|

市場調査レポート

商品コード

1693970

サステナビリティコンサルティングサービス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Sustainability Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サステナビリティコンサルティングサービス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

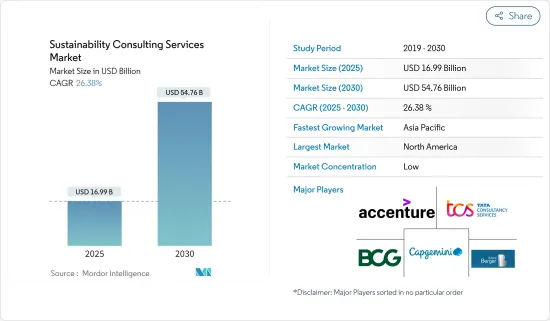

サステナビリティコンサルティングサービス市場規模は、2025年に169億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは26.38%で、2030年には547億6,000万米ドルに達すると予測されます。

サステナビリティコンサルティングサービス市場の拡大は、いくつかの要因によってもたらされています。環境・社会・ガバナンス(ESG)問題に対する意識の高まり、カーボンフットプリントの削減への関心の高まり、利害関係者からの圧力の高まり、規制遵守要件の厳格化、顧客の期待に応え評判を高めるために企業がサステイナブルプラクティスを採用する必要性などがあります。

主要ハイライト

- さらに、この成長は、サステナビリティが企業戦略や意思決定の中心を占めるという、ビジネス環境の極めて重要な変化を意味しています。企業がますます進化する気候条件に適応し、温室効果ガス排出量の削減を目指し、世界のサステナビリティベンチマークを達成しようと努力する中、世界のサステナビリティコンサルティングサービス市場は継続的に拡大する態勢を整えています。その結果、コンサルティング会社は、政府、企業、非営利団体が戦略を策定し、サステイナブルプラクティスを採用し、複雑化する気候変動を乗り切るのを支援する上で重要な役割を果たしています。

- 二酸化炭素排出量削減への関心の高まりと、企業のネットゼロ目標を達成する必要性の高まりが、サステナビリティコンサルティングサービスへの需要を後押ししています。世界中の企業が温室効果ガス排出量「ネットゼロ」の達成に取り組む姿勢を強めており、気候変動対策への取り組みと歩調を合わせています。このことは、ネットゼロ目標を効率的に達成するためのサステナビリティコンサルティングサービスに対する企業の需要を積極的に後押ししています。

- 世界各国は、気候変動と闘うための国家目標を設定し、サステナビリティコンサルティングサービスの需要を大幅に押し上げています。各国政府はネットゼロ排出を達成するための対策を実施しており、ネットゼロ目標に向けた戦略の策定や各国政府を指導する上で極めて重要な役割を果たすサステナビリティコンサルティングサービスへの需要に拍車をかけています。

- 現実とのギャップが大きく、導入レベルが低いことが、世界のサステナビリティコンサルティングサービス市場の成長を妨げる大きな要因となっています。環境コンサルティング会社は、様々な国でサステナビリティイニシアティブの採用が停滞しているため、サステナビリティの推進という課題に直面しています。組織は、財政的、技術的、人的資源に限りがあるため、気候変動への適応のような複雑で論争の的となる問題への対処が難しく、苦戦を強いられることが多いです。その結果、民間企業でも公的機関でも、サステナビリティに関するコンサルティングサービスの利用が減少しています。

- 現在進行中のロシア・ウクライナ戦争は、世界のサステナビリティコンサルティングサービス市場に大きな影響を与えています。ロシア・ウクライナ戦争は世界の経済成長と労働市場に大きな影響を与え、インフレ圧力を強め、サプライチェーンに大きな混乱をもたらしました。戦争は、特にサステナビリティプロジェクトに不可欠な材料や商品のサプライチェーンを混乱させています。特に、電気自動車用バッテリーに不可欠なニッケルとパラジウムは、サプライチェーンで大きな課題に直面しています。

サステナビリティコンサルティングサービス市場の動向

気候変動コンサルティングサービスが主要市場シェアを占める

- 気候変動コンサルティングサービスには、カーボンフットプリントと緩和分析、代替エネルギー開発とエネルギー効率化、気候適応と戦略、緊急事態管理、カーボンオフセット/ネットゼロサービス、環境規制遵守サービス、廃棄物管理と循環型社会、その他のサービスが含まれます。

- 気候変動コンサルタントサービスに対する需要の高まりは、環境負荷の低減、カーボンフットプリントの削減、気候変動への適応、リスク管理、法規制遵守の徹底、サステイナブル実践に関する専門家の助言を求める企業や組織によるものです。

- 世界中で、企業は気候変動の影響に取り組んでいます。その結果、物理的リスク、過渡的リスク、賠償責任によるリスクなど、気候変動に関連するリスクを管理することは、競合を維持し、新たなネットゼロのパラダイムで成功を収めようとする企業にとって最重要課題となっています。このような状況の変化により、気候変動を中心とした様々なコンサルティングサービスへの需要が高まっており、複雑な状況を乗り切るための支援を行っています。

- The Emissions Database for Global Atmospheric Research/Joint Research Centre(EDGAR/JRC)」が発表した世界各国の温室効果ガス(GHG)排出量に関する2024年版報告書によると、世界の温室効果ガス(GHG)排出量は2023年に過去最高を記録し、二酸化炭素換算で529億6,000万トン(Gt CO2e)に達し、前年比で2%増加しました。

- さらに、気候変動問題に率先して立ち向かう企業は、評判を高め、サステナビリティのリーダーとしての地位を確立します。このような積極的な姿勢は、顧客、優秀な人材、価値あるパートナーシップを引き寄せ、大きな競争上の優位性につながります。

- サステナビリティコンサルティング市場のベンダーは、気候変動コンサルティング会社を買収しています。この戦略の狙いは、提供するサービスの幅を広げ、市場での存在感を高め、気候変動コンサルティングサービスへの需要の高まりに対応することにあります。

- 例えば、2024年6月、サステナビリティアドバイザリー会社であるERMは、オーストラリアを拠点とする気候変動リスクとエネルギー転換のコンサルタント会社であるEnergeticsを買収することで合意したと発表しました。この動きは、アジア太平洋におけるERMの成長を強化することを目的としています。エナジェティクスは、気候変動リスクや再生可能エネルギー移行に関する洞察、ネットゼロ目標に向けた企業の指導、再生可能エネルギー取引のための電力購入契約(PPA)のモニタリングなど、気候変動に強い戦略の立案など、オーダーメイドのサービスを専門としています。ERMは、今回の買収により、オーストラリアとアジア太平洋全域において、戦略的アドバイスと実践的実施の両方をクライアントに提供する能力が強化されるとしています。

- 全体として、気候変動コンサルティングサービスは、世界のサステナビリティコンサルティング市場で最大のシェアを占めると予想されています。企業や組織が気候変動の影響をより強く認識するようになり、二酸化炭素排出量を削減するよう規制上の圧力に直面し、気候変動対策への取り組みが世界的に急増する中、気候変動コンサルティングサービスへの需要が高まっています。この需要は、積極的な気候変動リスク管理を通じて競合を高めようとする企業によって、さらに促進されています。

大きな成長を遂げるアジア太平洋

- 多様な規制の枠組みと急速な産業化が、アジア太平洋のサステナビリティコンサルティング市場を形成しています。特に製造業、石油・ガス、建設業といったエネルギー多消費セクタにおいて、環境基準に関する政府規制が強化されたことが、同地域の拡大に大きく寄与しています。これを受けて、アジア太平洋のサステナビリティコンサルティング会社は、企業がコンプライアンス目標を達成し、グリーン戦略を採用し、サステイナブルプラクティスを業務に取り入れるのを支援しています。

- 中国やインドのような国々は、急速な都市化と工業化が進み、環境悪化に直面しています。そのため、各国政府はより厳しい環境基準を設けるようになりました。このような状況において、サステナビリティコンサルティング会社は極めて重要な役割を担っており、国内と国際的なサステナビリティベンチマークを確実に遵守しながら、成長と環境スチュワードシップを調和させるビジネスモデルを構築するよう企業を指導しています。

- 例えば、都市化の進展と、2030年までに炭素排出量のピークを、2060年までに完全なカーボンニュートラルを目指す「デュアル・カーボン」国家目標に後押しされ、中国は建築・建設セクタのグリーン化への取り組みを強化しています。政府のデータによると、2020年には中国の新都市建設プロジェクトの77%がグリーンビルディングに分類されました。

- 2023年10月、上海市は市内に進出する外資系企業のESG能力を強化することを目的とした3カ年計画を発表しました。この計画では、企業が研究開発投資を拡大し、デジタル、グリーン、低炭素技術を導入することで、イノベーションと競合を強化し、サステナビリティコンサルティングソリューションの需要を高めることを奨励しています。

- アジア太平洋では、世界の投資家を呼び込み、ブランド評価を高めるために、ESG原則を採用する企業が増えています。サステナビリティコンサルティング会社は、強化すべきセグメントを特定し、ESG戦略を実行し、国際的なサステナビリティ報告基準に備えることで、こうした企業を支援しています。

サステナビリティコンサルティングサービス市場概要

サステナビリティコンサルティングサービス市場は、既存参入企業と新興参入企業の両方が多様に混在しているのが特徴です。Accenture(Accenture PLC)、ボストンコンサルティング・グループ(Boston Consulting Group, Inc)、タタコンサルタンシー・サービシズ(Tata Consultancy Services Limited)、キャップジェミニ(Capgemini SE)、ローランド・ベルガー(Roland Berger GmbH)などが主要参入企業です。

同市場における適度な撤退障壁は、新規参入企業にインセンティブを与える一方で、既存企業は低収益期に撤退することを可能にしています。産業をリードする企業は、顧客を引き付けるために統合ソリューションにますます力を入れるようになっています。これとは対照的に、小規模で新規参入する企業は、大手に対抗するために費用対効果の高い戦略を採用し、競争を激化させると予想されます。

さらに最近、合弁事業や買収が目立って増えているのは、世界のビジネス界がサステナビリティを重視していることを裏付けています。その結果、世界のサステナビリティ市場における競争企業間の敵対関係は依然として顕著です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場のマクロ経済要因の評価

第5章 市場力学

- 市場の促進要因

- カーボンフットプリントの削減とネットゼロ目標の達成への注目の高まり

- 気候変動と闘うための世界各国の国家目標

- 市場課題

- 現実的なシナリオに大きな隔たりがある低水準の普及率

第6章 市場セグメンテーション

- サービスタイプ別

- 気候変動コンサルティングサービス

- グリーンビルディングコンサルティングサービス

- ESGコンサルティングサービス

- その他サステナビリティコンサルティングサービス

- エンドユーザー別

- 建設・不動産

- エネルギー電力

- 公共部門

- その他

- 地域別

- 北米

- 欧州

- 英国

- ドイツ

- ベネルクス

- スペイン

- フランス

- 北欧

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Accenture PLC

- The Boston Consulting Group, Inc.

- Tata Consultancy Services Limited

- Capgemini SE

- Roland Berger GmbH

- Bain & Company, Inc.

- KPMG International Limited

- Ernst & Young Global Limited

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers LLP

- McKinsey & Company

- Kearney

- Godrej & Boyce Mfg. Co. Ltd(Godrej Industries Limited)

- RPS Group(Tetra Tech Inc.)

- SEA Energy

第8章 投資分析

第9章 市場の将来展望

The Sustainability Consulting Services Market size is estimated at USD 16.99 billion in 2025, and is expected to reach USD 54.76 billion by 2030, at a CAGR of 26.38% during the forecast period (2025-2030).

The expansion of the sustainability consulting services market is driven by several factors. These include increased awareness of environmental, social, and governance (ESG) issues, a stronger focus on reducing carbon footprints, heightened stakeholder pressures, more stringent regulatory compliance requirements, and the necessity for businesses to adopt sustainable practices to meet customer expectations and enhance their reputation.

Key Highlights

- Moreover, this growth signifies a pivotal transformation in the business landscape, with sustainability taking center stage in corporate strategies and decision-making. As companies increasingly adapt to evolving climate conditions, aim to reduce greenhouse gas emissions, and strive to meet global sustainability benchmarks, the global sustainability consulting services market is poised for continued expansion. Consequently, consulting firms play a vital role in assisting governments, businesses, and nonprofit entities in creating strategies, adopting sustainable practices, and navigating the increasing complexities of the changing climate.

- The rising focus on carbon footprint reduction and the growing need to fulfill businesses' net zero targets drive the demand for sustainability consulting services. Companies worldwide increasingly commit to achieving "net zero" greenhouse gas emissions, aligning with initiatives to combat climate change. This positively drives businesses' demand for sustainability consulting services to achieve their net-zero targets efficiently.

- Countries worldwide are setting national goals to combat climate change, significantly boosting the demand for sustainability consulting services. Governments are implementing measures to achieve net-zero emissions, fueling the demand for sustainability consulting services, which are pivotal in guiding governments and formulating strategies toward their net-zero targets.

- Lower levels of adoption, with large gaps in reality, are a major factor hindering the growth of the global sustainability consulting services market. Environmental consulting firms face challenges in promoting sustainability due to the sluggish adoption of sustainability initiatives across various nations. Organizations frequently struggle with limited financial, technical, and human resources, making addressing intricate and contentious issues such as climate change adaptation difficult. Consequently, this dynamic results in diminished uptake of sustainability consulting services, both in the private sector and among public sector enterprises.

- The ongoing Russia-Ukraine War significantly impacts the global sustainability consulting services market. It has profoundly affected global economic growth and labor markets, intensifying inflationary pressures and causing significant supply chain disruptions. The war has disrupted supply chains, especially for materials and goods vital to sustainability projects. Notably, nickel and palladium, essential for electric vehicle batteries, have faced significant supply chain challenges.

Sustainability Consulting Services Market Trends

Climate Change Consultancy Services Type Holds Major Market Share

- Climate change consultancy services considered under the scope include Carbon Footprint and Mitigation Analysis, Alternative Energy Development and Energy Efficiency, Climate Adaptation and Strategy, Emergency Management, Carbon Offset/Net Zero Services, Environmental Regulatory Compliance Services, Waste Management and Circularity, and Other Services.

- The increasing demand for climate change consultancy services is driven by businesses and organizations seeking expert advice on reducing environmental impact, lowering carbon footprints, adapting to climate change, managing risks, ensuring regulatory compliance, and implementing sustainable practices.

- Across the globe, businesses are grappling with the repercussions of climate change. As a result, managing climate-related risks, such as physical, transitional, or liability-based, has become paramount for firms eager to maintain their competitive edge and thrive in the emerging Net Zero paradigm. This evolving landscape has spurred a heightened demand for various consultancy services centered on climate change, aiding businesses in navigating these complexities.

- According to the 2024 report on GHG emissions from all world countries, published by 'The Emissions Database for Global Atmospheric Research/Joint Research Centre (EDGAR/JRC)'' global greenhouse gas (GHG) emissions hit a record high in 2023, reaching 52.96 billion metric tons of carbon dioxide equivalent (Gt CO2e), marking a two percent year-over-year increase.

- Moreover, companies that take the initiative in confronting climate change issues bolster their reputation and position themselves as leaders in sustainability. Such a proactive stance can translate into a significant competitive advantage, drawing in customers, top talent, and valuable partnerships.

- Vendors in the sustainability consulting market are acquiring climate change consulting firms. This strategy aims to broaden their service offerings, bolster their market presence, and cater to the rising demand for climate change consultancy services.

- For instance, in June 2024, ERM, a sustainability advisory firm, announced its agreement to acquire Energetics, a climate risk and energy transition consultancy based in Australia. This move aims to bolster ERM's growth in the Asia Pacific region. Energetics specializes in tailored services, such as crafting climate resiliency strategies, offering insights on climate risks and renewable energy transitions, guiding companies towards net-zero goals, and monitoring power purchase agreements (PPAs) for renewable energy transactions. ERM asserts that this acquisition will bolster its capacity to provide clients with both strategic advice and hands-on implementation across Australia and the broader Asia Pacific region.

- Overall, climate change consultancy services are expected to hold the largest share of the global sustainability consulting market. As businesses and organizations become more aware of climate impacts, face regulatory pressures to reduce their carbon footprints, and witness a global surge in climate action initiatives, there's a rising demand for climate change consultancy services. This demand is further fueled by businesses seeking a competitive edge through proactive climate change risk management.

Asia Pacific to Register Major Growth

- Diverse regulatory frameworks and swift industrialization shape the sustainability consulting market in the Asia-Pacific region. The region's expansion is largely fueled by heightened government regulations on environmental standards, especially in energy-intensive sectors such as manufacturing, oil and gas, and construction. In response, sustainability consulting firms in the Asia-Pacific help businesses meet compliance targets, adopt green strategies, and weave sustainable practices into their operations.

- Countries like China and India, witnessing rapid urbanization and industrialization, face environmental degradation. This has led their governments to enforce stricter environmental standards. In this context, sustainability consulting firms play a pivotal role, guiding companies to craft business models that harmonize growth with environmental stewardship, all while ensuring adherence to both national and international sustainability benchmarks.

- For instance, driven by rising urbanization and its national "Dual Carbon" targets-aiming for peak carbon emissions by 2030 and full carbon neutrality by 2060-China is intensifying its efforts to green its building and construction sector. Government data reveals that in 2020, a significant 77% of China's new urban construction projects were classified as green buildings.

- In October 2023, Shanghai unveiled a three-year initiative aimed at bolstering the ESG capabilities of foreign businesses in the city. Thereby, the plan encourages companies to ramp up Research and Development investments and embrace digital, green, and low-carbon technologies, enhancing their innovation and competitiveness, and heightening the demand for sustainability consulting solutions.

- In the Asia-Pacific region, companies are increasingly adopting ESG principles to draw in global investors and bolster their brand reputation. Sustainability consulting firms assist these businesses by pinpointing areas for enhancement, executing ESG strategies, and gearing up for international sustainability reporting standards.

Sustainability Consulting Services Market Overview

The sustainability consulting services market is characterized by a diverse mix of both established and emerging players. Some of the major players in the market are Accenture PLC, The Boston Consulting Group, Inc., Tata Consultancy Services Limited, Capgemini SE, and Roland Berger GmbH, among others.

Moderate exit barriers in the market incentivize new entrants while allowing established firms to exit during low-profit periods. Leading industry players are increasingly focusing on integrated solutions to attract customers. In contrast, smaller and newer market entrants are expected to adopt cost-benefit strategies to vie with their larger counterparts, intensifying competition.

Furthermore, a notable surge in joint ventures and acquisitions recently underscores the global business community's heightened emphasis on sustainability. As a result, competitive rivalry in the global sustainability market remains pronounced.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Focus on the Reduction of Carbon Footprint and Fulfilment of Net Zero Targets

- 5.1.2 National Goals Across the Globe to Combat Climate Change

- 5.2 Market Challenges

- 5.2.1 Lower Levels of Adoption with Large Gaps in the Realistic Scenario

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Climate Change Consultancy Services

- 6.1.2 Green Building Consultancy Services

- 6.1.3 ESG Consultancy Services

- 6.1.4 Other Sustainability Consultancy Services

- 6.2 By End User

- 6.2.1 Construction and Real Estate

- 6.2.2 Energy and Power

- 6.2.3 Public Sector

- 6.2.4 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 Benelux

- 6.3.2.4 Spain

- 6.3.2.5 France

- 6.3.2.6 Nordics

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Accenture PLC

- 7.1.2 The Boston Consulting Group, Inc.

- 7.1.3 Tata Consultancy Services Limited

- 7.1.4 Capgemini SE

- 7.1.5 Roland Berger GmbH

- 7.1.6 Bain & Company, Inc.

- 7.1.7 KPMG International Limited

- 7.1.8 Ernst & Young Global Limited

- 7.1.9 Deloitte Touche Tohmatsu Limited

- 7.1.10 PricewaterhouseCoopers LLP

- 7.1.11 McKinsey & Company

- 7.1.12 Kearney

- 7.1.13 Godrej & Boyce Mfg. Co. Ltd (Godrej Industries Limited)

- 7.1.14 RPS Group (Tetra Tech Inc.)

- 7.1.15 SEA Energy