|

市場調査レポート

商品コード

1693785

米国の信用格付機関:市場シェア分析、産業動向、成長予測(2025年~2030年)United States Credit Agency - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の信用格付機関:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

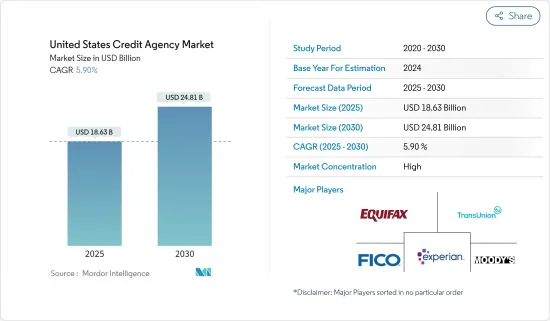

米国の信用格付機関市場規模は2025年に186億3,000万米ドルと推定され、2030年には248億1,000万米ドルに達すると予測され、市場推定・予測期間(2025~2030年)のCAGRは5.9%です。

国家認定統計格付機関(NRSRO)などの信用格付機関は、事業体や金融商品の信用力を評価する上で重要な役割を果たしています。NRSROは金融債務を迅速に履行する能力を測定し、投資家に極めて重要な洞察を提供しています。しかし、NRSROは2023年末までにわずか10社に絞られるなど、市場の集中度は高いです。信用格付機関は、主に「発行体ペイ」モデルが普及しているため、利益相反の管理という大きな課題に直面しています。このモデルは、顧客維持のために過度に楽観的な格付けを提供するインセンティブを格付機関に与える可能性があり、格付けの正確性を損なう可能性があります。

信用格付けの需要が高まっているにもかかわらず、特にストラクチャード・ファイナンスでは懸念があります。格付機関はリスク評価を拡大してきたが、特に金融危機の際には、格付が真のリスクを反映しなかった事例があります。破綻寸前の証券が依然として高格付けを受けており、こうした評価の信頼性に疑問が投げかけられています。信用機関は、進化する不正に対抗するため、先進的分析と不正検知モデルに多大な投資を行っています。ソーシャルメディアやデバイス情報のような従来とは異なるデータソースを活用することで、信用機関はより豊かな消費者プロファイルを描くことができ、不正の発見に役立っています。個人情報盗難の懸念が高まる中、消費者はますます保護サービスに目を向けるようになっています。

米国信用機関の市場動向

消費者信用残高の増加動向

消費者信用状況の拡大により、貸金業者は借り手のリスクを評価するために信用格付報告書に頼るようになっています。この依存度の高まりは、正確で詳細な信用格付に対する需要の高まりを浮き彫りにしています。クレジット口座数が増加するにつれて、消費者は自分の信用状態についてより慎重になり、個人信用報告書の需要が急増します。信用機関は、先進的分析とデータ処理能力によって強化された先進的クレジットスコアリングモデルに投資することで対応しています。貸し手は、クレジット・ポートフォリオの増加に伴い、より洗練されたリスク評価ツールを求めています。信用機関はこの需要に応えるため、専門的なリスク評価サービスを導入しています。信用機関はクレジットスコアリングの精度を高めるため、データ収集の幅を広げています。現在では、公共料金の決済、賃貸履歴、通信データなどの代替情報源を掘り下げています。このような取り組みには、データ、先進的処理インフラ、専門知識が必要です。

米国経済の安定が信用機関の革新と拡大を促進

経済が拡大するにつれ、金融機関は融資を増やし、信用情報機関による信用報告書や信用スコアの必要性を高めています。安定した経済は金融技術革新に拍車をかけ、新興経済諸国は新しいスコアリングモデルやリスクツールの開発を促します。経済成長によってデータ収集や報告業務が強化され、信用格付会社はモデルを改良するための豊富なデータセットを手に入れることができます。さらに、景気拡大は信用機関にとって新たなデータソースをもたらし、より正確なリスク評価に役立ちます。景気拡大に伴い、金融セクタでは複雑な商品が急増し、信用機関の先進的リスクツールの必要性が浮き彫りになっています。安定した経済は投資家の信頼を高め、投資機会を評価するための信用格付けへの需要を高めています。

経済成長により、独特の信用リスクプロファイルを持つ新しい市場セグメントが生まれることも多く、信用機関はサービスの幅を広げ、新たな顧客層を獲得することができます。この景気上昇を利用し、信用機関は未開拓の市場を開拓しています。信用格付報告書、スコアリングモデル、リスクツールに対する需要の高まりは、これらの機関の収益と利益率の向上に直結します。同時に、安定した経済背景は、AIや機械学習のような最先端技術への投資を後押しし、信用機関のサービスをさらに向上させています。安定した経済成長環境は、最終的に信用機関セクタが繁栄するための舞台を整え、需要を強化し、データアクセスを洗練させ、資産の質を高め、産業の基盤を強固なものにします。

米国信用機関産業概要

米国の信用機関市場は統合されています。Experian PLC、S& P Global、Moody's Corporation、Equifax、TransUnionといった大手数社が総体として圧倒的なシェアを占めています。これらの企業は、広範なデータベース、貸し手との深い関係、最先端の技術を駆使しており、新規参入の可能性のある企業にとって手ごわい課題となっています。これらの大手企業は、包括的なデータカバレッジと市場での確固たる存在感により、競争優位性を享受しています。しかし、技術、データ、法規制遵守に多額の投資を必要とすることから生じる市場の高い障壁が、新規参入の足かせとなっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 米国の格付機関に影響を与える人口動態とマクロ経済要因

- 市場の促進要因

- 詐欺やサイバー脅威の増加に伴う信用報告書需要の高まり

- 市場抑制要因

- 信用格付機関のビジネスモデルにおける利益相反

- 市場に影響を与える規制状況と産業施策

- 市場を形成する主要技術の進歩

- 産業の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 消費者債務の動向に関する洞察

- ストラクチャード・ファイナンス市場における信用格付機関の役割に関する洞察

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- 顧客タイプ別

- 個人

- 商業

- 産業別

- ダイレクト・ツーコンシューマー

- 政府・公共機関

- 医療

- 金融サービス

- ソフトウェアと専門サービス

- メディア技術

- 自動車

- 電気通信・公益事業

- 小売・eコマース

- その他の産業別

第6章 競合情勢

- 市場集中度概要

- 企業プロファイル

- Equifax Inc.

- Transunion

- Experian PLC

- Fair Isaac Corp.

- Moody's Corporation

- Fitch Ratings

- S& P Global Inc.

- Kroll Bond Rating Agency(KBRA)

- Morningstar DBRS

- A.M Best Ratings*

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

The United States Credit Agency Market size is estimated at USD 18.63 billion in 2025, and is expected to reach USD 24.81 billion by 2030, at a CAGR of 5.9% during the forecast period (2025-2030).

Credit rating agencies, such as National Recognized Statistical Rating Organizations (NRSROs), play a crucial role in assessing the creditworthiness of entities and financial products. They gauge the ability to meet financial obligations promptly, providing pivotal insights for investors. However, the market is highly concentrated, with only ten NRSROs by the end of 2023. Credit rating agencies face a significant challenge in managing conflicts of interest, primarily due to the prevalent 'issuer-pay' model. This model can incentivize agencies to offer overly optimistic ratings to retain clients, potentially compromising the ratings' accuracy.

Despite the rising demand for credit ratings, there have been concerns, especially in structured finance. While agencies have expanded their risk assessments, there have been instances, notably during the financial crisis, where ratings failed to reflect the true risks. Securities on the brink of bankruptcy were still receiving high ratings, raising questions about the reliability of these assessments. Credit agencies are investing significantly in advanced analytics and fraud detection models to combat evolving fraud. By leveraging unconventional data sources, like social media and device information, credit agencies can paint richer consumer profiles, aiding in spotting irregularities. With rising identity theft concerns, consumers are increasingly turning to protection services.

United States Credit Agency Market Trends

Rising Trends In Consumer Credit Outstanding

The expanding consumer credit landscape increasingly prompts lenders to rely on credit reports to assess borrower risk. This growing reliance highlights the escalating demand for precise and detailed credit reporting. As the number of credit accounts rises, consumers become more vigilant about their credit health, leading to a surge in demand for personal credit reports. Credit agencies are responding by investing in sophisticated credit scoring models bolstered by advanced analytics and data processing capabilities. Lenders are searching for more refined risk assessment tools with increasing credit portfolios. Credit agencies are introducing specialized risk assessment services to meet this demand. Credit agencies are broadening their data collection efforts to improve credit scoring accuracy. They are now delving into alternative sources like utility payments, rental histories, and telecommunications data. Such initiatives require data, advanced processing infrastructure, and specialized expertise.

US Economy's Stability Fuels Credit Agency Innovation And Expansion

As economies expand, financial institutions ramp up lending, driving the need for credit reports and scores from agencies. A stable economy spurs financial innovation, prompting credit agencies to develop new scoring models and risk tools. Economic growth often enhances data collection and reporting practices, equipping credit agencies with richer datasets to refine their models. Furthermore, economic upswings introduce fresh data sources for credit agencies, aiding in more precise risk assessments. With the economic expansion, the financial sector witnesses a surge in complex products, underscoring the necessity for advanced risk tools from credit agencies. A stable economy bolsters investor confidence, heightening the demand for credit ratings to evaluate investment opportunities.

Economic growth frequently ushers in new market segments with distinct credit risk profiles, enabling credit agencies to broaden their services and reach new clientele. Capitalizing on this economic upswing, credit agencies are exploring untapped markets. The escalating demand for credit reports, scoring models, and risk tools directly translates into heightened revenues and profitability for these agencies. Simultaneously, a stable economic backdrop empowers credit agencies to invest in cutting-edge technologies like AI and machine learning, further elevating their services. A stable economic growth environment ultimately sets the stage for the credit agency sector to flourish, bolstering demand, refining data access, enhancing asset quality, and solidifying the industry's base.

United States Credit Agency Industry Overview

The US credit agency market is consolidated. It is dominated by a few major players, namely Experian PLC, S&P Global, Moody's Corporation, Equifax, and TransUnion, collectively holding the lion's share. These firms wield extensive databases, deep lender relationships, and cutting-edge technology, posing formidable challenges for potential newcomers. These major players enjoy a competitive edge with their comprehensive data coverage and entrenched market presence. However, the market's high barriers, stemming from the need for substantial investments in technology, data, and regulatory compliance, deter new entrants.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.1.1 Demographic and Macroeconomic Factors Impacting Rating Agencies in the US Industry

- 4.2 Market Drivers

- 4.2.1 Rising Demands Of Credit Reports With Increasing Fraud And Cyber Threats

- 4.3 Market Restraints

- 4.3.1 Conflict Of Interest In Credit Rating Agency Business Model

- 4.4 Regulatory Landscape and Industry Policies Impacting the Market

- 4.5 Key Technological Advancement Shaping the Market

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights on Consumer Debt Trends in the Market

- 4.8 Insights on Role of Credit Rating Agencies in Structured Finance Market

- 4.9 Impact of Covid-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Client Type

- 5.1.1 Individual

- 5.1.2 Commercial

- 5.2 By Vertical

- 5.2.1 Direct-to-Consumer

- 5.2.2 Government and Public Sector

- 5.2.3 Healthcare

- 5.2.4 Financial Services

- 5.2.5 Software and Professional Services

- 5.2.6 Media and Technology

- 5.2.7 Automotive

- 5.2.8 Telecom and Utilities

- 5.2.9 Retail and E-commerce

- 5.2.10 Other Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Equifax Inc.

- 6.2.2 Transunion

- 6.2.3 Experian PLC

- 6.2.4 Fair Isaac Corp.

- 6.2.5 Moody's Corporation

- 6.2.6 Fitch Ratings

- 6.2.7 S&P Global Inc.

- 6.2.8 Kroll Bond Rating Agency (KBRA)

- 6.2.9 Morningstar DBRS

- 6.2.10 A.M Best Ratings*