エンドポイントセキュリティ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Endpoint Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 2044114

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

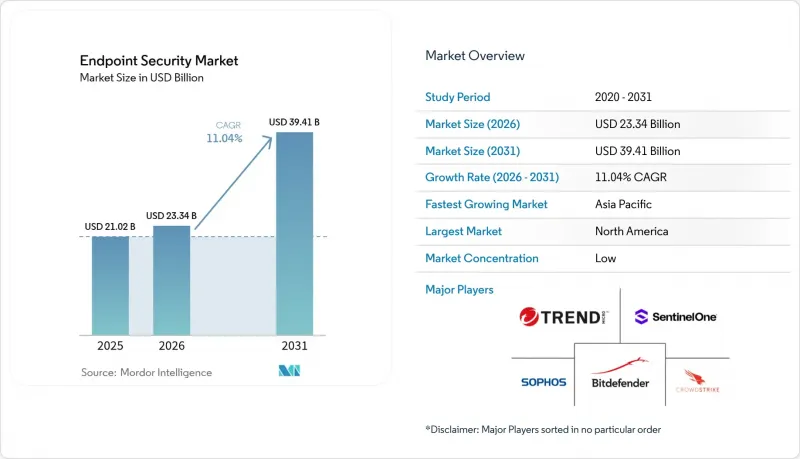

2026年のエンドポイントセキュリティ市場規模は233億4,000万米ドルと推定されており、2025年の210億2,000万米ドルから成長し、2031年には394億1,000万米ドルに達すると予測されています。

2026年から2031年にかけてのCAGRは11.04%となる見込みです。

エンドポイントセキュリティ市場における強い需要は、リモートワークやハイブリッドワークへの着実な移行、BYOD(Bring Your Own Device)ポリシーの拡大、およびRaaS(Ransomware-as-a-Service)ツールキットの高度化に起因しています。また、企業はIoT(Internet of Things)の普及拡大に直面しており、これによりITネットワークとOT(Operational Technology)ネットワークの境界線が曖昧になり、従来はオフィス機器を標的としていたのと同じ脅威に、重要な産業資産がさらされるようになっています。そのため、クラウド経由の制御機能、ゼロトラスト・アクセス・ポリシー、AIを活用した行動分析は、現代のエンドポイント保護戦略において標準的な構成要素となりつつあります。プラットフォームプロバイダーはこれに対応し、チップレベルのセキュリティ機能を組み込み、エンドポイント保護プラットフォーム(EPP)やエンドポイント検知・対応(EDR)機能をセキュア・アクセス・サービス・エッジ(SASE)ソリューションに統合することで、分散したユーザー全体でのポリシー適用を簡素化しています。

世界のエンドポイントセキュリティ市場の動向と洞察

BYODとモバイルワークフォースの急増

BYODポリシーにより、従来のファイアウォールの外側に位置する約47億台のモバイルエンドポイントが露呈したことで、企業データと個人用アプリを分離するモバイルデバイス管理ツールの急速な導入が進み、エンドポイントセキュリティ市場は強い勢いを見せています。現在、攻撃の70%でIDの侵害が確認されているため、企業はネットワークアクセスを許可する前にデバイスの状態を検証するゼロトラストフレームワークに依存しています。経営幹部はサイバーセキュリティを取締役会レベルの優先事項と捉える傾向が強まっており、91%がこれを単なるコンプライアンス対応ではなく、戦略的資産であると位置付けています。最新のエンドポイントスイートに組み込まれたAI機能は、リアルタイムの行動分析を行い、多様なデバイス環境全体でリスクのある行動を検知します。

ランサムウェア・アズ・ア・サービス(RaaS)の高度化

サービス型ランサムウェアは参入障壁を下げ、2024年初頭には感染件数が50%急増しました。医療分野における情報漏洩の平均被害額は現在1,010万米ドルに達しており、病院はエンドポイントとネットワークのテレメトリを相関分析する拡張型検知・対応(EDR)プラットフォームの導入を余儀なくされています。二重・三重の恐喝戦術はバックアップも標的としており、企業はデータ復旧計画の再設計を迫られています。アナリストは、2031年までにランサムウェアによる被害額が年間2,650億米ドルを超えると予測しており、これにより予防的なエンドポイント防御への投資が増加する見込みです。

SOCおよびインシデント対応チームにおけるスキル不足

世界的に300万人のサイバーセキュリティ専門家が不足していることから、最高情報セキュリティ責任者(CISO)の約半数が、対応体制の穴を懸念しています。そのため、マネージド・ディテクション・アンド・レスポンス(MDR)の導入が加速しており、2025年までに組織の半数が24時間365日の監視業務を外部委託すると予想されています。アラートの優先順位付けや封じ込め措置のスクリプト化を行う自動化およびAIツールは、人材供給体制が改善されるまでの実用的な暫定措置と見なされています。

セグメント分析

エンドポイント検知・対応(EDR)製品はCAGR15.52%で拡大しており、従来のアンチウイルスツールを容易に凌駕しています。組織はゼロデイ攻撃を特定する行動分析を好んでいますが、ファイアウォール/UTMアプライアンスは、既存のネットワーク機器との深い統合により、売上シェアの19.58%を維持しています。また、企業が社内のセキュリティオペレーションセンターを構築する代わりに専門知識を外部から調達する傾向が強まる中、マネージド・ディテクション・アンド・レスポンス(MDR)のサブスクリプションも勢いを増しています。

GDPRやNIS2などの規制が実証可能なデータ保護対策を求めていることから、規制当局の監視が暗号化およびデータ損失防止(DLP)モジュールに活気をもたらしています。セキュリティ更新プログラムの展開期間は依然として平均97日であり、攻撃対象領域が露出したままになるため、パッチ管理ツールへの投資が活発化しています。不正なソフトウェアをブロックするアプリケーション制御ツールは、企業ネットワーク上の個人用デバイスにおけるシャドーITのリスクを抑制するのに役立ちます。

クラウドプラットフォームは、2025年にはすでにエンドポイントセキュリティ市場規模の57.88%を占めており、2031年まで年率15.01%で成長する見込みです。一元化されたポリシーエンジンは、世界中に分散したデバイスへの展開を加速させ、大量のデータをリアルタイムでAIモデルに供給します。データ主権に関する規制や、専門的なオペレーショナルテクノロジー(OT)の制約に直面している企業では、ハイブリッドアーキテクチャが依然として人気を博しています。

オンプレミス展開は、ローカル処理が義務付けられている防衛および重要インフラ分野で依然として継続しています。そうした分野であっても、多くのチームは、管理を簡素化するために、ソフトウェア定義ネットワークとクラウド提供型セキュリティを組み合わせたSASEオーバーレイを採用しています。クラウドに統合されたEDR分析機能は、攻撃の潜伏時間を短縮し、平均対応時間を改善します。

エンドポイントセキュリティ市場は、ソリューションの種類(アンチウイルス/アンチマルウェア、ファイアウォール/UTMなど)、導入形態(オンプレミス、クラウド、ハイブリッド)、組織規模(大企業、中小企業)、エンドユーザー業界(BFSI、政府・防衛、ヘルスケア・ライフサイエンスなど)、および地域によってセグメンテーションされています。市場予測は金額(米ドル)ベースで提供されています。

地域別分析

北米は2025年に33.12%の売上シェアを維持しました。潤沢なセキュリティ予算、高度化する脅威の状況、そしてAIの早期導入が、継続的なアップグレードを後押ししています。政府によるクラウドセキュリティプログラムと、ベンダーの密なネットワークが、好循環的なイノベーションサイクルを生み出しています。

欧州の勢いは、2024年10月にNIS2指令が全面施行されることに起因しています。これにより、16万を超える組織が認定されたエンドポイント制御を導入することが義務付けられ、違反した場合は最大1,000万ユーロの罰金が科されます。この規制により、重要インフラ、製造業、デジタルサービスプロバイダー全体で需要が高水準に維持されています。

アジア太平洋地域はCAGR12.22%で、最も急速に成長している地域です。同地域の各国はサイバーレジリエンスの枠組みに投資を注ぎ込んでおり、通信事業者や金融機関に対する注目度の高い攻撃が、経営幹部の関心を一層高めています。中国のセキュリティチームはAPIの露出を最大の懸念事項としており、27%がマルウェアよりもこれを優先しています。政府の資金援助と現地のベンダーエコシステムにより、日本、韓国、オーストラリア、およびASEAN諸国全体での導入が加速しています。

中東・アフリカでは、サイバー保険料の値上げやプライバシー法の強化が進んでおり、銀行やエネルギー事業者がエンドポイント制御の強化に踏み切っています。ラテンアメリカでは、特に小売業やデジタルバンキング企業において、従来のオンプレミス環境を飛び越える形でクラウド導入が拡大しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- BYODおよびモバイルワークフォースの急増

- サービスとしてのランサムウェア(RaaS)の高度化

- OTネットワークにおけるIoTエンドポイントの普及

- エッジにおけるEPP/EDRを統合したSASEの普及拡大

- OEMによって統合されたチップレベルのセキュリティIP

- 認定EDRに対するサイバー保険料の割引

- 市場抑制要因

- SOCおよびインシデント対応チームにおけるスキル不足

- 中小企業における予算の制約

- 継続的なエンドポイントテレメトリに対するプライバシーへの反発の高まり

- サードパーティ製セキュリティエージェントのサプライチェーンリスク

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- 業界の魅力度- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因が市場に与える影響

第5章 市場規模と成長予測

- ソリューションタイプ別

- アンチウイルス/ アンチマルウェア

- ファイアウォール/UTM

- エンドポイント検出および対応(EDR)

- マネージド・ディテクション・アンド・レスポンス(MDR)

- 暗号化およびデータ損失防止

- パッチおよび構成管理

- アプリケーションおよびデバイス制御

- その他

- 展開モード別

- オンプレミス

- クラウド

- ハイブリッド

- 組織規模別

- 大企業

- 中小企業(SME)

- エンドユーザー業界別

- BFSI

- 政府・防衛

- ヘルスケアおよびライフサイエンス

- 製造業

- エネルギー・公益事業

- 小売およびEコマース

- ITおよび通信

- 教育

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- シンガポール

- マレーシア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Trend Micro Inc.

- CrowdStrike Holdings Inc.

- SentinelOne Inc.

- Sophos Ltd.

- Bitdefender LLC

- ESET Spol. s r.o.

- Kaspersky Lab JSC

- Trellix(Musarubra US LLC)

- OpenText(Cybersecurity & Carbonite Unit)

- WatchGuard Technologies Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Broadcom Inc.(Symantec Endpoint)

- Microsoft Corporation(Defender for Endpoint)

- Deep Instinct Ltd

- Cybereason Inc.

- BlackBerry Ltd(Cylance)

- Malwarebytes Inc.

- AhnLab Inc.

- F-Secure Corp.

- Elastic NV(Security)

- ReaQta BV(IBM)

- Comodo Security Solutions Inc.

- Seqrite(Quick Heal Technologies)

第7章 市場の機会と今後の動向

- 未開拓領域および未充足ニーズの評価

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日