|

市場調査レポート

商品コード

1773357

指紋センサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Fingerprint Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 指紋センサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月23日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

指紋センサーの世界市場は、2024年には42億米ドルと評価され、CAGR6.9%で成長し、2034年までには81億米ドルに達すると予測されています。

この成長の主な要因は、安全な生体認証に対する需要の高まりと、シームレスな認証ソリューションに対する消費者の志向の高まりです。デジタルセキュリティが日常生活に浸透するにつれ、指紋センサーは利便性と信頼性の理想的なバランスを提供します。センサーの設計と性能における急速な進歩は、業界全体にわたって指紋認証の精度と適応性を高めています。

従来の静電容量式技術から、より堅牢な超音波センサーや光学センサーへの進化により、指先が濡れていたり汚れていたりするような一般的な識別の課題が解消されました。例えば、超音波指紋センサーは音波マッピングに依存し、より高いなりすまし耐性と精度を実現します。こうした技術改良は、スマートフォン以外にも、スマートカード、自動車システム、高セキュリティの入退室管理など、新たな用途を開拓しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 42億米ドル |

| 予測金額 | 81億米ドル |

| CAGR | 6.9% |

指紋認証技術は現在、ノートパソコン、決済端末、ドアロック、携帯電子機器など、幅広い消費者・商業製品に組み込まれています。簡単なタッチ操作でデバイスのロックを解除したり、取引を完了したりできる機能は、ユーザー体験を複雑にすることなく、スピード、セキュリティ、プライバシーに対する期待の高まりと一致しています。メーカー各社は次世代電子機器に指紋センサーを組み込むことでこの動向を受け入れ、普及を後押ししています。

エリアタッチセンサーセクターは2024年に37億米ドルの市場規模を占めました。市場をリードしているのは、優れたスキャン能力、一貫した精度、さまざまなデバイスアーキテクチャに対応する互換性による。これらのセンサーは、その信頼性と統合の容易さにより、個人用・商業用アプリケーションの両方で広く使用されています。スケーラブルでコスト効率の高いソリューションを必要とする業界、特に価格に敏感な地域や資源に制約のある地域からの強い需要により、エリアセンサーとタッチセンサーは依然として最重要の選択肢となっています。

モバイルおよびポータブル指紋センサー分野は、2024年に33億米ドルを生み出しました。これらのセンサーの人気は、コンシューマーエレクトロニクス、金融サービス、政府機関などにおいて、外出先での迅速な本人確認ニーズが高まっていることに起因しています。これらの小型センサーは、認証を静的環境からモバイルプラットフォームへと移行させ、フィールドベースのセキュリティからアプリベースのeコマース認証まで幅広い業務をサポートしています。

米国の指紋センサー市場は、2024年に7億9,620万米ドルと評価されました。同国は、防衛、法執行、民間部門におけるバイオメトリクスの広範な利用に支えられ、世界の採用をリードし続けています。公共安全の近代化、国境管理の強化、デジタルIDイニシアチブへの多大な投資により、国家安全保障戦略における指紋センサーの役割は確固たるものとなっています。米国を拠点とする防衛およびハイテク請負業者は現在、生体認証ツールを安全な通信システムやユーザー認証デバイスに組み込み、従来の使用事例を超えて技術の有用性を拡大しています。

世界の指紋センサー業界で技術革新を推進し、競合情勢を形成している主要企業には、Synaptics Incorporated、Egis Technology Inc.、Shenzhen Goodix Technology Co.,Ltd.、Qualcomm Technologies, Inc.などが挙げられます。指紋センサー分野で競合する企業は、技術革新による製品の差別化に重点を置いています。精度と環境適応性を向上させるため、超音波や光学ベースのソリューションのような高度なセンサー技術に投資しています。

スマートウェアラブル、自動車ダッシュボード、入退室管理システムなど、より多様な最終用途デバイスにセンサーを統合するため、OEMとの戦略的提携が優先されています。さらに、モバイルやインフラアプリケーションに合わせたコスト効率と拡張性の高いソリューションを提供することで、新興市場に進出している企業も多いです。知的財産の保護と研究開発の拡大は、技術的な優位性を維持するために引き続き重要であり、バイオメトリックセキュリティの標準とコンプライアンスの枠組みへの参加は、信頼と規制の整合性を高めます。これらの戦略が相まって、持続的な成長、市場浸透の拡大、長期的なブランドエクイティを支えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 安全な生体認証の需要の高まり

- センサー技術の進歩

- モノのインターネット(IOT)およびスマートデバイスとの統合

- 政府の取り組みと規制遵守

- 利便性とユーザーエクスペリエンスに対する消費者の好み

- 業界の潜在的リスク・課題

- セキュリティの脆弱性とスプーフィングのリスク

- 新興アプリケーションにおける統合と互換性の制限

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 市場集中分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展、2021年~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:センサータイプ別、2021年~2034年

- 主要動向

- エリアセンサーとタッチセンサー

- スワイプセンサー

第6章 市場推計・予測:モビリティ、2021年~2034年

- 主要動向

- 固定式/指紋スキャナー

- モバイル/ポータブル

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 個人

- BFSI

- ヘルスケア

- 小売・eコマース

- 自動車

- 政府と防衛

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- BioEnable

- Egis Technology Inc.

- Fingerprint Cards AB

- GigaDevice

- HID Global Corporation

- Holtek Semiconductor Inc.

- IDEX Biometrics ASA

- Mantra Softech

- Next Biometrics

- Qualcomm Technologies, Inc.

- SecuGen Corporation

- Shenzhen Goodix Technology Co., Ltd.

- SUPREMA

- Synaptics Incorporated

- Thales

- Xthings Inc.

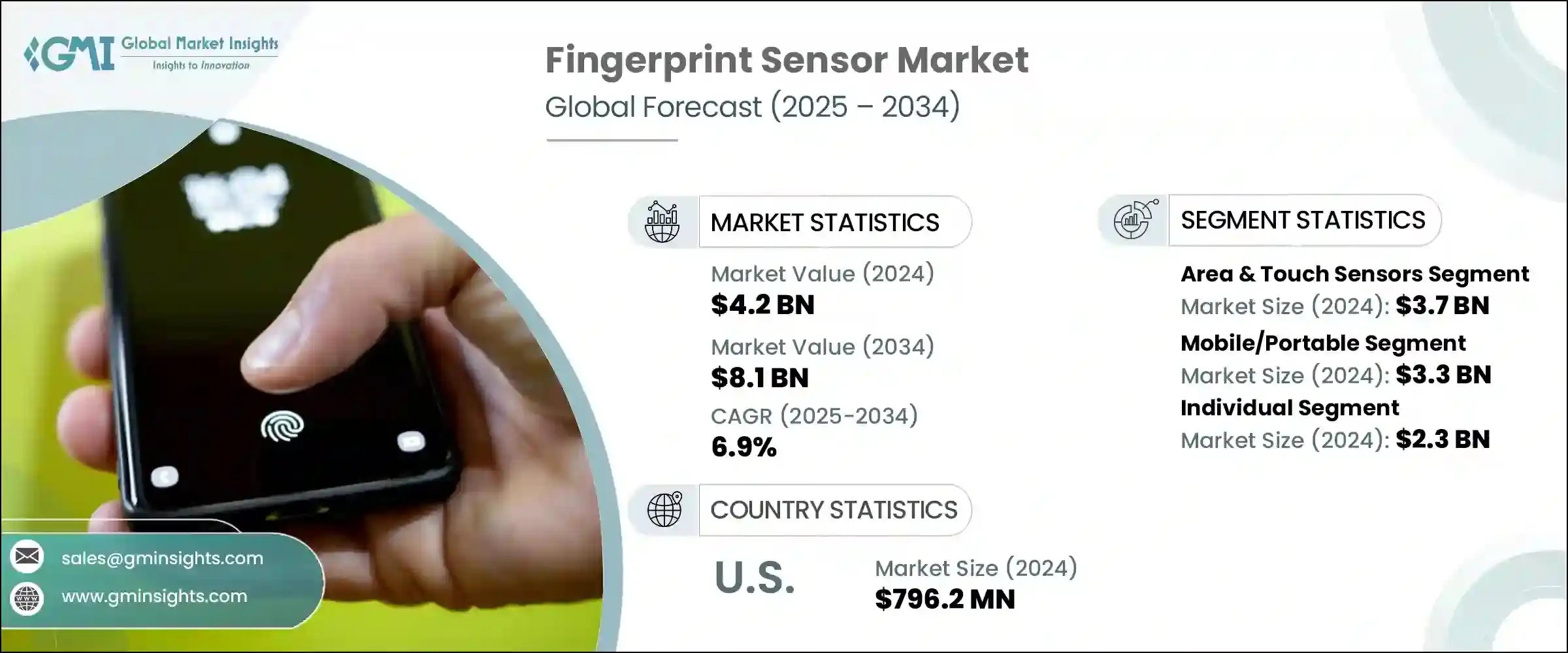

The Global Fingerprint Sensor Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 8.1 billion by 2034. This growth is primarily fueled by rising demand for secure biometric verification and increasing consumer inclination toward seamless authentication solutions. As digital security becomes more embedded in daily life, fingerprint sensors offer the ideal balance of convenience and reliability. Rapid advancements in sensor design and performance are enhancing the accuracy and adaptability of fingerprint authentication across industries.

The evolution from traditional capacitive technologies to more robust ultrasonic and optical sensors has eliminated common identification challenges such as wet or smudged fingertips. Ultrasonic fingerprint sensors, for instance, rely on sound wave mapping, delivering higher spoof resistance and precision. These technological improvements are unlocking new applications beyond smartphones, extending into smart cards, automotive systems, and high-security access control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 billion |

| Forecast Value | $8.1 billion |

| CAGR | 6.9% |

Fingerprint technology is now being integrated into a wide array of consumer and commercial products, including laptops, payment terminals, door locks, and portable electronics. The ability to unlock devices or complete transactions with a simple touch aligns with growing expectations for speed, security, and privacy without complicating the user experience. Manufacturers are embracing this trend by embedding fingerprint sensors into next-gen electronics, driving widespread adoption.

Area and touch sensors segment dominated the market with a value of USD 3.7 billion in 2024. Their market lead is attributed to superior scanning capabilities, consistent accuracy, and compatibility across various device architectures. These sensors are widely used in both personal and commercial applications due to their reliability and ease of integration. With strong demand from industries that require scalable, cost-efficient solutions, particularly in price-sensitive or resource-constrained regions, area and touch sensors remain a top choice.

The mobile and portable fingerprint sensor segment generated USD 3.3 billion in 2024. Their popularity stems from the growing need for fast, on-the-go identification across consumer electronics, financial services, and government sectors. These compact sensors have transitioned authentication from static environments to mobile platforms, supporting operations ranging from field-based security to app-based e-commerce verification.

U.S. Fingerprint Sensor Market was valued at USD 796.2 million in 2024. The country continues to lead global adoption, supported by the widespread use of biometrics in defense, law enforcement, and civilian sectors. Significant investments in public safety modernization, border management enhancements, and digital ID initiatives have cemented the role of fingerprint sensors in national security strategies. US-based defense and tech contractors are now embedding biometric tools into secured communications systems and user-authenticated devices, expanding the technology's utility beyond conventional use cases.

Key players driving innovation and shaping the competitive landscape in the Global Fingerprint Sensor Industry include Synaptics Incorporated, Egis Technology Inc., Shenzhen Goodix Technology Co., Ltd., and Qualcomm Technologies, Inc. Companies competing in the fingerprint sensor space are focusing heavily on product differentiation through technological innovation. They are investing in advanced sensor technologies like ultrasonic and optical-based solutions to improve accuracy and environmental adaptability.

Strategic collaborations with OEMs are being prioritized to integrate sensors into a wider variety of end-use devices such as smart wearables, automotive dashboards, and access control systems. Additionally, many are expanding into emerging markets by offering cost-effective, scalable solutions tailored for mobile and infrastructure applications. Intellectual property protection and R&D expansion remain critical to maintaining a technological edge, while participation in biometric security standards and compliance frameworks enhances trust and regulatory alignment. Together, these strategies support sustained growth, increased market penetration, and long-term brand equity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Sensor type trends

- 2.2.2 Mobility trends

- 2.2.3 End use trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for secure biometric authentication

- 3.2.1.2 Advancements in sensor technology

- 3.2.1.3 Integration with internet of things (IOT) and smart devices

- 3.2.1.4 Government initiatives and regulatory compliance

- 3.2.1.5 Consumer preference for convenience and user experience

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Security vulnerabilities and spoofing risks

- 3.2.2.2 Integration and compatibility limitations in emerging applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.11 Consumer sentiment analysis

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Sensor Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Area & touch sensors

- 5.3 Swipe sensors

Chapter 6 Market Estimates and Forecast, By Mobility, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Fixed/fingerprint scanners

- 6.3 Mobile/portable

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Individual

- 7.3 BFSI

- 7.4 Healthcare

- 7.5 Retail & e-commerce

- 7.6 Automotive

- 7.7 Government & defense

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BioEnable

- 9.2 Egis Technology Inc.

- 9.3 Fingerprint Cards AB

- 9.4 GigaDevice

- 9.5 HID Global Corporation

- 9.6 Holtek Semiconductor Inc.

- 9.7 IDEX Biometrics ASA

- 9.8 Mantra Softech

- 9.9 Next Biometrics

- 9.10 Qualcomm Technologies, Inc.

- 9.11 SecuGen Corporation

- 9.12 Shenzhen Goodix Technology Co., Ltd.

- 9.13 SUPREMA

- 9.14 Synaptics Incorporated

- 9.15 Thales

- 9.16 Xthings Inc.