|

市場調査レポート

商品コード

1694036

北米のゲーミングハードウェアとアクセサリ:市場シェア分析、産業動向、成長予測(2025~2030年)North America Gaming Hardware And Accessories - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のゲーミングハードウェアとアクセサリ:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 154 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

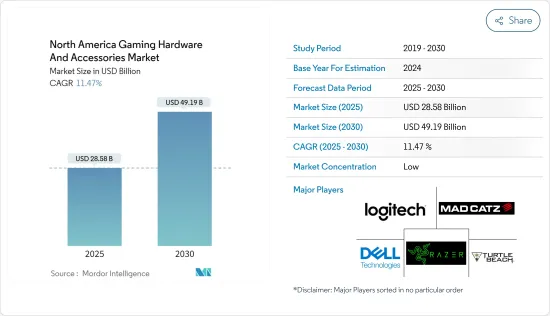

北米のゲーミングハードウェアとアクセサリ市場規模は2025年に285億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.47%で、2030年には491億9,000万米ドルに達すると予測されます。

ゲームの成長は、ゲーマーが次のレベルのパフォーマンスに到達することを可能にするゲームアクセサリの需要を大幅に強化しました。競合ゲームは、スピード、精度、信頼性を要求します。他のスポーツと同様に、ゲーミングマウス、キーボード、コントローラなどの高性能な専用ギアは、デジタルアスリートが最高のパフォーマンスを発揮することを可能にします。

主要ハイライト

- ESA 2023の調査によると、2億1,260万人以上のアメリカ人が週に1時間以上ビデオゲームをプレイしています。米国では、75%がすべてのプラットフォームで週4時間以上ゲームをプレイしており、ビデオゲーム参入企業の58%が複数のプラットフォームを利用しています。利用デバイス別では、モバイルが64%、コンソールが54%、PC/ラップトップが45%、ラップトップが24%、VRヘッドセットが10%。

- eスポーツは、現在の市場シナリオにおいてかなりの市場需要を目の当たりにしており、ゲーム産業を牽引しています。eスポーツ市場全体は今後数年間で成長すると予想されます。eスポーツの観客と参入企業の大半はミレニアル世代です。そのため、eスポーツのパブリッシャーは、ゲームプレイ体験をパーソナライズし、コンソール、PC、モバイルなどのさまざまなプラットフォームでゲームを提供することで、これらの顧客を対象にしています。

- 例えば、最近の例では、カウンターストライクは約160億米ドルを稼ぎ出し、当時の主要なコンソールゲームやPCゲームよりも年間売上が多くなりました。このように、エコシステムに新たなゲーマーが加わることで、eスポーツの観客がさらに増え、長期的に収益が増加することが予想されます。

- コンソールゲームの使用方法は年々変化しており、人気の需要はマルチプラットフォームデバイスに集中しています。そのため、現在ではゲーム機はゲームだけに使われているわけではありません。しかし、そのような機器を所有している回答者の25%は、1週間のゲーム機使用時間をオンラインとオフラインゲームのプレイに充てています。ゲームといえば、PS4とWii Uのゲーマーはオフラインゲームをプレイすることが多く、Xbox Oneの所有者はオンラインゲームをプレイすることが多いです。

- VGChartz Networkによると、プレイステーション5は南北アメリカ(アメリカ、カナダ、ラテンアメリカ)で最も売れたゲーム機であり、2024年3月には63万302台が販売されました。プレイステーション5は、南北アメリカで推定2,365万台の生涯販売台数を記録しました。ニンテンドースイッチは推定27万3,769台を販売し、生涯販売台数は5,317万台となりました。XboxシリーズX|Sは23万6,462台を販売し3位となり、生涯販売台数は1,701万台となりました。

- 世界の半導体不足により、スマートフォンからゲーム機、ハイテクに依存した自動車に至るまで、日常的に使用される機器の供給が根底から覆されています。このため、大手ゲーム会社の今年の計画は遅れており、彼らが市場に投入したデバイスの結果、そのアクセサリの需要が減少しています。

北米のゲーミングハードウェアとアクセサリ市場動向

ゲーミングPCが主要市場シェアを占める

ゲーミングPCは、ビデオゲームを高設定、高フレームレート、高解像度でプレイするために最適化された高性能コンピュータです。強力なプロセッサ(Intel Core i7/i9やAMD Ryzenなど)、専用グラフィックスカード(NVIDIA GeForce RTXやAMD Radeonなど)、スムーズなマルチタスクとゲームプレイのための十分なRAMを搭載しています。

これらのPCは、カスタマイズ可能なRGB照明、先進的冷却システム、最適なエアフローを実現する高品質ケースを備えていることが多いです。ゲーミングPCは、ユーザー固有の構成を可能にするため、事前構築またはカスタム構築することができます。ゲーミングPCは、高速でスムーズ、かつ没入感のあるゲームプレイを求めるゲーマー向けに設計されており、多くの場合、ゲーム体験を向上させるために高リフレッシュレートのモニターや先進的周辺機器を備えています。

北米におけるゲーミングPCの成長は、ゲーム文化やeスポーツの人気の高まりによって、強力なゲーミングシステムに対する高い需要が生まれたことが原動力となっています。高性能プロセッサやグラフィックスカードなどの技術的進歩により、ゲーム体験が向上し、この地域のゲーマーを魅了しています。ゲーミングPCで利用可能なカスタマイズやパーソナライズのオプションも、その魅力に貢献しています。オンラインゲームコミュニティの成長や、ゲームを通じた社会的交流も、この動向を後押ししています。

エントリーレベルのゲーミングPCの価格は、ユーザーが選択するコンポーネントによって異なりますが、一般的には300米ドルから800米ドルの間と予想されます。ゲーミングPCのセットアップ費用の決定は、ゲームのニーズ、予算、エネルギーの考慮事項に密接に関係しています。良いセットアップは、一般的にUSD 1,000からUSD 4,000の範囲ですが、予算に制約がある人のために、より安価なオプションがあります。ほとんどのゲーマーは、1,000~2,500米ドルの予算で快適な中間点を見つけています。

同市場では、主要参入企業によるさまざまな戦略的製品の発表や投資が行われています。

例えば、2024年1月、プレミアムノートパソコンブランドであるMSIは、最新のAI搭載ノートパソコンと、Intel第14世代HXシリーズプロセッサと産業最強を目指す最大のベイパーチャンバーサーマルモジュールを搭載した18インチノートパソコンシリーズを発売しました。MSIのAI搭載ノートパソコンの最新ラインは、NPU(Neural Processing Unit)、内蔵IntelCore Ultraプロセッサ、豪華な外観を備え、AI技術を活用した極限のパフォーマンスと革新的な技術を記載しています。

また、2024年4月、HPは最新のOmen 17でプレミアムゲーミングノートパソコンのラインナップを発表しました。AIを強化した最新のAMD Ryzen 8,000シリーズモバイルチップを搭載し、Microsoftの最新AIアシスタント専用のCopilotキーを搭載した初のOmen製品です。さらに、このノートパソコンは、内蔵ウェブカメラとマイクを強化してビデオ通話体験を向上させるなど、AIを強化したミーティング機能を記載しています。

Game Developers Conferenceによると、ゲームは急速に変化しており、ゲーム開発者は常に最新の動向に対応する必要があります。2023年には、北米で回答したゲーム開発者の64%が、ゲーム開発プラットフォームとしてPCに最も関心があると答えています。米国とカナダでは、このような開発と競合ゲームへの注目が高まっており、市場全体の成長機会を大きく後押ししています。

米国が大きな成長を遂げる見込み

米国におけるゲーミングアクセサリの成長は、参入企業層の拡大を伴うゲーム産業の拡大が牽引しており、ゲーム体験を向上させるアクセサリの需要を促進しています。eスポーツや競合ゲームの台頭は専用ギアのニーズを生み出し、コンテンツ制作やTwitchのようなストリーミングプラットフォームは高品質のマイク、カメラ、照明の需要を促進しています。リモートワークや学習へのシフトは、人間工学に基づいたゲーミングチェアやヘッドセットへの関心を高めています。

Entertainment Software Associationによると、フロリダ州、ノースカロライナ州、ニューヨーク州、テキサス州、カリフォルニア州、ワシントン州などの州はゲーム需要が高く、ゲーム産業からの収益率が高いです。

米国の成人の間では、アーケードゲームやパズルゲームなどのカジュアルジャンルが引き続き最もプレイされています。娯楽(テレビ、音楽、ゲームなど)に費やす時間のうち、ビデオゲームは全体の4分の1を占め、高く評価されています。半数近くが、「ビデオゲームは、使ったお金に対する娯楽価値が最も高い」と回答。成人ゲーム参入企業の約58%が複数のプラットフォームを利用しており、モバイル、コンソール、PCを組み合わせてプレイしています。このようなプラットフォームの利用の増加は、ゲーミングマウス、ヘッドセット、キーボード、コントローラを含むより良いゲームアクセサリを要求し、国内での市場の成長機会を大きく促進しています。

全体として、米国ではコンソールゲームがPCゲームよりもやや人気があるが、これはその他と比べると異常なことです。これは、米国ではPCの方が高価だと思われているためです。そのため、PC用アクセサリよりもコンソール用ヘッドセットやコントローラの需要が高まっています。PlayStation 5は2023年10月までの36ヶ月間に国内で1,610万台、Xbox Series X|Sは1,188万台売れており、米国におけるゲーム機の需要が強いことを示しています。

Consumer Technology Associationsによると、米国では2023年12月の次世代ゲーム機の世帯保有率は26%、購入意向率は20%となっています。

市場参入企業は、複数の産業別に注力することで、消費者基盤を強化するために厳格な行動をとっています。また、世界の事業展開とサービス提供の拡大にも注力しています。例えば、HyperXは2024年4月、ゲーム周辺機器産業においてゲーム体験を向上させるために調整された先進的イノベーションを発表しました。

HyperX Alloy Riseゲーミングキーボードシリーズの発売により、同ブランドはゲーマーの進化する要求に応える高性能ソリューションを提供するというコミットメントを再確認しました。クラフツマンシップと先進的技術を特徴とするHyperX Alloy Rise Gaming Keyboardとそのコンパクト版であるHyperX Alloy Rise 75 Gaming Keyboardは、卓越したゲーミングの新たな基準を打ち立てる態勢を整えています。

2024年4月、ロジクールは最新のゲーミング周辺機器であるロジクールG Pro X 60 LIGHTSPEEDを発表し、プロゲーマーや重度のホビー参入企業を引きつける努力を続けています。ロジクールG Pro X 60 LIGHTSPEEDは、コンパクトながら高性能でカスタマイズ性に優れたワイヤレスeスポーツキーボードです。洗練されたハードウェアと特別に開発されたサポートソフトウェアにより、その造りと多くの機能により、ロジクールはその最新デバイスを「プロ仕様」であるとアピールしています。

北米のゲーミングハードウェアとアクセサリ産業概要

北米のゲーミングハードウェアとアクセサリ市場は、世界参入企業と中小企業の両方が存在するため、非常にセグメント化されています。同市場の主要企業には、Alienware(Dell Technologies Inc.)、Logitech International SA、Razer Inc.、Mad Catz Global Limited、Turtle Beach Corporationなどがあります。市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2024年4月-ゲーマー向けの世界のライフスタイルブランドであるRazerは、eスポーツエンジニアリングの頂点であるRazer Viper V3 Proを発表しました。このマウスは、最近のVALORANT Champions Tour Masters Madridのチャンピオン兼MVPであるZekkenを含むeスポーツのトッププロとの緊密な協力によって作られており、最も要求の厳しい競合環境で実戦テストが行われています。

- 2024年3月-タートルビーチは、ゲーミングアクセサリの大手プロバイダであるPDPを、PDPの企業価値1億1,800万米ドルで買収する正式契約の締結を発表しました(以下、「本取引」)。PDPは、コントローラ、ヘッドセット、電源ケース、その他のアクセサリを含む、アフターマーケットのビデオゲームアクセサリを設計・販売する非上場のサードパーティゲームアクセサリリーダーです。本取引により、タートルビーチ社の規模が大幅に拡大し、PDPのゲーミングコントローラ部門がタートルビーチ社に加わることで、さらなる規模の拡大と将来の開発機会の創出が期待されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 市場推定・予測

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 産業バリューチェーン分析

第5章 市場力学

- 市場の促進要因

- eスポーツゲーミングの増加がゲーミングアクセサリ機器の需要を促進する

- 新しいゲーム機とコンピュータGPUユニットの発売によるアクセサリ需要の増加

- 市場抑制要因

- シリコンチップの生産量の変動がゲーミングアクセサリの需要不足につながる

- 北米進出の主要検討事項

- 主要動向の評価(定性分析)

第6章 市場セグメンテーション

- 製品タイプ別

- ゲーミングPC

- ゲーミングコンソール

- ゲーミングヘッドセット

- PC用ヘッドセット

- コンソール用ヘッドセット

- ゲーミングキーボード

- ゲーミングマウス

- ゲーミングコントローラ/ジョイスティック/ゲームパッド

- 仮想現実デバイス

- その他ゲームアクセサリ

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Alienware(Dell Technologies Inc.)

- Logitech International SA

- Razer Inc.

- Mad Catz Global Limited

- Turtle Beach Corporation

- Corsair Gaming Inc.

- Cooler Master Co. Ltd

- Sennheiser Electronic GmbH & Co. KG(Sonova Holding AG)

- HyperX(HP Inc.)

- Anker Innovations Technology Co. Ltd

- Redragon(Eastern Times Technology Co. Ltd)

- Nintendo Co. Ltd

- Sony Group Corporation

- Steelseries(GN Store Nord A/S)

- Nvidia Corporation

- 市場ポジショニング分析

第8章 投資分析

第9章 市場の将来

The North America Gaming Hardware And Accessories Market size is estimated at USD 28.58 billion in 2025, and is expected to reach USD 49.19 billion by 2030, at a CAGR of 11.47% during the forecast period (2025-2030).

The growth in gaming significantly enhanced the demand for gaming accessories that enable gamers to reach the next level of performance. Competitive gaming requires speed, precision, and reliability. As in other sports, specialized high-performance gear such as gaming mice, keyboards, and controllers allow digital athletes to perform at their best.

Key Highlights

- As per an ESA 2023 study, more than 212.6 million Americans played video games at least one hour per week. In the United States, 75% played at least 4 hours of games a week across all platforms; 58% of video game players used multiple platforms. In terms of device usage, 64% of usage was from mobile, 54% from console, 45% from PC/laptop, 24% from laptop, and 10% from VR headset.

- E-sports are witnessing substantial market demand in the current market scenario, driving the gaming industry. The entire e-sports market is expected to grow over the coming years. Most of the audience and players of e-sports are millennials. Thus, e-sports publishers target these customers by personalizing the gameplay experience and offering the game on different platforms, such as consoles, PCs, and mobiles.

- For instance, in the recent past, Counter-Strike generated nearly USD 16 billion, which was more annual revenue than any major console or PC games at that time. Thus, with new gamers in the ecosystem, more e-sports audiences are expected to be attracted, generating more revenue over time.

- The usage of console games has changed throughout the years, with popular demand focused on multiplatform devices. So, nowadays, gaming consoles are not solely used for gaming. However, 25 % of the respondents who own such devices devote their weekly console time to playing online and offline games. When it comes to gaming, PS4 and Wii U console gamers play offline games more often, while Xbox One owners are more likely to play online games.

- According to VGChartz Network, the PlayStation 5 was the best-selling console in the Americas (USA, Canada, & Latin America), with 630,302 units sold in March 2024. The PlayStation 5 has now sold an estimated 23.65 million units lifetime in the Americas. The Nintendo Switch was the second best-selling console, with an estimated 273,769 units sold, bringing lifetime sales to 53.17 million. The Xbox Series X|S came in third place with 236,462 units sold, bringing its lifetime sales to 17.01 million.

- A global semiconductor shortage has upended the supply of everyday devices, from smartphones to gaming consoles to tech-dependent cars. This has delayed plans for the big gaming companies in the year, and their launch of devices into the market has subsequently provided a decrease in demand for their consequent accessories.

North America Gaming Hardware And Accessories Market Trends

Gaming PCs to Hold Major Market Share

Gaming PCs are high-performance computers optimized for playing video games at high settings, frame rates, and resolutions. They feature powerful processors (like Intel Core i7/i9 or AMD Ryzen), dedicated graphics cards (such as NVIDIA GeForce RTX or AMD Radeon), and ample RAM for smooth multitasking and gaming.

These PCs often have customizable RGB lighting, advanced cooling systems, and high-quality cases for optimal airflow. Gaming PCs can be pre-built or custom-built, allowing for user-specific configurations. They are designed for gamers who demand fast, smooth, and immersive gameplay, often featuring high refresh rate monitors and advanced peripherals for enhanced gaming experiences.

The growth of gaming PCs in North America is driven by the rising popularity of gaming culture and esports, which has created a high demand for powerful gaming systems. Technological advancements, such as high-performance processors and graphics cards, have improved gaming experiences, attracting more gamers within the region. The customization and personalization options available with gaming PCs also contribute to their appeal. The growth of online gaming communities and social interaction through gaming also fuels this trend.

The price of an entry-level gaming PC can vary depending on the components the user chooses, but generally, one can expect to spend between USD 300 and USD 800. Determining the gaming PC setup cost relates closely to the gaming needs, budget, and energy considerations. A good setup typically ranges from USD 1,000 to USD 4,000, though less expensive options exist for those with budget constraints. Most gamers find a comfortable middle ground with a budget spanning between USD 1,000 and USD 2,500.

The market is witnessing various strategic product launches and investments by key players as part of their strategy to improve business and their presence to reach customers and meet their requirements for various applications.

For instance, in January 2024, MSI, a premium laptop brand, launched the latest AI-powered laptops and a series of 18" laptops featuring Intel 14th Gen HX-series processors and the largest vapor chamber thermal modules, aiming to be the most powerful in the industry. MSI's latest line of AI-powered laptops come equipped with NPU(Neural Processing Unit), a built-in Intel Core Ultra processor, and luxurious aesthetics that deliver extreme performance and innovative technology capitalizing on AI technology.

Also, in April 2024, HP introduced its lineup of premium gaming laptops with the latest Omen 17. Featuring the latest AI-enhanced AMD Ryzen 8000-series mobile chips, it is the first Omen product to come with a dedicated Copilot key for Microsoft's latest AI assistant. Additionally, the laptop provides AI-enhanced meeting features like enhancing the built-in webcam and microphone for an improved video calling experience.

According to the Game Developers Conference, gaming is rapidly changing, and game developers must adapt to continually keep up with the latest trends. In 2023, 64 percent of responding game developers in North America said they were most interested in PCs as a game development platform. The rise in such developments and an increased focus on competitive gaming among people in the United States and Canada is driving the overall market's growth opportunities significantly.

United States Expected to Witness Significant Growth

The growth of gaming accessories in the United States is driven by the expanding gaming industry, with a growing player base, which fuels demand for accessories that enhance gaming experiences. The rise of esports and competitive gaming creates a need for specialized gear, while content creation and streaming platforms like Twitch drive demand for high-quality microphones, cameras, and lighting. The shift to remote work and learning has raised interest in ergonomic gaming chairs and headsets.

According to the Entertainment Software Association, states like Florida, North Carolina, New York, Texas, California, and Washington possess a greater demand for gaming, yielding a higher rate of revenue from the gaming industry.

Casual genres, including arcade and puzzle games, continue to be the most played among US adults. Of players' total time spent on entertainment (TV, music, video games, etc.), video games accounted for a quarter of their overall time and are highly valued. Nearly half the players reported that video games deliver the most entertainment value for money spent. About 58% of adult video game players utilize multiple platforms to play and use a combination of mobile, consoles, and PCs. The rise in such usage of platforms demands better gaming accessories that include gaming mice, headsets, keyboards, and controllers, driving the market's growth opportunities significantly within the country.

Overall, in the United States, console gaming is somewhat more popular than PC gaming, which is an anomaly compared to the rest of the world. This is because people in the United States believe that PCs cost more. This drives the demand for console headsets and controllers more than PC accessories. The PlayStation 5 sold 16.10 million units in the country in 36 months till October 2023, while the Xbox Series X|S sold 11.88 million units, indicating a strong demand for gaming consoles in the United States.

According to Consumer Technology Associations, In the United States, in December 2023, NextGen gaming console ownership and purchase intentions among households were 26 and 20 percent, respectively.

The market players are taking rigorous action to enhance their consumer base by focusing on multiple industry verticals. They are also focusing on increasing their global footprint and service offerings. For instance, in April 2024, HyperX launched advanced innovations tailored to elevate the gaming experience in the gaming peripherals industry.

With the launch of the HyperX Alloy Rise Gaming Keyboard series, the brand reaffirmed its commitment to providing high-performance solutions catering to gamers' evolving demands. Featuring craftsmanship and advanced technology, the HyperX Alloy Rise Gaming Keyboard and its compact counterpart, the HyperX Alloy Rise 75 Gaming Keyboard, are poised to set new standards in gaming excellence.

In April 2024, Logitech continued its push to attract pro gamers and severe hobbyists by announcing its latest gaming peripheral, the Logitech G Pro X 60 LIGHTSPEED. It is mainly a compact but capable and highly customizable wireless esports keyboard. Due to its build and many features, Logitech is touting its latest device as being "professional-grade," with refined hardware and specially developed supporting software adding credence to this.

North America Gaming Hardware And Accessories Industry Overview

The North America gaming hardware and accessories market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Alienware (Dell Technologies Inc.), Logitech International SA, Razer Inc., Mad Catz Global Limited, and Turtle Beach Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- April 2024 - Razer, a global lifestyle brand for gamers, launched the apex of e-sports engineering, the Razer Viper V3 Pro, which is crafted in close collaboration with top esports pros, including Zekken, Champion and MVP of the recent VALORANT Champions Tour Masters Madrid; this mouse has been battle-tested in the most demanding competitive environments.

- March 2024 - Turtle Beach announced the execution of definitive agreements to acquire PDP, a significant gaming accessories provider, at an enterprise value for PDP of USD 118 million (the "Transaction"). PDP is a privately held third-party gaming accessories leader that designs and distributes aftermarket video game accessories, including controllers, headsets, power cases, and other accessories. The transaction substantially grows the size of Turtle Beach, bringing PDP's gaming controller category to Turtle Beach, which would provide additional scale and create future development opportunities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Size Estimates and Forecasts

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in E-sports Gaming to Fuel the Demand for Gaming Accessory Equipment

- 5.1.2 New Console and Computer GPU Unit Launch to Present an Increase in the Demand for Accessories

- 5.2 Market Restraints

- 5.2.1 Fluctuation in the Production of Silicon Chips is Leading to a Shortage in the Demand for Gaming Accessories

- 5.3 Key Considerations to Enter North America

- 5.4 Assessment of Key Trends (Qualitative Analysis)

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Gaming PCs

- 6.1.2 Gaming Consoles

- 6.1.3 Gaming Headsets

- 6.1.3.1 PC Headsets

- 6.1.3.2 Console Headsets

- 6.1.4 Gaming Keyboards

- 6.1.5 Gaming Mice

- 6.1.6 Gaming Controllers/Joysticks/Gamepads

- 6.1.7 Virtual Reality Devices

- 6.1.8 Other Gaming Accessories

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Alienware (Dell Technologies Inc.)

- 7.1.2 Logitech International SA

- 7.1.3 Razer Inc.

- 7.1.4 Mad Catz Global Limited

- 7.1.5 Turtle Beach Corporation

- 7.1.6 Corsair Gaming Inc.

- 7.1.7 Cooler Master Co. Ltd

- 7.1.8 Sennheiser Electronic GmbH & Co. KG (Sonova Holding AG)

- 7.1.9 HyperX (HP Inc.)

- 7.1.10 Anker Innovations Technology Co. Ltd

- 7.1.11 Redragon (Eastern Times Technology Co. Ltd)

- 7.1.12 Nintendo Co. Ltd

- 7.1.13 Sony Group Corporation

- 7.1.14 Steelseries (GN Store Nord A/S)

- 7.1.15 Nvidia Corporation

- 7.2 Market Positioning Analysis