|

市場調査レポート

商品コード

1851429

指紋センサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Fingerprint Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 指紋センサー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月10日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

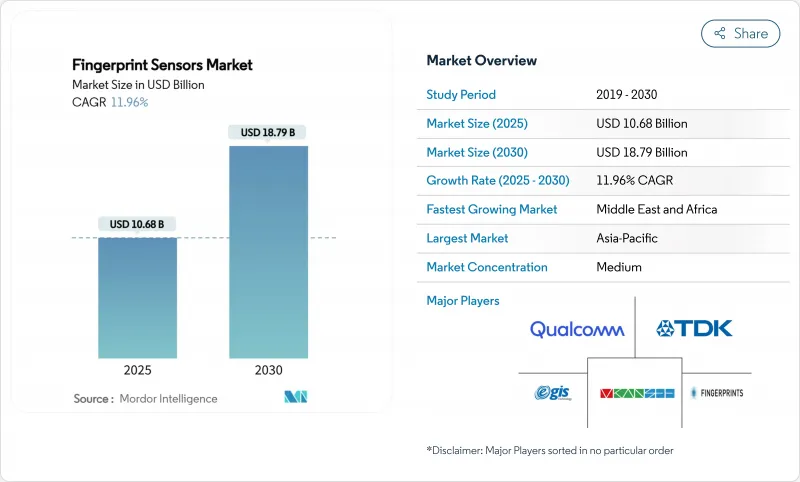

指紋センサー市場は2025年に106億8,000万米ドル、2030年には187億9,000万米ドルに達すると予測され、CAGRは11.96%です。

コンシューマー・エレクトロニクス、モビリティ、ペイメント、政府のアイデンティティ・プログラムにおける生体認証の義務付けが拡大し、対応可能な裾野が広がり続けています。スマートフォンブランドは、なりすまし耐性を損なうことなくベゼルフリーデザインを実現するために超音波アンダーディスプレイソリューションを採用し、決済グレードのバイオメトリックカードはPSD3とEMV要件を満たすカード提示取引を可能にしています。自動車部品メーカーは、キーレス・エントリーや車内パーソナライゼーション向けにAEC-Q100指紋ICの認定を取得しつつあり、PMUTの製造コストの低下により部品コストの圧力が緩和されています。AIベースの活性検出とエッジ処理の並行的な改善により、指紋認証の信頼性がさらに向上し、より広範なマルチモーダルセキュリティスタックにおけるその地位が強化されます。

世界の指紋センサー市場の動向と洞察

スマートフォンOEMのディスプレイ下超音波センサーへのシフト

超音波センサーをディスプレイ下に配置する設計により、携帯電話メーカーはエッジツーエッジのOLEDスクリーンを維持しながら、信頼性の高いバイオメトリクス・セキュリティを確保できます。クアルコムの最新の3D Sonic Maxトランスデューサは、600 mm2の画像を250 msでキャプチャし、湿った肌や油性の肌でもロック解除を維持します。サムスン、グーグル、シャオミは、2025年の製品ロードマップにおいて、FAR/FRR認証のしきい値を引き上げるAndroid 16バイオメトリックAPIに合わせて、フラッグシップラインに超音波実装を約束しています。その結果、スケールエコノミーがティア2OEMのASPを下げ、価格帯を超えた数量成長を加速させ、指紋センサー市場を次のデバイスサイクルへと押し上げます。

政府によるe-IDおよびe-パスポートの展開が需要を加速

アラブ首長国連邦(UAE)から南アフリカに至るまで、デジタルIDプログラムでは現在、セキュアエレメントに保存された指紋テンプレートを含む多要素バイオメトリクスが指定されています。モーリシャスは2024年2月にMNIC 3.0カードを発行し、ウォレット・ベースの国境を越えた認証を可能にするマッチ・オン・カード指紋認証を組み込みました。パプアニューギニアのセビスパス・パイロット(SevisPass pilot)は、小規模経済国がレガシー・インフラなしでバイオメトリクスIDに飛躍する方法を強調しています。このようなスキームは、信頼できるセンサー・モジュールの複数年にわたる調達の波を作り出し、指紋センサー市場を公共部門の予算サイクルに定着させる。

プレミアム・デバイスにおける顔認証の急速な普及

アップルのiPhone 17シリーズとサムスンのGalaxy Z7 Fold Proは、どちらも3D顔ロック解除をデフォルトとしており、生体認証のマインドシェアはカメラベースのモダリティにシフトしています。しかし、2025年に出荷される携帯端末の93%は依然として指紋リーダーを搭載しており、技術がアップルの0.002%のFAR目標を達成した暁には、ディスプレイ下センサーがiPhoneのポートフォリオに戻ると予想されています。指紋認証方式は、濡れた環境、手袋を着用した状態での使用、デバイス上のテンプレートストレージを必要とする銀行アプリのようなプライバシーに敏感なワークフローでは依然として好まれているため、カニバリゼーションは指紋センサー市場の大部分ではなく、プレミアムテールに大きく影響します。

セグメント分析

2024年の指紋センサー市場では、成熟したコストカーブと幅広いアプリケーションにより、静電容量式ユニットが51%のシェアを維持した。しかし、超音波チップはCAGR 15.42%で上昇し、OEMが高次の携帯電話や自動車コンソールを体積イメージングに移行させるため、2030年までに収益格差が縮小すると予測されます。超音波デバイスの指紋センサー市場規模は、プレミアムASPと自動車資格マージンを反映して、2030年までに40億米ドルを超える勢いです。バークレー校のセンサー&アクチュエーターセンターの調査によると、KNNベースのPMUTアレイは105.5dB/Vの出力を発生し、厚いカバーガラスや手袋を貫通します。

性能の優位性は認証の獲得にもつながっています。クアルコムの3D Sonic Maxは、2025年にFIDO Level-3およびBSI CC EAL 6+を達成し、ドイツのeIDコンプライアンスを実現しました。光学センサーはコスト重視の階層やキオスク端末にサービスを提供し続け、サーマル・センサーは過酷な環境や死後フォレンジック向けのニッチな製品にとどまっています。全体として、技術の多様性は、プレミアム・セグメントで超音波のリーダーシップが確固たるものとなっても、より広範な市場セグメンテーションを支えています。

背面/前面マウントは、レガシー・ハンドセット・デザインと頑丈なハンドヘルドに助けられ、2024年の売上高の42%を生み出しました。しかし、ディスプレイ下の超音波モジュールは、OLED基板の薄型化と局所的な音響結合層を利用して、CAGR最速の16.28%を記録します。ベゼルレスデザインが400ドル以下のデバイスに普及するにつれて、アンダーディスプレイ方式の指紋センサー市場シェアは2030年までに38%に達すると予想されます。Apple、Samsung、Oppoは、2024年下半期の生産枠で2億5,000万個を超えるアンダーディスプレイセンサーのダイを発注しており、大規模な採用を示唆しています。

サイドマウントの静電容量式ストリップは、迅速なタップ検出を優先する折りたたみ式携帯電話やゲーム用携帯電話では依然として人気が高いが、キーボードの交換サイクルがスマートフォンより2~3年遅れている企業向けノートパソコンでは、オンボタン/ホームキーの設計が残っています。BOEとVisionoxでテスト中のセンサーインOLEDプロトタイプは、指紋認証と心拍光電センサーを統合しており、指紋センサー市場の次の章を再定義する可能性のある多機能パネルを示唆しています。

指紋センサー市場は、センサータイプ(光学式、静電容量式、その他)、フォームファクター(リア/フロントマウント、サイドマウント、その他)、アプリケーション(スマートフォン&タブレット、ノートPC/PC、その他)、エンドユーザー産業(家電OEM、BFSI&FinTech、その他)、地域別に細分化されています。市場予測は金額(米ドル)で提供されます。

地域分析

アジア太平洋地域の収益シェア46%は、サプライチェーンの深さとエンドマーケットの需要のユニークな統合を反映しています。中国の垂直統合された携帯電話エコシステム、韓国のAMOLEDイノベーション、日本の圧電セラミックスのリーダーシップが、この地域のバリューチェーンを強固なものにしています。インドのAadhaar 2.0ロードマップとインドネシアのe-KTPアップグレードパイプラインは、複数年の国内需要をさらに下支えします。また、各国政府は現地でのシリコン製造の奨励策を講じることで、陸揚げコストを引き下げ、アジア太平洋を指紋センサー市場の重力の中心地として強化しています。

中東・アフリカはCAGR 15.4%と世界最速で拡大すると予測されています。アラブ首長国連邦(UAE)の国家バイオメトリクス・ウォレットとサウジアラビアのNafathプラットフォームは、市民のオンボーディングに認証指紋モジュールを要求しており、カードとキオスクの大量注文のきっかけとなっています。南アフリカの250万米ドルのスマートIDカード入札は、2029年の選挙前の大量発行を目指しており、アフリカのデジタルIDインフラへの飛躍を物語っています。madeやe-Fawateerなどの地域決済ネットワークがバイオメトリクス・トークナイゼーションに移行する中、センサーのサプライヤー・パイプラインは逼迫しており、新興国における指紋センサー市場の成長可能性が浮き彫りになっています。

北米と欧州は、自動車バイオメトリクス、企業セキュリティのアップグレード、厳格なデータプライバシーコンプライアンスに支えられ、一桁台半ばの成長軌道を維持しています。欧州のデジタルIDフレームワークは、2026年までにウォレットの導入を義務付けており、4億5,000万人の住民がデバイスまたはカードベースの指紋認証を必要とすることになります。TSMCの400億米ドルを投じたアリゾナ工場は、2026年に第2期ラインを開設する予定であり、米国の主要な携帯電話会社向けに超音波PMUTウエハーの生産を開始し、オンショア供給の回復力を強化し、指紋センサー市場の世界的な分布のバランスをとる。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- スマートフォンOEMのディスプレイ下超音波センサーへのシフト

- 政府によるe-IDとe-パスポートの導入が需要を加速させる

- 決済用バイオメトリクス・スマートカードの商業販売開始

- 自動車の車内生体認証がキーレスアクセスに義務付けられる

- AIによるなりすまし検知でセキュリティ認証が向上

- 薄膜圧電PMUTアレイのコスト/面積の低下

- 市場抑制要因

- プレミアムデバイスにおける顔認識の急速な採用

- バイオメトリクス・データの保持を制限するデータ・プライバシー法制

- ハイエンド8インチCIS鋳造へのサプライチェーン依存度

- 濡れた指の屋外環境における誤認不安

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- ライバルの激しさ

第5章 市場規模と成長予測

- センサータイプ別

- 光学

- 静電容量式

- サーマル

- 超音波

- フォームファクター/設置別

- リア/フロントマウント

- サイドマウント

- アンダーディスプレイ(光学)

- アンダーディスプレイ(超音波)

- オンボタン/ホームキー

- 用途別

- スマートフォンおよびタブレット

- ノートパソコン/PC

- スマートカードと決済トークン

- IoT/スマートロックとウェアラブル

- エンドユーザー業界別

- コンシューマーエレクトロニクスOEM

- BFSIとフィンテック

- 政府・法執行

- 軍事・防衛

- 自動車・モビリティ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Apple Inc.

- AU Optronics Corp.

- CrucialTec Co., Ltd.

- Egis Technology Inc.

- Fingerprint Cards AB

- Goodix Technology Co., Ltd.

- HID Global Corporation

- IDEX Biometrics ASA

- Infineon Technologies AG

- NEC Corporation

- Next Biometrics ASA

- Qualcomm Technologies Inc.

- Samsung System LSI Business

- Shenzhen Chipone/Novatek(Biometric BU)

- Sonavation Inc.

- STMicroelectronics N.V.

- Synaptics Incorporated

- TDK Corporation(InvenSense)

- Thales Group

- TKH Group(Nedap)

- VKANSEE Technology Inc.