インターベンショナル、カーディオロジー機器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Interventional Cardiology Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1850223

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

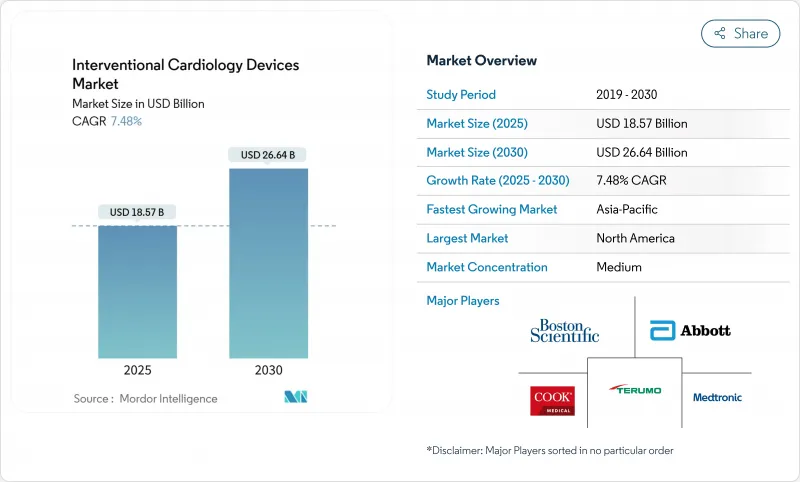

インターベンショナル、カーディオロジー機器市場は2025年に185億7,000万米ドルを生み出し、2030年には266億4,000万米ドルに達すると予測され、CAGRは7.48%を記録します。

現在の成長は、薬剤溶出ステント、血管内結石破砕(IVL)システム、AI強化イメージングに依存する低侵襲手技の活発な取り込みによって支えられています。冠動脈疾患(CAD)の世界的な負担の拡大は、即日退院パスウェイや外来手術センター(ASC)の採用とともに、対応可能な患者プールを拡大し続けています。規制当局や医療提供者が長期的な安全性と持続可能性を重視するようになり、製品パイプラインはより細いストラット、生体吸収性プラットフォームへとシフトしています。大手メーカーが差別化技術の追加やサプライチェーンの強化を目的とした買収を進める中、競合の激しさは増しています。規制当局による監視の強化、労働力不足、材料に関する法規制が逆風となっているが、市場の上昇軌道を狂わせるまでには至っていないです。

世界のインターベンショナル、カーディオロジー機器市場の動向と洞察

CADおよびPCI手技の普及率の高まり

CADは依然として世界的な死亡原因のトップであり、米国だけでも2,000万人以上の成人が罹患しています。高齢化、肥満、座りがちなライフスタイルにより、特にIVL療法が有効な多枝病変や複雑な石灰化病変に対するPCI需要が増加しています。アジア太平洋市場は、都市化によって食生活や活動パターンが変化しているため、最も急増しています。CADは慢性疾患として管理されているため、再手術が手技件数の大部分を占めるようになり、単発の治療を超えて機器の利用が持続しています。

加速する低侵襲治療へのシフト

病院と支払者は、入院期間を短縮し合併症を減少させる経皮的アプローチを好んでいます。COVID-19の大流行はこの嗜好を強め、薬剤溶出性バルーンや生体吸収性スキャフォールドの採用を促進しました。AI支援画像は精度を高め、造影剤の負担を軽減し、かつて開腹手術のリスクが高いと判断された高齢者や合併症のある患者への適応を拡大します。

厳しい複数地域の規制経路

EUの医療機器規制は、より厳格な臨床データと市販後サーベイランスを要求し、市場投入までの時間とコンプライアンス・コストを増大させています。同時に米国では、いくつかのクラスi事象を受け、リコール監視が強化されています。地域によって要求が異なるため、メーカーは並行した承認プログラムの実施を余儀なくされ、中小のイノベーターに負担を強いています。

セグメント分析

冠動脈ステントは、経皮的インターベンションの持続的な需要に支えられ、2024年のインターベンショナル、カーディオロジー機器市場の41.35%を占め、最大の売上を生み出しました。IVLプラットフォームはまだ始まったばかりだが、2030年までのCAGRは11.25%と予測されます。IVL技術のインターベンショナル、カーディオロジー機器市場規模は、重度に石灰化した病変の経皮的治療がより頻繁に行われるようになるにつれて著しく拡大すると予測されます。極細ストラットの薬剤溶出ステントと次世代生体吸収性スキャフォールドは再狭窄を減少させ、血管の生理的治癒を促進します。ベアメタルステントは、現在では抗血小板二重療法を必要としない患者にのみ使用されています。PTCAバルーンとガイドワイヤーは安定した数量成長を維持し、薬剤コーティングバルーンは2024年にFDAからAgentプラットフォームが承認された後、ステント内再狭窄管理用として注目されるようになります。

IVUSカテーテルやOCTカテーテルなどの手技補助器具は、病変の評価を精緻化し、器具のサイジングを最適化するAIオーバーレイの恩恵を受ける。即座の歩行が可能な止血デバイスは、即日退院プロトコルに不可欠です。これらの技術革新は総体的に、手技の効率を高め、PCIの臨床的範囲を拡大します。

地域分析

北米は、広範な保険適用、強固な臨床研究ネットワーク、AIガイド下画像診断の急速な普及を背景に、2024年の売上高で41.82%を占め、インターベンショナル、カーディオロジー機器市場をリードしました。この地域はまた、FDAのリコールへの警戒やカテラボの人員不足が成長を抑制しているもの、ASCの採用や複雑なPCIに対する即日退院の先駆けとなっています。欧州は成熟しつつも技術革新に優しい地域であり、持続可能性への取り組みが生体吸収性足場や低炭素サプライチェーンを後押ししています。MDRのコンプライアンス・コストは小規模メーカーに重くのしかかっているが、ドイツとフランスでは次世代医療機器の早期人体使用が試験的に続けられています。

アジア太平洋地域は顕著な成長エンジンであり、予測CAGRは12.61%です。中国の公的保険拡大と病院建設ブームがPCI生産量を拡大し、インドの価格抑制環境が現地生産に支えられた費用対効果の高いDESプラットフォームを後押ししています。日本は承認プロセスが厳格であるため導入が遅れるが、承認が得られれば高価格で販売されます。韓国とオーストラリアは、高い手続き品質と早期のAI統合を示し、二次的イノベーションの拠点として位置づけられています。これらの動向は、地域の競争力学を再形成し、インターベンショナル、カーディオロジー機器市場における将来の収益プールを再分配することになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- CADおよびPCI処置の普及率の増加

- 低侵襲治療への移行を加速

- DES価格の継続的な下落によるアドレス可能プールの拡大

- AIを活用したPCI前画像診断と意思決定支援の導入

- 病院の当日退院とASC設定への移行

- 完全生体吸収性プラットフォームの持続可能性推進

- 市場抑制要因

- 厳格な複数地域規制経路

- 強力な第一選択薬物療法の利用可能性

- カテーテル検査室の人員とインターベンション心臓専門医の世界の不足

- ポリマーベースのDESサプライチェーンに課題をもたらす反プラスチック法

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- ライバル関係の激しさ

第5章 市場規模と成長予測

- 製品タイプ別

- 冠動脈ステント

- ベアメタルステント

- 薬剤溶出ステント

- 生体吸収性スキャフォールド

- カテーテル

- 血管造影カテーテル

- IVUS/OCTカテーテル

- PTCAガイドカテーテル

- PTCAバルーン

- ガイドワイヤー

- 止血および血管閉鎖デバイス

- 血管内結石破砕術(IVL)システム

- 冠動脈ステント

- エンドユーザー別

- 病院

- 外来手術センター

- 心臓カテーテル検査室

- 素材別

- コバルトクロム合金

- プラチナクロム合金

- ニチノール

- ポリマー/生体吸収性

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Abbott Laboratories

- Medtronic PLC

- Boston Scientific Corp.

- B. Braun Melsungen AG

- Terumo Corp.

- Biosensors International

- Biotronik SE & Co. KG

- Cardinal Health Inc.

- Cook Medical Inc.

- Koninklijke Philips N.V.

- Edwards Lifesciences Corp.

- Nano Therapeutics Pvt. Ltd.

- Shockwave Medical Inc.

- Merit Medical Systems

- Siemens Healthineers AG

- AngioDynamics Inc.

- C. R. Bard(BD)

- MicroPort Scientific Corp.

- Alvimedica

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日