|

市場調査レポート

商品コード

1850120

流体管理システム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Fluid Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 流体管理システム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月16日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

概要

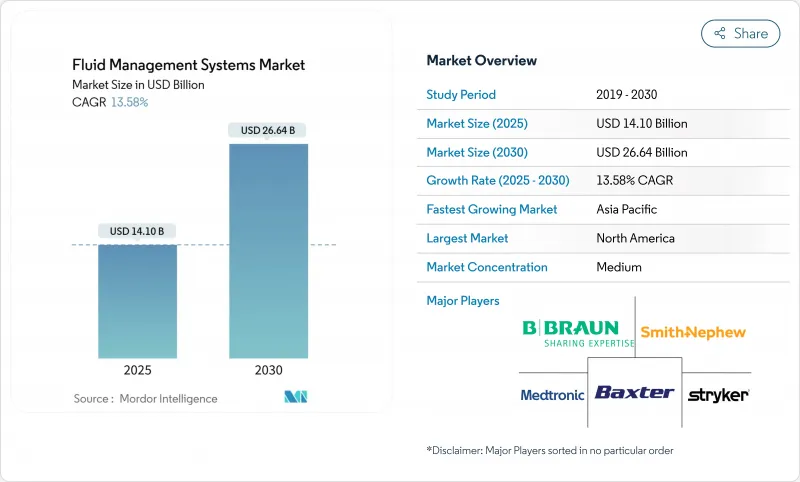

流体管理システム市場規模は、2025年に141億米ドルと推定され、予測期間(2025-2030年)のCAGRは13.58%で、2030年には266億4,000万米ドルに達すると予測されます。

急成長は、低侵襲手術量の増加、慢性腎臓病の有病率の増加、AI対応閉ループ限外ろ過プラットフォームの採用加速に起因します。病院は依然として主要な購入者であるが、ポータブル透析装置によって在宅治療が可能になるため、在宅医療の採用が急速に拡大しています。大手ベンダーがハードウェア、ソフトウェア、アナリティクスをバンドルしてエンド・ツー・エンドのソリューションを提供することで競合は激化しているが、外科医の人材不足と医療用ポリマーの供給制約が当面の利益を抑制する可能性があります。

世界の流体管理システム市場の動向と洞察

低侵襲手術の増加

低侵襲手術は現在、整形外科や一般外科のサービスラインの多くを占めており、鮮明な視界と安定した腔圧を維持できる灌流、吸引、気腹技術の需要が高まっています。外来手術センターは、ワークフローと文書化を合理化する統合流体管理プラットフォームを確保するため、医療技術ベンダーとの購買契約を標準化しています。AIを搭載した機器は、フローパラメーターをさらに最適化し、出血量のばらつきを抑えています。こうしたシフトが相まって、病院と外来施設の両方でハイスペックシステムの設置ベースが拡大しています。

慢性腎臓病とESRDの有病率の増加

慢性腎臓病は世界中で8億5,000万人以上の患者を罹患させており、透析導入量を増加させ、針のないコネクターと双方向データフィードを備えた新しいダイアライザー膜を必要としています。米国では2025年中に血液透析濾過が導入され、毒素クリアランスが改善されることが期待されています。このような進歩は、クリニックや在宅での透析に特化した体液管理プラットフォームに対する持続的な需要を支えています。

内視鏡訓練を受けた外科医の不足

2028年までに外科専門医が18%減少すると予測され、多くの地域で手技の遅れが生じています。地方の病院では人材の確保が難しく、高度な内視鏡流体システムの導入が制限され、利用率が低下しています。農村部は外科医不足の影響を不釣り合いに受けており、高度な流体管理技術へのアクセスが制限され、医療提供に地理的格差が生じています。最新の流体管理システムは複雑であるため、専門的なトレーニングが必要であるが、そのトレーニングはすべてのヘルスケア環境で容易に受けられるとは限らず、技術の進歩にもかかわらず導入率が制限される可能性があります。

セグメント分析

ダイアライザーは2024年の売上高の26.78%を占め、より広範な流体管理システム市場において腎代替療法が不可欠であることを反映しています。フレゼニウス・メディカル・ケアは2024年の売上高に215億ユーロを計上し、ダイアライザー製品の底堅さを確認しました。流体廃棄物管理システムは、廃棄の厳格化によって2030年までのCAGRが14.41%で上昇する見込みです。吸引器、吸引ユニット、輸液ウォーマーは、プロバイダーが低侵襲手術室に最新の安全基準を満たす温度制御、排煙対応のキットを装備するにつれて、安定した伸びを記録します。

AIセンサー、クラウドダッシュボード、モジュラーハブで構成されるロングテールの「その他製品」バケットは、予測アルゴリズムが測定可能なコスト削減を実現すれば、ソフトウェア中心のベンダーにシェアをシフトする可能性があります。ダイアライザーの消耗品は高い経常収益を享受しているのに対し、資本集約的なコンソールの交換サイクルは長く、各サブ市場における戦略的重要性が浮き彫りになっています。

カテーテルは、2024年の売上高の33.67%を占め、血管アクセス、灌漑、ドレナージなど、あらゆる場面での用途を反映しています。LSI素材、抗菌コーティング、耐変色性形状はプレミアムSKUを差別化し、病院の感染制御目標をサポートします。バルブはCAGR17.04%で今後の成長を牽引し、スマートポンプとシームレスに組み合わされる自動シャットオフや逆流防止設計に対する需要の高まりを反映しています。チューブセットと血液ラインは大量生産の定番品だが、圧力センサーとRFIDトラッキングをバンドルした統合キットへの価値移行が進行中です。

樹脂価格の高騰によりマージンが不安定になり、OEMはポリマーの二重調達やパッケージの再設計によるプラスチックの軽量化に取り組んでいます。EUの法規制がリサイクル可能性の閾値を引き上げているため、早期に配合を調整したサプライヤーは複数年の供給契約を締結し、流体管理システム市場でのシェアポジションを固めることができると思われます。

地域分析

北米は2024年の売上高の41.56%を占め、堅調な償還とAIモニターの早期導入が寄与しました。ボストン・サイエンティフィックの2025年第1四半期の売上高46億6,300万米ドルは、同地域の正確な灌流コントロールに依存するハイエンドの心血管ソリューションに対する意欲を裏付けています。FDAルールの整合化により、多施設展開の合理化が期待されるが、迫り来る外科手術の労働力不足が成長を抑制する可能性があります。

アジア太平洋地域は拡大の原動力であり、CAGR14.98%で前進しています。中国は三次病院を拡大し、インドは公的資金を透析クリニックに投入しています。規制の多様性により、市場参入経路のカスタマイズが必要であるが、規制当局が枠組みを近代化するにつれ、医療機器の承認は全体的に加速しています。

欧州では、成熟と持続可能性の両立が求められています。市販後調査やリサイクル可能な包装に関するEU指令は、部品設計を再構築し、ゆりかごから墓場までのコンプライアンスを検証できるメーカーを優遇しています。一方、ドイツとフランスでは地方分権政策により、移動式流体機器に依存する外来患者処置件数が増加しています。

中東・アフリカと南米は、絶対的な規模では後塵を拝しているが、非感染性疾患負担の増加とインフラプロジェクトが合致しているため、2桁台の成長ポケットを提供しています。為替変動と輸入関税は依然として逆風であり、サプライヤーは現地組立と戦略的販売代理店提携を推進し、流体管理システム市場のこれらのセグメントへの浸透を図っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 低侵襲手術件数の増加

- 慢性腎臓病と末期腎不全の罹患率の増加

- AI対応閉ループ限外濾過制御の導入

- 統合型液体廃棄物および使い捨て吸入システム

- ポータブル在宅透析液プラットフォームへの移行

- OR液体廃棄物コンプライアンスに関する規制の推進

- 市場抑制要因

- 内視鏡検査の訓練を受けた外科医の不足

- 統合プラットフォームの高資本コスト

- 使い捨てプラスチックに関する法律が消耗品コストを高騰させる

- 医療グレードのポリマーと樹脂の不安定な供給

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- ダイアライザー

- インサフレーター

- 吸引・灌漑システム

- 液体加温装置

- 体液廃棄物管理

- その他の製品

- 使い捨て用品とアクセサリー

- カテーテル

- ブラッドライン

- トランスデューサー

- バルブ

- チューブセット

- その他の使い捨て品

- 用途別

- 関節鏡検査

- 腹腔鏡検査

- 神経学

- 心臓病学

- 泌尿器科

- 歯科

- 消化器内科

- その他の用途

- エンドユーザー別

- 病院

- 外来手術センター

- 透析センター

- 専門クリニック

- 在宅ケア環境

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- B. Braun Melsungen AG

- Baxter International Inc.

- Becton, Dickinson & Co.

- Cardinal Health Inc.

- Hologic Inc.

- Johnson & Johnson

- Medtronic plc

- Smiths Medical(ICU Medical)

- Smith & Nephew plc

- Stryker Corp.

- Fresenius Medical Care AG & Co. KGaA

- Olympus Corp.

- Zimmer Biomet Holdings Inc.

- Arthrex Inc.

- AngioDynamics Inc.

- Ecolab(Skytron)

- Teleflex Inc.

- Nipro Corp.

- Asahi Kasei Corp.

- ConMed Corp.

- Karl Storz SE & Co. KG

- Boston Scientific Corp.