|

市場調査レポート

商品コード

1851490

ヘキサメチレンジアミン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Hexamethylenediamine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘキサメチレンジアミン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月11日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

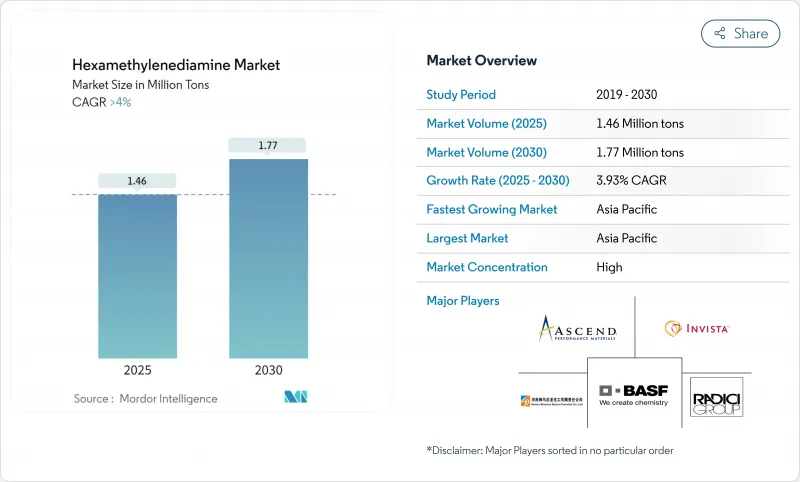

ヘキサメチレンジアミン市場規模は2025年に146万トンと推定され、予測期間(2025-2030年)のCAGRは4%を超え、2030年には177万トンに達すると予測されます。

需要の強さはナイロン6,6の生産に根ざしている一方、アジポニトリルからヘキサメチレンジアミンへの連鎖における生産能力の制約が、アジア太平洋、北米、欧州での新たな投資の引き金となっています。軽量自動車部品への戦略的注力、パンデミック後のテクニカル・テキスタイルの復活、エポキシ硬化剤などの特殊用途の着実な普及が、生産量の拡大を支えています。生産者は、垂直統合を加速させ、低コストと排出量削減を約束するバイオベースの原料を試験的に導入することで、最近の供給ショックに対応してきました。同時に、原油に連動した原料の不安定性、REACH主導のアミン排出制限、バイオルートのスケールアップリスクなどが、先行きの見通しを弱めています。

世界のヘキサメチレンジアミン市場の動向と洞察

自動車軽量化部品におけるナイロン66の消費増加

自動車の軽量化目標がナイロン66の採用を加速しており、川下への浸透がヘキサメチレンジアミン市場を押し上げています。自動車メーカーは、ポリアミドの強度対重量比、耐熱性、リサイクル性を高く評価しており、特に質量が航続距離に直接影響する電池式電気自動車ではその傾向が顕著です。アジア太平洋地域のOEMは、ポリアミドの生産能力増強と並行して、ナイロンのインテークマニホールドと構造部材の使用を拡大し、地域間のバランスを強化し、総合サプライヤーに報酬を与えています。北米では、ティア1のサプライヤーが、ターボチャージングの熱負荷に対応するため、ナイロン6,6を中心にエンジンベイ部品を再設計しています。したがって、材料の代替動向は、単なる循環的な需要増加ではなく、構造的な需要増加をもたらしています。

アジポニトリルからHMDへの急速な能力増強

2024年の供給ショックは、少数のアジポニトリルユニットへの依存を露呈させました。生産者は、中国、メキシコ湾岸、西欧でアジポニトリルーヘキサメチレンジアミンの生産能力を増強するために、ボトルネック解消とグラスルーツラインを推進することで対応しました。インビスタのメイトランド再稼働とアセンドのアラバマでの年産90トンの増設は、この動向を象徴しています。この波は、原料の逼迫を緩和する一方で、短期的な供給過剰と地域的な価格変動を加速させるリスクもはらんでいます。それでも、大半のオペレーターは、川下のナイロン経済性を守り、アジア中心の最終用途クラスターにおける近接優位性を獲得するために、設備投資は正当化されると考えています。

原油由来アジポニトリル価格の変動性

アジポニトリルは原油とナフサのスプレッドに連動するため、上流の価格変動はヘキサメチレンジアミンの契約決済に迅速に伝わり、統合されていないプレーヤーを圧迫します。2015年の中国のプラント事故は集中リスクを浮き彫りにし、その後の製油所の操業停止はスポット・プレミアムの幅を広げました。輸入の多い欧州は変動を最も敏感に感じ取り、ナイロン紡績の専業メーカーにマージン圧力を強めています。ユーロ安はドル建ての原料を高騰させ、競争力をさらに低下させる。これらの要因は、バックインテグレーションプロジェクトに拍車をかけ、原油の変動からコストを切り離すバイオルートへの関心を強めています。

セグメント分析

2024年のヘキサメチレンジアミン市場では、ナイロン生産が78.19%のシェアを占める。このセグメントの生産量は114万トンで、自動車ボンネット下部品とカーペット繊維に支えられています。このプールは、予測期間中最大の絶対需要増を支えるが、CAGRは3.68%にとどまる。対照的に、エポキシ硬化剤や殺生物剤中間体などの特殊用途は5.05%のペースで拡大し、ヘキサメチレンジアミン市場規模に占めるシェアを2025年の25万トンから2030年には32万トンに引き上げます。

利益率の高いニッチ分野への多角化により、ナイロン価格サイクルに対する収益エクスポージャーが軽減されます。生産者は製剤化可能なグレードを供給することで、顧客の認定時間を短縮し、スイッチング・コストを強化します。また、このアプローチは既存の精製トレインを活用するため、追加的な設備投資額は収益に比して低く抑えられます。その結果、特殊グレードの普及は、全地域でベースポリマーの伸びを上回り続けると予想されます。

ヘキサメチレンジアミン市場レポートは、用途(ナイロン生産、コーティング用中間体、殺生物剤、その他の用途(硬化剤、潤滑剤など))、エンドユーザー産業(繊維、プラスチック、自動車、その他のエンドユーザー産業(塗料・コーティング、石油化学など))、地域(アジア太平洋、北米、欧州、南米、中東・アフリカ)で区分されています。

地域分析

アジア太平洋地域のヘキサメチレンジアミン市場におけるシェア52.06%は、中国の精製からナイロンまでの一貫したエコシステムと、同地域の自動車および繊維セクターの拡大を反映しています。この地域の需要はCAGR 4.96%で増加し、2025年の76万トンから2030年には97万トン近くまで増加します。政府は先端材料クラスターを推進しており、アジピン酸原料に近接しているため供給ラインが短縮されます。上海におけるインビスタの17億5,000万人民元の生産能力倍増のような投資は、現地のサプライチェーンを強化し、競争力を強化します。

北米のシェアは、シェールオイルに有利な原料と自動車用樹脂の需要に支えられています。しかし、輸入品とのコスト競争や、最近の大手生産者の破産手続きは、価格サイクルに対する脆弱性を浮き彫りにしています。生産者は高純度グレードとバイオベースグレードを重視し、マージンを確保し、電子機器や医療用OEMからの引き取りを確保しています。

欧州は持続可能性と特殊ニッチに注力しています。BASFの年産260キロの新フランス工場は、先進的な精製とエネルギー効率の高い反応器を統合し、強化される脱炭素指令に対応しています。アミン排出に関するREACH規制は他地域より厳しく、コンプライアンス・コストを引き上げているが、現地生産に価格競争力のない堀を提供しています。

南米と中東・アフリカの両地域は、競争力のあるガス経済と拡大する下流プラスチック需要を活用しています。ブラジルの自動車生産回復とサウジアラビアの化学多角化イニシアチブは、小規模な基盤からではあるが、この地域のHMDユニットに活路を開きます。政治的・物流的リスクにより、アジア太平洋に比べれば成長は緩やかだが、国境を越えたジョイント・ベンチャーが、こうしたフロンティアの生産量を開拓しようとしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 軽量自動車部品におけるナイロン66の消費拡大

- アジポニトリルからHMDAへの急速な能力増強

- バイオベースのアジポニトリル原料へのシフト

- ヘキサメチレンジアミンベースのエポキシ硬化剤の出現

- 繊維産業におけるヘキサメチレンジアミンの需要拡大

- 市場抑制要因

- 原油由来アジポニトリル価格の変動性

- バイオベースのヘキサメチレンジアミン技術のスケールアップリスク

- アミン排出に対する厳しいREACH規制

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 用途別

- ナイロン生産

- コーティング中間体

- 殺生物剤

- その他の用途(硬化剤、潤滑剤など)

- グレード別

- 標準産業グレード

- 高純度グレード

- バイオベースグレード

- 最終用途産業別

- 自動車

- テキスタイル

- プラスチック

- その他のエンドユーザー産業(塗料・コーティング、エレクトロニクスなど)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- タイ

- インドネシア

- ベトナム

- マレーシア

- フィリピン

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- トルコ

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ナイジェリア

- エジプト

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Ascend Performance Materials

- BASF

- Cathay Biotech Inc.

- Dow

- DOMO Chemicals

- Evonik Industries AG

- Genomatica Inc.

- INVISTA

- Radici Partecipazioni SpA

- Solvay

- Shenma Industrial Co. Ltd

- Spectrum Chemical

- Thermo Fisher Scientific Inc.