by the government due to improper disposal of plastic bottles will likely curb the bottled water packaging market size during the forecast period.

- Moreover, the Russia-Ukraine war significantly impacted the bottled water packaging market. Businesses operating in the area with close financial ties to the region are considering the war into account as they examine how it may affect their operations over the long run.

Bottled Water Packaging Market Trends

Plastic Packaging to Dominate the Market

- Plastics are the most popular materials for manufacturing water bottles. They occupy 97.3 % of the global bottled packaging market, and glass occupies the rest. Plastic containers are inexpensive, lightweight, and durable materials for manufacturing containers. Polyethylene terephthalate (PET) is the most commonly used type of plastic and is also 100% recyclable.

- Innovative packaging technologies developed lightweight and durable plastic water pack bottles that positively impact the market. Furthermore, packaging containers with a low carbon footprint and recyclable material will further drive the growth of the global bottled water packaging market.

- Further, manufacturing advancements and lowering operational costs, resins, and packaging are pacing the industry's growth. Low feedstock costs are encouraging the utilization and adoption of plastic bottle packaging.

- Moreover, by focusing on customers, brand owners are pushing design innovations in plastic bottling that are unparalleled in the rest of the packaging sector, such as weight savings in transport and manufacturing. This factor is fueling the bottled water plastic packaging market.

- PET is used to make plastic bottles for beverages and other frequently used things, according to Indorama Ventures. The demand for PET reached 27 million metric tonnes in 2020. The demand for PET is anticipated to reach 42 metric tonnes by 2030. The rise in PET demand shows an increase in plastic bottle production capacity. Producers will spend money extending their production capacities to satisfy the rising demand, increasing the availability of plastic bottles for use in bottled water and other uses.

North America to Hold Prominent Share

- According to the International Bottled Water Association (IBWA) and the Beverage Marketing Corporation (BMC), Americans drink more bottled water than any other packaged beverage. Health awareness, a higher standard of living, and rising demand and consumption of bottled water are major driving factors of bottled water packaging in North America.

- In developed economies like the United States and Canada, available water is becoming a major commercial and popular beverage category, as it is an appealing option for health-conscious consumers. Hence, the factor is augmenting the bottled water market.

- The single-serve sparkling water products, bulk water, and produced ice are the primary products of the Canadian bottled water production sector. Due to a rise in customer interest in buying bottled water, industry income grew throughout the study period. It is due to customers' increased health consciousness and desires to consume fewer sugary beverage items like sodas and juices. The demand for at-home alternatives to bottled water, such as tap water filters, which are not often included in the industry, surged due to this shift in views toward health.

- Moreover, according to a recent nationwide study of more than 2,000 United States adults 18 and older conducted online by The Harris Poll on behalf of the International Bottled Water Association (IBWA), 88% of Americans say they include a favorable impression of bottled water as a beverage option.

Bottled Water Packaging Industry Overview

The bottled water packaging market is fragmented and competitive because of major players. The key bottled water packaging market players are Amcor Ltd, Plastipak Holdings, Ball Corporation, and Sidel International. The bottle manufacturers also invest in advertising and marketing campaigns to capture a larger customer base and a high industry share.

- October 2022- Sidel introduces their 1SKIN bottle, the future of environmentally friendly packaging for delicate beverages. Sidel developed a one-of-a-kind recycled PET bottle with no labels. It was created to assist Sidel's customers in achieving their sustainability goals and boost sales of high-end items by fusing exceptional shelf appeal with the best eco credentials.

- July 2022- Amcor Limited launched samples of spirits bottles made of recyclable polyethylene terephthalate (PET) that meet the newly approved US Tax and Trade Bureau (TTB) sizes. Amcor's new offering is developed to give customers the freedom and flexibility to explore new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increasing Bottled Water Consumption

- 4.3.2 Technological Innovations in Bottled Water Equipment

- 4.4 Market Restraints

- 4.4.1 Stringent Regulatory Concerning the Environment Regarding Disposable of Plastics Bottles

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Plastic

- 5.1.2 Metal

- 5.1.3 Glass

- 5.1.4 Other Materials

- 5.2 By Product

- 5.2.1 Still Bottled Water

- 5.2.2 Carbonated Bottled Water

- 5.2.3 Flavored Bottled Water

- 5.2.4 Functional Bottled Water

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia

- 5.3.4 Australia and New Zealand

- 5.3.5 Latin America

- 5.3.6 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Alpack Packaging

- 6.1.2 Alpha Packaging ( Protective Packaging Solutions)

- 6.1.3 Amcor Limited

- 6.1.4 Ball Corporation

- 6.1.5 Exo Packaging

- 6.1.6 Graham Packaging Company

- 6.1.7 Greif Inc.

- 6.1.8 Plastipak Holdings Inc.

- 6.1.9 Rpc Group PLC

- 6.1.10 Sidel International

- 6.1.11 Silgan Holdings Inc.

- 6.1.12 Tetra Pak International SA