|

市場調査レポート

商品コード

1444783

ラボオンチップ・マイクロアレイ(バイオチップ)の世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Lab-on-a-chip and Microarrays (Biochip) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ラボオンチップ・マイクロアレイ(バイオチップ)の世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 134 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

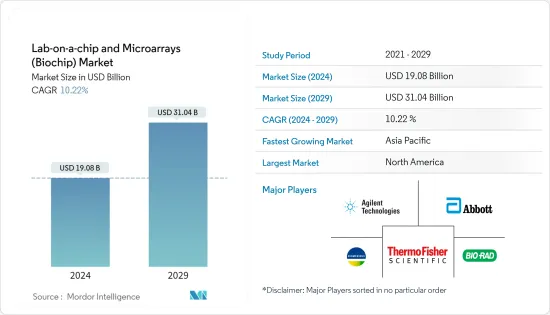

世界のラボオンチップ・マイクロアレイ(バイオチップ)の市場規模は、2024年に190億8,000万米ドルに達し、2024~2029年の予測期間中にCAGR 10.22%で成長し、2029年までに310億4,000万米ドルに達すると予測されております。

COVID-19のパンデミックは、ラボオンチップ・マイクロアレイ(バイオチップ)市場に大きな影響を与えました。たとえば、2021年1月にNature Communication誌に掲載された論文では、このマイクロアレイが診断ツールとして、COVID-19による疾患負担をより正確に推定するための疫学ツールとして、そして抗体を相関させるための研究ツールとして使用できる可能性があると報告されています。臨床結果を伴う反応。このように、COVID-19のパンデミックにより、ラボオンチップ診断ツールの需要が増加しました。ただし、現在のシナリオでは、他の慢性疾患や感染症の存在により、研究対象市場の需要は予測期間中に増加すると予想されます。

研究対象市場の成長を促進する要因は、ポイントオブケア検査の需要の増加、慢性疾患の発生率の増加、がん研究におけるプロテオミクスとゲノミクスの応用の増加です。ほとんどの市場関係者は、技術的に高度な新しい診断テストの開発に焦点を当てています。慢性疾患は、世界中で死亡および障害の主な原因となっています。たとえば、2022年 3月にジャーナルPlos Oneに掲載された記事では、インドの高齢者の21%が少なくとも1つの慢性疾患を患っていると報告しました。インドの高齢者における障害と死亡の主な原因は慢性疾患です。

同様に、2022年1月に欧州公衆衛生会議が発表した別の記事では、欧州では2030年までに300万人以上ががんに罹患すると報告されています。世界的に、慢性疾患(CD)が障害や疾病の主な原因であることがわかっています。これらの疾患は慢性であるため、正確かつタイムリーな臨床上の意思決定が必要とされます。この方向では、慢性疾患の診断のための新しいラボオンチップベースのPOCシステムの開発に向けた研究が新興分野となっています。したがって、慢性疾患の高い発生率が研究対象市場の成長を促進すると予想されます。

バイオチップは生物医学およびバイオテクノロジー研究の分野でますます使用されています。技術の進歩に伴い、プロテオミクスにおけるバイオチップの採用が増加しています。プロテインバイオチップの利点は、小型化傾向によりサンプル消費量が少ないことです。マイクロアレイのこれらの特性は、プロテオーム全体の分析にとって重要です。プロテオミクスは、バイオマーカーや創薬に広く採用されています。たとえば、2021年 4月、PathogenDx Inc.は、米国食品医薬品局が特許取得済みのCOVID-19多重ウイルス診断アッセイであるDetectX-Rvに対して緊急使用許可(EUA)を発行したと報告しました。 DetectX-Rvは、SARS-CoV-2綿棒からの核酸の定性的検出を目的としたRT-PCRおよびDNAマイクロアレイハイブリダイゼーションテストです。したがって、このような新製品の承認も研究対象市場の成長に貢献しています。

したがって、ポイントオブケア検査の需要の増加、慢性疾患の発生率の増加、がん研究におけるプロテオミクスとゲノミクスの応用の増加により、研究対象の市場は予測期間中に大幅な成長を遂げると予想されます。ただし、ラボオンチップ技術の設計上の制約と代替技術の利用可能性により、研究対象市場の成長が鈍化する可能性があります。

ラボオンチップ・マイクロアレイ(バイオチップ)の市場動向

ラボオンチップセグメントは予測期間中に大幅な成長が見込まれる

ラボオンチップ(LOC)セグメントは、慢性疾患の増加と技術の進歩により、市場のプラスの成長が見込まれています。また、個別化医療の導入やラボオンチップ技術の容易な利用も増加しており、世界中で同様の需要が高まると考えられます。また、LOCのさまざまなアプリケーションが急速に成長しています。粒子または細胞の検出、粒子パッキング、選別、電気泳動、PCRなどのための電極を備えたラボオンチップ装置が市販されています。

COVID-19の症例数の増加に伴い、この病気の治療と予防に関する研究研究の数も増えています。これにより、ラボオンチップの需要が高まりました。たとえば、2021年 1月、アルバータ大学の研究者は協力して、COVID-19抗体を迅速に検出するためのハンドヘルドLOCデバイスを開発しました。また、カリフォルニア大学アーバインの科学者らによって開発されたラボオンチップ技術を利用した低コストのイメージングプラットフォームは、コロナウイルスの迅速診断や抗体検査に利用できる可能性があります。

さらに、市場ではラボオンチップ(LOC)プラットフォームベースのイムノアッセイが頻繁に開発されています。このような高度なLOCプラットフォームには、マイクロ流体チップ、紙、側方流動、電気化学、および新しいバイオセンサーの概念が含まれます。ポイントオブケア診断に対する需要の急速な増加は、予測期間中にこの分野を推進すると予想される最も顕著な推進力です。たとえば、Onera Healthは2022年 2月に、ウェアラブルデバイス用の超低電力生体信号センサーサブシステムであるOnera Biomedical-Lab-on-Chipを発売しました。この生物医学用のコンパクトなチップは、複数の生体信号を処理するように設計されており、健康機器にとって大きなチャンスを生み出します。したがって、このような開発がこのセグメントの成長を推進しています。

したがって、慢性疾患の増加、技術の進歩の高まり、個別化医療の採用の増加、ラボオンチップ技術の容易なアクセスにより、このセグメントは予測期間中に大幅な成長を遂げると予想されます。

北米は予測期間中に大幅な成長が見込まれる

北米は、この地域の主要な市場プレーヤーの存在とヘルスケアインフラの発展により、予測期間中に大幅な成長を遂げると予想されます。さらに、この地域では、マイクロアレイ技術の研究開発に大規模な投資を行っているヘルスケア大手企業との大規模な協力活動も見られました。たとえば、Illumina Inc.は2022年 9月に、より高速で強力、より持続可能なシーケンシングを可能にする新しい量産規模のシーケンサーであるNovaSeq Xシリーズを発売しました。この革新的な新技術であるNovaSeq X Plusは、従来のシーケンサーの2.5倍のスループットである年間20,000以上の全ゲノムを生成することができ、ゲノムの発見と臨床的洞察を大幅に加速して疾患を理解し、最終的に患者の生活を変革します。したがって、この地域のこのような発展は、研究対象市場の成長を推進しています。

ポイントオブケア(POC)診断の分野でも、リソースが限られた環境で、分子診断、感染症、慢性疾患などのさまざまな用途にマイクロ流体技術が広く使用されています。たとえば、ジャーナル「Frontiers of Bioengineering and Biotechnology」に2021年1月に掲載された記事では、ラテラルフローアッセイ(LFA)がPOC検査で広く使用されており、特定のバイオマーカーを同定することでがんなどの病気の診断や予後診断に使用できると報告しました。 LFAは、抗体および核酸の増幅を介して一連の病原体およびタンパク質を検出するために広く使用されています。したがって、マイクロ流体工学の研究における最新の進歩は、自己完結型で自動化され、使いやすく、迅速な統合デバイスを製造することを目的としています。

さらに、この地域で報告されている慢性疾患の発生率が高いことも、この部門の成長に貢献しています。たとえば、2021年11月に発表されたカナダのがん統計によると、2021年に推定22万9,200人のカナダ人ががんと診断されたと報告されています。同様に、国際糖尿病連盟(IDF)が発表した2021年によると、メキシコの成人は推定1,400万人でした。糖尿病とともに生きています。したがって、この地域で慢性疾患を抱えて暮らす人々の数がこれほど多いことも、この地域で研究対象となっている市場の成長に貢献しています。

ここ数年、米国では学術研究におけるハイスループットスクリーニング(HTS)技術への関心が大幅に高まっています。たとえば、2022年 10月に、Ginkgo Bioworksはメルクと提携し、メルクの医薬品有効成分(API)製造の取り組みで生体触媒として使用できる最大4つの酵素を開発しました。この提携を通じて、Ginkgoは細胞工学および酵素設計における豊富な経験に加え、自動ハイスループットスクリーニング、製造プロセス開発/最適化、バイオインフォマティクス、および分析における能力を活用して、標的生体触媒の発現に最適な菌株を提供します。

したがって、この地域の主要な市場プレーヤーの存在、慢性疾患の増加、ヘルスケアインフラの発展により、この地域は予測期間中に大幅な成長を遂げると予想されます。

ラボオンチップ・マイクロアレイ(バイオチップ)産業の概要

ラボオンチップ・マイクロアレイ(バイオチップ)市場は、世界的および地域的に事業を展開する数社の企業が存在するため、適度な競争が見られます。最大の市場プレーヤーには、Abbott Laboratories、Agilent Technologies Inc.、Bio-Rad Laboratories Inc.、Danaher Corporation(Cepheid)、Fluidigm Corporation、Thermo Fisher Scientific Inc.、PerkinElmer Inc.、Micronit BV、Illumina Inc.、Phalanx Biotech、Group Inc.、BioMerieux SA、Qiagen NV、Merck Kommanditgesellschaft auf Aktienなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 研究の前提条件と市場の定義

- 研究範囲

第2章 研究手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ポイントオブケア検査の需要の増加

- 慢性疾患の発生率の増加

- がん研究におけるプロテオミクスとゲノミクスの応用の増加

- 市場抑制要因

- ラボオンチップ技術の設計上の制約

- 代替技術の利用可能性

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ別

- ラボオンチップ

- マイクロアレイ

- 製品別

- 機器

- 試薬・消耗品

- ソフトウェア・サービス

- 用途別

- 臨床診断

- 創薬

- ゲノミクス・プロテオミクス

- その他の用途

- エンドユーザー別

- バイオテクノロジー企業・製薬企業

- 病院・診断センター

- 学術研究機関

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Agilent Technologies Inc.

- Bio-Rad Laboratories Inc.

- Danaher Corporation(Cepheid)

- Fluidigm Corporation

- Thermo Fisher Scientific Inc.

- PerkinElmer Inc.

- Micronit BV

- Illumina Inc.

- Phalanx Biotech Group Inc.

- BioMerieux SA

- Qiagen NV

- Merck Kommanditgesellschaft auf Aktien

第7章 市場機会と将来の動向

The Lab-on-a-chip and Microarrays Market size is estimated at USD 19.08 billion in 2024, and is expected to reach USD 31.04 billion by 2029, growing at a CAGR of 10.22% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the lab-on-a-chip and microarrays (biochips) market. For instance, an article published by the journal Nature Communication in January 2021 reported that this microarray could be used as a diagnostic tool, as an epidemiologic tool to estimate the disease burden of COVID-19 more accurately, and as a research tool to correlate antibody responses with clinical outcomes. Thus, the COVID-19 pandemic increased the demand for lab-on-a-chip diagnostic tools. However, in the current scenario, it is anticipated that with the presence of other chronic and infectious diseases, the demand for the studied market is expected to increase over the forecast period.

The factors driving the growth of the studied market are increasing demand for point-of-care testing, increasing incidences of chronic diseases, and increasing application of proteomics and genomics in cancer research. Most market players are focusing on the development of new and technologically advanced diagnostic tests. Chronic diseases are the leading cause of death and disability across the world. For instance, an article published by the journal Plos One in March 2022 reported that 21% of the elderly in India had at least one chronic disease. Chronic diseases are the leading causes of disability and mortality among the elderly population in India.

Similarly, another article published by European Public Health Conference in January 2022 reported that more than 3 million people will be affected by cancer by 2030 in Europe. Globally, chronic diseases (CDs) are found to be the leading causes of disability and morbidity. Since those diseases are chronic, accurate and timely clinical decision-making is required. In this direction, research toward developing new lab-on-a-chip-based POC systems for the diagnosis of chronic diseases is an emerging area. Thus, a high incidence of chronic diseases is expected to drive the growth of the studied market.

Biochips are increasingly being used in the field of biomedical and biotechnological research. With the advancement of technologies, there has been a rise in the adoption of biochips in proteomics. The advantages of protein biochips are the low sample consumption due to their inclination toward miniaturization. These characteristics of microarrays are important for proteome-wide analysis. Proteomics is being widely adopted for biomarker and drug discoveries. For instance, in April 2021, PathogenDx Inc. reported that the USFDA had issued an Emergency Use Authorization (EUA) for its patented COVID-19 multiplexed viral diagnostic assay, DetectX-Rv. DetectX-Rv is an RT-PCR and DNA microarray hybridization test intended for the qualitative detection of nucleic acids from SARS-CoV-2 swabs. Thus, such approvals for new products are also contributing to the growth of the studied market.

Thus, due to the increasing demand for point-of-care testing, increasing incidences of chronic diseases, and increasing application of proteomics and genomics in cancer research, the studied market is expected to witness significant growth over the forecast period. However, the design constraints of lab-on-chip technology and the availability of alternative technologies may slow down the growth of the studied market.

Lab-on-a-chip and Microarrays Market Trends

Lab-on-a-chip Segment Expected to Witness Significant Growth over the Forecast Period

The lab-on-a-chip (LOC) segment is expected to have positive market growth due to the increasing number of chronic diseases and rising technological advancements. There is also a rise in the adoption of personalized medicine and easy accessibility of lab-on-chip technology, which will boost the demand for the same across the world. Also, there are various applications of LOC that are growing rapidly. Lab-on-a-chip devices equipped with electrodes for particle or cell detection, particle packing, sorting, electrophoresis, PCR, etc., are commercially available.

With the increasing number of COVID-19 cases, there is a growing number of research studies to treat and prevent this disease. This has boosted the demand for labs-on-a-chip. For instance, in January 2021, researchers at the University of Alberta joined forces to develop a handheld LOC device for the rapid detection of COVID-19 antibodies. Also, a low-cost imaging platform utilizing the lab-on-a-chip technology created by the University of California by Irvine scientists may be available for rapid coronavirus diagnostic and antibody testing.

Furthermore, the market has witnessed frequent developments in lab-on-a-chip (LOC) platform-based immunoassays. Such advanced LOC platforms include microfluidic chips, paper, lateral flow, electrochemistry, and new biosensor concepts. The rapid increase in demand for point-of-care diagnosis is the most prominent driver expected to propel the segment during the forecast period. For instance, in February 2022, Onera Health launched the Onera Biomedical-Lab-on-Chip, an ultra-low-power biosignal sensor subsystem for wearable devices. This biomedical compact chip is designed to process multiple biosignals, which creates a massive opportunity for health devices. Thus, such developments are propelling the growth of this segment.

Thus, due to the increasing number of chronic diseases, rising technological advancements, rise in the adoption of personalized medicine, and easy accessibility of lab-on-chip technology, the segment is expected to witness significant growth over the forecast period.

North America Expected to Witness a Significant Growth Over the Forecast Period

North America is expected to witness significant growth over the forecast period owing to the presence of key market players in the region and the development of healthcare infrastructure. In addition, the region has witnessed major collaborative activities with healthcare giants that are extensively investing in R&D in microarray technology. For instance, in September 2022, Illumina Inc. launched the NovaSeq X Series, new production-scale sequencers, enabling faster, more powerful, and more sustainable sequencing. This revolutionary new technology, NovaSeq X Plus can generate more than 20,000 whole genomes per year, 2.5 times the throughput of prior sequencers, greatly accelerating genomic discovery and clinical insights to understand the disease and ultimately transform patient lives. Thus, such developments in the region are driving the growth of the studied market.

The field of point-of-care (POC) diagnostics also widely uses microfluidic technology for various applications, like molecular diagnostics, infectious diseases, and chronic diseases, in resource-limited settings. For instance, an article published by the journal Frontiers of Bioengineering and Biotechnology in January 2021 reported that Lateral Flow Assays (LFAs) were widely being used in POC testing and can be used for diagnosis and prognosis of diseases like cancer by identifying specific biomarkers. LFAs have widely been used to detect an array of pathogens and proteins via antibody and nucleic acid amplification. Thus, the latest advances in the research in microfluidics aim to produce integrated devices that are self-contained, automated, easy to use, and rapid.

Moreover, the high incidence of chronic diseases reported in the region is also contributing to the growth of this segment. For instance, as per the Canadian Cancer Statistics released in November 2021 reported that an estimated 229,200 Canadians were diagnosed with cancer in 2021. Similarly, according to the International Diabetes Federation (IDF) published, in 2021, an estimated 14 million adults in Mexico were living with diabetes. Thus, such a high number of people living with chronic diseases in the region is also contributing to the growth of the studied market in the region.

Over the last few years, the interest in high throughput screening (HTS) technologies within academic research has increased drastically in the United States. For instance, in October 2022, Ginkgo Bioworks entered into a collaboration with Merck to engineer up to four enzymes for use as biocatalysts in Merck's active pharmaceutical ingredient (API) manufacturing efforts. Through this collaboration, Ginkgo is to leverage its extensive experience in cell engineering and enzyme design, as well as its capabilities in automated high throughput screening, manufacturing process development/optimization, bioinformatics, and analytics to deliver optimal strains for expression of targeted biocatalysts.

Thus, due to the presence of key market players in the region, the increase in chronic diseases, and the development of healthcare infrastructure, the region is expected to witness significant growth over the forecast period.

Lab-on-a-chip and Microarrays Industry Overview

The lab-on-a-chip and microarrays (biochip) market is moderately competitive, with the presence of a few companies operating globally and regionally. Some of the largest market players include Abbott Laboratories, Agilent Technologies Inc., Bio-Rad Laboratories Inc., Danaher Corporation (Cepheid), Fluidigm Corporation, Thermo Fisher Scientific Inc., PerkinElmer Inc., Micronit BV, Illumina Inc., Phalanx Biotech Group Inc., BioMerieux SA, Qiagen NV, and Merck Kommanditgesellschaft auf Aktien.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Point-of-care Testing

- 4.2.2 Increasing Incidences of Chronic Diseases

- 4.2.3 Increasing Application of Proteomics and Genomics in Cancer Research

- 4.3 Market Restraints

- 4.3.1 Design Constraints of Lab-on-chip Technology

- 4.3.2 Availability of Alternative Technologies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Lab-on-a-chip

- 5.1.2 Microarray

- 5.2 By Products

- 5.2.1 Instruments

- 5.2.2 Reagents and Consumables

- 5.2.3 Software and Services

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.2 Drug Discovery

- 5.3.3 Genomics and Proteomics

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Biotechnology and Pharmaceutical Companies

- 5.4.2 Hospitals and Diagnostic Centers

- 5.4.3 Academic and Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle-East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle-East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Agilent Technologies Inc.

- 6.1.3 Bio-Rad Laboratories Inc.

- 6.1.4 Danaher Corporation (Cepheid)

- 6.1.5 Fluidigm Corporation

- 6.1.6 Thermo Fisher Scientific Inc.

- 6.1.7 PerkinElmer Inc.

- 6.1.8 Micronit BV

- 6.1.9 Illumina Inc.

- 6.1.10 Phalanx Biotech Group Inc.

- 6.1.11 BioMerieux SA

- 6.1.12 Qiagen NV

- 6.1.13 Merck Kommanditgesellschaft auf Aktien