|

市場調査レポート

商品コード

1850135

アルファルファヘイ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Alfalfa Hay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アルファルファヘイ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月21日

発行: Mordor Intelligence

ページ情報: 英文 182 Pages

納期: 2~3営業日

|

概要

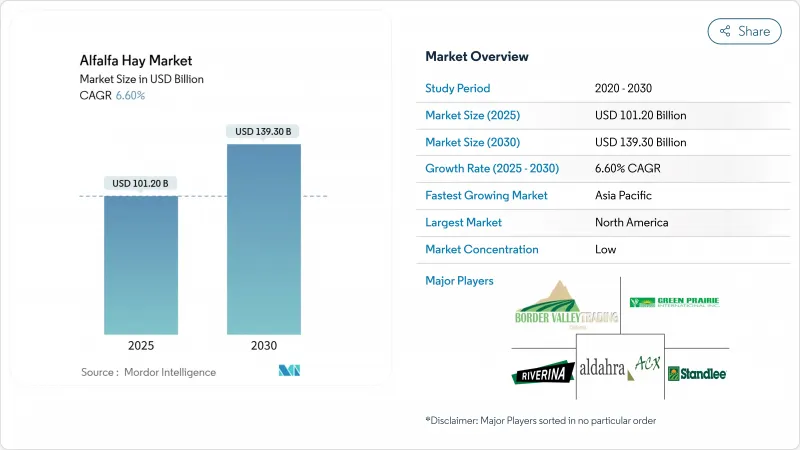

アルファルファヘイ市場の2025年の市場規模は1,012億米ドルで、2030年には1,393億米ドルに達し、CAGR 6.6%で成長すると予測されています。

市場の成長は、世界のアルファルファ作付面積の46%が干ばつ状態に直面しているにもかかわらず、乳製品需要の増加、アルファルファの高い栄養価、水効率の高い加工技術への投資が牽引しています。北米が最大市場の座を維持する一方、アジア太平洋地域はタンパク質消費の増加と強力な飼料輸入プログラムにより急成長を示しています。市場は依然として細分化されており、水、労働力、輸送コストの上昇を管理できる資金力のある企業にチャンスをもたらしています。炭素クレジットプログラムや太陽光発電による脱水プロセスなどの持続可能性イニシアチブの開発は、こうした運用コストの相殺に役立ち、アルファルファヘイ市場の長期的収益性を向上させる。

世界のアルファルファヘイ市場の動向と洞察

乳製品と動物性タンパク質の需要急増

動物性タンパク質への世界的なシフトが飼料調達戦略に影響を与えています。インド、インドネシア、ベトナムで拡大する酪農事業は、一貫したタンパク質密度を重視する正式な購入契約を結んでおり、高リシンアルファルファは飼料配合に不可欠となっています。米国の生乳加工業者は、粗タンパク質アルファルファを18~22%含む飼料は乳量とバター脂肪の質を向上させると報告しています。馬の分野では、パフォーマンスに重点を置いているため、プレミアムグレードの購入が維持されており、高品質アルファルファの安定した価格プレミアムを支えています。牛群の拡大と飼料転換の必要性が組み合わさることで、生産性の向上を目指す生産者にとってアルファルファヘイが重要な要素となっています。

飼料輸入プログラムの拡大

明確な構造を持つ輸入プログラムは、価格の安定と一貫した需要パターンの確立に役立ちます。日本は為替変動にもかかわらず2023年に35万6,504トンの輸入を維持し、サウジアラビアは水使用規制の強化を受けて輸入量を43万1,400トンに増やしました。2030年までに国内生産面積を900万ヘクタールまで拡大するという中国の計画は、現在の輸入需要を牽引しており、2023年の出荷量が47%減少するにもかかわらず、北米の輸出業者に安定したビジネスを提供しています。これらのプログラムに基づく長期供給契約は、明確な需要予測を提供し、出荷効率を改善するための脱水・圧縮設備への輸出業者の投資をサポートします。

ウォーターフットプリントと干ばつ政策の圧力

アリゾナ州で2024年に外資が所有するアルファルファ農場のリース契約が打ち切られたことで、水集約型農業に対する懸念が高まっていることが浮き彫りになりました。干ばつは世界のアルファルファ生産地の約50%に影響を及ぼし、農家は赤字灌漑方法を採用するようになります。こうしたやり方は収量を15~20%減少させるが、飼料としての価値は高まる可能性があります。精密灌漑システムや干ばつに強い品種はリスク管理に役立つが、コストが高いため小規模農家には影響があります。カリフォルニアの貯水池レベルの低下とオーストラリアの水配分制限により、市場の不確実性が生じ、アルファルファ生産は北米全域で北上し内陸部へとシフトしています。

セグメント分析

2024年のアルファルファヘイ市場の43.0%は俵であり、これは確立されたハンドリングシステムと畜産業者への普及に支えられています。機械化された酪農場は大きな四角いベールを好み、一方、丸いベールは大規模な牛肉経営に天候保護を提供します。このような形態の多様性により、各地域で一貫した需要が確保されています。脱水ペレットは市場シェアが小さいが、自動給餌システムと、海上輸送コストを削減するコンテナ積載密度の増加により、CAGRは7.6%となっています。ペレットはまた、一貫した品質を提供し、酪農や馬の市場にサービスを提供する配合飼料工場の配合工程を簡素化します。

移動式ペレットラインへの投資は、エネルギー消費量の増加を補い、ベール価格を上回るトン当たり30~40米ドルのプレミアムを生み出します。キューブや圧縮ベールは、ユーザーがコストよりも利便性を優先する馬や小型反芻家畜のセグメントに対応しています。1.5時間以内に含水率を12%以下にするフィールド・ドライヤーは、収穫期の天候リスクを最小限に抑えます。これらの技術的進歩は、アルファルファヘイ市場を強化し、加工フォーマットへの移行を加速します。

シュプリームグレードのアルファルファヘイは2024年の市場シェアの28.3%を占め、CAGR 6.1%と最も高い成長率を達成したが、これはタンパク質が豊富な飼料に対する需要の増加を示しています。プレミアムグレード(RFV 170-185)は、コストと生乳生産目標の最適なバランスを提供することで、商業酪農場の間で支配的な地位を維持しています。グッドグレードは、主にコスト効率の高い消化性タンパク質含有量を重視する肉牛経営に供給されています。フェア等級とユーティリティ等級は、バイヤーがマイコトキシンと汚染物質の制限を厳しくしているため、市場での存在感が低下しています。

品質評価では、検査した中国産サンプルのすべてにマイコトキシンが検出されたため、プレミアム・バイヤーは北米のサプライヤーにシフトしています。正確な収穫時期、効率的な現場乾燥方法、高度な貯蔵モニタリング・システムを導入している生産者は、トン当たり50~60米ドルの価格プレミアムを確保することができ、品質基準に基づく市場の価値差別化を実証しています。

アルファルファヘイ市場レポートは、製品タイプ(ベールなど)、グレード(シュプリームなど)、加工技術(現場乾燥従来型など)、流通チャネル(直接農場ゲートなど)、畜産用途(乳牛飼料など)、最終用途セクター(商業農場など)、地域(北米など)別に分類しています。市場予測は金額(米ドル)と数量(メトリックトン)で提供されます。

地域分析

北米は2024年の売上高の36.2%を占め、機械化されたオペレーション、質の高い格付けシステム、太平洋の輸出ターミナルへのアクセスに支えられています。米国の乾牧草生産量は3.3%増の1億2,250万トンとなったが、アリゾナ州とカリフォルニア州における水政策の変更が生産地にリスクをもたらしました。ウィスコンシン州は生産量を75%増の303万トンとし、地域的な適応を示したが、これは水資源が確保されている地域への栽培転換の可能性を示唆しています。

アジア太平洋は2030年までCAGR 6.8%で成長すると予想されています。インドと東南アジアにおける酪農経営の近代化が飼料需要を牽引する一方、中国は数量調整にもかかわらず、88万6,661トンと最大の輸入国としての地位を維持しています。中国は国内生産の拡大を目指しているが、牛群の増加により短期的な輸入需要は続きます。ナムルディ・プロジェクトの中断に伴うオーストラリアの乾牧草供給制約は、気候関連の脆弱性を浮き彫りにしています。

欧州は、持続可能性とトレーサビリティに重点を置いて安定した需要を維持しており、炭素認証を取得した生産者が市場で優位に立っています。南米は、特にチリとアルゼンチンにおいて、適切な気候条件と改善された港湾施設の恩恵を受けて、競争力のある輸出国として開発されつつあります。中東市場は、水の制約から引き続き輸入に依存しており、2024年にはサウジアラビアが日本を抜いて第2位の輸入国になります。アフリカでは、ケニアとナイジェリアで商業的酪農事業が拡大し、アルファルファヘイ市場の将来的機会を示唆するように、初期成長の可能性を示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 乳製品と動物性タンパク質の需要急増

- 飼料輸入プログラムの拡大

- 優れたタンパク質と繊維プロファイル

- 炭素クレジットと土壌健全性の収益化

- 外出先での乾燥とベール圧縮技術で損失を削減

- DDGS(蒸留乾燥穀物可溶性穀物)価格の高騰が飼料タンパク質の使用量増加を促進

- 市場抑制要因

- 水フットプリントと干ばつ政策への圧力

- 海上運賃とコンテナ運賃の変動

- 水耕飼料と代替粗飼料の台頭

- 輸出レーンにおける植物検疫上の障壁

- バリューチェーン/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- ベール

- ラウンドベール

- スクエアベール

- ペレット

- キューブ

- 脱水ペレット

- 圧縮ベール

- ベール

- グレード/品質別

- 最上(RFV 185以上)

- 上(RFV 170-185)

- 良(RFV 150-169)

- 可(RFV 130-149)

- ユーティリティ(RFV 130未満)

- 処理技術別

- 野外乾燥従来型

- 強制空気移動式乾燥機

- ロータリードラム脱水

- 太陽光を利用した脱水

- 流通チャネル別

- ダイレクトファームゲート

- 輸出商社

- 飼料インテグレーターおよびミル

- eコマース/オンラインプラットフォーム

- 家畜用途別

- 乳牛飼料

- 肉牛飼料

- 家禽飼料

- 馬用飼料

- 小型反芻動物用飼料

- ラクダ科動物とその他

- 最終用途セクター別

- 商業農場

- 配合飼料メーカー

- 家庭/趣味で動物を飼っている人

- ペットフードと特殊栄養

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- ケニア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- AL Dahra ACX Global Inc.

- Anderson Hay & Grain Co., Inc.

- Standlee Premium Products, LLC

- Border Valley Trading

- Alfalfa Monegros

- Grupo Oses(Nafosa)

- Gruppo Carli

- Green Prairie International Inc

- Cubeit Hay Company

- Haykingdom Inc.

- SL Follen Company

- Riverina

- McCracken Hay Company

- Bailey Farms International

- Hay USA Inc