|

市場調査レポート

商品コード

1444097

膵臓がん治療・診断:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Pancreatic Cancer Therapeutics and Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 膵臓がん治療・診断:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 204 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

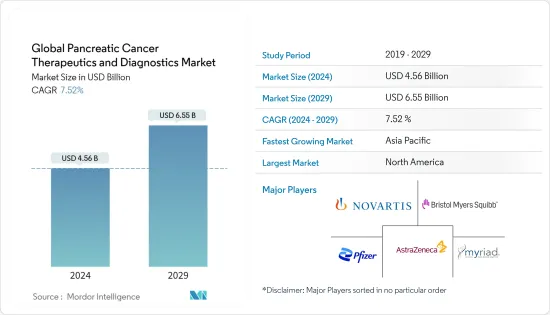

世界の膵臓がん治療・診断市場規模は、2024年に45億6,000万米ドルと推定され、2029年までに65億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.52%のCAGRで成長します。

COVID-19の発生により、病院と医療サービスが大幅に減少し、膵臓がん治療・診断市場に影響を与えました。さらに、COVID-19のパンデミックは世界経済に影響を及ぼし、病院での新型コロナウイルス感染症以外の患者に対する一般的な病院医療の機能に大きな影響を与えました。 2020年 6月、国立バイオテクノロジー情報センターに掲載された記事では、COVID-19のパンデミックが世界中で内視鏡装置の使用に与える影響について研究しました。この研究では、2020年4月23日から5月12日まで6大陸の55か国を調査しました。この研究では、COVID-19のパンデミック中に実施された内視鏡検査の数が減少し、基準値と比較して83%減少したことがわかりました。この研究では、同じ期間に上部内視鏡検査が82%減少し、下部内視鏡検査が85%減少したことも判明しました。 2020年8月、がん患者の膵臓手術に対するCOVID-19の影響に関する調査結果がPubMedに発表されました。この調査は、37か国の267センターからの337人の回答者を対象に実施されました。調査によると、COVID-19のパンデミックにより、ほとんどのセンターで膵臓手術の実施件数が減り、週当たりの膵臓切除率が3件から1件に減少しました。したがって、COVID-19のパンデミックは、調査対象市場の成長に大きな影響を与えると予想されます。

膵臓がん治療・診断には、膵臓がんの診断とその後の治療に使用される医療手順が含まれます。膵臓がんの有病率と発生率の増加、分子生物学、医薬品の開発、診断技術の進歩などの要因が市場の成長に大きな役割を果たしています。研究開発の取り組みの増加、有利な償還シナリオ、新製品の発売により、市場は予測期間中に大幅に成長すると予想されます。 2021年1月、Myriad Genetics Inc.は、膵臓がん検診にも使用されているBRACAnalysis診断システムについて、日本の厚生労働省から償還を受けると発表しました。この取り組みにより、日本における膵臓がんの遺伝子検査の患者数が増加すると期待されています。また、市場では多くのコラボレーションが行われており、市場開発にプラスの影響を与えることが期待されています。 2020年10月、Oncolytics Biotech Inc.は、転移性膵臓がんの治療におけるペラオレップおよびアテゾリズマブの有効性を試験する第1/2相試験でロシュおよびAIOと提携すると発表しました。したがって、これらの発展は、予測期間中の調査対象の市場の成長にプラスの影響を与えると予想されます。

膵臓がん治療・診断市場動向

化学療法セグメントは、予測期間中に調査対象市場で大きなシェアを獲得すると予想される

化学療法は、膵臓がん細胞の増殖と分裂を阻止することで膵臓がん細胞を死滅させる主要ながん治療法の1つです。これらの薬は全身治療です。薬物は血流を通って移動し、体中のがん細胞に損傷を与えます。残念ながら、化学療法は一部の健康な細胞を損傷し、重大な副作用を引き起こす可能性があります。化学療法は膵臓腫瘍を縮小させたり、増殖を防止したりする可能性があります。米国がん協会によると、膵臓がんの治療に使用される化学療法薬には、ゲムシタビン(ジェムザール)、5-フルオロウラシル(5-FU)、イリノテカン(カンプトサール)、オキサリプラチン(エロキサチン)、アルブミン結合パクリタキセル(アブラキサン)、カペシタビン(ゼローダ)、シスプラチン、パクリタキセル(タキソール)、ドセタキセル(タキソテール)、およびイリノテカンリポソーム(オニバイド)があります。

1990年代以来、化学療法薬ゲムシタビン(ジェムザール)は、手術で切除できる(切除可能)膵臓がん患者の治療の中核となってきました。伝統的に、ゲムシタビンは患者が手術から回復した後に補助化学療法として投与されてきたが、この手術は多くの患者にとってホイップル手術として知られる過酷な手術です。最近では、ゲムシタビンは化学療法薬カペシタビン(ゼローダ)と併用されることがあります。化学療法は、単独で、または手術、標的療法、免疫療法、および/または放射線療法と組み合わせて行われることもあります。化学療法を放射線と組み合わせて行う場合、通常は低用量の化学療法が使用されます。放射線療法と併用して最も一般的に使用される化学療法薬は、フルオロウラシル(5-FU)とゲムシタビン(ジェムザール)です。 5-FUは放射線と併用した経験が豊富であり、副作用が少ないため、最も頻繁に使用されます。

2020年3月、ルストガルテン財団とスタンド・アップ・トゥ・キャンサー(SU2C)の戦略的パートナーシップである膵臓がんコレクティブは、ダナ・ファーバーがん研究所のチームを含むトップ研究者の4チームに最大1,600万米ドルを授与されました。 New Therapies Challenge Grants、American Association for Cancer調査(AACR)、およびSU2Cの科学パートナーの一部です。化学療法と組み合わせたDNA修復阻害剤を試験する3件の膵臓がん臨床試験を支援するために、400万米ドル近くの資金が利用可能です。したがって、膵臓がんの効果的な治療選択肢に対する需要が急増しているため、研究対象セグメントは予測期間中に大幅な成長を遂げると予想されます。

北米が市場全体を支配し、今後もその優位性を維持すると予想される

米国は、膵臓がんの発生率の上昇、補助的な償還政策、高額な医療支出により、重要な市場シェアを維持すると予想されています。

MedCrave Gastroenterology and Hepatologyジャーナルの2018年の発表によると、膵臓がんは発生率が中程度であるにもかかわらず、9番目に頻度の高いがんでした。 2030年までに、膵臓がんはがんの死亡原因の中で2番目に多いものになると予想されています。また、GLOBOCAN 2020レポートによると、2020年には新たに約56,654人の膵臓がん患者が報告されました。さらに、2020年には膵臓がんによる約47,683人の死亡が報告されました。米国。 USFDAはまた、臨床段階で医薬品を承認し、それによって臨床開発を加速することにより、膵臓がんの治療薬および診断市場の成長を促進するための措置を講じています。企業や調査機関は研究開発に投資しています。したがって、市場は急速に拡大しています。たとえば、2020年にエリテックの主要製品候補であるエリアスパーゼは、国内の二次治療の転移性膵臓がん患者に対する新たな治療選択肢の可能性が緊急に必要とされていることから、FDAからファストトラック指定を受けました。 FDAによるこのような製品の承認は、市場全体を押し上げると予想されます。

2020年、NANOBIOTIXは膵臓がんを対象としたNBXR3を用いた最初の第I相試験を発表したが、これは米国FDAに従って安全に実施できるものです。この治験はNanobiotixと共同開発され、MDアンダーソンが治験のスポンサーおよび実施者です。これらの臨床試験の良好な結果は新しい治療法をもたらし、地域市場の成長にプラスの影響を与えるでしょう。したがって、上記の要因により、調査対象の市場は、この地域で予測期間中に大幅な成長を記録すると予想されます。

膵臓がん治療・診断業界の概要

膵臓がん治療・診断市場は競争が激しく、多くの主要企業が市場を独占しています。 Novartis AG、Pfizer Inc.、Bristol-Myers Squibb Company、AstraZeneca PLC、Myriad Genetics Inc.、Viatris Inc.などの大手市場プレーヤーの存在により、競合が激化しています。市場プレーヤーは、激化する市場競争を維持するために、研究開発投資の増加、合併、買収、製品革新などの戦略を採用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 膵臓がんの発生率と有病率の増加

- 分子生物学の進歩、医薬品開発、診断技術

- 市場抑制要因

- 診断と治療に伴う高額な費用

- 厳格な規則性ガイドライン

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ別

- 治療別

- 標的療法

- 化学療法

- 手術

- その他

- 診断別

- イメージング

- 生検

- 超音波内視鏡

- その他

- 治療別

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Myriad Genetics Inc.

- Pfizer Inc.

- Novartis AG

- Bristol-Myers Squibb Company

- AstraZeneca PLC

- Amgen Inc.

- Viatris Inc.

- Boston Scientific Corporation

- FUJIFILM Holdings Corporation

- Canon Inc.(canon Medical Systems Corporation)

- Rafael Holdings Inc(rafael Pharmaceuticals)

- Immunovia AB

- Apexigen Inc.

- Merck KGaA

- F Hoffmann-La Roche AG

第7章 市場機会と将来の動向

The Global Pancreatic Cancer Therapeutics and Diagnostics Market size is estimated at USD 4.56 billion in 2024, and is expected to reach USD 6.55 billion by 2029, growing at a CAGR of 7.52% during the forecast period (2024-2029).

The outbreak of COVID-19 significantly reduced hospital and healthcare services, impacting the pancreatic cancer therapeutics and diagnostics market. Moreover, the COVID-19 pandemic affected the global economy and showed a huge impact on the functioning of general hospital care for non-COVID-19 patients in hospitals. In June 2020, an article appearing in the National Center for Biotechnology Information studied the impact of the COVID-19 pandemic on the use of endoscopy units globally. The study looked into 55 countries across 6 continents from April 23 to May 12, 2020. The study found that the number of endoscopy procedures performed during the COVID-19 pandemic decreased, constituting an 83% reduction compared to the baseline figures. The study also found out that there was an 82% reduction in upper endoscopy procedures and an 85% reduction in lower endoscopy procedures during the same time. In August 2020, a survey was published in PubMed on the impact of COVID-19 on pancreatic surgery for cancer patients. The survey was conducted amongst 337 respondents from 267 centers from 37 countries. According to the survey, most centers performed fewer pancreatic surgeries due to the COVID-19 pandemic, which reduced the weekly pancreatic resection rate from 3 to 1. Thus, the COVID-19 pandemic is expected to impact the studied market's growth significantly.

Pancreatic cancer therapeutics and diagnostics involve medical procedures used to diagnose pancreatic cancer and subsequent treatment. Factors such as the increasing prevalence and incidence of pancreatic cancer and advancements in molecular biology, development of drugs, and diagnostic technology play a major part in market growth. With the increase in R&D initiatives, favorable reimbursement scenarios, and the launch of novel products, the market is expected to grow significantly during the forecast period. In January 2019, scientists from the Van Andel Research Institute (VARI) developed a novel blood test (CA19-9 test) that, when combined with an existing test, can detect nearly 70% of pancreatic cancers with a less than 5% of false-positive rate. Moreover, in January 2021, Myriad Genetics Inc. announced that it would receive reimbursement for its BRACAnalysis Diagnostic System, which is also used for pancreatic cancer screening from Japan's Ministry of Health, Labour, and Welfare. The initiative is expected to increase the patient pool for genetic testing for pancreatic cancer in Japan. Also, many collaborations are taking place in the market, which is expected to affect market development positively. In October 2020, Oncolytics Biotech Inc. announced a collaboration with Roche and AIO for a phase 1/2 trial of testing the efficacy of pelareorep and atezolizumab in the treatment of metastatic pancreatic cancer. Thus, these developments are expected to impact the studied market growth over the forecast period positively.

Pancreatic Cancer Therapeutics & Diagnostics Market Trends

The Chemotherapy Segment is Expected to Witness a Major Share in the Studied Market Over the Forecast Period

Chemotherapy is one of the main cancer treatments that kill pancreatic cancer cells by preventing them from growing and dividing. These drugs are systemic treatments; the drugs travel through the bloodstream and damage cancer cells throughout the body. Unfortunately, chemotherapy can damage some healthy cells and cause major side effects. Chemotherapy may shrink and/or prevent the growth of pancreatic tumors. According to the American Cancer Society, the chemotherapy drugs used to treat pancreatic cancer include Gemcitabine (Gemzar), 5-fluorouracil (5-FU), Irinotecan (Camptosar), Oxaliplatin (Eloxatin), Albumin-bound paclitaxel (Abraxane), Capecitabine (Xeloda), Cisplatin, Paclitaxel (Taxol), Docetaxel (Taxotere), and Irinotecan liposome (Onivyde).

Since the 1990s, the chemotherapy drug gemcitabine (Gemzar) has been the backbone of treating people with pancreatic cancer that can be removed with surgery (resectable). Traditionally, gemcitabine has been given as adjuvant chemotherapy after the patient has recovered from the surgery, which, for many patients, is a grueling procedure known as the Whipple procedure. More recently, gemcitabine is sometimes combined with the chemotherapy drug capecitabine (Xeloda). Chemotherapy may also be given alone or combined with surgery, targeted therapy, immunotherapy, and/or radiation. When chemotherapy is given in combination with radiation, a low dose of chemotherapy is typically used. The chemotherapy drugs most commonly used in conjunction with radiation therapy are fluorouracil (5-FU) and gemcitabine (Gemzar). 5-FU is used most often since there is more experience using this drug in combination with radiation, and there are fewer side effects.

In March 2020, the Pancreatic Cancer Collective, the strategic partnership of the Lustgarten Foundation and Stand Up To Cancer (SU2C), was awarded up to USD 16 million to four teams of top researchers, including a team at Dana-Farber Cancer Institute, as part of its New Therapies Challenge Grants, the American Association for Cancer Research (AACR), and Scientific Partner of SU2C. Nearly USD 4 million in funding is available to help support three pancreatic cancer clinical trials testing DNA repair inhibitors combined with chemotherapy. Thus, due to the surging demand for effective treatment options for pancreatic cancers, the studied segment is expected to witness significant growth over the forecast period.

North America Dominated the Overall Market and is Expected to Retain its Dominance

The United States is expected to retain its significant market share due to the rising incidence of pancreatic cancers, supportive reimbursement policies, and high healthcare spending.

As per a 2018 publication in the MedCrave Gastroenterology and Hepatology journal, pancreatic cancer was the ninth most frequent cancer, despite its moderate incidence. It was expected to be among the second-deadliest cause of cancer by 2030. Also, according to the GLOBOCAN 2020 report, about 56,654 new cases of pancreatic cancer were reported in 2020. Moreover, approximately 47,683 deaths due to pancreatic cancer were reported in the United States. The USFDA is also taking steps to enhance the growth of the pancreatic cancer therapeutics and diagnostic market by approving drugs in the clinical phase, thereby accelerating clinical developments. Companies and research organizations are investing in R&D. Thus, the market is expanding quickly. For instance, in 2020, ERYTECH's lead product candidate, eryaspase, received the fast track designation by the FDA due to the urgent need for potential new treatment options for patients with second-line metastatic pancreatic cancer in the country. Such product approvals by the FDA are expected to lift the overall market.

In 2020, NANOBIOTIX announced its first phase I trial with NBTXR3 in Pancreatic Cancer, which is safe to proceed as per the US FDA. The trial was co-developed with Nanobiotix, and MD Anderson is the sponsor and executor of the trial. These clinical trials' positive outcomes will result in a new treatment, positively influencing the regional market growth. Thus, owing to the factors mentioned above, the studied market is anticipated to register significant growth over the forecast period in the region.

Pancreatic Cancer Therapeutics & Diagnostics Industry Overview

The Pancreatic Cancer Therapeutics and Diagnostics market is highly competitive, with many key players dominating the market. The presence of major market players like Novartis AG, Pfizer Inc., Bristol-Myers Squibb Company, AstraZeneca PLC, Myriad Genetics Inc., and Viatris Inc. is intensifying the competition. The market players are adopting strategies, such as rising R&D investments, mergers, acquisitions, and product innovations, to sustain the increasing market rivalry. For instance, in January 2021, Myriad Genetics Inc. entered into a strategic partnership with Illumina Inc. for the latter to create a kit-based version of the myChoice companion diagnostic (CDx) test for international markets, which can be used to detect pancreatic cancer.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence and Prevalence of Pancreatic Cancer

- 4.2.2 Advancements in Molecular Biology, Development of Drugs, and Diagnostic Technology

- 4.3 Market Restraints

- 4.3.1 High Costs Associated with Diagnosis and Treatments

- 4.3.2 Stringent Regularity Guidelines

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 By Treatment

- 5.1.1.1 Targeted Therapies

- 5.1.1.2 Chemotherapy

- 5.1.1.3 Surgery

- 5.1.1.4 Other Treatments

- 5.1.2 By Diagnostics

- 5.1.2.1 Imaging

- 5.1.2.2 Biopsy

- 5.1.2.3 Endoscopic Ultrasound

- 5.1.2.4 Other Diagnostics

- 5.1.1 By Treatment

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Myriad Genetics Inc.

- 6.1.2 Pfizer Inc.

- 6.1.3 Novartis AG

- 6.1.4 Bristol-Myers Squibb Company

- 6.1.5 AstraZeneca PLC

- 6.1.6 Amgen Inc.

- 6.1.7 Viatris Inc.

- 6.1.8 Boston Scientific Corporation

- 6.1.9 FUJIFILM Holdings Corporation

- 6.1.10 Canon Inc. (canon Medical Systems Corporation)

- 6.1.11 Rafael Holdings Inc (rafael Pharmaceuticals)

- 6.1.12 Immunovia AB

- 6.1.13 Apexigen Inc.

- 6.1.14 Merck KGaA

- 6.1.15 F Hoffmann-La Roche AG