|

市場調査レポート

商品コード

1693964

東南アジアの民間航空機MRO-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Southeast Asia Commercial Aircraft MRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 東南アジアの民間航空機MRO-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

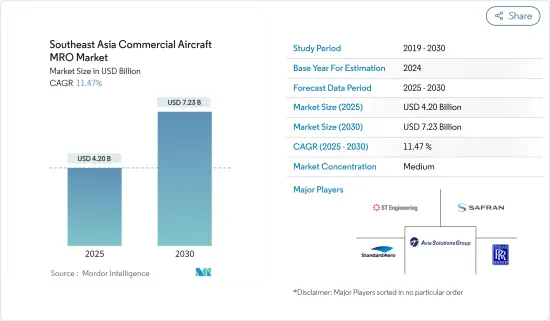

東南アジアの民間航空機MRO市場規模は2025年に42億米ドルと推定・予測され、予測期間(2025~2030年)のCAGRは11.47%で、2030年には72億3,000万米ドルに達すると予測されます。

過去数十年間、東南アジアは最先端の航空インフラで補完することで、その有利な地理的立地を最大限に活用してきました。この地域の戦略的位置と強力な現地サプライチェーンは、多くの民間航空機MRO企業にとって好ましい場所となっています。

東南アジア地域のさまざまな空港で、航空機MROサービスの提供に対応できるオンサイト施設の開発が進んでいます。付加製造、予知保全、航空機健康モニタリングシステム、複合材修理能力、人工知能、ビッグデータにおける技術的進歩は、今後数年間で大きな役割を果たすと考えられます。この地域のMRO企業の多くは、予測期間中に高い収益を上げるために、自動化による業務の合理化を選択する可能性が高いからです。

東南アジア地域における民間航空機納入数の増加と、同地域における民間航空機MRO施設への投資の増加は、予測期間中に市場を成長へと導く主要因です。一方、熟練労働者の不足と民間航空機に必要な整備を実施するためのスペースの不足は、予測期間中に市場の成長を妨げる可能性のある主要因となり得る。

東南アジアの民間航空機MRO市場動向

予測期間中はエンジンセグメントが市場を独占

エンジンMROは、MROの重要かつ高価な部分です。エンジン部品の複雑化とエンジン故障による航空機墜落の増加により、運航会社は頻繁なエンジン整備と定期点検に注力しています。エンジンは航空機の最も重要な部品の一つであり、飛行中、地上を問わず、定期的にメンテナンスする必要があります。

エンジンMROセグメントでは、OEMが市場の約半分を支配しており、残りの半分は独立系と航空会社のオーバーホール工場でほぼ二分されています。航空会社は、エンジンのメンテナンスを外注したり、新しい世代のパワープラントの完全なMROサポートプログラムを利用したりすることが多いです。例えば、2021年12月、サフラン・エアクラフトエンジンはSIAエンジニアリング・カンパニー(SIAEC)と新たに10年間のエンジンMRO契約を締結しました。この契約に基づき、シンガポール航空のMRO部門は、CFMインターナショナルのLEAP-1A(A320neoファミリー)とLEAP-1B(737 MAXファミリー)のエンジン検査サービスを、サフラン・テストセルが供給する最新のデータ収集・制御システムでアップグレードされた近代化されたエンジン検査施設を通じて提供することが求められました。

2050年までの空港技術ロードマップと題されたIATAの報告書によると、新しい民間航空機は2035年、従来のジェット燃料を動力源とするターボファンエンジンを搭載した、伝統的チューブ&ウィング構成の画期的な開発機であることに変わりはありません。2035年以降、航空機産業は、航空機の構成と推進システムに革命的な変化を確認することになると予想されます。新しい設計には、支柱で支えられた翼、混合翼体、バッテリー電気航空機などが含まれます。したがって、航空機納入の増加と旧式機体の近代化が、予測期間中のこのセグメントの成長を牽引します。

予測期間中、マレーシアが最も高い成長を示すと予測される

航空旅客輸送量の増加と国際線と国内線における航空サービスの拡大が、マレーシアの民間航空セクタの需要を牽引すると推定されます。マレーシアの2022年5月の年間累計(YTD)旅客数は1,630万人で、2021年同期比574.6%増でした。マレーシア航空、マリンドエア、エアアジアがマレーシアの主要航空会社です。これらの航空会社は航空需要の大部分に対応しています。2023年9月現在、マレーシア航空の保有する航空機は286機で、平均機齢は11.4年です。過去5年間で、約65機の航空機が新たに納入されました。

例えば、2022年9月、マレーシア航空Bhdとスピリット・エアロシステムズ社は、BoeingB737次世代(NG)航空機のメンテナンス、修理、オーバーホール(MRO)サービスを提供する覚書に調印しました。この契約に基づき、スピリット・エアロシステムズとマレーシア航空は、同航空の保有機をサポートするため、ナセルと飛行制御面の修理サービスの確立に共同で取り組みます。また、2022年4月、Honeywellは、マレーシアにおける同社のプレゼンスと同国と地域の主要利害関係者との関係をさらに強化する2つのMoUに調印しました。この協力関係は、Honeywellがアイロッド・テクノパワー(ATP)とギャラクシー・エアロスペースと個別にMOUを締結しているように、航空機の整備・修理・オーバーホール(MRO)におけるHoneywellの専門知識を様々な能力で活用することを意図したものです。このような市場の開拓は、予測期間中、マレーシアの航空機MRO市場の需要を促進すると予想されます。

東南アジアの民間航空機MRO産業概要

東南アジアの民間航空機MRO市場は半固体化した性質を持っており、少数の世界参入企業と地場企業が市場で大きなシェアを占めています。市場の主要企業には、Singapore Technologies Engineering Ltd、Rolls-Royce PLC、Safran、AVIA SOLUTIONS GROUP PLC、StandardAeroなどがあります。市場の主要参入企業は、研究開発への投資を積極的に行い、民間航空機向けの先進的なMROソリューションを導入しています。例えば、2022年2月、SIAはシンガポールに900万米ドルの航空機エンジンサービス(AES)施設を新設しました。この施設は、少なくとも年間60回のクイックタンを行うよう特注設計されており、需要の急増に対応するため、さらに50%の能力を追加しています。同様に2021年には、マレーシアのスバン空港が、マレーシア空港と同国の世界企業であるDviation Group of Companiesの協力により、東南アジア地域で初めて航空機MRO施設の開発に成功しました。さらに、この新しい施設は、整備・修理・オーバーホール(MRO)、航空機の分解、航空機材料のリサイクル、部品取引など、エンド・ツー・エンドのアフターマーケットサービスを記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 市場抑制要因

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- MROタイプ

- 機体

- エンジン

- コンポーネント

- ライン

- 航空機タイプ

- ナローボディ

- ワイドボディ

- 地域

- 東南アジア

- マレーシア

- インドネシア

- シンガポール

- タイ

- その他の東南アジア

- 東南アジア

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Singapore Technologies Engineering Ltd

- SIA Engineering Company Limited

- Singapore Aero Engine Services Limited

- StandardAero

- Garuda Indonesia(GMF AeroAsia)

- Triumph Group

- Safran

- Rolls-Royce plc

- ExecuJet MRO Services

- AVIA SOLUTIONS GROUP PLC

- Subang MRO Sdn Bhd

- Asia Digital Engineering Sdn Bhd

- Sepang Aircraft Engineering Sdn Bhd

- Asia AeroTechnic Sdn Bhd

第7章 市場機会と今後の動向

The Southeast Asia Commercial Aircraft MRO Market size is estimated at USD 4.20 billion in 2025, and is expected to reach USD 7.23 billion by 2030, at a CAGR of 11.47% during the forecast period (2025-2030).

For the past few decades, Southeast Asia has been making the most of its favorable geographic location by complementing it with state-of-the-art aviation infrastructure. The region's strategic position and the strong local supply chain have made it a preferred location for many commercial aircraft MRO companies.

There have been growing developments about onsite facilities at various airports across the Southeast Asian region, which can cater to providing aircraft MRO services. Technological advancement in additive manufacturing, predictive maintenance, aircraft health monitoring systems, composite repair capabilities, artificial intelligence, and big data will play a major role in the coming years, as most of the MRO players in the region will most likely opt to streamline their operations through automation to generate higher revenue during the forecast period.

The increasing number of commercial aircraft deliveries in the Southeast Asian region, coupled with the growing investments in commercial aircraft MRO facilities in the region, will be the main factors that will lead the market toward growth during the forecast period. On the other hand, the shortage of skilled labour and lack of availability of space for carrying out the required maintenance on commercial aircraft can be the key factors that may hamper the market's growth during the forecast period.

Southeast Asia Commercial Aircraft MRO Market Trends

Engine Segment Dominates the Market During the Forecast Period

Engine MRO is a vital and expensive part of an MRO. The increasing complexity of engine parts and the increased number of aircraft crashes due to engine failures have made operators focus on frequent engine maintenance and periodic checks. An engine is one of the most critical components of the aircraft, which must be maintained regularly, irrespective of whether it is flying or on the ground.

In the engine MRO sector, OEMs control approximately half of the market, with the other half roughly split between independent and airline overhaul shops. Operators frequently outsource engine maintenance and use complete MRO-support programs for new powerplant generations. For instance, in December 2021, Safran Aircraft Engines signed a new 10-year engine MRO contract with SIA Engineering Company (SIAEC). Under the agreement, Singapore Airlines' MRO division was required to provide engine testing services for CFM International's LEAP-1A (A320neo family) and LEAP-1B (737 MAX family) through a modernized engine test facility upgraded with the latest data acquisition and control system supplied by Safran Test Cells.

According to the IATA report titled Airport Technology Roadmap to 2050, new commercial aircraft will still be revolutionary developments with a traditional tube-and-wing configuration and turbofan engines powered by conventional jet fuel until 2035. From 2035 onwards, the industry is expected to witness revolutionary changes in aircraft configurations and propulsion systems. The new designs include strut-braced wings, blended wing bodies, and battery-electric aircraft. Hence, increasing aircraft deliveries and modernization of the old fleet drive the growth of the segment during the forecast period.

Malaysia is Projected to Show the Highest Growth During the Forecast Period

The growth in air passenger traffic and expansion in aviation services on international and domestic routes is estimated to drive demand in the Malaysian commercial aviation sector. Malaysia's year-to-date (YTD) passenger number in May 2022 was 16.3 million, a 574.6% increase over the same period in 2021. Malaysia Airlines, Malindo Air, and Air Asia Berhad are the major airlines in Malaysia. They cater to the majority of the demand for air travel. As of September 2023, Malaysia Airlines had 286 active aircraft in its fleet, with an average age of 11.4 years. During the last five years, around 65 new aircraft have been delivered.

For instance, in September 2022, Malaysia Airlines Bhd and Spirit AeroSystems Inc. signed a memorandum of understanding (MoU) to offer maintenance, repair, and overhaul (MRO) services for the Boeing B737 Next Generation (NG) aircraft. Under the terms of the agreement, Spirit AeroSystems and Malaysia Airlines would jointly work on establishing repair services for nacelle and flight control surfaces to support the airline's fleet. Also, in April 2022, Honeywell signed two MoUs that will further strengthen the company's presence in Malaysia and relationships with key stakeholders in the country and region. The cooperation is intended to tap into Honeywell's expertise in the maintenance, repair, and overhaul (MRO) of aircraft in various capacities, as the company has signed separate MOUs with Airod Techno Power (ATP) and Galaxy Aerospace. Such developments are expected to drive the demand for the aircraft MRO market in Malaysia during the forecast period.

Southeast Asia Commercial Aircraft MRO Industry Overview

The Southeast Asia commercial aircraft MRO market is semi-consolidated in nature, with few global and local players holding significant shares in the market. Some of the key players in the market are Singapore Technologies Engineering Ltd, Rolls-Royce PLC, Safran, AVIA SOLUTIONS GROUP PLC, and StandardAero. Key players in the market are highly investing in research and development and introducing advanced MRO solutions for commercial aircraft. For instance, in February 2022, SIA opened a new USD 9 million aircraft engine service (AES) facility in Singapore, which is custom-designed to perform at least 60 quick turns per year, with an additional 50% capacity to cope with a surge in demand. Similarly, in 2021, Subang Airport in Malaysia became the first airport in the Southeast Asian region to witness the development of an aircraft MRO facility through a collaboration between Malaysia Airports and homegrown global player Dviation Group of Companies. Moreover, the new facility offers end-to-end aftermarket services, including maintenance, repair, and overhaul (MRO), aircraft teardown, aircraft material recycling, and parts trading.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 MRO Type

- 5.1.1 Airframe

- 5.1.2 Engine

- 5.1.3 Component

- 5.1.4 Line

- 5.2 Aircraft Type

- 5.2.1 Narrowbody

- 5.2.2 Widebody

- 5.3 Geography

- 5.3.1 Southeast Asia

- 5.3.1.1 Malaysia

- 5.3.1.2 Indonesia

- 5.3.1.3 Singapore

- 5.3.1.4 Thailand

- 5.3.1.5 Rest of Southeast Asia

- 5.3.1 Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Singapore Technologies Engineering Ltd

- 6.2.2 SIA Engineering Company Limited

- 6.2.3 Singapore Aero Engine Services Limited

- 6.2.4 StandardAero

- 6.2.5 Garuda Indonesia (GMF AeroAsia)

- 6.2.6 Triumph Group

- 6.2.7 Safran

- 6.2.8 Rolls-Royce plc

- 6.2.9 ExecuJet MRO Services

- 6.2.10 AVIA SOLUTIONS GROUP PLC

- 6.2.11 Subang MRO Sdn Bhd

- 6.2.12 Asia Digital Engineering Sdn Bhd

- 6.2.13 Sepang Aircraft Engineering Sdn Bhd

- 6.2.14 Asia AeroTechnic Sdn Bhd