|

市場調査レポート

商品コード

1443996

農業用燻蒸剤:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Agricultural Fumigants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農業用燻蒸剤:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

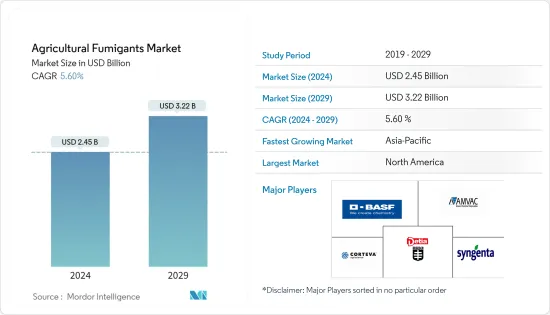

農業用燻蒸剤の市場規模は、2024年に24億5,000万米ドルと推定され、2029年までに32億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.60%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックにより、燻蒸剤を含む農薬市場の運営が混乱しました。パンデミックはサプライチェーンネットワークに影響を与え、企業や農家に損失をもたらしました。供給面では、流通のボトルネックによる短期的な移民労働者の不足により、生産に必要な労働者の数との間に大きな格差が生じた。その他の制限には、通関、輸出許可、輸入許可、植物検疫証明書などが含まれます。

農業用燻蒸剤市場は、農業分野における急速な技術進歩、収穫後の損失に対する懸念の高まり、収量の増加につながった先進的な農業慣行の変化などの要因によって動かされています。保管中に燻蒸剤を使用すると、保管損失の削減に役立ちます。したがって、燻蒸剤の使用は収穫後の損失を軽減する効果的かつ経済的な方法であるため、燻蒸剤の需要は増加すると予想されます。

ホスフィン系燻蒸剤は、昆虫やげっ歯類から保護しながら農産物を保管するために広く使用されており、世界のあらゆる種類の燻蒸剤の中で最大のセグメントとして浮上しています。北米が市場を独占しています。技術と研究開発への急速な投資により、毒性が低く、効率が向上した多くの新しい種類の製品が開発されています。農業用燻蒸剤市場の成長は、農産物の品質向上に対する消費者の傾向の高まり、農業慣行の変化、高度な保管技術など、いくつかの要因に起因すると考えられます。しかし、燻蒸剤は、作物の種類や品種、季節条件、湿度、温度、燻蒸剤の濃度、処理期間に応じて、植物毒性の可能性など、いくつかの問題を引き起こします。したがって、呼吸器毒としての毒性が高いため、専門の燻蒸者のみが使用することをお勧めします。

農業用燻蒸剤の市場動向

農業生産の拡大

農業生産の増加に伴い、燻蒸剤の需要は長年にわたって増加傾向にあります。燻蒸の使用は穀物と油糧種子のサプライチェーンのあらゆるレベルで増加しており、農場レベルでの主要な昆虫管理オプションとして浮上しています。農場レベルの保管やサイロ内での燻蒸は、害虫の抵抗性を回避しながら害虫の侵入の蓄積を防ぐ最も好ましい方法の1つです。ただし、法律上の制限により、利用できる活性物質は限られた数の燻蒸剤および貯蔵殺虫剤に制限されています。臭化メチル(MB)燻蒸は、製品が植物検疫上のリスクを最小限に抑えるための効果的な処理です。欧州連合はMBの使用を禁止していますが、カナダは依然として、一部の製品の検疫および出荷前の用途で承認された唯一の治療法としてMBを要求しています。

国連食糧農業機関(FAO)は、増大する食料需要を満たすために、農業生産性が2050年までに70%増加する可能性が高いと予測しています。農作物の需要は、2050年までに約67億5,900万トンに増加すると予想されています。世界の穀物生産量は、2018年の29億650万トンから2020年には29億9,610万トンに増加しました。したがって、農業用倉庫、保管技術、および次のような関連製品に対する需要が高まっています。燻蒸剤は長期的には増加すると予想されます。倉庫ではほとんどの作物が害虫によって被害を受けており、燻蒸剤の使用により農産物の損失が減少します。したがって、これにより、世界中の農業用燻蒸剤市場の需要が高まると予想されます。

世界市場をリードする北米

北米は農業用燻蒸剤の最大の市場であり、主要国で250以上の認定製品が入手可能です。食品および穀物の加工および保管業界では、保管製品の昆虫の管理が大きな関心事であり、広く研究されているテーマです。

この地域で貯蔵および土壌用途の両方に燻蒸剤を消費する主な品目は、トウモロコシ、米、大麦、ジャガイモ、トマト、小麦、イチゴ、キャベツなどです。北米では、米国が最大の市場であり、半分以上を占めています。地域市場のシェア。米国市場の主要な燻蒸剤には、クロロピクリン、フッ化スルフリル、リン化アルミニウム、酸化エチレンなどが含まれます。カナダでは90を超える燻蒸剤ベースの製品が登録されており、25社が製造しています。主要企業としては、AMVAC Chemicals、Degesch America Inc.、Syngenta Canada Inc.、United Phosphorus Inc.などが挙げられます。

農業用燻蒸剤業界の概要

世界の農業用燻蒸剤市場は統合されており、数社が最大の市場シェアを占めています。北米と欧州の市場は高度に統合されており、少数の大手企業が大きな市場シェアを占め、高いレベルの競合が繰り広げられています。新製品イントロダクションの根幹となる研究開発によるポートフォリオの多様化は、成熟市場の更なる激化に向けて適用されている顕著な戦略の1つです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ

- 臭化メチル

- クロロピクリン

- ホスフィン

- メタムナトリウム

- 1,3-ジクロロプロペン

- その他

- 適用方法

- 土壌

- 倉庫

- 形態

- 固体

- 液体

- ガス

- 作物適用

- 作物ベース

- 非作物ベース

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- DowDuPont

- Amvac Chemical Corporation

- Syngenta AG

- UPL Group

- Detia Degesch GmbH

- ADAMA Agricultural Solution Ltd

- BASF SE

- Cytec Solvay Group

- FMC Corporation

- Fumigation Services

- Ikeda Kogyo Co. Ltd

- Industrial Fumigation Company

- Isagro SpA

- Lanxess

- Reddick Fumigants LLC

- Trical Inc.

- TriEst Ag Group Inc.

- VFC

- Industrial Fumigation Company

第7章 市場機会と将来の動向

第8章 COVID-19が市場に与える影響の評価

The Agricultural Fumigants Market size is estimated at USD 2.45 billion in 2024, and is expected to reach USD 3.22 billion by 2029, growing at a CAGR of 5.60% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the operations of the crop protection chemicals market, including fumigants. The pandemic affected supply chain networks, resulting in losses for companies and farmers. In terms of supply, a short-term shortage of migrant laborers amid distribution bottlenecks created a wide gap between the number of workers required for production. Some other restraints included customs clearances, export permits, import permits, and phytosanitary certificates.

The agricultural fumigants market is driven by factors, like rapid technological advancements in the agricultural sector, growing concerns over post-harvest losses, and a shift in the advanced farming practices, which have led to increased yields. The use of fumigants during storage helps in the reduction of storage loss. Thus, the demand for fumigants is expected to increase as the use of fumigants is an effective and economical method to reduce post-harvest losses.

A widely used fumigant for storing agricultural commodities while offering protection against insects and rodents, phosphine-based fumigants have emerged as the largest segment among all types of global fumigants. North America dominates the market. With rapid investments in technology and R&D, many new varieties of products are being developed with less toxicity and more efficiency. The growth of the agricultural fumigants market can be attributed to several factors, such as the increased inclination of consumers for improving the quality of agricultural output, changing farming practices, and advanced storage technology. However, fumigants cause several problems, including possible phytotoxicity, depending on the type of crop and its variety, seasonal conditions, humidity, temperature, fumigant concentration, and duration of treatment. Therefore, it is recommended to be used by professional fumigators only due to its high toxicity as a respiratory poison.

Agricultural Fumigants Market Trends

Growing Agricultural Production

In line with increasing agricultural production, the demand for fumigants has been witnessing an upward trend over the years. The use of fumigation has increased at all levels of the grain and oilseeds supply chain, emerging as the main insect management option at the farm level. For farm-level storage and in silos, fumigation is among the most preferred methods to prevent the build-up of insect infestations while avoiding pest resistance. However, the available active substances are constrained to a limited number of fumigants and storage insecticides due to legislative restrictions. Methyl bromide (MB) fumigation is an effective treatment to ensure that products pose a minimal phytosanitary risk. While the European Union has banned the use of MB, Canada still requires it as the only approved treatment for the quarantine and pre-shipment applications of some products.

The Food and Agriculture Organization (FAO) of the United Nations has predicted that agricultural productivity is likely to increase by 70% by 2050 in order to meet the growing demand for food. The demand for agricultural crops is expected to rise to around 6,759 million ton by 2050. Global cereal production increased from 2906.5 million ton in 2018 to 2996.1 million ton in 2020. Thus, the demand for agricultural warehouses, storage technologies, and associated products, like fumigants, is anticipated to grow in the long run. In warehouses, pests damage most crops, and the use of fumigants decrease the loss of agricultural products. Therefore, this is expected to boost demand for the agricultural fumigants market across the world.

North America Leading the Global Market

North America is the largest market for agricultural fumigants, with over 250 authorized products available in its major countries. Management of stored product insects is a major concern and widely researched topic in the food and grain processing and storage industry.

The major commodities consuming fumigants for both storage and soil applications in the region are corn, rice, barley, potato, tomato, wheat, strawberry, cabbage, etc. In North America, the United States is the largest market, accounting for more than half of the regional market's share. The major fumigants in the US market include chloropicrin, sulfuryl fluoride, aluminum phosphide, ethylene oxide, etc. Over 90 fumigant-based products are registered in Canada, manufactured by 25 companies. A few key players are AMVAC Chemicals, Degesch America Inc., Syngenta Canada Inc., United Phosphorus Inc., etc.

Agricultural Fumigants Industry Overview

The global agricultural fumigants market is consolidated, with a few companies occupying the largest market share. The markets in North America and Europe are highly consolidated, with a few major players occupying large market shares and having a high level of competition. Diversification of portfolios through R&D, which is the backbone of the introduction of new products, is one of the prominent strategies being applied to the matured markets for further intensification.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Methyl Bromide

- 5.1.2 Chloropicrin

- 5.1.3 Phosphine

- 5.1.4 Metam Sodium

- 5.1.5 1,3-Dichloropropene

- 5.1.6 Other Agricultural Fumigants

- 5.2 Method of Application

- 5.2.1 Soil

- 5.2.2 Warehouse

- 5.3 Form

- 5.3.1 Solid

- 5.3.2 Liquid

- 5.3.3 Gas

- 5.4 Crop Application

- 5.4.1 Crop-based

- 5.4.2 Non-crop-based

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Spain

- 5.5.2.6 Italy

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 DowDuPont

- 6.3.2 Amvac Chemical Corporation

- 6.3.3 Syngenta AG

- 6.3.4 UPL Group

- 6.3.5 Detia Degesch GmbH

- 6.3.6 ADAMA Agricultural Solution Ltd

- 6.3.7 BASF SE

- 6.3.8 Cytec Solvay Group

- 6.3.9 FMC Corporation

- 6.3.10 Fumigation Services

- 6.3.11 Ikeda Kogyo Co. Ltd

- 6.3.12 Industrial Fumigation Company

- 6.3.13 Isagro SpA

- 6.3.14 Lanxess

- 6.3.15 Reddick Fumigants LLC

- 6.3.16 Trical Inc.

- 6.3.17 TriEst Ag Group Inc.

- 6.3.18 VFC

- 6.3.19 Industrial Fumigation Company