|

|

市場調査レポート

商品コード

1742432

エンドポイントセキュリティの世界市場 (~2030年):ソリューション (ファイアウォール・パッチ管理・Webコンテンツフィルタリング・アンチウイルス)・サービス (プロフェッショナル・マネージド)・適用ポイント (ワークステーション・モバイルデバイス・サーバー・POS端末)・産業・地域別Endpoint Security Market by Solution (Firewall, Patch Management, Web Content Filtering, Antivirus), Service (Professional, Managed), Enforcement Point (Workstations, Mobile Devices, Server, POS Terminal), Vertical, Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| エンドポイントセキュリティの世界市場 (~2030年):ソリューション (ファイアウォール・パッチ管理・Webコンテンツフィルタリング・アンチウイルス)・サービス (プロフェッショナル・マネージド)・適用ポイント (ワークステーション・モバイルデバイス・サーバー・POS端末)・産業・地域別 |

|

出版日: 2025年06月02日

発行: MarketsandMarkets

ページ情報: 英文 340 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界のエンドポイントセキュリティの市場規模は、2025年の274億6,000万米ドルから、予測期間中は6.3%のCAGRで推移し、2030年には382億8,000万米ドルに成長すると予測されています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2019-2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025-2030年 |

| 単位 | 米ドル |

| セグメント別 | 提供区分・適用ポイント・展開モード・組織規模・産業・地域別 |

| 対象地域 | 北米・欧州・アジア太平洋・中東&アフリカ・ラテンアメリカ |

リモートワークアーキテクチャ、サードパーティアクセス、ハイブリッドITの普及に伴い、組織は故意または過失による社内での権限悪用のリスクに対する認識を高めています。過剰なユーザー権限や不十分なユーザー権限管理の可能性はかつてないほど高くなっています。エンドポイント権限管理は、最小権限の原則を適用することでこの問題を軽減できます。これは、ユーザーに対して必要なときにのみ必要最小限の権限を付与するという考え方です。このアプローチにより、攻撃対象領域の縮小、ラテラルムーブメント (侵入後の横方向移動) のリスク低下、不適切なデータアクセスの防止が可能になります。特にBFSI (銀行・金融・保険) 業界、医療、ITサービスなどの規制業界においては、強力な権限管理が求められており、あらゆる成功するエンドポイントセキュリティポリシーにおいて、強固な権限管理はもはや前提条件とされています。

”産業別では、BFSIセグメントが予測期間中最大の市場シェアを占める”

BFSI業界にとって、エンドポイントセキュリティは非常に重要です。これらの業界は、膨大な機密性の高い金融および個人情報を取り扱っており、ネットワークに接続されるすべてのデバイス (ノートパソコン、モバイル端末、ATM、POS端末など) を不正アクセスや脅威から保護する必要があります。エンドポイントセキュリティは、最新のセキュリティツール、脅威検知、マルウェア対策、暗号化、アクセス制御などを組み合わせてエンドポイントを保護するものです。2022年12月だけで、金融・保険業界では566件の情報漏洩が発生し、2億5,400万件以上の記録が流出しました。さらに、2024年1月には、LoanDepotが情報漏洩の被害を受け、1,690万人分の個人および金融データが侵害されました。また、Evolve Bank & Trustでも情報漏洩が発生し、760万人分の社会保障番号や口座情報などが流出しました。このようなリスクに対応するため、BFSI業界では、リアルタイム検知を含むエンドポイントセキュリティソリューションへの投資を強化し、顧客情報を保護して信頼を維持し、法的および評判上のリスクを最小限に抑える戦略的投資を進めています。

当レポートでは、世界のエンドポイントセキュリティの市場を調査し、市場概要、市場成長への各種影響因子の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と業界動向

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ケーススタディ分析

- ポーターのファイブフォース分析

- バリューチェーン分析

- エコシステム分析

- 特許分析

- 価格分析

- 技術分析

- エンドポイントセキュリティ市場における生成AIの影響

- 顧客ビジネスに影響を与える動向/混乱

- 主要な利害関係者と購入基準

- 関税と規制状況

- 2025年の主な会議とイベント

- 投資と資金調達のシナリオ

- 貿易分析

- 2025年の米国関税の影響- 概要

第6章 エンドポイントセキュリティ市場:提供区分別

- ソリューション

- ウイルス対策/マルウェア対策

- ウェブコンテンツフィルタリング

- ファイアウォール

- パッチ管理

- その他

- サービス

- 専門サービス

- マネージドサービス

第7章 エンドポイントセキュリティ市場:適用ポイント別

- ワークステーション

- モバイルデバイス

- サーバー

- POS端末

- その他

第8章 エンドポイントセキュリティ市場:展開モード別

- オンプレミス

- クラウド

第9章 エンドポイントセキュリティ市場:組織規模別

- 大企業

- 中小企業

第10章 エンドポイントセキュリティ市場:産業別

- BFSI

- ヘルスケア

- 政府

- IT・ITES

- 通信

- 製造

- 小売・eコマース

- エネルギー・ユーティリティ

- 教育

- その他

第11章 エンドポイントセキュリティ市場:地域別

- 北米

- マクロ経済見通し

- 市場促進要因

- 米国

- カナダ

- 欧州

- マクロ経済見通し

- 市場促進要因

- 英国

- ドイツ

- フランス

- イタリア

- その他

- アジア太平洋

- マクロ経済見通し

- 市場促進要因

- 中国

- 日本

- インド

- タイ

- フィリピン

- インドネシア

- マレーシア

- その他

- 中東・アフリカ

- マクロ経済見通し

- 市場促進要因

- GCC諸国

- 南アフリカ

- その他

- ラテンアメリカ

- ラテンアメリカ:市場促進要因

- ラテンアメリカ:マクロ経済見通し

- ブラジル

- メキシコ

- その他

第12章 競合情勢

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- ブランド比較

- 企業評価と財務指標

- 企業評価マトリックス:主要企業

- 企業評価マトリックス:スタートアップ/中小企業

- 競合シナリオ

第13章 企業プロファイル

- 主要企業

- MICROSOFT

- CROWDSTRIKE

- TREND MICRO

- PALO ALTO NETWORKS

- SENTINELONE

- CHECK POINT

- BROADCOM

- FORTINET

- CISCO

- TRELLIX

- KASPERSKY

- IBM

- BLACKBERRY

- ST ENGINEERING

- SOPHOS

- ESET

- その他の企業

- CORO

- ACRONIS

- VIPRE SECURITY GROUP

- MORPHISEC

- XCITIUM

- SECURDEN

- DEEP INSTINCT

- CYBEREASON

- OPTIV

- ELASTIC

第14章 隣接市場

第15章 付録

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2019-2023

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 ENDPOINT SECURITY MARKET AND GROWTH RATE, 2019-2024 (USD MILLION, Y-O-Y %)

- TABLE 4 ENDPOINT SECURITY MARKET AND GROWTH RATE, 2025-2030 (USD MILLION, Y-O-Y %)

- TABLE 5 CASE STUDY 1: EUROPE ENERGY PROTECTS CUSTOMER DATA AND MULTIMILLION EURO TRADING TRANSACTIONS WITH CROWDSTRIKE SOLUTIONS

- TABLE 6 CASE STUDY 2: AUSTRALIAN MEDIA LEADER STRENGTHENS CLOUD PUBLISHING SECURITY WITH PALO ALTO NETWORKS PLATFORM

- TABLE 7 CASE STUDY 3: UNIVERSITY BOOSTS ENDPOINT SECURITY WITH SYMANTEC MANAGEMENT SUITE

- TABLE 8 CASE STUDY 4: SOPHOS INSPIRES HEALTHCARE PROVIDER TO TAKE ITS SECURITY TO ADVANCED LEVEL OF ENDPOINT AND NETWORK PROTECTION

- TABLE 9 CASE STUDY 5: STRENGTHENING CYBERSECURITY AT BOLSHOI THEATRE WITH KASPERSKY'S MANAGED DETECTION AND RESPONSE SOLUTION

- TABLE 10 IMPACT OF PORTER'S FIVE FORCES ON ENDPOINT SECURITY MARKET

- TABLE 11 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 12 LIST OF TOP PATENTS IN ENDPOINT SECURITY MARKET, 2022-2025

- TABLE 13 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SOLUTION

- TABLE 14 INDICATIVE PRICING ANALYSIS OF KEY PLAYERS, BY OFFERING, 2025

- TABLE 15 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

- TABLE 16 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- TABLE 17 TARIFF RELATED TO ENDPOINT SECURITY SOLUTIONS, 2024

- TABLE 18 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 21 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 ENDPOINT SECURITY MARKET: DETAILED LIST OF CONFERENCES & EVENTS

- TABLE 23 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 24 KEY PRODUCT-RELATED TARIFF EFFECTIVE FOR ENDPOINT SECURITY HARDWARE

- TABLE 25 EXPECTED CHANGE IN PRICES AND LIKELY IMPACT ON END-USE MARKET DUE TO TARIFF IMPACT

- TABLE 26 ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 27 ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 28 ENDPOINT SECURITY MARKET, BY SOLUTION, 2019-2024 (USD MILLION)

- TABLE 29 ENDPOINT SECURITY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 30 SOLUTIONS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 31 SOLUTIONS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 32 ANTIVIRUS/ANTI-MALWARE: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 33 ANTIVIRUS/ANTI-MALWARE: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 34 WEB CONTENT FILTERING: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 35 WEB CONTENT FILTERING: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 36 FIREWALLS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 37 FIREWALLS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 38 PATCH MANAGEMENT: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 39 PATCH MANAGEMENT: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 40 OTHER SOLUTIONS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 41 OTHER SOLUTIONS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 42 ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 43 ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 44 SERVICES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 45 SERVICES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 46 PROFESSIONAL SERVICES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 47 PROFESSIONAL SERVICES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 48 MANAGED SERVICES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 49 MANAGED SERVICES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 50 ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2019-2024 (USD MILLION)

- TABLE 51 ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2025-2030 (USD MILLION)

- TABLE 52 WORKSTATIONS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 53 WORKSTATIONS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 54 MOBILE DEVICES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 55 MOBILE DEVICES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

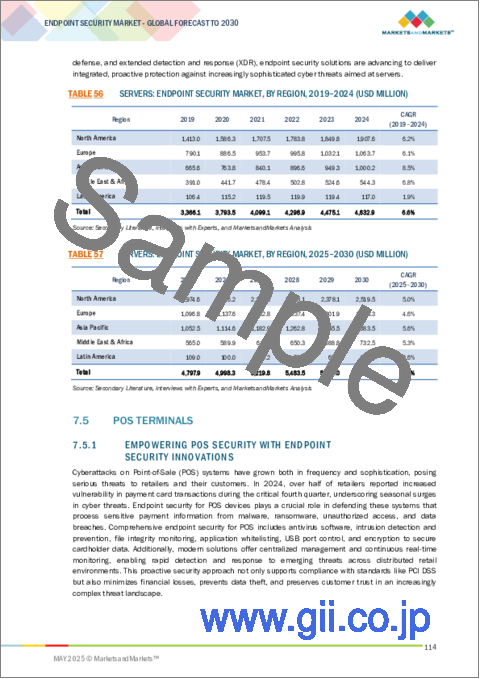

- TABLE 56 SERVERS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 57 SERVERS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 58 POS TERMINALS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 59 POS TERMINALS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 60 OTHER ENFORCEMENT POINTS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 61 OTHER ENFORCEMENT POINTS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 62 ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 63 ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 64 ON-PREMISES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 65 ON-PREMISES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 66 CLOUD: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 67 CLOUD: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 68 ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 69 ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 70 LARGE ENTERPRISES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 71 LARGE ENTERPRISES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 72 SMES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 73 SMES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 74 ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 75 ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 76 BFSI: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 77 BFSI: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 78 HEALTHCARE: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 79 HEALTHCARE: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 80 GOVERNMENT: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 81 GOVERNMENT: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 82 IT & ITES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 83 IT & ITES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 84 TELECOMMUNICATIONS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 85 TELECOMMUNICATIONS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 86 MANUFACTURING: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 87 MANUFACTURING: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 88 RETAIL & E-COMMERCE: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 89 RETAIL & E-COMMERCE: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 90 ENERGY & UTILITIES: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 91 ENERGY & UTILITIES: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 92 EDUCATION: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 93 EDUCATION: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 94 OTHER VERTICALS: ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 95 OTHER VERTICALS: ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 96 ENDPOINT SECURITY MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 97 ENDPOINT SECURITY MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 98 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 99 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 100 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY SOLUTION, 2019-2024 (USD MILLION)

- TABLE 101 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 102 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 103 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 104 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 105 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 106 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 107 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 108 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2019-2024 (USD MILLION)

- TABLE 109 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2025-2030 (USD MILLION)

- TABLE 110 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 111 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 112 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY COUNTRY, 2019-2024 (USD MILLION)

- TABLE 113 NORTH AMERICA: ENDPOINT SECURITY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 114 US: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 115 US: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 116 US: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 117 US: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 118 US: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 119 US: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 120 US: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 121 US: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 122 US: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 123 US: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 124 CANADA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 125 CANADA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 126 CANADA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 127 CANADA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 128 CANADA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 129 CANADA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 130 CANADA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 131 CANADA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 132 CANADA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 133 CANADA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 134 EUROPE: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 135 EUROPE: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 136 EUROPE: ENDPOINT SECURITY MARKET, BY SOLUTION, 2019-2024 (USD MILLION)

- TABLE 137 EUROPE: ENDPOINT SECURITY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 138 EUROPE: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 139 EUROPE: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 140 EUROPE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 141 EUROPE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 142 EUROPE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 143 EUROPE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 144 EUROPE: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2019-2024 (USD MILLION)

- TABLE 145 EUROPE: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2025-2030 (USD MILLION)

- TABLE 146 EUROPE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 147 EUROPE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 148 EUROPE: ENDPOINT SECURITY MARKET, BY COUNTRY, 2019-2024 (USD MILLION)

- TABLE 149 EUROPE: ENDPOINT SECURITY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 150 UK: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 151 UK: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 152 UK: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 153 UK: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 154 UK: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 155 UK: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 156 UK: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 157 UK: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 158 UK: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 159 UK: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 160 GERMANY: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 161 GERMANY: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 162 GERMANY: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 163 GERMANY: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 164 GERMANY: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 165 GERMANY: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 166 GERMANY: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 167 GERMANY: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 168 GERMANY: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 169 GERMANY: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 170 FRANCE: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 171 FRANCE: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 172 FRANCE: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 173 FRANCE: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 174 FRANCE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 175 FRANCE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 176 FRANCE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 177 FRANCE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 178 FRANCE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 179 FRANCE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 180 ITALY: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 181 ITALY: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 182 ITALY: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 183 ITALY: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 184 ITALY: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 185 ITALY: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 186 ITALY: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 187 ITALY: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 188 ITALY: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 189 ITALY: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 190 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 191 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 192 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 193 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 194 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 195 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 196 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 197 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 198 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 199 REST OF EUROPE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 200 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 201 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 202 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY SOLUTION, 2019-2024 (USD MILLION)

- TABLE 203 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 204 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 205 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 206 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 207 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 208 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 209 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 210 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2019-2024 (USD MILLION)

- TABLE 211 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2025-2030 (USD MILLION)

- TABLE 212 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 213 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 214 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY COUNTRY, 2019-2024 (USD MILLION)

- TABLE 215 ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 216 CHINA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 217 CHINA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 218 CHINA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 219 CHINA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 220 CHINA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 221 CHINA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 222 CHINA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 223 CHINA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 224 CHINA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 225 CHINA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 226 JAPAN: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 227 JAPAN: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 228 JAPAN: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 229 JAPAN: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 230 JAPAN: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 231 JAPAN: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 232 JAPAN: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 233 JAPAN: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 234 JAPAN: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 235 JAPAN: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 236 INDIA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 237 INDIA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 238 INDIA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 239 INDIA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 240 INDIA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 241 INDIA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 242 INDIA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 243 INDIA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 244 INDIA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 245 INDIA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 246 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 247 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 248 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 249 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 250 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 251 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 252 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 253 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 254 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 255 REST OF ASIA PACIFIC: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 256 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 257 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 258 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY SOLUTION, 2019-2024 (USD MILLION)

- TABLE 259 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 260 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 261 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 262 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 263 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 264 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 265 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 266 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2019-2024 (USD MILLION)

- TABLE 267 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2025-2030 (USD MILLION)

- TABLE 268 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 269 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 270 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY COUNTRY, 2019-2024 (USD MILLION)

- TABLE 271 MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 272 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 273 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 274 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 275 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 276 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 277 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 278 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 279 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 280 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 281 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 282 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY COUNTRY, 2019-2024 (USD MILLION)

- TABLE 283 GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 284 KSA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 285 KSA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 286 KSA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 287 KSA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 288 KSA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 289 KSA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 290 KSA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 291 KSA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 292 KSA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 293 KSA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 294 UAE: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 295 UAE: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 296 UAE: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 297 UAE: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 298 UAE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 299 UAE: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 300 UAE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 301 UAE: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 302 UAE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 303 UAE: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 304 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 305 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 306 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 307 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 308 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 309 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 310 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 311 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 312 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 313 REST OF GCC COUNTRIES: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 314 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 315 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 316 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 317 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 318 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 319 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 320 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 321 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 322 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 323 SOUTH AFRICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 324 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 325 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 326 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 327 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 328 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 329 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 330 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 331 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 332 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 333 REST OF MIDDLE EAST & AFRICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 334 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 335 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 336 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY SOLUTION, 2019-2024 (USD MILLION)

- TABLE 337 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 338 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 339 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 340 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 341 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 342 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 343 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 344 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2019-2024 (USD MILLION)

- TABLE 345 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2025-2030 (USD MILLION)

- TABLE 346 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 347 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 348 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY COUNTRY, 2019-2024 (USD MILLION)

- TABLE 349 LATIN AMERICA: ENDPOINT SECURITY MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 350 BRAZIL: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 351 BRAZIL: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 352 BRAZIL: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 353 BRAZIL: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 354 BRAZIL: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 355 BRAZIL: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 356 BRAZIL: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 357 BRAZIL: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 358 BRAZIL: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 359 BRAZIL: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 360 MEXICO: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 361 MEXICO: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 362 MEXICO: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 363 MEXICO: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 364 MEXICO: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 365 MEXICO: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 366 MEXICO: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 367 MEXICO: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 368 MEXICO: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 369 MEXICO: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 370 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 371 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 372 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2019-2024 (USD MILLION)

- TABLE 373 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY SERVICE, 2025-2030 (USD MILLION)

- TABLE 374 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2019-2024 (USD MILLION)

- TABLE 375 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 376 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 377 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 378 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 379 REST OF LATIN AMERICA: ENDPOINT SECURITY MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 380 OVERVIEW OF STRATEGIES ADOPTED BY KEY ENDPOINT SECURITY VENDORS, 2022-2024

- TABLE 381 ENDPOINT SECURITY MARKET: DEGREE OF COMPETITION

- TABLE 382 ENDPOINT SECURITY MARKET: REGION FOOTPRINT, BY KEY PLAYERS

- TABLE 383 ENDPOINT SECURITY MARKET: OFFERING FOOTPRINT, BY KEY PLAYERS

- TABLE 384 ENDPOINT SECURITY MARKET: DEPLOYMENT MODE FOOTPRINT, BY KEY PLAYERS

- TABLE 385 ENDPOINT SECURITY MARKET: VERTICAL FOOTPRINT, BY KEY PLAYERS

- TABLE 386 ENDPOINT SECURITY MARKET: KEY STARTUPS/SMES

- TABLE 387 ENDPOINT SECURITY MARKET: REGION FOOTPRINT

- TABLE 388 ENDPOINT SECURITY MARKET: OFFERING FOOTPRINT

- TABLE 389 ENDPOINT SECURITY MARKET: DEPLOYMENT MODE FOOTPRINT

- TABLE 390 ENDPOINT SECURITY MARKET: VERTICAL FOOTPRINT

- TABLE 391 ENDPOINT SECURITY MARKET: PRODUCT LAUNCHES & ENHANCEMENTS, JANUARY 2023-MAY 2025

- TABLE 392 ENDPOINT SECURITY MARKET: DEALS, JANUARY 2023-MAY 2025

- TABLE 393 MICROSOFT: COMPANY OVERVIEW

- TABLE 394 MICROSOFT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 395 MICROSOFT: DEALS

- TABLE 396 CROWDSTRIKE: COMPANY OVERVIEW

- TABLE 397 CROWDSTRIKE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 398 CROWDSTRIKE: DEALS

- TABLE 399 TREND MICRO: COMPANY OVERVIEW

- TABLE 400 TREND MICRO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 401 TREND MICRO: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 402 TREND MICRO: DEALS

- TABLE 403 PALO ALTO NETWORKS: COMPANY OVERVIEW

- TABLE 404 PALO ALTO NETWORKS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 405 PALO ALTO NETWORKS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 406 PALO ALTO: DEALS

- TABLE 407 SENTINELONE: COMPANY OVERVIEW

- TABLE 408 SENTINELONE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 409 SENTINELONE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 410 SENTINELONE: DEALS

- TABLE 411 CHECK POINT: COMPANY OVERVIEW

- TABLE 412 CHECK POINT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 413 CHECK POINT: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 414 CHECK POINT: DEALS

- TABLE 415 BROADCOM: COMPANY OVERVIEW

- TABLE 416 BROADCOM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 417 FORTINET: COMPANY OVERVIEW

- TABLE 418 FORTINET: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 419 FORTINET: DEALS

- TABLE 420 CISCO: COMPANY OVERVIEW

- TABLE 421 CISCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 422 CISCO: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 423 TRELLIX: COMPANY OVERVIEW

- TABLE 424 TRELLIX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 425 TRELLIX: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 426 TRELLIX: DEALS

- TABLE 427 KASPERSKY: COMPANY OVERVIEW

- TABLE 428 KASPERSKY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 429 KASPERSKY: DEALS

- TABLE 430 IBM: COMPANY OVERVIEW

- TABLE 431 IBM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 432 IBM: PRODUCT LAUNCHES

- TABLE 433 IBM: DEALS

- TABLE 434 BLACKBERRY: COMPANY OVERVIEW

- TABLE 435 BLACKBERRY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 436 BLACKBERRY: DEALS

- TABLE 437 ST ENGINEERING: COMPANY OVERVIEW

- TABLE 438 ST ENGINEERING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 439 SOPHOS: COMPANY OVERVIEW

- TABLE 440 SOPHOS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 441 SOPHOS: PRODUCT LAUNCHES

- TABLE 442 SOPHOS: DEALS

- TABLE 443 ESET: COMPANY OVERVIEW

- TABLE 444 ESET: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 445 ESET: PRODUCT LAUNCHES

- TABLE 446 ESET: DEALS

- TABLE 447 ADJACENT MARKETS AND FORECASTS

- TABLE 448 CYBERSECURITY MARKET, BY OFFERING, 2017-2022 (USD MILLION)

- TABLE 449 CYBERSECURITY MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 450 CYBERSECURITY MARKET, BY SOLUTION TYPE, 2017-2022 (USD MILLION)

- TABLE 451 CYBERSECURITY MARKET, BY SOLUTION TYPE, 2023-2028 (USD MILLION)

- TABLE 452 CYBERSECURITY MARKET, BY DEPLOYMENT MODE, 2017-2022 (USD MILLION)

- TABLE 453 CYBERSECURITY MARKET, BY DEPLOYMENT MODE, 2023-2028 (USD MILLION)

- TABLE 454 CYBERSECURITY MARKET, BY ORGANIZATION SIZE, 2017-2022 (USD MILLION)

- TABLE 455 CYBERSECURITY MARKET, BY ORGANIZATION SIZE, 2023-2028 (USD MILLION)

- TABLE 456 CYBERSECURITY MARKET, BY SECURITY TYPE, 2017-2022 (USD MILLION)

- TABLE 457 CYBERSECURITY MARKET, BY SECURITY TYPE, 2023-2028 (USD MILLION)

- TABLE 458 CYBERSECURITY MARKET, BY VERTICAL, 2017-2022 (USD MILLION)

- TABLE 459 CYBERSECURITY MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 460 ENDPOINT PROTECTION PLATFORM MARKET, BY OFFERING, 2018-2023 (USD MILLION)

- TABLE 461 ENDPOINT PROTECTION PLATFORM MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 462 ENDPOINT PROTECTION PLATFORM MARKET, BY ENFORCEMENT POINT, 2018-2023 (USD MILLION)

- TABLE 463 ENDPOINT PROTECTION PLATFORM MARKET, BY ENFORCEMENT POINT, 2024-2029 (USD MILLION)

- TABLE 464 ENDPOINT PROTECTION PLATFORM MARKET, BY DEPLOYMENT MODE, 2018-2023 (USD MILLION)

- TABLE 465 ENDPOINT PROTECTION PLATFORM MARKET, BY DEPLOYMENT MODE, 2024-2029 (USD MILLION)

- TABLE 466 ENDPOINT PROTECTION PLATFORM MARKET, BY ORGANIZATION SIZE, 2018-2023 (USD MILLION)

- TABLE 467 ENDPOINT PROTECTION PLATFORM MARKET, BY ORGANIZATION SIZE, 2024-2029 (USD MILLION)

- TABLE 468 ENDPOINT PROTECTION PLATFORM MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 469 ENDPOINT PROTECTION PLATFORM MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

List of Figures

- FIGURE 1 ENDPOINT SECURITY MARKET: RESEARCH DESIGN

- FIGURE 2 BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 3 ENDPOINT SECURITY MARKET: DATA TRIANGULATION

- FIGURE 4 ENDPOINT SECURITY MARKET ESTIMATION: RESEARCH FLOW

- FIGURE 5 APPROACH 1 (SUPPLY SIDE): REVENUE FROM SOLUTIONS/SERVICES OF ENDPOINT SECURITY VENDORS

- FIGURE 6 APPROACH 2 (SUPPLY-SIDE ANALYSIS)

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY (APPROACH 2): BOTTOM-UP (DEMAND SIDE) - SOLUTIONS/SERVICES

- FIGURE 8 GLOBAL ENDPOINT SECURITY MARKET SIZE AND Y-O-Y GROWTH RATE

- FIGURE 9 SEGMENTS WITH SIGNIFICANT MARKET SHARE AND GROWTH RATE

- FIGURE 10 NORTH AMERICA TO ACCOUNT FOR LARGEST SHARE IN 2025

- FIGURE 11 GROWING INSTANCES OF CYBER-THREATS TARGETING ENDPOINTS TO FUEL MARKET GROWTH

- FIGURE 12 ENDPOINT SECURITY SOLUTIONS TO FORM LARGER MARKET

- FIGURE 13 WORKSTATIONS SEGMENT TO ACCOUNT FOR LARGEST MARKET

- FIGURE 14 ON-PREMISES TO ACCOUNT FOR LARGER MARKET

- FIGURE 15 LARGE ENTERPRISES TO ACCOUNT FOR LARGER MARKET

- FIGURE 16 BFSI TO ACCOUNT FOR LARGEST MARKET SIZE DURING FORECAST PERIOD

- FIGURE 17 ASIA PACIFIC TO EMERGE AS BEST BET FOR INVESTMENTS IN NEXT FIVE YEARS

- FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: ENDPOINT SECURITY MARKET

- FIGURE 19 ENDPOINT SECURITY MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 20 ENDPOINT SECURITY MARKET: VALUE CHAIN ANALYSIS

- FIGURE 21 ENDPOINT SECURITY MARKET: ECOSYSTEM ANALYSIS

- FIGURE 22 NUMBER OF PATENTS GRANTED FOR ENDPOINT SECURITY MARKET, 2015-2025

- FIGURE 23 ENDPOINT SECURITY MARKET: REGIONAL ANALYSIS OF PATENTS GRANTED

- FIGURE 24 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SOLUTION

- FIGURE 25 MARKET POTENTIAL OF GENERATIVE AI IN ENHANCING ENDPOINT SECURITY MARKET ACROSS INDUSTRIES

- FIGURE 26 IMPACT OF GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- FIGURE 27 REVENUE SHIFT IN ENDPOINT SECURITY MARKET

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

- FIGURE 29 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- FIGURE 30 INVESTMENTS & FUNDING IN ENDPOINT SECURITY MARKET, 2020-2025

- FIGURE 31 ENDPOINT SECURITY HARDWARE EXPORT, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 32 ENDPOINT SECURITY HARDWARE IMPORT, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 33 SOLUTIONS TO ACCOUNT FOR LARGER MARKET DURING FORECAST PERIOD

- FIGURE 34 WORKSTATIONS TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- FIGURE 35 CLOUD DEPLOYMENT MODE TO RECORD HIGHER GROWTH RATE DURING FORECAST PERIOD

- FIGURE 36 SMES TO RECORD HIGHER GROWTH RATE DURING FORECAST PERIOD

- FIGURE 37 HEALTHCARE VERTICAL TO RECORD HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 38 LATIN AMERICA TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 39 NORTH AMERICA: MARKET SNAPSHOT

- FIGURE 40 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 41 SEGMENTAL REVENUE ANALYSIS OF TOP FIVE MARKET PLAYERS, 2020-2024 (USD MILLION)

- FIGURE 42 SHARE OF LEADING COMPANIES IN ENDPOINT SECURITY MARKET, 2024

- FIGURE 43 ENDPOINT SECURITY MARKET: COMPARISON OF VENDOR BRANDS

- FIGURE 44 COMPANY VALUATION OF KEY VENDORS, 2024 (USD BILLION)

- FIGURE 45 EV/EBIDTA, 2025

- FIGURE 46 ENDPOINT SECURITY MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 47 ENDPOINT SECURITY MARKET: COMPANY FOOTPRINT

- FIGURE 48 ENDPOINT SECURITY MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 49 MICROSOFT: COMPANY SNAPSHOT

- FIGURE 50 CROWDSTRIKE: COMPANY SNAPSHOT

- FIGURE 51 TREND MICRO: COMPANY SNAPSHOT

- FIGURE 52 PALO ALTO NETWORKS: COMPANY SNAPSHOT

- FIGURE 53 SENTINELONE: COMPANY SNAPSHOT

- FIGURE 54 CHECKPOINT: COMPANY SNAPSHOT

- FIGURE 55 BROADCOM: COMPANY SNAPSHOT

- FIGURE 56 FORTINET: COMPANY SNAPSHOT

- FIGURE 57 CISCO: COMPANY SNAPSHOT

- FIGURE 58 KASPERSKY: COMPANY SNAPSHOT

- FIGURE 59 IBM: COMPANY SNAPSHOT

- FIGURE 60 BLACKBERRY: COMPANY SNAPSHOT

- FIGURE 61 ST ENGINEERING: COMPANY SNAPSHOT

The global endpoint security market size is projected to grow from USD 27.46 billion in 2025 to USD 38.28 billion by 2030 at a Compound Annual Growth Rate (CAGR) of 6.3% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD (Billion) |

| Segments | By Offering, Enforcement Point, Deployment Mode, Organization Size, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

Organizations are increasingly aware of the risks of internal misuse of entitlement, whether on purpose or inadvertently, with remote work architectures, third-party access, and hybrid IT prevalent. The potential for excessive user privileges or poorly managed user privileges is likely to be greater than ever. Endpoint privilege management is able to mitigate this issue by applying the principle of least privilege, meaning users have the minimum permission that they require, when required. This approach decreases the potential attack surface, decreases lateral movement risk, and mitigates inappropriate access to data. Given the requirement for strong privilege controls in regulated industries such as BFSI, healthcare, and IT services, strong privilege controls in any endpoint security policy are now table stakes for any successful policy.

"By vertical, the BFSI segment accounts for the largest market share during the forecast period."

Endpoint security is very important for BFSI organizations, which involve a considerable amount of sensitive financial and personal information. It is all about protecting all devices connected to the network, such as laptops, mobile devices, ATMs, and point-of-sale terminals, from unauthorized access and threats. Endpoint security involves modern tools, threat detection, malware and protection, encryption, and access control to secure endpoints. In December 2022 alone, finance and insurance organizations across the world suffered 566 breaches that resulted in over 254 million records being leaked. In January 2024, LoanDepot was breached, with the impact of 16.9 million individuals' security being compromised, including sensitive personal and financial data. Evolve Bank & Trust reported a breach in security that compromised the security of 7.6 million people, including social security numbers and account information. By developing and investing in endpoint security solutions that include real-time detection, protecting customer information to uphold trust, and strategic investment to sustain customers, BFSI organizations are seeking to reduce legal and reputational exposure to US legislation.

"By region, North America accounts for the largest market share."

North America's endpoint security landscape is changing fast through strong collaborations between public and private organizations and technology partnerships between organizations, large and small, across Canada and the US. In Canada, Bell Canada partnered with SentinelOne to provide next-generation Managed Threat Detection and Response (MTDR) capabilities to its Security Operations Centre, while the University of Toronto gained 'next-gen' centralized threat management for nearly 10,000 endpoints across its campuses. In the US, federal funding and cooperation with industry partners facilitated programs including: Xage Security's USD 1.5 million contract with the US Navy to deliver Zero Trust Access as a multi-faceted and complex naval environment; and the White House combined with Microsoft and Google to deploy endpoint security capabilities, including training to critical rural hospitals. Additionally, Shepherd and Intel partnered to provide advanced Threat Detection Technology against ransomware threats. Together, all of the above describe the continent-wide approach toward advancing endpoint security through collaboration and investment and innovative platforms, aimed at addressing evolving cyber threats in all sectors, including healthcare, defense, academia, and enterprise.

Breakdown of primaries

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C-level - 45%, Directors - 35%, and Managers - 20%

- By Region: North America - 55%, Europe - 25%, Asia Pacific - 15%, RoW - 5%

The key players in the endpoint security market include Microsoft (US), Palo Alto (US), SentinelOne (US), Trend Micro (Japan), Fortinet (US), Cisco (US), Check Point (Israel), Blackberry (Canada), ESET (Slovakia), Kaspersky (Russia), Trellix (US), CrowdStrike (US), IBM (US), Broadcom (US), Sophos (UK), and others.

The study includes an in-depth competitive analysis of the key players in the endpoint security market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the endpoint security market and forecasts its size by offering [solutions (antivirus/antimalware, patch management, web content filtering, firewall, others (EDR, MDM, device control & authentication, endpoint encryption, configuration management)) and services (professional services (design, consulting, and implementation, training & education, support & maintenance), managed services], enforcement point [workstations, mobile devices, servers, point of sale terminals, others (kiosks, industrial system, and removable media)], deployment mode [cloud, on-premises], organization size [large enterprises, SMEs], vertical [BFSI, healthcare, government, IT & ITeS, energy & utilities, retail & e-commerce, telecommunications, manufacturing, education, other verticals (media & entertainment, construction, real estate and travel & hospitality], and region [North America, Europe, Asia Pacific, Middle East & Africa, and Latin America].

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall endpoint security market and its subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (growing surge of cyberattacks, increasing shift toward remote work, the rapid growth of IoT devices), restraints (high deployment costs, impact on device performance), opportunities (growing adoption of cloud, integration of AL/ML into endpoint security solutions), and challenges (shortage skilled cybersecurity professionals, zero-day vulnerabilities)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the endpoint security market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the endpoint security market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the endpoint security market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Microsoft (US), Palo Alto Networks (US), Trellix (US), CrowdStrike (US), Xcitium (US), Optiv (US), Deep Instinct (US), Securden (India), Morphisec (Israel), Coro (US), IBM (US), Trend Micro (Japan), SentinelOne (US), Sophos (UK), Broadcom (US), Elastic (US), Cybereason (US), Vipre Security (US), Acronis (Switzerland), VMware (US), Blackberry (Canada), ESET (Slovakia), Fortinet (US), Cisco (US), Check Point (Israel), and Kaspersky (Russia) in the endpoint security market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primaries

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR KEY MARKET PLAYERS

- 4.2 ENDPOINT SECURITY MARKET, BY OFFERING, 2025

- 4.3 ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT, 2025

- 4.4 ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE, 2025

- 4.5 ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE, 2025

- 4.6 ENDPOINT SECURITY MARKET, BY VERTICAL

- 4.7 MARKET INVESTMENT SCENARIO

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing surge of cyberattacks

- 5.2.1.2 Increasing shift toward remote work

- 5.2.1.3 Rapid growth of IoT devices

- 5.2.2 RESTRAINTS

- 5.2.2.1 High deployment costs

- 5.2.2.2 Impact on device performance

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing adoption of cloud

- 5.2.3.2 Integration of AI/ML into endpoint security solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Shortage of skilled cybersecurity professionals

- 5.2.4.2 Zero-day vulnerabilities

- 5.2.1 DRIVERS

- 5.3 CASE STUDY ANALYSIS

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- 5.4.1 THREAT OF NEW ENTRANTS

- 5.4.2 THREAT OF SUBSTITUTES

- 5.4.3 BARGAINING POWER OF SUPPLIERS

- 5.4.4 BARGAINING POWER OF BUYERS

- 5.4.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.5 VALUE CHAIN ANALYSIS

- 5.5.1 RESEARCH AND DEVELOPMENT

- 5.5.2 PLANNING AND DESIGNING

- 5.5.3 SOLUTION AND SERVICE PROVIDERS

- 5.5.4 SYSTEM INTEGRATORS

- 5.5.5 RETAIL/DISTRIBUTION/VARS

- 5.5.6 END USERS

- 5.6 ECOSYSTEM ANALYSIS

- 5.7 PATENT ANALYSIS

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SOLUTION

- 5.8.2 INDICATIVE PRICING ANALYSIS, BY OFFERING

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 AI/ML

- 5.9.1.2 Behavior-based detection

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Authentication technologies

- 5.9.2.2 Cloud analytics

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Zero Trust Architecture (ZTA)

- 5.9.3.2 Public Key Infrastructure (PKI)

- 5.9.1 KEY TECHNOLOGIES

- 5.10 IMPACT OF GENERATIVE AI ON ENDPOINT SECURITY MARKET

- 5.10.1 TOP USE CASES & MARKET POTENTIAL

- 5.10.1.1 Key use cases

- 5.10.2 IMPACT OF GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 5.10.2.1 Identity and Access Management (IAM)

- 5.10.2.2 Cloud Security

- 5.10.2.3 Network Security

- 5.10.2.4 Zero trust

- 5.10.1 TOP USE CASES & MARKET POTENTIAL

- 5.11 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.12 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 TARIFFS AND REGULATORY LANDSCAPE

- 5.13.1 TARIFFS RELATED TO ENDPOINT SECURITY

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.3 KEY REGULATIONS

- 5.13.3.1 General Data Protection Regulation

- 5.13.3.2 Health Insurance Portability and Accountability Act (HIPAA)

- 5.13.3.3 Payment Card Industry Data Security Standard

- 5.13.3.4 ISO 27001

- 5.14 KEY CONFERENCES & EVENTS IN 2025

- 5.15 INVESTMENT AND FUNDING SCENARIO

- 5.16 TRADE ANALYSIS

- 5.16.1 EXPORT SCENARIO OF ENDPOINT SECURITY HARDWARE, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- 5.16.2 IMPORT SCENARIO OF ENDPOINT SECURITY DEVICES, BY KEY COUNTRY, 2020-2024 (USD MILLION)

- 5.17 IMPACT OF 2025 US TARIFF - OVERVIEW

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 KEY IMPACT ON VARIOUS REGIONS/COUNTRIES

- 5.17.4.1 US

- 5.17.4.2 Canada

- 5.17.4.3 Mexico

- 5.17.4.4 Europe

- 5.17.4.4.1 Germany

- 5.17.4.4.2 France

- 5.17.4.4.3 United Kingdom

- 5.17.4.5 APAC

- 5.17.4.5.1 China

- 5.17.4.5.2 India

- 5.17.4.5.3 Australia

- 5.17.5 INDUSTRIES

- 5.17.5.1 Manufacturing

- 5.17.5.2 IT & ITeS

- 5.17.5.3 Manufacturing

- 5.17.5.4 Healthcare

6 ENDPOINT SECURITY MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: MARKET DRIVERS

- 6.2 SOLUTIONS

- 6.2.1 COMPREHENSIVE SECURITY SOLUTIONS TO MITIGATE CYBER THREATS

- 6.2.2 ANTIVIRUS/ANTI-MALWARE

- 6.2.3 WEB CONTENT FILTERING

- 6.2.4 FIREWALLS

- 6.2.5 PATCH MANAGEMENT

- 6.2.6 OTHER SOLUTIONS

- 6.3 SERVICES

- 6.3.1 LEVERAGING ENDPOINT SECURITY SERVICES FOR ENDPOINT DEFENSE

- 6.3.2 PROFESSIONAL SERVICES

- 6.3.2.1 Design, consulting, and implementation

- 6.3.2.2 Training and education

- 6.3.2.3 Support and maintenance

- 6.3.3 MANAGED SERVICES

7 ENDPOINT SECURITY MARKET, BY ENFORCEMENT POINT

- 7.1 INTRODUCTION

- 7.1.1 ENFORCEMENT POINT: MARKET DRIVERS

- 7.2 WORKSTATIONS

- 7.2.1 ENHANCING WORKSTATION SECURITY: LEVERAGING BEHAVIORAL ANALYTICS AND MACHINE LEARNING

- 7.3 MOBILE DEVICES

- 7.3.1 COMPREHENSIVE ENDPOINT SECURITY SOLUTIONS FOR IOS AND ANDROID DEVICES

- 7.4 SERVERS

- 7.4.1 ADDRESSING SERVER THREATS WITH ENDPOINT SECURITY

- 7.5 POS TERMINALS

- 7.5.1 EMPOWERING POS SECURITY WITH ENDPOINT SECURITY INNOVATIONS

- 7.6 OTHER ENFORCEMENT POINTS

8 ENDPOINT SECURITY MARKET, BY DEPLOYMENT MODE

- 8.1 INTRODUCTION

- 8.1.1 DEPLOYMENT MODE: MARKET DRIVERS

- 8.2 ON-PREMISES

- 8.2.1 ENSURING COMPLIANCE AND CONTROL WITH ON-PREMISES ENDPOINT SECURITY

- 8.3 CLOUD

- 8.3.1 SCALABILITY AND EFFICIENCY: DRIVING CLOUD-BASED ENDPOINT SECURITY ADOPTION

9 ENDPOINT SECURITY MARKET, BY ORGANIZATION SIZE

- 9.1 INTRODUCTION

- 9.1.1 ORGANIZATION SIZE: MARKET DRIVERS

- 9.2 LARGE ENTERPRISES

- 9.2.1 NEED TO MAINTAIN OPERATIONAL INTEGRITY AND REGULATORY COMPLIANCE DRIVES ENDPOINT SECURITY GROWTH IN LARGE ENTERPRISES

- 9.3 SMES

- 9.3.1 HIGH INCIDENT RATE AMONG SMES DRIVES GROWTH OF ENDPOINT SECURITY SOLUTIONS MARKET

10 ENDPOINT SECURITY MARKET, BY VERTICAL

- 10.1 INTRODUCTION

- 10.1.1 VERTICAL: MARKET DRIVERS

- 10.2 BFSI

- 10.2.1 INCREASING CYBERATTACKS DRIVES NEED FOR INTEGRATED SOLUTIONS

- 10.3 HEALTHCARE

- 10.3.1 NEED TO SAFEGUARD SENSITIVE PATIENT DATA DRIVES SURGE IN HEALTHCARE ENDPOINT SECURITY

- 10.4 GOVERNMENT

- 10.4.1 NEED TO FORTIFY GOVERNMENT NETWORKS DRIVES SURGE IN ENDPOINT SECURITY

- 10.5 IT & ITES

- 10.5.1 DEMAND TO MAINTAIN OPERATIONAL CONTINUITY SPURS ENDPOINT SECURITY GROWTH

- 10.6 TELECOMMUNICATIONS

- 10.6.1 LEVERAGING ENDPOINT SECURITY SOLUTIONS TO ENSURE UNINTERRUPTED SERVICE

- 10.7 MANUFACTURING

- 10.7.1 ENHANCING MANUFACTURING SECURITY WITH ADVANCED ENDPOINT SECURITY

- 10.8 RETAIL & E-COMMERCE

- 10.8.1 PROLIFERATION OF ONLINE TRANSACTION PLATFORMS SPURS DEMAND FOR ENDPOINT SECURITY

- 10.9 ENERGY & UTILITIES

- 10.9.1 ADOPTION OF ADVANCED TECHNOLOGIES AND MEETING REGULATORY COMPLIANCE

- 10.10 EDUCATION

- 10.10.1 SAFEGUARDING EDUCATIONAL INSTITUTIONS WITH ADVANCED ENDPOINT SECURITY

- 10.11 OTHER VERTICALS

11 ENDPOINT SECURITY MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 11.2.2 NORTH AMERICA: MARKET DRIVERS

- 11.2.3 US

- 11.2.3.1 Investments and partnerships propel endpoint security advancements

- 11.2.4 CANADA

- 11.2.4.1 University of Toronto enhanced security with next-gen endpoint security deployment

- 11.3 EUROPE

- 11.3.1 EUROPE: MARKET DRIVERS

- 11.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 11.3.3 UK

- 11.3.3.1 Increase in cyberattacks drives need for endpoint security solutions

- 11.3.4 GERMANY

- 11.3.4.1 Cybersecurity innovations boost endpoint security growth

- 11.3.5 FRANCE

- 11.3.5.1 Strengthening endpoint protection in France amidst digital expansion

- 11.3.6 ITALY

- 11.3.6.1 Enhancing endpoint security in Italy through strategic initiatives

- 11.3.7 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: MARKET DRIVERS

- 11.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 11.4.3 CHINA

- 11.4.3.1 Increasing internet penetration and cyberattacks drives growth of endpoint security solutions

- 11.4.4 JAPAN

- 11.4.4.1 Strategic collaborations drive endpoint security growth in Japan

- 11.4.5 INDIA

- 11.4.5.1 Rapid digitalization transformation to spur demand for endpoint security solutions in India

- 11.4.6 THAILAND

- 11.4.6.1 Strengthening Thailand's endpoint security with innovative technologies and collaborative initiatives

- 11.4.7 PHILIPPINES

- 11.4.7.1 Surge in cyberattacks accelerates endpoint security adoption across Philippines

- 11.4.8 INDONESIA

- 11.4.9 MALAYSIA

- 11.4.9.1 Rising cyber threats and strengthened regulatory measures driving endpoint security growth in Malaysia

- 11.4.10 REST OF ASIA PACIFIC

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 MIDDLE EAST & AFRICA: MARKET DRIVERS

- 11.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 11.5.3 GULF COOPERATION COUNCIL (GCC)

- 11.5.3.1 KSA

- 11.5.3.1.1 Transformative cybersecurity initiatives driving endpoint security growth

- 11.5.3.2 UAE

- 11.5.3.2.1 Cybersecurity initiatives propel UAE's endpoint security market growth

- 11.5.3.3 Qatar

- 11.5.3.3.1 Demand for strengthened endpoint security in Qatar's cyber strategy

- 11.5.3.4 Rest of GCC countries

- 11.5.3.1 KSA

- 11.5.4 SOUTH AFRICA

- 11.5.4.1 Local expertise and comprehensive solutions drive endpoint security growth

- 11.5.5 REST OF MIDDLE EAST & AFRICA

- 11.6 LATIN AMERICA

- 11.6.1 LATIN AMERICA: MARKET DRIVERS

- 11.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 11.6.3 BRAZIL

- 11.6.3.1 Acronis and Xcitium fortify endpoint security landscape in Brazil

- 11.6.4 MEXICO

- 11.6.4.1 AWS's strategic investment creates opportunity for endpoint security advancements in Mexico

- 11.6.5 REST OF LATIN AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2024

- 12.2 REVENUE ANALYSIS, 2020-2024

- 12.3 MARKET SHARE ANALYSIS, 2024

- 12.4 BRAND COMPARISON

- 12.4.1 MICROSOFT

- 12.4.2 CROWDSTRIKE

- 12.4.3 TRENDMICRO

- 12.4.4 PALO ALTO NETWORKS

- 12.4.5 SENTINELONE

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.5.1 COMPANY VALUATION, 2024

- 12.5.2 FINANCIAL METRICS USING EV/EBIDTA

- 12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.6.5.1 Company footprint

- 12.6.5.2 Region footprint

- 12.6.5.3 Offering footprint

- 12.6.5.4 Deployment mode footprint

- 12.6.5.5 Vertical footprint

- 12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.7.5.1 Detailed list of key startups/SMEs

- 12.7.6 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 12.7.6.1 Region footprint

- 12.7.6.2 Offering footprint

- 12.7.6.3 Deployment mode footprint

- 12.7.6.4 Vertical footprint

- 12.8 COMPETITIVE SCENARIO

- 12.8.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 12.8.2 DEALS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 MICROSOFT

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices made

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 CROWDSTRIKE

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices made

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 TREND MICRO

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches and enhancements

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices made

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 PALO ALTO NETWORKS

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches and enhancements

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices made

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 SENTINELONE

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches and enhancements

- 13.1.5.3.2 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths

- 13.1.5.4.2 Strategic choices made

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 CHECK POINT

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches and enhancements

- 13.1.6.3.2 Deals

- 13.1.7 BROADCOM

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.8 FORTINET

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.9 CISCO

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches and enhancements

- 13.1.10 TRELLIX

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches and enhancements

- 13.1.10.3.2 Deals

- 13.1.11 KASPERSKY

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Deals

- 13.1.12 IBM

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Solutions/Services offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches

- 13.1.12.3.2 Deals

- 13.1.13 BLACKBERRY

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Solutions/Services offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Deals

- 13.1.14 ST ENGINEERING

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Solutions/Services offered

- 13.1.15 SOPHOS

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Solutions/Services offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Product launches

- 13.1.15.3.2 Deals

- 13.1.16 ESET

- 13.1.16.1 Business overview

- 13.1.16.2 Products/Solutions/Services offered

- 13.1.16.3 Recent developments

- 13.1.16.3.1 Product launches

- 13.1.16.3.2 Deals

- 13.1.1 MICROSOFT

- 13.2 OTHER PLAYERS

- 13.2.1 CORO

- 13.2.2 ACRONIS

- 13.2.3 VIPRE SECURITY GROUP

- 13.2.4 MORPHISEC

- 13.2.5 XCITIUM

- 13.2.6 SECURDEN

- 13.2.7 DEEP INSTINCT

- 13.2.8 CYBEREASON

- 13.2.9 OPTIV

- 13.2.10 ELASTIC

14 ADJACENT MARKETS

- 14.1 INTRODUCTION

- 14.2 LIMITATIONS

- 14.2.1 CYBERSECURITY MARKET

- 14.2.2 CYBERSECURITY MARKET, BY OFFERING

- 14.2.3 CYBERSECURITY MARKET, BY SOLUTION TYPE

- 14.2.4 CYBERSECURITY MARKET, BY DEPLOYMENT MODE

- 14.2.5 CYBERSECURITY MARKET, BY ORGANIZATION SIZE

- 14.2.6 CYBERSECURITY MARKET, BY SECURITY TYPE

- 14.2.7 CYBERSECURITY MARKET, BY VERTICAL

- 14.3 ENDPOINT PROTECTION PLATFORM (EPP) MARKET

- 14.3.1 ENDPOINT PROTECTION PLATFORM MARKET, BY OFFERING

- 14.3.2 ENDPOINT PROTECTION PLATFORM MARKET, BY ENFORCEMENT POINT

- 14.3.3 ENDPOINT PROTECTION PLATFORM MARKET, BY DEPLOYMENT MODE

- 14.3.4 ENDPOINT PROTECTION PLATFORM MARKET, BY ORGANIZATION SIZE

- 14.3.5 ENDPOINT PROTECTION PLATFORM MARKET, BY VERTICAL

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS