|

|

市場調査レポート

商品コード

1444682

乳酸:市場シェア分析、業界動向と統計、成長予測(2024-2029)Lactic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 乳酸:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

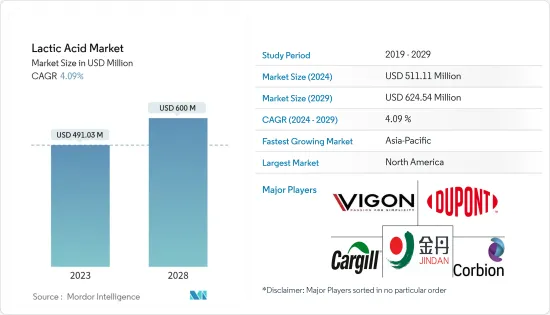

乳酸市場規模は、2024年に5億1,111万米ドルと推定され、2029年までに6億2,454万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.09%のCAGRで成長します。

乳酸には、その純度や用途に応じてさまざまなグレードがあります。医薬品や飲食品のさまざまな最終用途分野での乳酸の使用により、特にアジア太平洋などの新興地域で、予測期間中にこの製品の需要が高まると予想されます。乳酸のこうしたさまざまな機能的性質と国際規則による規制当局の承認が、乳酸市場の主な推進力となっています。

PLAは生分解性ポリマーであり、発酵プロセスで生成される乳酸などの再生可能資源から作られた堆肥化可能な熱可塑性プラスチックです。 PLAは主に乳酸から作られます。米国食品医薬品局はこの化学物質をGRASと宣言しました。これは、この化学物質が食品業界で大きな市場潜在力を持っていることを意味します。化学合成や発酵によっても作ることができます。

インスタント食品志向の高まりにより、発酵工程を必要とする加工食品には発酵工程で乳酸が含まれる傾向にあります。乳酸は、飲むヨーグルトやスプーンで食べるヨーグルトなどの発酵飲料に広く使用されており、消費者の間で人気が高まっています。この要因により、製造業者は乳酸および乳酸由来の成分を乳製品ベースの飲食品に組み込むことが奨励されています。これは主に、さまざまな乳製品ベースの製品における乳酸の食感を付与し、風味を高める性質があるためです。したがって、乳酸は世界中で乳製品に広く使用されています。

乳酸菌市場動向

食品酸味料の高い需要

乳酸は、その多様な機能特性により、食品および飲料製品において重要な成分です。食品および飲料分野における乳酸の幅広い用途と、食品酸味料によってもたらされるさまざまな機能的利点が市場を牽引しています。食品・飲料分野の堅調な拡大が業界を後押ししています。アジア太平洋における消費者行動の進化と経済発展に伴い、この地域は食品酸味料の使用を増やす食品・飲料業界にとって有望な市場として浮上しています。乳酸は保存産業でも広く使用されています。欧州、米国、オーストラリア、ニュージーランドでは食品添加物として許可されています。したがって、さまざまな食品製造プロセスで乳酸の使用量が増加すると、世界中で需要が増加する可能性があります。

アジア太平洋は最も急成長している地域市場です

食品添加物としての乳酸の使用の増加に伴い、アジア太平洋における乳酸の需要が急速に増加しています。肉およびその他の食品用途における乳酸の需要の増加、低コストの原材料の入手可能性、技術革新、およびこの地域の大手製造企業からの強力な支援が、市場の主な促進要因となっています。通常、乳酸は食肉産業において細菌ベースの病原体を減らすために使用され、肉を汚染から守ります。糖蜜、サトウキビ、デンプン、その他の炭水化物などの製造業者にとっての原材料の低コストは、最終製品のコストを即座に削減するため、この分野に大きな恩恵をもたらしています。河南金丹乳酸など、この地域で事業を展開している大手企業は、食品加工における重要な成分の1つとして乳酸を組み込むことに注力しています。

乳酸菌業界の概要

乳酸市場は本質的に高度に統合されています。市場における主な競合他社は、カーギル社、コービオンNV、河南金丹乳酸テクノロジー社、およびデュポンドヌムール社です。商品価格が不安定であるため、大手競合他社は自社の地位を維持するために新製品の開発とマーケティング戦略に投資することを好みます。ほとんどの主要企業は、新しく革新的なテクノロジーを開発するために研究開発に投資しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 由来

- 天然

- 合成

- 用途

- 肉、鶏肉、魚

- 飲料

- 菓子類

- ベーカリー

- 果物と野菜

- 乳製品

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Corbion NV

- Henan Jindan Lactic Acid Technology Co. Ltd

- Futerro SA

- DuPont de Nemours Inc.

- VIGON INTERNATIONAL INC.

- Cargill Incorporated

- Cellulac

- Galactic

- Mushashino Chemical

- Danimer Scientific

第7章 市場機会と将来の動向

第8章 出版社について

The Lactic Acid Market size is estimated at USD 511.11 million in 2024, and is expected to reach USD 624.54 million by 2029, growing at a CAGR of 4.09% during the forecast period (2024-2029).

Lactic acid comes in various grades, depending on its purity and intended use. The use of lactic acid in different end-use sectors, including pharmaceuticals and food and beverages, is expected to boost demand for this product over the forecast period, particularly in emerging regions like Asia-Pacific. These varied functional qualities of lactic acid and regulatory approval by international rules are the primary drivers for the lactic acid market.

PLA is a biodegradable polymer and compostable thermoplastic made from renewable sources such as lactic acid produced through fermentation processes. PLA is chiefly made from lactic acid. The US Food and Drug Administration has declared this chemical GRAS, which means it has significant market potential in the food business. It can also be made through chemical synthesis or fermentation.

With an increasing inclination toward convenience food, processed food that requires fermentation processes tends to include lactic acid in the fermentation process. Lactic acid is widely used in fermented beverages such as drinkable and spoonable yogurts, which are becoming popular among consumers. This factor has encouraged the manufacturers to incorporate lactic acid and derived ingredients in dairy-based food and beverages, mainly due to the texture-imparting and flavor-enhancing nature of lactic acid in various dairy-based products. Hence, lactic acid is extensively used in dairy-based products across the world.

Lactic Acid Market Trends

High Demand for Food Acidulants

Lactic acid is a crucial ingredient in food and beverage products due to its diverse functional qualities. Lactic acid's wide range of applications in the food and beverage sector and the variety of functional benefits offered by food acidulants drive the market. The industry is boosted by solid expansion in the food and beverage sector. With evolving consumer behavior and economic development in Asia-Pacific, the region emerges as a prospective market for the food and beverage industry to increase the use of food acidulants. Lactic acid is also widely used in the preservation industry. It is permitted as a food additive in Europe, the United States, Australia, and New Zealand. Hence, the increasing usage of lactic acid across various food manufacturing processes could possibly increase the demand across the world.

Asia-Pacific is the Fastest-growing Regional Market

With the rising use of lactic acid as a food additive, the demand for lactic acid in Asia-Pacific is rapidly increasing. Increased demand for lactic acid in meat and other foods applications, availability of low-cost raw materials, technological innovations, and strong backing from large manufacturing businesses in the region are the main drivers for the market. Usually, lactic acid is used in the meat-based industry to reduce bacterial-based pathogens, hence keeping the meat safe from contamination. The low cost of raw materials for manufacturers, such as molasses, sugarcane, starch, and other carbohydrates, has significantly benefited the sector as it immediately decreases the final product's cost. Major players operating in the region, such as Henan Jindan Lactic Acid Co. Ltd, are focusing on incorporating lactic acid as one of the key ingredients in food processing.

Lactic Acid Industry Overview

The lactic acid market is highly consolidated in nature. The leading competitors in the market are Cargill Incorporated, Corbion NV, Henan Jindan Lactic Acid Technology Co. Ltd, and DuPont de Nemour Inc. Due to commodity price instability, the big competitors prefer to invest in new product development and marketing strategies to maintain their positions. Most significant firms are investing in R&D to develop new and innovative technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Source

- 5.1.1 Natural

- 5.1.2 Synthetic

- 5.2 Application

- 5.2.1 Meat, Poultry, and Fish

- 5.2.2 Beverage

- 5.2.3 Confectionery

- 5.2.4 Bakery

- 5.2.5 Fruits and Vegetable

- 5.2.6 Dairy

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Corbion NV

- 6.3.2 Henan Jindan Lactic Acid Technology Co. Ltd

- 6.3.3 Futerro SA

- 6.3.4 DuPont de Nemours Inc.

- 6.3.5 VIGON INTERNATIONAL INC.

- 6.3.6 Cargill Incorporated

- 6.3.7 Cellulac

- 6.3.8 Galactic

- 6.3.9 Mushashino Chemical

- 6.3.10 Danimer Scientific