|

|

市場調査レポート

商品コード

1444623

遠隔診療:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Telemedicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 遠隔診療:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

遠隔診療市場規模は2024年に1,724億4,000万米ドルと推定され、2029年までに3,302億6,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に13.88%のCAGRで成長します。

遠隔診療は、COVID-19感染症のパンデミックにおいてヘルスケアに不可欠な要素として浮上しました。遠隔診療サービスはパンデミックが始まる前からほとんどのヘルスケアシステムに統合されていましたが、サービスが広く使用され始めたのはCOVID-19症危機の期間になってからです。ギリシャ調査技術財団が2021年10月に発表した記事では、パンデミック中、新型COVID-19感染症がデジタルヘルスケアイノベーションの触媒および加速器として機能したと説明しています。規制当局は、イノベーションをより効果的に促進するために、人工知能とデジタルヘルスにおけるデータサイロを排除することに取り組みました。さらに、米国はよりシームレスなデータフローを可能にする法案を承認し、欧州連合はパンデミック中に国境を越えて電子医療記録(EHR)の交換を許可するために加盟国全体のデータを統合しました。さらに、2022年9月に『Health Affairs』誌に掲載された研究によると、COVID-19パンデミックの最中に、遠隔患者モニタリング(RPM)の使用量が4倍以上に増加した原因は、少数のプライマリケア医師の責任だったといいます。遠隔診療ソリューションは、COVID-19感染症のパンデミックのような高ストレス期間中に健康成果を向上させる能力が実証されており、遠隔ヘルスケアサービスと統合されています。

遠隔診療市場の成長の主な要因には、ヘルスケア費の増加、技術革新と遠隔患者モニタリングに対する需要の高まり、慢性疾患の負担の増大などが含まれます。例えば、2022年5月に発表された英国医療会計の暫定推計、2021年報告書によると、2021年の現在のヘルスケア支出総額は2,770億ポンド(3,170億米ドル)と推定されており、これは名目で7.4%の増加となります。さらに、カナダ保健情報研究所の2022年の最新情報によると、病院(24.34%)、医師(13.60%)、医薬品(13.58%)のカテゴリーが引き続き最大のシェアを占めており、これは終わりました。対面での診察はオンライン診療に比べてはるかに面倒で高価であるため、遠隔診療が注目を集めています。これは、予測期間中に調査された市場の成長を促進する可能性があります。

さらに、CDCによると、2021年には米国で20歳以上の成人約1,820万人が冠動脈疾患(CAD)を患っていました。心臓病は米国の主な死因です。また、国際糖尿病連盟(IDF)の2022年の最新情報によると、約5億3,700万人の成人(20~79歳)が糖尿病を抱えて暮らしています。糖尿病を抱えて生きる人の総数は、2030年までに6億4,300万人、2045年までに7億8,300万人に増加すると予測されています。慢性疾患の発生率が高いため、膨大な遠隔診療の需要が増加し、それが市場を牽引しています。

したがって、上記の要因は遠隔診療市場の市場成長に影響を与えています。ただし、法的および償還の問題、高い初期資本要件、および医師のサポートの欠如により、予測期間中の市場の成長が妨げられると予想されます。

遠隔診療市場の動向

テレホーム部門は予測期間中に大幅な成長が見込まれる

テレホームには、自宅にいる顧客にヘルスケアサービスを提供することが含まれます。慢性疾患の増加は世界の懸念であり、ヘルスケア資源に負担を与えています。遠隔在宅医療は、最新のテクノロジーを使用してケアを提供し、患者を監視し、情報を提供する革新的な方法です。モニタリングにより病気を早期に特定でき、緊急事態に役立ちます。したがって、テレホームサービスの利用が増加しています。たとえば、JMIR Publicationsが2022年 1月に掲載した記事によると、スペインでは従来の病院での治療よりも9%費用が安く、より複雑な状況に備えて病院のベッドが解放されるため、子供たちとその家族は小児遠隔在宅治療を選択しました。

さらに、人々は利便性の向上と総コストの削減により、治療のために病院に行くよりも自宅でのテレホームを好みます。たとえば、質の高い在宅ヘルスケアのためのパートナーシップが発行した記事によると、2021年に成人の約86%が自宅で「入院後の短期ヘルスケア」を受けることを希望したが、米国では老人ホームを好む人はわずか5%だった。州。テレホームサービスは、患者と病院に大幅な節約の機会を提供します。したがって、テレホームサービスの普及率の増加は、遠隔診療市場の成長に直接影響を与えています。したがって、普及率の増加やテレホームの低コストなどの要因が、予測期間中に市場のセグメント的な成長を促進すると予想されます。

予測期間中、北米が遠隔診療市場を独占すると予想される

遠隔診療は、慢性疾患の負担の増大と高度なヘルスケア技術の高度な導入により、米国のヘルスケアの構成要素として急速に成長しています。遠隔診療の導入により、ケア管理、患者の生活の質が向上し、ヘルスケア費が削減されました。さらに、モバイルテクノロジーに対する需要の高まり、患者による在宅ケアの採用の増加、ヘルスケア費の増加、通院の減少により、予測期間中に市場の成長が促進されると予想されます。たとえば、カナダ保健情報研究所の2021年の報告書によると、カナダの医療支出は2020年の3,015億米ドルと比較して、2021年の3,081億米ドルに増加しました。同様に、メディケアおよびメディケイドサービスセンターの2022年の報告書によると(CMS)によると、米国の医療支出は約4兆3,000億米ドルで、前年より約1,730億米ドル増加しました。したがって、ヘルスケア支出の増加により遠隔診療の機会が生まれ、それによって市場の成長が促進されると予想されます。

さらに、企業は、予測期間の成長を促進する遠隔診療市場での革新を目的として、パートナーシップ、コラボレーション、買収、合併、および製品の発売に取り組んでいます。たとえば、2021年4月、米国のバージニア北部およびワシントンDC地域のInova Health Systemは、パーキンソン病と本態性振戦の治療を受けている脳深部刺激(DBS)患者の遠隔神経調節のためのFDA承認の遠隔診療オプションを提供しました。また、2022年 8月に、Hicuity Healthは、サウスカロライナ州コロンビアのMUSC Health Columbia Medical Center Downtownで遠隔 ICUサービスを開始しました。したがって、このような発展が市場を牽引すると予想されます。したがって、上記の要因を考慮すると、遠隔診療市場は予測期間中に北米で大幅に成長すると予想されます。

遠隔診療業界の概要

遠隔診療市場は、世界的および地域的に事業を展開する複数の企業が存在するため、本質的に細分化されています。競合情勢には、Allscriptsヘルスケア Solutions Inc.、BioTelemetry、Medtronic、Koninklijke Philips NV、Aerotel Medical Systems(1998)Ltd、AMD Global Telemedicine Incなど、市場シェアを保持しよく知られているいくつかの国際企業と地元企業の分析が含まれています。 .、SOC Telemedなど。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ヘルスケア費の増加

- 技術革新と遠隔患者モニタリングの需要の高まり

- 増大する慢性疾患の負担

- 市場抑制要因

- 法的および償還の問題

- 高額な初期資本要件と医師のサポートの欠如

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額別の市場規模)

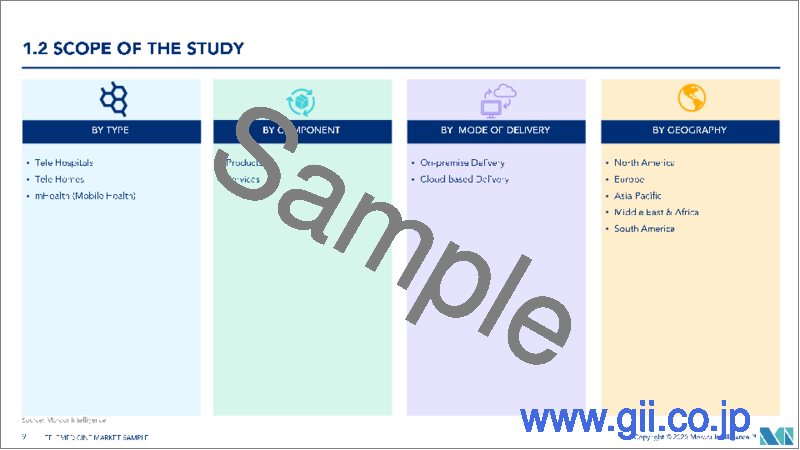

- タイプ別

- テレホスピタル

- テレホーム

- mヘルス(モバイルヘルス)

- コンポーネント別

- 製品

- ハードウェア

- ソフトウェア

- その他の製品

- サービス

- 遠隔病理学

- 遠隔心臓学

- 遠隔放射線学

- 遠隔皮膚科

- 遠隔精神医学

- 他のサービス

- 製品

- 提供モード別

- オンプレミス提供

- クラウドベース提供

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Aerotel Medical Systems(1998)Ltd

- IBM

- Allscripts Healthcare Solutions Inc.

- AMD Global Telemedicine Inc.

- SOC Telemed

- Resideo Technologies Inc.

- Koninklijke Philips NV

- Medtronic PLC

- SHL Telemedicine

- Teladoc Health Inc.(InTouch Technologies Inc.)

- Cerner Corporation

- Cisco System

第7章 市場機会と将来の動向

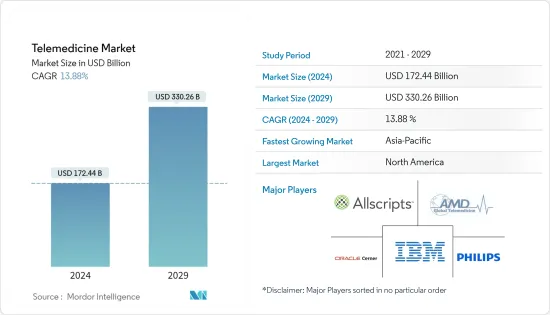

The Telemedicine Market size is estimated at USD 172.44 billion in 2024, and is expected to reach USD 330.26 billion by 2029, growing at a CAGR of 13.88% during the forecast period (2024-2029).

Telehealth has emerged as an essential component of healthcare during the COVID-19 pandemic. Though telemedicine services were integrated into most healthcare systems even before the onset of the pandemic, services began to be extensively used only during the COVID-19 crisis. An article published in October 2021, by Foundation for Research and Technology Greece, explained that during the pandemic, COVID-19 served as a catalyst and accelerator for digital healthcare innovation. Regulators worked to eliminate data silos in artificial intelligence and digital health to better promote innovation. Furthermore, the United States has approved legislation to allow for more seamless data flow, while the European Union integrated the data across member states to permit the interchange of electronic health records (EHRs) across borders during the pandemic. Additionally, according to a study published in Health Affairs, in September 2022, during the COVID-19 pandemic, a small percentage of primary care doctors were responsible for the more than 4-fold rise in the usage of remote patient monitoring (RPM). Telemedicine solutions have demonstrated the ability to enhance health outcomes during a high-stress period like the COVID-19 pandemic and being integrated with conventional healthcare services which are expected to further increase the demand for telemedicine services.

The major factors for the growth of the telemedicine market include rising healthcare expenditure, technological innovations and rising demand for remote patient monitoring, and the growing burden of chronic diseases. For instance, according to the UK Health Accounts provisional estimates, the 2021 report, published in May 2022, the total current healthcare expenditure in 2021 was estimated at GBP 277 billion (USD 317 billion), which is an increase in nominal terms of 7.4% on spending in 2020. Furthermore, as per the 2022 update from the Canadian Institute for Health Information, hospitals (24.34%), physicians (13.60%), and drugs (13.58%) categories continued to account for the largest shares, which is over half of the total health spending in 2022. As the cost of in-person consultation is much more tedious and costly as compared to an online consultation and hence telemedicine gained traction. This is likely to boost the growth of the market studied over the forecast period.

Furthermore, according to CDC, in 2021, around 18.2 million adults aged 20 and older had coronary artery disease (CAD) in the United States. Heart disease is the leading cause of death in the United States. Also, as per the 2022 update from the International Diabetic Federation (IDF), approximately 537 million adults (20-79 years) are living with diabetes. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The high incidence of chronic diseases increases the demand for huge telemedicine, which, in turn, drives the market.

Thus, the abovementioned factors are impacting the market growth of the telemedicine market. However, legal and reimbursement issues and high initial capital requirements, and lack of physician support are expected to hinder market growth over the forecast period.

Telemedicine Market Trends

Tele homes Segment is Expected to Witness a Significant Growth Over the Forecast Period

Tele homes involve delivering healthcare services to clients in their own homes. The rise of chronic diseases is a global concern that strains healthcare resources. Tele-homecare is an innovative way to provide care, monitor a patient, and provide information using the latest technology. Monitoring allows early identification of diseases and provides aid in emergencies. Hence, the use of tele home services is increasing. For instance, according to an article published by JMIR Publications, in January 2022, children and their families chose pediatric tele home care since it is 9% less expensive than traditional hospital care, freeing up hospital beds for more complicated situations in Spain.

Further, people prefer tele home at home rather than visiting a hospital for treatment owing to greater convenience and reduction in overall cost. For instance, according to an article published by the Partnership for Quality Home Healthcare, in 2021, some 86% of adults preferred to receive "post-hospital, short-term healthcare" at home, while only 5% preferred nursing homes in the United States. Tele home services provide an opportunity for significant savings for patients and hospitals. Thus, the increasing adoption rate of tele homes services is directly affecting the growth of the telemedicine market. Therefore, factors such increase adoption rate and low cost of tele home are expected to drive segmental growth in the market during the forecast period.

North America is Expected to Dominate the Telemedicine Market Over the Forecast Period

Telemedicine is a rapidly growing component of healthcare in the United States due to the growing burden of chronic diseases and the high adoption of advanced healthcare technologies. The adoption of telemedicine has improved care management, patients' quality of life, and reduced healthcare spending. Furthermore, the rising demand for mobile technologies, rising home care adoption by patients, increased healthcare expenditure, and reduction in hospital visits are expected to propel the market's growth over the forecast period. For instance, according to the 2021 report from the Canadian Institute of Health Information, Canadian health expenditure increased to USD 308.1 billion in 2021 compared to USD 301.5 billion in 2020. Similarly, as per the 2022 report of the Centers for Medicare and Medicaid Services (CMS), the health expenditure of the United States was about USD 4.3 trillion, an increase of about USD 173 billion from the previous year. Thus, the increasing healthcare spending is anticipated to create opportunities for telemedicine, thereby propelling the market growth.

Additionally, companies are engaged in partnerships, collaborations, acquisitions, mergers, and product launches to innovate in the telemedicine market driving growth in the forecast period. For instance, in April 2021, Inova Health System in the Northern Virginia and Washington DC area, United States, offered an FDA-approved telemedicine option for remote neuromodulation of deep brain stimulation (DBS) patients being treated for Parkinson's disease and essential tremor. Also, in August 2022, Hicuity Health launched tele-ICU services at MUSC Health Columbia Medical Center Downtown in Columbia, South Carolina. Therefore, such development is expected to drive the market. Thus, given the factors above, the telemedicine market is expected to grow significantly in North America over the forecast period.

Telemedicine Industry Overview

The Telemedicine Market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies which hold market shares and are well known including Allscripts Healthcare Solutions Inc., BioTelemetry, Medtronic, Koninklijke Philips NV, Aerotel Medical Systems (1998) Ltd, AMD Global Telemedicine Inc., and SOC Telemed, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Healthcare Expenditure

- 4.2.2 Technological Innovations and Rising Demand for Remote Patient Monitoring

- 4.2.3 Growing Burden of Chronic Diseases

- 4.3 Market Restraints

- 4.3.1 Legal and Reimbursement Issues

- 4.3.2 High Initial Capital Requirements and Lack of Physician Support

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 By Type

- 5.1.1 Tele hospitals

- 5.1.2 Tele homes

- 5.1.3 mHealth (Mobile Health)

- 5.2 By Component

- 5.2.1 Products

- 5.2.1.1 Hardware

- 5.2.1.2 Software

- 5.2.1.3 Other Products

- 5.2.2 Services

- 5.2.2.1 Telepathology

- 5.2.2.2 Telecardiology

- 5.2.2.3 Teleradiology

- 5.2.2.4 Teledermatology

- 5.2.2.5 Telepsychiatry

- 5.2.2.6 Other Services

- 5.2.1 Products

- 5.3 By Mode of Delivery

- 5.3.1 On-premise Delivery

- 5.3.2 Cloud-based Delivery

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 US

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 UK

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerotel Medical Systems (1998) Ltd

- 6.1.2 IBM

- 6.1.3 Allscripts Healthcare Solutions Inc.

- 6.1.4 AMD Global Telemedicine Inc.

- 6.1.5 SOC Telemed

- 6.1.6 Resideo Technologies Inc.

- 6.1.7 Koninklijke Philips NV

- 6.1.8 Medtronic PLC

- 6.1.9 SHL Telemedicine

- 6.1.10 Teladoc Health Inc. (InTouch Technologies Inc.)

- 6.1.11 Cerner Corporation

- 6.1.12 Cisco System