|

市場調査レポート

商品コード

1640438

スキン包装:市場シェア分析、産業動向、成長予測(2025~2030年)Skin Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スキン包装:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 128 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

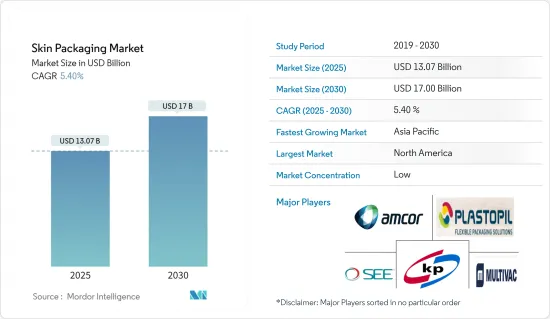

スキン包装市場規模は2025年に130億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.4%で、2030年には170億米ドルに達すると予測されます。

主要ハイライト

- スキン包装は、熱成形トレイや製造されたプラスチック容器の上に薄いプラスチックフィルムを重ねる最先端の技術です。このプラスチックフィルムは、顧客が汚染のリスクなしに製品を見ることができることに加え、製品を劣化させたり腐敗させたりする可能性のある空気や湿気に対して非常に透明な保護層を記載しています。

- 食品を保護し、賞味期限を延ばし、廃棄物を減らし、視認性を向上させるというニーズの高まりにより、スキン包装は、耐久性のあるトレイで信頼性などの利点を提供し、出荷、保管、陳列の際に製品を支え、保護するため、食品産業からの需要が高まっている

- チーズ、コールドカット、様々な形の牛肉など、様々な肉や乳製品の保存に対する需要の高まりが、スキン包装市場を牽引しています。真空スキン包装はより優れた耐久性を提供するため、従来の包装技術は近年、様々な食品産業用途で廃止されつつあります。さらに、従来の包装ソリューションと比較して食品を保護する追加の層を提供し、その採用を増加させ、市場の成長をサポートしています。

- リサイクルとバイオプラスチックの利点に対する理解が広まり、スキン包装の需要は世界的に増加しています。主要市場促進要因には、豊富な原料とスキン包装市場における技術開発のスピードアップが含まれます。

- インド包装工業協会(PIAI)によると、インドのスキン包装市場は2025年末までに2,048億1,000万米ドル以上の規模になるといいます。一人当たりの消費支出が増加し、軽くて耐久性があり、汚染から保護できる柔軟なプラスチック包装の優れた製品に対する需要が高まっているため、市場は予測期間を通じて発展を続けるとみられます。

- 一部は、消費者がより長い賞味期限と製品のより良い視認性を望んでいることが市場を牽引しています。スキン包装は、より良い製品保護を提供し、商品の完全性と鮮度を保つ。また、商品の視認性が向上するため、消費者は実際の商品やその特性を見ることができ、購買意欲が高まる可能性があります。

- 電子製品や部品は水に弱いため、保護鎧が必要です。そのため、耐水性があるスキン包装の需要は高いです。また、電気製品の損傷や傷から本体を保護するのにも役立ちます。さらに、工具や自動車部品などの工業製品はボディにダメージを受けやすく、ダイナミックな気象条件にさらされるため、さまざまな工業製品の包装用途でスキン包装のニーズが高まっている

- サステイナブル包装は未来であり、環境に優しい代替品の探求は食品産業における最優先事項です。従来のプラスチックで作られた生肉包装はプレッシャーに直面しており、そのため産業は環境に優しいソリューションへとシフトしています。2023年4月、Stora Ensoの新製品Trayforma BarrPeel(真空スキン包装用バリアコート板紙)は、生鮮品をリサイクル可能な板紙トレイで包装できるようにすることで、包装全体のプラスチック含有量を10%以下に抑えることを目指しました。

- 原料価格の変動や、食品包装用プラスチックの使用に関して政府が課す厳しい規制が、市場の成長を抑制する可能性が高いです。環境に優しい代替品が入手可能であることや、環境に対する懸念が高まっていることが、さらに市場成長の妨げになると予想されます。

スキン包装市場の動向

食品下の食肉サブセグメントが主要市場シェアを占める見込み

- スキン包装は、従来の真空包装から派生した最近の食肉保存方法です。この方法では、生の食肉をプラスチック・トレイに載せ、食肉が置かれている間に同時に加熱される熱成形プラスチック・フィルムで覆う。このプロセスにより、上皮が収縮して正確に成形されるため、空気の発生を防ぎ、目に見える滲出の可能性を低減し、製品の保存性を高めることができます。

- この技術は、小売店で購入できる少量の生肉、ミンチ肉、食肉加工品を商品化するために考案されました。プラスチックフィルムを製品に密着させることで、消費者が感じるあらゆる感覚を向上させることができます。

- 国連のサステイナブル開発目標(SDGs)への意識の高まりに後押しされ、賞味期限を延長し食品ロスを最小限に抑えるために、スーパーマーケットやその他の小売店ではスキン包装がますます一般的になっています。ブロック肉は購入されるまで長い間棚に置かれる傾向があるため、スキン包装方式は主に、家庭で消費されるスライス肉などではなく、ブロック肉に使用されます。

- 骨に刺さりにくく賞味期限が延びること、商品をしっかり固定できること、流通時に食肉を保護できること、消費者が商品を確認できる透明性がスキンフィルムの主要特徴です。マーチャンダイジングや賞味期限に対する利点はもちろんのこと、スキン包装シールのサイズは食肉の廃棄や返品を減らします。特に食肉産業では、液漏れやシール不良による小売店からの返品が多いです。

- 食肉・カット肉包装の需要はeコマースブームにより急速に増加しており、予測期間中も一定していることが予想されます。経済協力開発機構のデータによると、世界の鶏肉消費量は2022年の135.62キロトンから増加し、2028年には147.47キロトンに達すると予想されています。このように、食肉製品の消費が増加しているため、スキン包装のニーズが絶えないです。

アジア太平洋が市場で大きなシェアを占める見込み

- 組織型小売業やeコマースセクターが拡大し、原料の入手が容易であることから、アジア太平洋は市場参入企業にとって有望な成長の可能性をもたらすと予想されます。中国、インド、インドネシアでは消費者の購買力が高まっているため、包装食品の需要が増加すると予想され、市場の拡大を後押しすると考えられます。

- 中国のスキン包装産業は、同国の好景気、急速な都市化、生活水準の向上により成長しています。消費者は、より安全で、実用的で、個性的で、環境に配慮した包装を好みます。中国国家統計局によると、中国の総人口の約63.9%は都市部に住んでいます。中国は過去数十年にわたり、都市化率が着実に上昇しています。

- アジア太平洋が発展し続けるにつれ、企業はアジア太平洋での存在感を高めています。例えば、責任ある包装ソリューションのリーダーであるアムコーは、中国の恵州に最新鋭の生産施設を開設しました。1億米ドル以上を投じて建設された59万平方フィートの工場は、生産能力において中国最大の軟質包装施設であり、アジア太平洋全域で高まる顧客需要を満たすアムコーの能力を高めています。

- 人口の増加、所得水準の向上、ライフスタイルの変化により、消費者の支出が増加し、インドにおけるスキン包装製品の需要が高まると予想されます。さらに、インターネットやテレビを通じたメディアの普及が進み、農村部からの包装商品の需要が高まっている

- 需要の増加と飲食品産業における新規事業の出現に伴い、インドでは飲食品に使用される包装が急増しました。ZomatoやSwiggyのような食品宅配サービスの立ち上げと急速な拡大により、飲食品包装の利用が増加しています。スキン包装で食品の品質とレベルを維持しながら、ブランド認知を強調する食品包装がかなり先進化しています。

- 人口増加と都市化に伴い、中国における食肉需要は著しく伸びており、これは食肉の鮮度と柔らかさをより長く保つための様々なタイプのスキン包装の需要に影響を与えています。経済協力開発機構(OECD)によると、中国の1人当たり食肉消費量は増加傾向にあります。2021年には45.17キログラムだったが、2023年には48.28キログラムに増加し、2029年には52.84キログラムに達すると予想されています。

- この市場を牽引しているのは、肉、チーズ、魚、豚肉、魚介類、野菜など、保存性を高めるためにほとんどが皮付きパックになっているものに対する中国の顧客の嗜好の高まりです。中国の顧客は、新鮮魚介類を購入することに慣れてきています。

スキン包装産業概要

スキン包装市場の競合情勢は細分化されており、Amcor Group GmbH、Sealed Air Corporation、Clondalkin Flexible Packaging Orlando Inc.、Plastopil Hazorea Co.などの市場参入企業による研究開発費の増加は、競争優位性を確保する戦略である製品の差別化につながっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- レディトゥイート包装食品への需要の高まり

- 風味保持包装への需要の高まり

- 市場抑制要因

- 環境に対する懸念の高まりとプラスチック使用に関する政府の厳しい規制

- 技術スナップショット

- スキン包装機械

- 最近のスキン包装技術の動向

第6章 市場セグメンテーション

- 用途別

- 食品

- 食肉

- 魚介類

- 加工食品

- チーズ

- 工業製品(電子・電気部品を含む)

- 医療機器

- 耐久消費財

- 食品

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- アジア

- 中国

- 日本

- インド

- オーストラリアとニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Plastopil Hazorea Co. Ltd

- Sealed Air Corporation

- Amcor Group GmbH

- MULTIVAC Sepp Haggenmller SE & Co. KG

- Klckner Pentaplast Ltd

- Flexopack SA

- Winpak LTD

- SUDPACK Holding GmbH

- Taghleef Industries Group

- KM Packaging Services Ltd

第8章 投資分析

第9章 市場の将来

The Skin Packaging Market size is estimated at USD 13.07 billion in 2025, and is expected to reach USD 17.00 billion by 2030, at a CAGR of 5.4% during the forecast period (2025-2030).

Key Highlights

- Skin packaging is a state-of-the-art technique consisting of thin layers of plastic film over a thermoforming tray or manufactured plastic container. In addition to allowing customers to look at the product without any risk of contamination, this plastic film provides a very transparent layer of protection against air and moisture that may degrade products or cause them to spoil.

- The growing need to protect food, increase shelf life, reduce waste, and increase visibility is raising the demand for skin packaging from the food industry since it offers benefits, such as reliability, with durable trays, which support and protect products during shipping, storage, and display.

- The growing demand for the preservation of various meat and dairy products, such as cheese, cold cuts, and various forms of beef, is driving the skin packaging market. As vacuum skin packaging provides better durability, traditional packaging techniques have been phased out in various food industry applications in recent years. Moreover, it provides an additional layer that protects the food compared to conventional packaging solutions, increasing its adoption and supporting market growth.

- The demand for skin packaging has increased globally due to the growing understanding of the advantages of recycling and bioplastics. Key market drivers include the abundance of raw materials and the quickening pace of technical developments in the skin packaging market.

- According to the Packaging Industry Association of India (PIAI), the Indian skin packaging market will be worth more than USD 204.81 billion by the end of 2025. The market will continue to develop throughout the forecast period due to rising per capita spending and growing demand for superior products with flexible plastic packaging that is light and durable and can provide protection against contamination.

- In part, the market is driven by consumers wanting longer shelf life and better visibility of products. Skin packaging offers better product protection, preserving the integrity and freshness of the goods. It also gives the goods better visibility so that consumers can see the actual product and its characteristics, which may motivate purchases.

- Since electronic products and components are sensitive to water, they require protective armor. Hence, the demand for skin packaging is high due to its water-resistant properties. It also helps protect the body from damage and scratches in electrical products. Furthermore, industrial goods, such as tools and automotive parts, are prone to body damage and are exposed to dynamic weather conditions, increasing the need for skin packaging in different industrial goods packaging applications.

- Sustainable packaging is the future, and the quest for eco-friendly alternatives is a top priority in the food industry. Fresh meat packaging made from conventional plastic is facing pressure; hence, the industry is shifting toward eco-friendly solutions. In April 2023, Stora Enso's new Trayforma BarrPeel (barrier-coated paperboard for vacuum skin packaging) aimed to enable perishable products to be packaged in recyclable paperboard trays, reducing the overall plastic content of packaging to less than 10%.

- The fluctuating prices of raw materials and stringent regulations imposed by the government on the application of plastic for food packaging are likely to restrain market growth. The availability of environmentally friendly alternatives and rising environmental concerns are further expected to hamper market growth.

Skin Packaging Market Trends

The Meat Sub-segment Under Food is Expected to Hold a Major Market Share

- Skin packaging is a recent method of meat storage derived from traditional vacuum packaging. This method involves placing raw meats on a plastic tray and then covering them with a thermoformed plastic film that is heated simultaneously while the meat is being positioned. This process ensures that the upper skin is precisely shaped by shrinking it, thus preventing the formation of air and reducing the likelihood of visible exudation, increasing the product's shelf-life.

- This technique was created to commercialize small amounts of raw, minced, or meat preparations that can be bought in a retail store. The close fixation of the plastic film on the product also has the finality to enhance all sensory aspects perceived by the consumer since this technique is mainly used for self-service purchases.

- Skin packaging is becoming increasingly common in supermarkets and other retail outlets to extend expiration dates and minimize food loss, supported by the increased awareness of the UN Sustainable Development Goals (SDGs). As meat blocks tend to remain on the shelves long before being purchased, the skin packaging method is primarily used for blocks of meat rather than sliced meat for household consumption and other products.

- The ability to resist bone punctures and increase shelf life, hold the product in place, and protect the meat during distribution, as well as the clarity of the film that allows consumers to see the product, are the main characteristics of skin films. Aside from its advantages for merchandising and shelf life, the skin packaging seal's size reduces meat waste and returns. There can be many returns from retailers due to leaks or packages with poor seals, especially in the meat industry.

- The demand for meat and cut meat packaging is rapidly increasing due to the e-commerce boom, and it is expected to be constant during the forecast period. According to the Organisation for Economic Co-operation and Development data, poultry meat consumption worldwide is expected to reach 147.47 metric kilotons in 2028, an increase from 135.62 metric kilotons in 2022. Thus, due to the increasing consumption of meat products, there is a constant need for skin packaging.

Asia-Pacific is Expected to Hold Significant Share of the Market

- Due to the expanding organized retail and e-commerce sectors and the simplicity with which raw materials can be obtained, Asia-Pacific is anticipated to present prospective growth possibilities for market players. The demand for packaged food goods is expected to increase due to the rising consumer buying power in China, India, and Indonesia, which would boost market expansion.

- China's skin packaging industry is growing due to the country's booming economy, rapid urbanization, and rising standard of living. Consumers gravitate toward more secure, practical, distinctive, and environmentally responsible packaging. According to the National Bureau of Statistics of China, approximately 63.9% of China's total population resides in cities. China has experienced a steady increase in its urbanization rate over the past few decades.

- Companies are extending their presence in Asia-Pacific as the region continues to develop. For instance, Amcor, a leader in responsible packaging solutions, opened its brand-new, cutting-edge production facility in Huizhou, China. The 590,000 square foot factory, which cost over USD 100 million to build, is China's largest flexible packaging facility in terms of production capacity, enhancing Amcor's capabilities to fulfill rising client demand throughout Asia-Pacific.

- The rising population, rising income levels, and changing lifestyles are expected to increase consumer spending, raising the demand for skin packaging products in India. Moreover, the increased media penetration via the Internet and television is boosting the demand from the rural sector for packaged goods.

- With increased demand and the emergence of new businesses in the food and beverage industry, India witnessed a surge in the packaging used for food and beverages. Food and beverage packaging use has increased due to the launch and rapid expansion of food delivery services like Zomato and Swiggy. There have been considerable advancements in food packaging that emphasize brand recognition while upholding the caliber and level of the food product with contain skin packs.

- With the growing population and urbanization, the demand for meat in China is growing significantly, which impacts the demand for different types of skin packaging for meat to keep it fresh and tender for a longer duration. According to the Organisation for Economic Co-operation and Development, per capita meat consumption in China showed a growing trend. It was 45.17 kilograms in 2021, which increased to 48.28 kilograms in 2023; it is expected to reach 52.84 kilograms by 2029.

- The market is driven by the growing preference of Chinese customers for meat, cheese items, fish, pork, seafood, vegetables, and others that are mostly skin-packed to make them shelf-stable. Customers in the nation are becoming increasingly accustomed to purchasing fresh fish and seafood.

Skin Packaging Industry Overview

The competitive landscape of the skin packaging market is fragmented, consisting of several players like Amcor Group GmbH, Sealed Air Corporation, Clondalkin Flexible Packaging Orlando Inc., and Plastopil Hazorea Co. Increased R&D spending by market participants leads to product differentiation, which is a strategy to secure a competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Demand for Ready-to-Consume Packaged Food Products

- 5.1.2 Growing Demand for Flavor Retaining Packaging

- 5.2 Market Restraint

- 5.2.1 Rising Concerns About the Environment and Stringent Government Regulations Regarding the Use of Plastic

- 5.3 Technology Snapshot

- 5.3.1 Skin Packaging Machinery

- 5.3.2 Recent Developments in Skin Packaging Technology

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Food

- 6.1.1.1 Meat

- 6.1.1.2 Fish and Seafood

- 6.1.1.3 Processed Food

- 6.1.1.4 Cheese

- 6.1.2 Industrial Goods (Including Electronic and Electrical Components)

- 6.1.3 Medical Devices

- 6.1.4 Durable Consumer Goods

- 6.1.1 Food

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United kingdom

- 6.2.2.2 France

- 6.2.2.3 Germany

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 Australia and New Zealand

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Mexico

- 6.2.5 Middle East And Africa

- 6.2.5.1 Saudi Arabia

- 6.2.5.2 United Arab Emirates

- 6.2.5.3 South Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Plastopil Hazorea Co. Ltd

- 7.1.2 Sealed Air Corporation

- 7.1.3 Amcor Group GmbH

- 7.1.4 MULTIVAC Sepp Haggenmller SE & Co. KG

- 7.1.5 Klckner Pentaplast Ltd

- 7.1.6 Flexopack SA

- 7.1.7 Winpak LTD

- 7.1.8 SUDPACK Holding GmbH

- 7.1.9 Taghleef Industries Group

- 7.1.10 KM Packaging Services Ltd