|

|

市場調査レポート

商品コード

1494825

嫌気性消化市場の2030年までの予測: 原料タイプ、容量、提供、消化システム、用途、地域別の世界分析Anaerobic Digestion Market Forecasts to 2030 - Global Analysis By Feedstock Type, Capacity, Offering, Digestion System, Application and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 嫌気性消化市場の2030年までの予測: 原料タイプ、容量、提供、消化システム、用途、地域別の世界分析 |

|

出版日: 2024年06月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、嫌気性消化の世界市場は2024年に113億3,000万米ドルを占め、2030年には233億4,000万米ドルに達すると予測され、予測期間中に12.8%のCAGRで成長する見込みです。

嫌気性消化は、微生物が酸素のない状態で有機物を分解し、製品別としてバイオガスを生産する生物学的プロセスです。このプロセスは、沼地、埋立地、動物の消化器官で自然に発生します。嫌気性消化槽のような制御された環境では、有機廃棄物をバイオガスのような貴重な資源に効率的に変換するために利用されます。このプロセスはまた、肥料として使用できる栄養価の高い消化物を生成します。

世界銀行の『What A Waste 2.0』報告書によると、世界では年間20億1,000万トンの都市固形廃棄物が発生しています。そのうちの33%近くが、環境的に安全な方法で管理されていないです。同報告書はまた、世界の廃棄物は2050年までに34億トンに増加すると予測しています。

原料の入手可能性

原料の入手可能性は、嫌気性消化市場の重要な促進要因であり、市場の成長と持続可能性に影響を与えます。この促進要因は、農業残渣、食品廃棄物、廃水汚泥など、嫌気性消化プロセスに適した有機物へのアクセスと豊富さに焦点を当てています。これらの供給源が豊富な地域は、嫌気性消化産業がより強固になる傾向があります。農業慣行、都市化率、廃棄物管理政策などの要因は、原料の入手可能性に影響を与えます。環境上の利点に対する意識の高まりと再生可能エネルギーに対する政府の支援は、嫌気性消化施設用の多様で安定した原料供給を確保する努力をさらに後押しします。

経済性

経済的実行可能性の制約は、嫌気性消化プロジェクトを財政的に実現可能にする上で直面する課題によるものです。こうした制約の多くは、消化槽やバイオガス精製システムなどのインフラ設置に必要な初期資本コストが高いことに起因します。さらに、原料の入手可能性や品質の変動、規制の不確実性が収益性に影響することもあります。資金調達へのアクセスが限られていることや、バイオガスや消化液の販売による収入源が十分でないことが、事業性の問題をさらに深刻にしています。こうした制約に対処するには、長期的な原料契約を確保し、収益源を強化するための支援政策やインセンティブを実施する必要があります。

廃棄物管理ソリューション

嫌気性消化市場は、廃棄物管理と再生可能エネルギー発電という二重の利点があるため、廃棄物管理ソリューションにとって大きなビジネスチャンスとなります。嫌気性消化は、有機廃棄物を利用して再生可能エネルギー源であるバイオガスを生産すると同時に、温室効果ガスの排出を削減します。環境への関心が高まり、規制が強化されるにつれ、嫌気性消化のような持続可能な廃棄物管理ソリューションへの需要が高まっています。さらに、政府のインセンティブや補助金がこの市場の魅力をさらに高めています。廃棄物管理ソリューションは、環境に優しい廃棄物管理ソリューションの需要増加に対応するため、技術的進歩への投資、インフラの拡大、パートナーシップの育成を行うことで、この機会を活用することができます。

代替技術との競合

代替技術との競合は、嫌気性消化市場にとって大きな脅威となります。持続可能なエネルギーソリューションが進化するにつれ、熱分解、ガス化、微生物燃料電池といった選択肢が手ごわい競合相手として浮上しています。これらの選択肢は、高いエネルギー効率、高い拡張性、幅広い原料適合性など、多様な利点を提供します。さらに、嫌気性消化に比べて初期投資が少なくて済み、投資回収が早いことも多いです。その結果、嫌気性消化技術が技術革新を続け、処理時間の長さや特定の原料への依存といった限界に対処しない限り、こうした代替ソリューションに市場シェアを奪われるリスクがあります。

COVID-19の影響:

COVID-19の大流行は、いくつかの点で嫌気性消化(AD)市場に大きな影響を与えました。操業停止や規制によって廃棄物のサプライチェーンが混乱し、ADプラント向けの原料供給に影響が出ました。経済不況はまた、新しいADプロジェクトへの投資を妨げ、市場の成長を停滞させました。さらに、パンデミックの間のエネルギー需要の減少は、バイオガス生産のインセンティブを低下させ、ADの収益性に影響を与えました。しかし、パンデミック後の持続可能性と再生可能エネルギー発電への関心の高まりは、実行可能な廃棄物管理とエネルギー発電ソリューションとしてのADへの関心を再び高める可能性があります。

予測期間中、一般廃棄物セグメントが最大となる見込み

嫌気性消化市場内の一般廃棄物セグメントは、環境に優しい廃棄物管理ソリューションを求める自治体の環境持続可能性に対する意識の高まりにより、著しい成長を遂げています。嫌気性消化は、バイオガスの形で再生可能エネルギーを発電しながら有機廃棄物を管理する持続可能な方法を提供します。さらに、嫌気性消化技術の進歩により、より効率的で費用対効果の高いものとなり、自治体の廃棄物管理への採用をさらに促進しています。さらに、自治体と民間企業とのパートナーシップにより、自治体の廃棄物を効率的に処理するための大規模な嫌気性消化施設の開発が促進されています。

予測期間中、発電分野が最も高いCAGRが見込まれる

嫌気性消化市場内の発電分野は、いくつかの要因により顕著な成長を遂げています。嫌気性消化施設は、農業残渣、食品廃棄物、下水汚泥などの有機廃棄物を利用して、主にメタンから成るバイオガスを生産します。このバイオガスは発電機で利用され、電気を生産します。再生可能エネルギー源への注目の高まりと温室効果ガス排出削減の必要性が、嫌気性消化システムの需要を促進しています。さらに、技術の進歩により、バイオガスによる発電の効率と信頼性が向上しています。再生可能エネルギーを促進する政府のインセンティブや政策も、市場の成長を刺激しています。

最大のシェアを持つ地域:

アジア太平洋地域は、いくつかの要因によって嫌気性消化市場が大きく成長しています。廃棄物管理や炭素排出に関する厳しい規制と相まって、環境の持続可能性に関する意識の高まりが嫌気性消化技術の採用を後押ししています。この地域全体の政府は、再生可能エネルギー・プロジェクトにインセンティブを与えており、嫌気性消化システムにとって好都合な環境を育成しています。さらに、農業残渣や都市固形廃棄物などの有機廃棄物の豊富な供給源が、市場の拡大をさらに促進しています。技術の進歩や研究開発への投資も効率改善とコスト削減を促進し、嫌気性消化をこの地域のエネルギー事情においてますます魅力的なものにしています。

CAGRが最も高い地域:

近年、北米はいくつかの要因によって嫌気性消化市場が大きく成長しています。持続可能な廃棄物管理手法に対する意識の高まり、厳しい環境規制、再生可能エネルギー源に対する需要の高まりが、この地域全体での嫌気性消化技術の採用を後押ししています。さらに、再生可能エネルギー・プロジェクトの促進を目的とした政府のインセンティブや補助金が、市場の成長をさらに刺激しています。北米では、嫌気性消化のような革新的で環境に優しいソリューションを通じて、温室効果ガス排出の削減とエネルギー自立の達成に向けた取り組みが優先されるため、この成長動向は今後も続くと予想されます。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 用途分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の嫌気性消化市場:原料タイプ別

- 農業残渣

- 下水廃棄物

- 都市ごみ

- 産業廃棄物

- 有機性廃棄物

- その他の原料タイプ

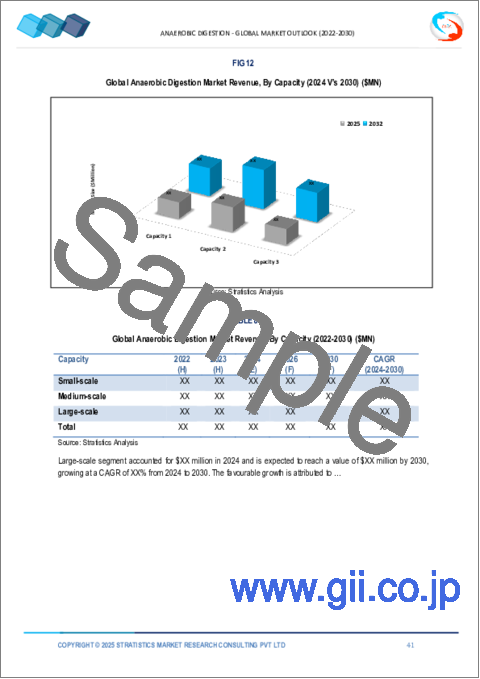

第6章 世界の嫌気性消化市場:容量別

- 小規模

- 中規模

- 大規模

第7章 世界の嫌気性消化市場:提供別

- ハードウェア

- 監視・制御機器

- 原料前処理装置

- 消化槽タンク

- バイオガス処理設備

- その他のハードウェア

- サービス

- 運用・保守サービス

- 設計・設置サービス

- ソフトウェア

- データ管理ソフトウェア

- シミュレーションソフトウェア

- エネルギーモデリングソフトウェア

- その他の提供

第8章 世界の嫌気性消化市場:消化システム別

- 高温嫌気性消化

- マルチステージ階嫌気性消化

- 中温嫌気性消化

第9章 世界の嫌気性消化市場:用途別

- 発電

- バイオ肥料生産

- バイオガス生産

- 発熱

- その他の用途

第10章 世界の嫌気性消化市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第11章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第12章 企業プロファイリング

- AAT Abwasser-und Abfalltechnik GmbH

- Agraferm GmbH

- Agrinz Technologies GmbH

- Biogen

- BTS Biogas Srl/GmbH

- Capstone Green Energy Corporation

- ENGIE SA

- EnviTec Biogas AG

- Evoqua Water Technologies LLC

- Hitachi Zosen Inova AG

- Nature Energy

- Renewi plc

- Veolia Water Technologies UK

- Zero Waste Energy, LLC

List of Tables

- Table 1 Global Anaerobic Digestion Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Anaerobic Digestion Market Outlook, By Feedstock Type (2022-2030) ($MN)

- Table 3 Global Anaerobic Digestion Market Outlook, By Agricultural Residues (2022-2030) ($MN)

- Table 4 Global Anaerobic Digestion Market Outlook, By Sewage Waste (2022-2030) ($MN)

- Table 5 Global Anaerobic Digestion Market Outlook, By Municipal Waste (2022-2030) ($MN)

- Table 6 Global Anaerobic Digestion Market Outlook, By Industrial Waste (2022-2030) ($MN)

- Table 7 Global Anaerobic Digestion Market Outlook, By Organic Waste (2022-2030) ($MN)

- Table 8 Global Anaerobic Digestion Market Outlook, By Other Feedstock Types (2022-2030) ($MN)

- Table 9 Global Anaerobic Digestion Market Outlook, By Capacity (2022-2030) ($MN)

- Table 10 Global Anaerobic Digestion Market Outlook, By Small-scale (2022-2030) ($MN)

- Table 11 Global Anaerobic Digestion Market Outlook, By Medium-scale (2022-2030) ($MN)

- Table 12 Global Anaerobic Digestion Market Outlook, By Large-scale (2022-2030) ($MN)

- Table 13 Global Anaerobic Digestion Market Outlook, By Offering (2022-2030) ($MN)

- Table 14 Global Anaerobic Digestion Market Outlook, By Hardware (2022-2030) ($MN)

- Table 15 Global Anaerobic Digestion Market Outlook, By Monitoring & Control Equipment (2022-2030) ($MN)

- Table 16 Global Anaerobic Digestion Market Outlook, By Feedstock Pre-processing Equipment (2022-2030) ($MN)

- Table 17 Global Anaerobic Digestion Market Outlook, By Digesters Tanks (2022-2030) ($MN)

- Table 18 Global Anaerobic Digestion Market Outlook, By Biogas Handling Equipment (2022-2030) ($MN)

- Table 19 Global Anaerobic Digestion Market Outlook, By Other Hardware (2022-2030) ($MN)

- Table 20 Global Anaerobic Digestion Market Outlook, By Services (2022-2030) ($MN)

- Table 21 Global Anaerobic Digestion Market Outlook, By Operations & Maintenance Services (2022-2030) ($MN)

- Table 22 Global Anaerobic Digestion Market Outlook, By Designing & Installation Services (2022-2030) ($MN)

- Table 23 Global Anaerobic Digestion Market Outlook, By Software (2022-2030) ($MN)

- Table 24 Global Anaerobic Digestion Market Outlook, By Data Management Software (2022-2030) ($MN)

- Table 25 Global Anaerobic Digestion Market Outlook, By Simulation Software (2022-2030) ($MN)

- Table 26 Global Anaerobic Digestion Market Outlook, By Energy Modeling Software (2022-2030) ($MN)

- Table 27 Global Anaerobic Digestion Market Outlook, By Other Offerings (2022-2030) ($MN)

- Table 28 Global Anaerobic Digestion Market Outlook, By Digestion System (2022-2030) ($MN)

- Table 29 Global Anaerobic Digestion Market Outlook, By Thermophilic Anaerobic Digestion (2022-2030) ($MN)

- Table 30 Global Anaerobic Digestion Market Outlook, By Multi-Stage Anaerobic Digestion (2022-2030) ($MN)

- Table 31 Global Anaerobic Digestion Market Outlook, By Mesophilic Anaerobic Digestion (2022-2030) ($MN)

- Table 32 Global Anaerobic Digestion Market Outlook, By Application (2022-2030) ($MN)

- Table 33 Global Anaerobic Digestion Market Outlook, By Electricity Generation (2022-2030) ($MN)

- Table 34 Global Anaerobic Digestion Market Outlook, By Biofertilizer Production (2022-2030) ($MN)

- Table 35 Global Anaerobic Digestion Market Outlook, By Biogas Production (2022-2030) ($MN)

- Table 36 Global Anaerobic Digestion Market Outlook, By Heat Generation (2022-2030) ($MN)

- Table 37 Global Anaerobic Digestion Market Outlook, By Other Applications (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Anaerobic Digestion Market is accounted for $11.33 billion in 2024 and is expected to reach $23.34 billion by 2030 growing at a CAGR of 12.8% during the forecast period. Anaerobic digestion is a biological process where microorganisms break down organic matter in the absence of oxygen, producing biogas as a byproduct. This process occurs naturally in marshes, landfills, and the digestive systems of animals. In controlled environments, such as anaerobic digesters, it's harnessed to efficiently convert organic waste into valuable resources like biogas, which is primarily methane and carbon dioxide. The process also yields nutrient-rich digestate, which can be used as fertilizer.

According to the World Bank's What A Waste 2.0 report, the world generates 2.01 billion tonnes of municipal solid waste yearly. Among that, nearly 33% of the waste is not managed in an environmentally safe manner. The report also estimates that global waste is projected to grow to 3.4 billion tonnes by 2050.

Market Dynamics:

Driver:

Feedstock availability

Feedstock availability is a crucial driver in the anaerobic digestion market, influencing its growth and sustainability. This driver focuses on the accessibility and abundance of organic materials suitable for anaerobic digestion processes, such as agricultural residues, food waste, and wastewater sludge. Regions with ample sources of these feedstocks tend to have more robust anaerobic digestion industries. Factors like agricultural practices, urbanization rates, and waste management policies impact feedstock availability. Increased awareness about environmental benefits and governmental support for renewable energy further drives efforts to secure diverse and consistent feedstock supplies for anaerobic digestion facilities.

Restraint:

Economic viability

The economic viability restriction is due to the challenges faced in making anaerobic digestion projects financially feasible. These constraints often stem from the high initial capital costs required for infrastructure setup, such as digesters and biogas purification systems. Additionally, fluctuations in feedstock availability and quality, as well as regulatory uncertainties, can affect profitability. Limited access to financing and insufficient revenue streams from biogas and digestate sales further compound the viability issue. Addressing these constraints securing long-term feedstock contracts, and implementing supportive policies and incentives to enhance revenue streams.

Opportunity:

Waste management solutions

The anaerobic digestion market presents a significant opportunity for waste management solutions due to its dual benefits of waste management and renewable energy generation. Anaerobic digestion utilizes organic waste to produce biogas, a renewable energy source, while also reducing greenhouse gas emissions. As environmental concerns grow and regulations tighten, the demand for sustainable waste management solutions like anaerobic digestion is on the rise. Additionally, government incentives and subsidies further bolster the attractiveness of this market. Waste Management Solutions can capitalize on this opportunity by investing in technological advancements, expanding infrastructure, and fostering partnerships to meet the increasing demand for eco-friendly waste management solutions.

Threat:

Competition from alternative technologies

Competition from alternative technologies poses a significant threat to the anaerobic digestion market. As sustainable energy solutions evolve, options like pyrolysis, gasification, and microbial fuel cells emerge as formidable contenders. These alternatives offer diverse benefits, such as higher energy efficiency, greater scalability, and broader feedstock compatibility. Moreover, they often require less initial investment and offer faster returns on investment compared to anaerobic digestion. Consequently, unless anaerobic digestion technology continues to innovate and address its limitations, such as long processing times and dependency on specific feedstocks, it risks losing market share to these alternative solutions.

Covid-19 Impact:

The COVID-19 pandemic significantly impacted the anaerobic digestion (AD) market in several ways. Lockdowns and restrictions disrupted waste supply chains, affecting feedstock availability for AD plants. Economic downturns also hindered investments in new AD projects, stalling market growth. Moreover, reduced energy demand during the pandemic decreased the incentive for biogas production, impacting AD profitability. However, increased focus on sustainability and renewable energy post-pandemic may drive renewed interest in AD as a viable waste management and energy generation solution.

The municipal waste segment is expected to be the largest during the forecast period

The municipal waste segment within the anaerobic digestion market has seen significant growth due to increasing awareness about environmental sustainability that has driven municipalities to seek eco-friendly waste management solutions. Anaerobic digestion provides a sustainable method to manage organic waste while generating renewable energy in the form of biogas. Additionally, advancements in anaerobic digestion technology have made it more efficient and cost-effective, further driving its adoption in municipal waste management. Furthermore, partnerships between municipalities and private sector players have facilitated the development of large-scale anaerobic digestion facilities to handle municipal waste effectively.

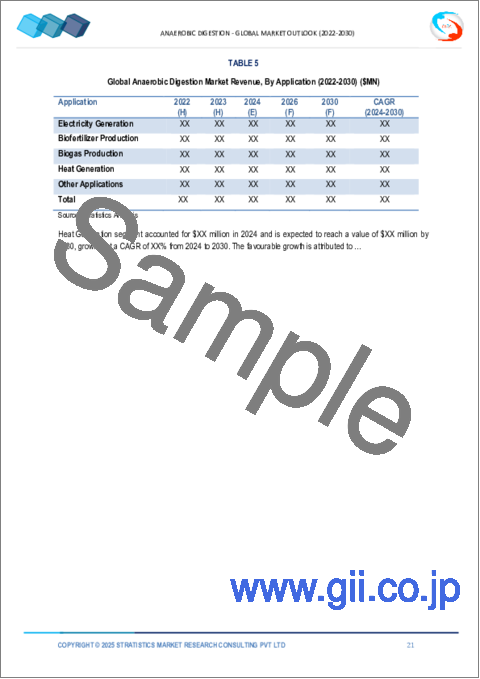

The electricity generation segment is expected to have the highest CAGR during the forecast period

The electricity generation segment within the anaerobic digestion market has experienced notable growth due to several factors. Anaerobic digestion facilities harness organic waste materials such as agricultural residues, food waste, and sewage sludge to produce biogas, primarily composed of methane. This biogas is then utilized in generators to produce electricity. The increasing focus on renewable energy sources and the need to reduce greenhouse gas emissions have propelled the demand for anaerobic digestion systems. Moreover, technological advancements have improved the efficiency and reliability of electricity generation from biogas. Government incentives and policies promoting renewable energy have also stimulated market growth.

Region with largest share:

The Asia-Pacific region has witnessed significant growth in the anaerobic digestion market due to several factors. Increasing awareness about environmental sustainability, coupled with stringent regulations on waste management and carbon emissions, has propelled the adoption of anaerobic digestion technologies. Governments across the region are incentivizing renewable energy projects, fostering a conducive environment for anaerobic digestion systems. Additionally, the abundance of organic waste sources, such as agricultural residues and municipal solid waste, further fuels market expansion. Technological advancements and investments in research and development are also driving efficiency improvements and lowering costs, making anaerobic digestion increasingly attractive in the region's energy landscape.

Region with highest CAGR:

In recent years, North America has witnessed significant growth in the anaerobic digestion market, driven by several factors. Increasing awareness about sustainable waste management practices, stringent environmental regulations, and rising demand for renewable energy sources have propelled the adoption of anaerobic digestion technologies across the region. Additionally, government incentives and subsidies aimed at promoting renewable energy projects have further stimulated market growth. This growth trend is expected to continue as North America prioritizes efforts towards reducing greenhouse gas emissions and achieving energy independence through innovative and eco-friendly solutions like anaerobic digestion.

Key players in the market

Some of the key players in Anaerobic Digestion market include AAT Abwasser- und Abfalltechnik GmbH, Agraferm GmbH, Agrinz Technologies GmbH, Biogen, BTS Biogas Srl/GmbH, Capstone Green Energy Corporation, ENGIE SA, EnviTec Biogas AG, Evoqua Water Technologies LLC, Hitachi Zosen Inova AG, Nature Energy, Renewi plc, Veolia Water Technologies UK and Zero Waste Energy, LLC.

Key Developments:

In May 2024, GTT Strategic Ventures and Engie New Ventures are dedicated to supporting sustainable technologies and innovative start-ups that help accelerate the energy transition. Established in 2017, CryoCollect specializes in the design and engineering of gas treatment, liquefaction, and separation technologies for gases such as biomethane, CO2, and hydrogen.

In February 2024, Aptar has entered into an enterprise agreement with Biogen Inc to operate and develop digital health solutions for neurological and rare diseases. As part of the agreement, Biogen will transfer ownership of select digital health solutions to Aptar Digital Health (Aptar). Through this collaboration, Aptar will provide a full range of capabilities including the product management, design, development and maintenance of software applications, secured cloud hosting, and customer and marketing support to Biogen.

Feedstock Types Covered:

- Agricultural Residues

- Sewage Waste

- Municipal Waste

- Industrial Waste

- Organic Waste

- Other Feedstock Types

Capacities Covered:

- Small-scale

- Medium-scale

- Large-scale

Offerings Covered:

- Hardware

- Services

- Software

- Other Offerings

Digestion Systems Covered:

- Thermophilic Anaerobic Digestion

- Multi-Stage Anaerobic Digestion

- Mesophilic Anaerobic Digestion

Applications Covered:

- Electricity Generation

- Biofertilizer Production

- Biogas Production

- Heat Generation

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Anaerobic Digestion Market, By Feedstock Type

- 5.1 Introduction

- 5.2 Agricultural Residues

- 5.3 Sewage Waste

- 5.4 Municipal Waste

- 5.5 Industrial Waste

- 5.6 Organic Waste

- 5.7 Other Feedstock Types

6 Global Anaerobic Digestion Market, By Capacity

- 6.1 Introduction

- 6.2 Small-scale

- 6.3 Medium-scale

- 6.4 Large-scale

7 Global Anaerobic Digestion Market, By Offering

- 7.1 Introduction

- 7.2 Hardware

- 7.2.1 Monitoring & Control Equipment

- 7.2.2 Feedstock Pre-processing Equipment

- 7.2.3 Digesters Tanks

- 7.2.4 Biogas Handling Equipment

- 7.2.5 Other Hardware

- 7.3 Services

- 7.3.1 Operations & Maintenance Services

- 7.3.2 Designing & Installation Services

- 7.4 Software

- 7.4.1 Data Management Software

- 7.4.2 Simulation Software

- 7.4.3 Energy Modeling Software

- 7.5 Other Offerings

8 Global Anaerobic Digestion Market, By Digestion System

- 8.1 Introduction

- 8.2 Thermophilic Anaerobic Digestion

- 8.3 Multi-Stage Anaerobic Digestion

- 8.4 Mesophilic Anaerobic Digestion

9 Global Anaerobic Digestion Market, By Application

- 9.1 Introduction

- 9.2 Electricity Generation

- 9.3 Biofertilizer Production

- 9.4 Biogas Production

- 9.5 Heat Generation

- 9.6 Other Applications

10 Global Anaerobic Digestion Market, By Geography

- 10.1 Introduction

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 France

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 New Zealand

- 10.4.6 South Korea

- 10.4.7 Rest of Asia Pacific

- 10.5 South America

- 10.5.1 Argentina

- 10.5.2 Brazil

- 10.5.3 Chile

- 10.5.4 Rest of South America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 Qatar

- 10.6.4 South Africa

- 10.6.5 Rest of Middle East & Africa

11 Key Developments

- 11.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 11.2 Acquisitions & Mergers

- 11.3 New Product Launch

- 11.4 Expansions

- 11.5 Other Key Strategies

12 Company Profiling

- 12.1 AAT Abwasser- und Abfalltechnik GmbH

- 12.2 Agraferm GmbH

- 12.3 Agrinz Technologies GmbH

- 12.4 Biogen

- 12.5 BTS Biogas Srl/GmbH

- 12.6 Capstone Green Energy Corporation

- 12.7 ENGIE SA

- 12.8 EnviTec Biogas AG

- 12.9 Evoqua Water Technologies LLC

- 12.10 Hitachi Zosen Inova AG

- 12.11 Nature Energy

- 12.12 Renewi plc

- 12.13 Veolia Water Technologies UK

- 12.14 Zero Waste Energy, LLC