アフリカのフッ素樹脂:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Africa Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 157 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693832

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

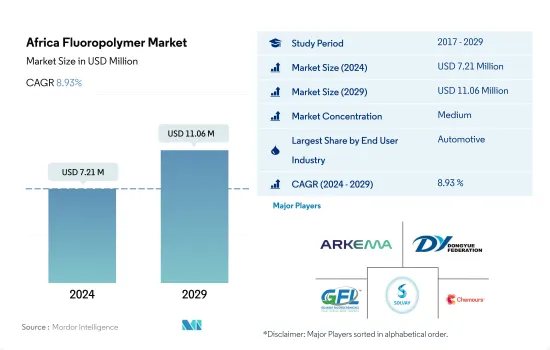

アフリカのフッ素樹脂市場規模は2024年に721万米ドルと推定・予測され、2029年には1,106万米ドルに達し、予測期間(2024~2029年)のCAGRは8.93%で成長すると予測されています。

自動車産業への海外投資が市場需要を拡大

- フッ素樹脂は、石油・ガス、半導体エレクトロニクス、化学処理、自動車、電線・ケーブル、建築、航空宇宙、医薬品など、さまざまな産業で応用されています。アフリカにおけるフッ素樹脂の需要は、2023年には前年比金額ベースで2022年比8.04%成長すると推定されます。

- この地域では自動車セグメントがフッ素樹脂の最大消費者で、2023年には金額ベースで36.58%のシェアを占めます。同産業では、2023年の自動車生産台数が2022年比で2.95%増加しました。電気自動車(EV)の主要部品であるリチウムイオンバッテリーにおけるフッ素樹脂の消費拡大が、予測期間中の市場を牽引するとみられます。

- この地域では、電気・電子産業がフッ素樹脂の第2位の消費者です。この産業における生産量の増加は、今後数年間、フッ素樹脂の需要を押し上げると考えられます。同地域の電気・電子製品からの収益は、2023年の306億米ドルから2029年には512億米ドルに達すると予測されています。技術の進歩が今後の民生用電子機器需要の増加に寄与すると予想され、産業の予測収益は2023年の105億9,000万米ドルから2027年には177億9,000万米ドルに達します。

- 建築・建設産業は、この地域で最も急成長しているフッ素樹脂のエンドユーザー産業であり、予測期間(2023~2029年)に金額ベースでCAGR 9.01%を記録すると予想されます。この成長の背景には、建設プロジェクトに手頃な価格で耐久性のある構造物が急速に採用されていることがあり、これが今後数年間、フッ素樹脂の需要をさらに押し上げると考えられます。

南アフリカは引き続きこの地域最大の急成長市場

- フッ素樹脂はナイジェリアや南アフリカなどのアフリカ諸国で、自動車、航空宇宙、産業機械などさまざまな産業に使用されています。2022年のフッ素樹脂の世界消費量に占めるアフリカの割合は、金額ベースで0.21%です。

- 南アフリカは、航空宇宙、自動車、産業、機械セグメントが伸びているため、この地域最大のフッ素樹脂消費国です。同国は、2022年に地域レベルで航空機部品生産68.7%増収、自動車生産44.4%増量を記録し、フッ素樹脂の需要増加を牽引しています。気候に配慮した施策の増加による自動車、工業、機械生産の増加が、同国のフッ素樹脂需要を牽引すると予想されます。

- ナイジェリアのフッ素樹脂需要は、自動車生産、工業、機械などの増加により大幅に増加しています。2022年の同国の自動車生産台数は39万4,000台で、地域シェアは32.88%です。同国の産業機械セグメントも拡大しており、工具・機械セグメントの売上は2023年に30億2,000万米ドルに達すると予測されています。同市場の年間成長率は5.17%(CAGR 2023~2029)と予想されています。これらの要因が、同国におけるフッ素樹脂の需要を促進すると予想されます。

- 南アフリカはフッ素樹脂の急成長国で、予測期間2023~2029年の売上高CAGRは8.25%です。エレクトロニクスセグメントの急成長と旧式航空機のアップグレードが相まって、同地域での同樹脂の需要増加が見込まれています。

アフリカのフッ素樹脂市場動向

急増する需要に対応するため製造業が増加中

- 南アフリカはアフリカ有数の製造拠点です。その製造能力、効率的な物流ネットワーク、優遇的な地域市場アクセスにより、南アフリカはアフリカへの製品供給を目指すエレクトロニクス企業にとって理想的な立地となっています。南アフリカには、電気機械、民生用電子機器製品、通信機器から消費者向け電子機器に至るまで、多様なエレクトロニクス産業があります。2022年、アフリカ地域は現地の電気・電子機器需要の約70%を輸入しました。

- 民生用電子機器産業は依然として輸入に大きく依存しています。推定によると、2018年には南アフリカが全消費者向け電子機器の60%をアフリカに持ち込みました。2020年、同国における電気・電子機器生産は、政府によって採用された広範な封鎖と、封鎖のために直面したサプライチェーンの混乱により、売上高ベースで前年比約3.2%の成長率で減少しました。フィーチャーフォンのセグメントでは、ベンダーがフィーチャーフォンからエントリーレベルのスマートフォンへの移行を進めたため、出荷台数は前年比26.6%減の2,190万台となりました。このような要因がすべて、2020~2022年のCAGRマイナス9.41%で、この地域の電気・電子部品の生産減少につながりました。

- 政府は、国内製造の促進・支援、研究開発、電気・電子製造業の安全基準の開発に注力しています。電気・電子産業用部品の生産高は、アフリカの新興中産階級に供給するため、予測期間中(2023~2029年)にCAGR 6.28%を記録すると予想されます。

アフリカのフッ素樹脂産業概要

アフリカのフッ素樹脂市場は適度に統合されており、上位5社で59.76%を占めています。この市場の主要企業は、Arkema、Dongyue Group、Gujarat Fluorochemicals Limited(GFL)、Solvay、The Chemours Companyなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- フッ素樹脂貿易

- 規制の枠組み

- ナイジェリア

- 南アフリカ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- その他

- サブレジンタイプ

- エチレンテトラフルオロエチレン(ETFE)

- フッ素化エチレンプロピレン(FEP)

- ポリテトラフルオロエチレン(PTFE)

- ポリフッ化ビニル(PVF)

- ポリフッ化ビニリデン(PVDF)

- その他のサブレジンタイプ

- 国名

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arkema

- Dongyue Group

- Gujarat Fluorochemicals Limited(GFL)

- Solvay

- The Chemours Company

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 5000170

The Africa Fluoropolymer Market size is estimated at 7.21 million USD in 2024, and is expected to reach 11.06 million USD by 2029, growing at a CAGR of 8.93% during the forecast period (2024-2029).

Foreign investments in the automotive industry to augment market demand

- Fluoropolymers have applications in various industries, including oil and gas, semiconductor and electronics, chemical processing, automotive, wire and cable, building, aerospace, and pharmaceuticals. The demand for fluoropolymer resin in Africa is estimated to grow by 8.04% in year-on-year value terms in 2023 compared to 2022.

- The automotive segment is the largest consumer of fluoropolymers in the region, accounting for a share of 36.58% in value terms in 2023. The industry witnessed a 2.95% increase in vehicle production volume in 2023 compared to 2022. The growing consumption of fluoropolymers in lithium-ion batteries, a key component in electric vehicles (EVs), is expected to drive the market in the forecast period.

- The electrical and electronics industry is the second-largest consumer of fluoropolymer resin in the region. The rising production in this industry will drive the demand for fluoropolymer resin over the coming years. The revenue from electrical and electronics products in the region is projected to reach USD 51.2 billion by 2029, up from USD 30.6 billion in 2023. Technological advancements are expected to contribute to the increased demand for consumer electronics in the future, with the industry's projected revenue reaching USD 17.79 billion in 2027 from USD 10.59 billion in 2023.

- The building & construction industry is the fastest-growing end-user industry for fluoropolymer resin in the region, expected to record a CAGR of 9.01% in terms of value during the forecast period (2023-2029). This growth is attributed to the rapid adoption of affordable and durable structures for construction projects which will further drive the demand for fluoropolymer resin over the coming years.

South Africa will continue to be the region's largest and fastest-growing market

- Fluoropolymer is used in African countries such as Nigeria and South Africa for various industries, including automotive, aerospace, and industrial machinery. Africa accounted for 0.21% by value of the global consumption of fluoropolymer resins in 2022.

- South Africa is the region's largest consumer of this resin due to its rising aerospace, automotive, industrial, and machinery segments. The country recorded aircraft components production by 68.7% in revenue and vehicle production by 44.4% in volume at the regional level in 2022, driving the increasing demand for fluoropolymer resins. The rising automotive, industrial, and machinery production due to an increase in climate-conscious policies is expected to drive the demand for fluoropolymer resins in the country.

- Nigeria's demand for fluoropolymer resins is increasing significantly due to rising vehicle production, industrial and machinery, and others. In 2022, the country produced 394 thousand units of vehicles, with a share of 32.88% of the region. The country's industrial machinery segment is also expanding, and it is projected that revenue in the tools and machines segment will amount to USD 3.02 billion in 2023. The market is expected to grow annually by 5.17% (CAGR 2023-2029). These factors are expected to drive the demand for fluoropolymer resins in the country.

- South Africa is the fastest-growing country of fluoropolymer resins, with a CAGR of 8.25% by revenue during the forecast period 2023-2029. The rapid growth of the electronics segment, coupled with the upgradation of older aircraft, is expected to increase the demand for this resin in the region.

Africa Fluoropolymer Market Trends

Manufacturing on the rise to tackle the rapidly growing demand

- South Africa is the leading manufacturing hub in Africa. Its manufacturing capabilities, efficient logistics network, and preferential regional market access position the country as an ideal location for electronics companies seeking to supply their products to Africa. South Africa has a diverse electronics industry that ranges from electrical machinery, household appliances, and telecommunication equipment to consumer electronics. In 2022, the African region imported around 70% of its local electrical and electronics demand.

- The consumer electronics industry still relies heavily on imports. According to estimates, South Africa brought 60% of all consumer electronics into Africa in 2018. In 2020, the electrical and electronic production in the country decreased at a growth rate of around 3.2%, by revenue, compared to the previous year, owing to the widespread lockdown adopted by the government and the supply chain disruption faced due to the lockdown. In the feature phone space, shipments were down by 26.6% to 21.9 million units as vendors were transitioning away from these devices toward entry-level smartphones. All such factors led to a decrease in the production of electrical and electronic components in the region at a CAGR of -9.41% from 2020 to 2022.

- The government is focused on promoting and supporting domestic manufacturing, R&D, and developing safety standards for the electrical and electronics manufacturing industry. The output of electrical and electronic industrial components is anticipated to record a CAGR of 6.28% during the forecast period (2023-2029) to supply the emerging African middle-class population.

Africa Fluoropolymer Industry Overview

The Africa Fluoropolymer Market is moderately consolidated, with the top five companies occupying 59.76%. The major players in this market are Arkema, Dongyue Group, Gujarat Fluorochemicals Limited (GFL), Solvay and The Chemours Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.3 Regulatory Framework

- 4.3.1 Nigeria

- 4.3.2 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.3 Polytetrafluoroethylene (PTFE)

- 5.2.4 Polyvinylfluoride (PVF)

- 5.2.5 Polyvinylidene Fluoride (PVDF)

- 5.2.6 Other Sub Resin Types

- 5.3 Country

- 5.3.1 Nigeria

- 5.3.2 South Africa

- 5.3.3 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arkema

- 6.4.2 Dongyue Group

- 6.4.3 Gujarat Fluorochemicals Limited (GFL)

- 6.4.4 Solvay

- 6.4.5 The Chemours Company

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アフリカのフッ素樹脂:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 157 Pages

- 納期

- 2~3営業日