|

市場調査レポート

商品コード

1637773

ジルコニウム-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Zirconium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ジルコニウム-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

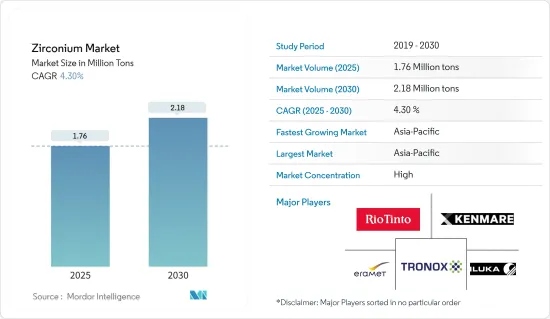

ジルコニウム市場規模は2025年に176万トンと推定され、2030年には218万トンに達すると予測され、予測期間(2025~2030年)のCAGRは4.3%です。

COVID-19の感染者数が急増したため、多くの国が閉鎖措置に踏み切り、世界経済に大きな影響を与えました。経済・産業活動が一時的に停止したため、ジルコニウム市場は鉄鋼、セメント、エネルギー・化学、セラミックなどのエンドユーザー産業からの生産と需要の両面で影響を受けました。しかし、原子力資源開発への注目が高まっていることから、予測期間中に市場はプラス成長を遂げることが期待されます。

主要ハイライト

- 中期的には、鋳造と耐火物の成長、アジア太平洋における原子力発電所の増加、表面コーティングの使用加速が市場成長の主要要因です。

- 一方、ジルコンへの依存度が低下していることは、市場の成長を大きく妨げる可能性が高いです。

- 整形外科用の医療セグメントでのジルコニウム需要の高まりと、自動車産業に関する厳しい排出基準が、調査した市場に機会をもたらすと予想されます。

- 中国が市場全体の収益の大部分を占めており、予測期間中に最も速いCAGRを示すことが期待されています。

ジルコニウム市場の動向

ジルコン粉/砂からの需要の増加

- ジルコンは、あらゆる有機と無機砂結合剤と結合する能力、低酸性、低熱膨張係数、高温での高い空間安定性、高温での化学的安定性、良好なリサイクル性などの様々な特性により、主に砂や粉(粉砕砂)の形でセラミックや鋳造に広く使用されています。

- セラミックでは、ジルコンサンドは、不透明化のための高い屈折率など、その非常に価値のある特性のために使用されます。セラミック本体やガラス母材に高い機械的強度、靭性、耐久性を付与する能力などの付随的な利点は、確立された特性であり、セラミック産業の特定のセグメントで用途を見つけることを可能にし、それによってこれらの特性を好む市場に対応しています。

- 鋳造用途では、砂型鋳造、インベストメント鋳造、コスワース鋳造(アルミニウム)用の成形母材として広く使用されています。また、他の鋳物砂の濡れ性を低下させるため、ダイカストや耐火物の塗料や洗浄の金型コーティングとしても使用されます。

- ジルコン砂は金型や中子の製造に使用され、その耐火性、低膨張性、溶鋼による濡れ性の低減、高熱伝導性により、珪砂よりも大きな利点があります。

- ジルコン鋳造砂は、より良い金属仕上げ、「バーンオン」の可能性の低減、金属凝固の改善をもたらします。金属の浸透に対する抵抗力を高め、鋳物に均一な仕上がりを与えます。

- 前述の要因から、ジルコン粉/砂の需要は予測期間中に伸びると予想されます。

市場を独占する中国

- 中国はジルコニウムの世界市場シェアを独占しており、現在のシナリオでは最も急速に成長している原子力エネルギーの消費国として人気を集めています。原子力資源開発への関心が高まっていることから、ジルコニウムの需要が増加すると予想されます。

- 中国は世界最大の鉄鋼生産国です。世界鉄鋼協会が発表した報告書によると、中国は世界の鉄鋼生産量全体の53%(1950.5トン)を占めています。さらに、2021年には、中国政府は、合計粗鋼生産能力2,933万トン/年の43の新しいEAFの建設を承認しました。したがって、新しい鉄鋼プラントの建設は耐火物市場を牽引し、それによって国内のジルコニウム消費量を増加させる可能性が高いです。

- インフラ整備のペースが速まるにつれて、中国では住宅や商業用ビルが増加しています。このため、セメント産業や鉄鋼産業における耐火物需要が増加し、市場の研究が進むと予想されます。

- 中国は現在、最も急速に成長している原子力エネルギーの消費国として人気を集めています。同国には運転可能な原子炉が50基あり、その合計容量は47,518MWです。原子力資源開発への注目が高まるにつれ、ジルコニウムの需要も増加すると予想されます。

- 中国の原子力研究イニシアティブによると、2035年までに原子力発電所の稼働は約180GWに達するはずです。したがって、原子力発電の生産能力の増加は、同国におけるジルコニウムの消費を増加させる可能性が高いです。

- 耐火物やセラミックなどの産業の成長は、予測期間中の市場調査を促進すると予想されます。

ジルコニウム産業概要

世界のジルコニウム市場は統合されており、上位5社が世界消費の主要シェアを占めています。ジルコニウム消費の大半はアジア太平洋と欧州です。市場の主要参入企業は、Iluka Resources Limited、Rio Tinto、Tronox Holdings PLC、Kenmare Resources PLC、Erametなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋における原子力発電所の成長

- 鋳造と耐火物における安定した成長

- 表面コーティングでの使用加速

- 抑制要因

- ジルコンへの依存度の低下

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 輸出入

- 貿易規制施策分析

- 価格動向

第5章 市場セグメンテーション(市場規模(数量ベース))

- 産出タイプ

- ジルコン

- ジルコニア

- その他

- 用途

- ジルコン粉/粉砕砂

- ジルコン不透明化剤

- 耐火物(ジルコニア)

- ジルコン化学品

- ジルコン金属

- 地域

- 生産

- オーストラリア

- ブラジル

- 中国

- インド

- インドネシア

- 南アフリカ

- ウクライナ

- その他

- 消費

- 中国

- 米国

- 日本

- 欧州連合

- インド

- ロシア

- その他

- 生産

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析

- 主要企業の戦略

- 企業プロファイル

- Australian Strategic Materials Ltd

- Base Resources Limited

- Binh Dinh Minerals Company

- Doral Mineral Sands Pty Ltd

- Eramet

- Iluka Resources Limited

- INB

- Kenmare Resources PLC

- Lanka Mineral Sands Limited

- MZI Resources Ltd

- Rio Tinto

- Tronox Holdings PLC

第7章 市場機会と今後の動向

- 医療セグメント、特に整形外科インプラントでの用途拡大

- 自動車に関する厳しい排出基準

The Zirconium Market size is estimated at 1.76 million tons in 2025, and is expected to reach 2.18 million tons by 2030, at a CAGR of 4.3% during the forecast period (2025-2030).

A sharp increase in the number of COVID-19 cases led to numerous countries resorting to lockdowns, which significantly affected the global economy. The economic and industrial activities came to a temporary halt, which led the zirconium market to witness repercussions in terms of both production and demand from end-user industries, such as iron and steel, cement, energy and chemicals, and ceramics. However, the increasing focus on developing nuclear power resources is expected to help the market achieve positive growth during the forecast period.

Key Highlights

- Over the medium term, the major factors driving the market's growth are the growth in foundries and refractories, the increasing number of nuclear power stations in Asia-Pacific, and the accelerating usage of surface coatings.

- On the other hand, the reducing dependence on zircon is likely to hinder the growth of market significantly.

- The rising demand for zirconium in the healthcare sector for orthopedics and stringent emission standards pertaining to the automotive industry are expected to create the opportunities for the market studied.

- China dominated the market studied, accounting for a major share of the total revenue, and it is expected to witness the fastest CAGR over the forecast period.

Zirconium Market Trends

Increasing Demand from Zircon Flour/Sand

- Zircon is widely used in ceramics and foundry, mostly in the form of sand and flour (milled sand), due to its various properties, such as the ability to bind with all organic and inorganic sand binders, low acidity, low thermal expansion coefficient, and high spatial stability at increased temperatures, chemical stability at high temperatures, and good recyclability.

- In ceramics, zircon sand is used for its highly valuable properties, such as its high refractive index for opacification. Its ancillary benefits, including its ability to impart greater mechanical strength, toughness, and durability to ceramic bodies and glass matrices, are established attributes and enable it to find applications in specific segments of the ceramic industry, thereby catering to markets with a preference for these attributes.

- In foundry applications, it is used widely as a molding base material for sand casting, investment casting, and Cosworth casting (aluminum). It is also used as a mold coating in die casting and refractory paints and washes, as it reduces the wettability of other foundry sands.

- Zircon sand is used for mold and core manufacturing, where its refractoriness, low expansion, reduced wettability by molten steel, and high thermal conductivity offer significant advantages over silica sand.

- Zircon foundry sands produce a better metal finish, a lesser likelihood of 'burn-on,' and improved metal solidification. It increases the resistance to metal penetration and imparts a uniform finish to the casting.

- Owing to the aforementioned factors, the demand for zircon flour/sand is expected to grow over the forecast period.

China to Dominate the Market

- China dominated the global market share for zirconium, and it is gaining popularity as the fastest-growing consumer of nuclear energy in the present scenario. The increasing focus on developing nuclear power resources is expected to increase the demand for zirconium.

- China is the largest steel producer in the world. According to the report published by World Steel Association, China accounted for 53% of the overall production of steel in the world, which is 1950.5 metric tons. Additionally, in 2021, the Chinese government approved the construction of 43 new EAFs with a total crude steel capacity of 29.33 million mt/year. Thus, the construction of new steel plants is likely to drive the market for refractories, thereby increasing the consumption of zirconium in the country.

- The increased pace of infrastructural activities has led to an increase in residential and commercial buildings in China. This is expected to drive the demand for refractories in the cement and iron steel industries, thereby driving the market studied.

- China is currently gaining popularity as the fastest-growing consumer of nuclear energy. The country has 50 operable nuclear reactors, with a combined net capacity of 47,518 MW. The increasing focus on the development of nuclear power resources is expected to increase the demand for zirconium.

- According to China's Atomic Energy Research Initiative, by 2035, nuclear plants operation should reach around 180 GW. Thus, increasing nuclear power production capacities is likely to increase the consumption of zirconium in the country.

- The growth in industries, such as refractories and ceramics, is expected to drive the market studied in the forecast period.

Zirconium Industry Overview

The global zirconium market is consolidated, with the top five companies accounting for major shares of global consumption. Most of the consumption of zirconium is in the Asia-Pacific region and Europe. The major players in the market include Iluka Resources Limited, Rio Tinto, Tronox Holdings PLC, Kenmare Resources PLC, and Eramet.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth of Nuclear Power Stations in the Asia-Pacific

- 4.1.2 Consistent Growth in Foundries and Refractories

- 4.1.3 Accelerating Usage in Surface Coatings

- 4.2 Restraints

- 4.2.1 Reducing Dependence on Zircon

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Import and Export

- 4.5.1 Trade Regulatory Policy Analysis

- 4.5.2 Price Trends

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Occurrence Type

- 5.1.1 Zircon

- 5.1.2 Zirconia

- 5.1.3 Other Occurrence Types

- 5.2 Applications

- 5.2.1 Zircon Flour/Milled Sand

- 5.2.2 Zircon Opacifier

- 5.2.3 Refractories (Zirconia)

- 5.2.4 Zircon Chemicals

- 5.2.5 Zircon Metal

- 5.3 Geography

- 5.3.1 Production

- 5.3.1.1 Australia

- 5.3.1.2 Brazil

- 5.3.1.3 China

- 5.3.1.4 India

- 5.3.1.5 Indonesia

- 5.3.1.6 South Africa

- 5.3.1.7 Ukraine

- 5.3.1.8 Rest of the World

- 5.3.2 Consumption

- 5.3.2.1 China

- 5.3.2.2 United States

- 5.3.2.3 Japan

- 5.3.2.4 European Union

- 5.3.2.5 India

- 5.3.2.6 Russia

- 5.3.2.7 Rest of the World

- 5.3.1 Production

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Australian Strategic Materials Ltd

- 6.4.2 Base Resources Limited

- 6.4.3 Binh Dinh Minerals Company

- 6.4.4 Doral Mineral Sands Pty Ltd

- 6.4.5 Eramet

- 6.4.6 Iluka Resources Limited

- 6.4.7 INB

- 6.4.8 Kenmare Resources PLC

- 6.4.9 Lanka Mineral Sands Limited

- 6.4.10 MZI Resources Ltd

- 6.4.11 Rio Tinto

- 6.4.12 Tronox Holdings PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Usage in the Healthcare Sector, Especially Orthopedic Implants

- 7.2 Stringent Emission Standards Pertaining to Automotive