|

市場調査レポート

商品コード

1693833

中東のフッ素樹脂:市場シェア分析、産業動向、統計、成長予測(2024~2029年)Middle East Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のフッ素樹脂:市場シェア分析、産業動向、統計、成長予測(2024~2029年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 163 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

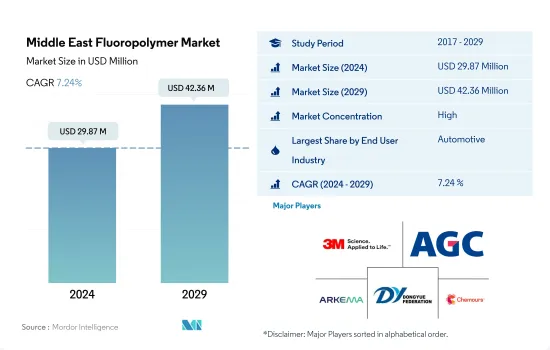

中東のフッ素樹脂市場規模は2024年に2,987万米ドルと推定・予測され、2029年には4,236万米ドルに達し、予測期間(2024~2029年)のCAGRは7.24%で成長すると予測されます。

航空宇宙産業と自動車産業が市場に機会をもたらす

- フッ素樹脂は石油・ガス、半導体・電子、化学処理、自動車、電線・ケーブル、建築、航空宇宙、医薬などのセグメントに応用されています。中東のフッ素樹脂市場は建築・建設産業と自動車産業が牽引しており、2021年の売上高シェアは9.75%と39.96%です。

- 建築・建設産業は、同地域におけるフッ素樹脂の最大消費者です。2022年の中東のフッ素樹脂市場規模シェアは11.4%でした。同地域の新設床面積は、2022年の42億平方フィートから2029年には49億平方フィートに達すると予想されており、これが今後数年間のフッ素樹脂需要を牽引するとみられます。

- 自動車産業はこの地域におけるフッ素樹脂の第2位の消費者で、2022年の消費量シェアでは25.58%を占めます。同産業では、2022年の自動車生産台数が2021年比で32.8%増加しました。EVの主要部品であるリチウムイオンバッテリーにおけるフッ素樹脂の消費増加が、予測期間中の市場を牽引するとみられます。

- 航空宇宙産業は、予測期間(2023~2029年)のCAGRが8.42%で、収益面でこの地域で最も急成長する産業となる見込みです。この成長は、フッ素樹脂成分が攻撃的なエッチングプロセスに耐え、航空宇宙産業で使用されるマイクロチップやその他の電子機器の製造に必要な純度を提供できることに起因しています。また、極端な温度にも耐え、腐食にも耐えることから、さまざまな航空宇宙部品のコーティングにも使用されています。

アラブ首長国連邦への投資がフッ素樹脂の需要を押し上げる

- フッ素樹脂は中東で、産業機械や自動車などのコーティングやライナーなどの用途に使用されています。同地域のフッ素樹脂市場は、サウジアラビアとアラブ首長国連邦が世界のフッ素樹脂市場全体の売上高の0.83%を占めています。

- サウジアラビアはこの地域のフッ素樹脂市場で最大の消費国であり、需要の増加により航空宇宙、自動車、産業機械セグメントの主要用途で金額ベースで25.69%のシェアを占めています。自動車生産の増加がサウジアラビアのフッ素樹脂市場を牽引しており、2022年の地域全体のシェアは1.13%でした。

- アラブ首長国連邦は中東のフッ素樹脂市場で第2位の消費国で、2022年の売上高シェアは6.06%です。同国の電子機器生産による収益のCAGRは8.71%であり、アラブ首長国連邦のフッ素樹脂需要は予測期間中に増加するとみられます。

- その他の中東セグメントは、自動車生産の増加により、フッ素樹脂市場の金額ベースで58.8%のシェアを持つ中東最大の市場の1つです。その他の中東地域の自動車生産台数は、中東地域全体で98.4%のシェアを占めています。

- アラブ首長国連邦はこの地域で最も急成長している国で、予測期間中のCAGRは売上高で約7.06%と予想されます。この成長は、アラブ首長国連邦の金融ハブとして、2033年に経済規模を倍増させ、イノベーションによる経済開発技術セグメントで8兆7,000億米ドルを計上するための投資計画の結果であると予想されます。

中東のフッ素樹脂市場の動向

政府と民間企業からの投資拡大

- 中東では、サウジアラビアが電気・電子産業の主要市場の一つとして急浮上しています。石油・ガス産業のほか、サウジアラビアには大規模な消費者基盤と幅広い産業があり、これが電気・電子産業の年間生産量の急速な増加に寄与しています。このため、同地域の電気・電子機器生産は、2017~2019年にかけて収益ベースでCAGR 18%を記録しました。

- 2020年には、COVID-19の大流行により、リモートワークやホームエンターテイメント用の民生用電子機器製品の需要が増加しました。2020年、サウジアラビアは世界で最も高いスマートフォン普及率約97%を記録し、これによりサウジアラビアの顧客の約60%がソーシャルネットワークを通じて新しい売り手を発見することが可能になりました。サウジアラビアは、主にパンデミックの影響により、eコマースの成長率が60%近く(2019~2020年にかけて)上昇しました。電気・電子生産からの収益は、前年度比で1.8%増加しました。

- 電気・電子生産は、予測期間中(2023~2029年)に金額で8.51%のCAGRが見込まれます。成長の主要原動力は、政府とSamsungのようなメーカーからの投資の拡大であると考えられます。Samsungは中東にも5G無線技術を売り込んでいます。サウジアラビアはビジョン2030構想に沿って5Gネットワークを導入しました。このような要因がすべて、同地域の予測期間中のエレクトロニクス生産を押し上げると予想されます。

中東のフッ素樹脂産業の概要

中東のフッ素樹脂市場はかなり統合されており、上位5社で75.30%を占めています。この市場の主要企業は、3M、AGC Inc.、Arkema、Dongyue Group、The Chemours Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- フッ素樹脂貿易

- 規制の枠組み

- サウジアラビア

- アラブ首長国連邦

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- その他

- サブレジンタイプ

- エチレンテトラフルオロエチレン(ETFE)

- フッ素化エチレンプロピレン(FEP)

- ポリテトラフルオロエチレン(PTFE)

- ポリフッ化ビニル(PVF)

- ポリフッ化ビニリデン(PVDF)

- その他のサブレジンタイプ

- 国名

- サウジアラビア

- アラブ首長国連邦

- その他の中東

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- AGC Inc.

- Arkema

- Dongyue Group

- Solvay

- The Chemours Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 5000171

The Middle East Fluoropolymer Market size is estimated at 29.87 million USD in 2024, and is expected to reach 42.36 million USD by 2029, growing at a CAGR of 7.24% during the forecast period (2024-2029).

Aerospace and automotive industries to create opportunities for the market

- Fluoropolymers have applications in oil and gas, semiconductor and electronic, chemical processing, automotive, wire and cable, building, aerospace, and pharmaceutical sectors. The Middle Eastern fluoropolymer market is led by the building and construction and automotive industries, accounting for 9.75% and 39.96% shares in 2021 in terms of revenue.

- The building and construction industry is the largest consumer of fluoropolymers in the region. It held a share of 11.4% of the Middle Eastern fluoropolymer market in 2022 by volume. The region's new floor area is expected to reach 4.9 billion sq. ft by 2029 from 4.2 billion sq. ft in 2022, which is expected to drive the demand for fluoropolymers in the coming years.

- The automotive industry is the second-largest consumer of fluoropolymers in the region, accounting for 25.58% of the consumption share in 2022 by volume. The industry witnessed a 32.8% increase in the production of vehicles by volume in 2022 compared to 2021. The increased consumption of fluoropolymers in lithium-ion batteries, the main components of an EV, is expected to drive the market during the forecast period.

- The aerospace industry is expected to be the fastest-growing industry in the region in terms of revenue, with a CAGR of 8.42% during the forecast period (2023-2029). This growth can be attributed to the fluoropolymer component's ability to withstand the aggressive etching process and provide the necessary purity required to produce microchips and other electronics used in the aerospace industry. It is also used in the coatings of various aerospace components as it can withstand extreme temperatures and resist corrosion.

Investments in UAE to boost the demand for fluoropolymer

- Fluoropolymers are used in the Middle East for applications such as coatings and liners for industrial machinery, automotive, and many others. The fluoropolymers market in the region is dominated by Saudi Arabia and the United Arab Emirates, with a share of 0.83% of the revenue of the global overall fluoropolymers market.

- Saudi Arabia is the largest consumer in the regional fluoropolymer market, with a share of 25.69% by a value in major applications in the aerospace, automotive, and industrial machinery sectors due to increasing demand. The rise in the production of automobiles drives the fluoropolymer market in Saudi Arabia, which contributed a 1.13% share of the overall region in 2022.

- The United Arab Emirates is the second-largest consumer in the Middle Eastern fluoropolymer market, with a share of 6.06% of the revenue in 2022. With a CAGR of 8.71% in terms of revenue from electronics production in the country, the demand for fluoropolymers in the United Arab Emirates is likely to increase during the forecast period.

- The Rest of the Middle East segment is one of the largest markets in the Middle East, with a share of 58.8% by value of the fluoropolymer market due to the rise in automotive production. Automotive production in the Rest of Middle East has a share of 98.4% in the overall Middle Eastern region.

- The United Arab Emirates is the fastest-growing country in the region, with an expected CAGR of around 7.06% by revenue during the forecast period. This growth is expected to be a result of the plans for investment in the United Arab Emirates' financial hub to double the size of its economy by 2033, accounting for USD 8.7 trillion in economic development technology sectors through innovation.

Middle East Fluoropolymer Market Trends

Growing investments from the government and private players

- In the Middle East, Saudi Arabia is quickly emerging as one of the key markets for the electrical and electronics industry. Aside from the oil and gas industry, the country has a sizable consumer base and a broad range of industrial pursuits, contributing to the rapid annual increase in production for the electrical and electronics industry. Thus, electrical and electronics production in the region registered a CAGR of 18% from 2017 to 2019 in revenue terms.

- In 2020, the demand for consumer electronics for remote working and home entertainment increased due to the COVID-19 pandemic. In 2020, Saudi Arabia registered the highest smartphone penetration rate, around 97%, in the world, which enabled approximately 60% of Saudi customers to discover new sellers through social networks. Saudi Arabia faced a higher rate of e-commerce growth, nearly 60% (between 2019 and 2020), mainly due to the pandemic. The revenue from electrical and electronics production increased by 1.8% compared to the previous year.

- Electrical and electronic production is expected to witness a CAGR of 8.51% in value during the forecast period (2023-2029). The major driving component behind the growth is likely to be the growing investments from the government and the manufacturers like Samsung. Samsung has also been pitching its 5G wireless technology to the Middle East. Saudi Arabia implemented a 5G network in line with the Vision 2030 initiative. All such factors are expected to boost electronics production over the forecast period in the region.

Middle East Fluoropolymer Industry Overview

The Middle East Fluoropolymer Market is fairly consolidated, with the top five companies occupying 75.30%. The major players in this market are 3M, AGC Inc., Arkema, Dongyue Group and The Chemours Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.3 Regulatory Framework

- 4.3.1 Saudi Arabia

- 4.3.2 United Arab Emirates

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.3 Polytetrafluoroethylene (PTFE)

- 5.2.4 Polyvinylfluoride (PVF)

- 5.2.5 Polyvinylidene Fluoride (PVDF)

- 5.2.6 Other Sub Resin Types

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arkema

- 6.4.4 Dongyue Group

- 6.4.5 Solvay

- 6.4.6 The Chemours Company

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms