|

市場調査レポート

商品コード

1851351

可変周波数ドライブ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Variable Frequency Drives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 可変周波数ドライブ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月08日

発行: Mordor Intelligence

ページ情報: 英文 183 Pages

納期: 2~3営業日

|

概要

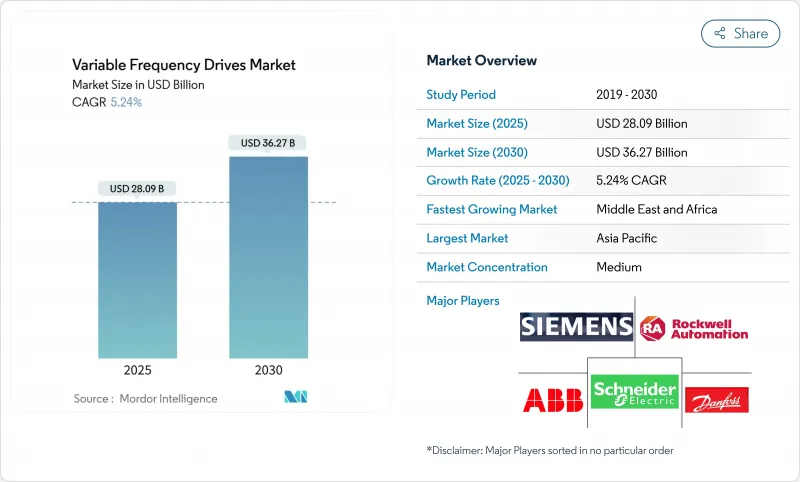

可変周波数ドライブの世界市場規模は、2025年に280億9,000万米ドルとなり、2030年には362億7,000万米ドルに達し、CAGR 5.24%で成長すると予測されています。

モーターレベルの効率化を求める強い政策圧力、省エネルギーによる迅速な投資回収、生産ラインのデジタル化への移行により、採用の裾野は着実に広がっています。資本支出サイクルが厳しくなっても需要は底堅く、これはVFDの改修がエネルギー多消費型プラントの電力コストを即座に削減するからです。鉱業や金属業界における中電圧アップグレードプロジェクト、中東における海水淡水化施設建設、商業ビルにおけるHVAC効率化義務化などが、まとめて対応可能な機会を拡大した。イーサネット、サイバーセキュリティ機能、シリコンカーバイドスイッチングデバイスをポートフォリオに組み込んだサプライヤーは、マージンを保護し、サービス収益を確保しました。SiC/GaNチップの不足と電磁干渉コンプライアンスコストの上昇に伴う逆風は、出荷台数の伸びをやや抑制したもの、複数年にわたる効率化投資の流れを頓挫させることはありません。

世界の可変周波数ドライブ市場動向と洞察

モーターレベルのエネルギー最適化を求めるデジタルネイティブなプロセスプラント

デジタル設計のプラントでは、生産スケジュールとリアルタイムの電力価格に合わせてモータ負荷を調整するために、最新のVFD内部の予測分析に依存しています。例えば、ロックウェル・オートメーションのPowerFlex 755TSプラットフォームは、エッジ解析をバンドルし、複数のモータライン全体でエネルギー使用量を削減しながら、ダウンタイムの削減を実現しました。半導体製造と製薬施設は、歩留まりが正確な速度制御と中断のないサービス接続に依存するため、採用をリードしました。

HVACおよび水分野での可変トルク効率規則の義務化

効率化に関する法規制により、ポンプやエアハンドリングユニットにVFDの統合は譲れないものとなりました。米国エネルギー省の2028年サーキュレーターポンプ規則では、高度なドライブと組み合わせた電子整流モーターが義務付けられました。それを見越して、TraneなどのOEMはDanfossと複数年の購入契約を結び、準拠したVFDの供給を保証しました。

690Vを超えるEMI/高調波コンプライアンスコストの上昇

規制当局が690V以上の設備に対するIEEE 519の制限を強化したため、電磁干渉と高調波歪みに関連するコンプライアンス・コストが急増しました。中電圧プロジェクトでは、特大リアクトル、マルチパルス変圧器、シールドケーブルが必要となり、材料費、試運転費、エンジニアリング費が追加され、設置されたドライブのコストが15%以上上昇する可能性があります。小規模メーカーは、設計と認証のオーバーヘッドをより少ない出荷量に分散しなければならないため、不釣り合いな影響を受け、新規参入を抑制し、統合を加速させる可能性があります。

セグメント分析

1kV未満の低電圧ユニットは、中小規模の工場でコンベア、ミキサー、HVACファンを制御する主力製品であり続けた。2024年には62.4%の売上を獲得し、可変周波数ドライブ市場を支えます。費用対効果の高い設置、豊富なインテグレーターの専門知識、豊富なサプライヤー・カタログがシェアを維持した。並行して、製鉄所や地下鉱山のブラウンフィールド拡張により、調達は1~6kVソリューションにシフトし、中電圧層のCAGRは6.8%となりました。995 V送電網にアップグレードする鉱山では、ケーブルの引き回しを制限し、電圧の安定性を向上させるために、専用のドライブが選択されました。

中電圧機器の可変周波数ドライブ市場規模は、2030年までに104億米ドルに達すると予測され、高調波緩和のためのグリッドコード要件を高める再生可能エネルギーインフィードから恩恵を受けています。ベンダーは、全高調波歪みを3%未満に抑える耐アーク性筐体やモジュール式アクティブ・フロントエンド設計でこれに対応しました。6 kVを超える高電圧製品は、ニッチなハイドロポンプや圧延機プロジェクトに対応したが、割高な価格と設置の複雑さにより、その普及は限定的でした。

20 kW未満の超小型ドライブは、工場が自律移動ロボットやスマートビルディングサブシステムに小型モーターを組み込んで分散制御を採用したため、CAGRが最高となる7.2%を記録しました。センサーの多いHVACゾーニングや食品加工用フィーダーと連動して出荷台数も増加しました。低電力(20~200kW)モデルは依然として2024年の売上高の40.3%を支えており、化学および水事業の遠心ポンプと軸流ファンに不可欠であることを証明しています。

開発者は、ヒートシンクの容量を拡大し、SiCダイオードに切り替えて、砂漠の太陽電池分野での差別化要因である60℃を超える周囲温度での動作限界を引き上げました。600 kWを超えるハイパワークラスの可変周波数ドライブ市場シェアは5%未満にとどまったが、パワーモジュールのリレーや高調波フィルタの監査などの長期サービス契約を通じて、販売ごとに大きなアフターマーケット収益がもたらされました。

可変周波数ドライブ市場レポートは、電圧タイプ(低電圧、中電圧、高電圧)、電力定格(マイクロ、低、中、高)、ドライブタイプ(ACドライブ、DCドライブ、サーボ/ベクトルドライブ、その他)、用途(ポンプ、ファン、ブロワー、その他)、エンドユーザー産業(インフラとビル、食品と飲料加工、その他)、地域(北米、南米、その他)で区分されています。

地域分析

アジア太平洋は2024年の売上高の46.3%を占め、首位を維持した。これは中国の自動化された家電工場と、モーターの効率改修を奨励するインドの生産連動インセンティブ制度に支えられたものです。VEICHIのような現地のチャンピオンは、クラウドゲートウェイをバンドルして継続的に監視することで輸出販売を拡大し、地域のコスト競争力を強化しました。いくつかのASEAN諸国では政府のリベート制度とIE3モータ義務化政策がベースライン需要を維持し、台湾と韓国の半導体工場ではサーボドライブの受注が加速しました。

中東・アフリカでは、海水淡水化パイプラインと銅ベルト鉱山の電化により、高い耐衝撃性を持つ頑丈な中電圧ドライブが必要とされたため、CAGR見通しで最高の7.3%を記録しました。ACCIONAのShuqaiq 3マイルストーンは、水の安全保障の必要性が数メガワットのポンプドライブ契約を生み出すことを浮き彫りにしました。アフリカの公益事業会社は、資本に制約があるもの、開発金融機関を利用してVFDを多用した水処理アップグレードの資金を調達し、地域の受注を拡大しました。

北米と欧州では、古い設備が耐用年数を迎え、効率化規制が強化されたことで、更新サイクルが着実に伸びています。電力会社のリベート制度や企業のESG目標が採用を早め、特に料金値上げが積極的な脱炭素化目標に合致しました。欧州の粉末冶金工場では、高調波規制を満たすためにアクティブ・フロントエンド・ドライブが採用され、米国中西部の化学工場では、予測VFDアルゴリズムでモーター負荷を調整することにより、天然ガス価格の変動を利用しました。サイバーセキュリティの強化要件は、入札評価期間を延長したが、最終的には、パッチ管理とセキュリティ証明書の更新パッケージを提供するベンダーのサービス収益を拡大した。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- モーターレベルのエネルギー最適化が求められるデジタルネイティブなプロセスプラント

- HVACと水分野における可変トルク効率規則の義務化

- インダストリー4.0レトロフィット向け低遅延イーサネット対応モーターの急増

- 海水淡水化と水再利用インフラの急速な整備(中東中心)

- 坑内掘車両の電化

- インフレに連動する電気料金がVFD改修のROIを加速させる

- 市場抑制要因

- 690Vクラス以上のEMI/高調波対応コストの上昇

- 発展途上国の公益事業における設備投資の抑制

- レガシードライブのリフレッシュサイクルを遅らせるサイバーハードニング費用

- パワーエレクトロニクスグレードのSiC/GaNチップの持続的不足

- マクロ経済要因の影響

- 投資分析

- バリューチェーン分析

- 規制情勢

- 技術スナップショット

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 電圧タイプ別

- 低電圧(1 kV未満)

- 中電圧(1-6 kV)

- 高電圧(6 kV超)

- 定格出力別(kW)

- マイクロ(20未満)

- 低(20-200)

- 中(200-600)

- 高(600超)

- ドライブタイプ別

- ACドライブ

- DCドライブ

- サーボ/ベクトル・ドライブ

- マルチレベルおよびマトリックス・ドライブ

- 用途別

- ポンプ

- ファンとブロワー

- コンプレッサー

- コンベヤ

- HVACシステム

- 押出機と混合機

- エンドユーザー業界別

- インフラと建物

- 飲食品加工

- エネルギー・発電

- 石油・ガス・石油化学

- 鉱業および金属

- パルプ・紙

- 上下水道

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Danfoss A/S

- Rockwell Automation Inc.

- Mitsubishi Electric Corporation

- Yaskawa Electric Corporation

- Fuji Electric Co. Ltd.

- Eaton Corporation plc

- WEG Industries S.A.

- Nidec Corporation

- Toshiba Corporation

- Hitachi Ltd.

- Johnson Controls International plc

- Inovance Technology Co. Ltd.

- Delta Electronics Inc.

- Emerson Electric Co.

- LS Electric Co. Ltd.

- SEW-Eurodrive GmbH & Co KG

- Veichi Electric Co. Ltd.

- Control Techniques(Nidec)

- HARS Drives Co. Ltd.

- Vacon(Part of Danfoss)

- Parker Hannifin-SSD Drives

- Kollmorgen Corporation

- Bonfiglioli Riduttori S.p.A.