|

市場調査レポート

商品コード

1693726

米国と欧州の光ファイバーケーブル- 市場シェア分析、産業動向、成長予測(2025年~2030年)United States And European Fiber Optic Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国と欧州の光ファイバーケーブル- 市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

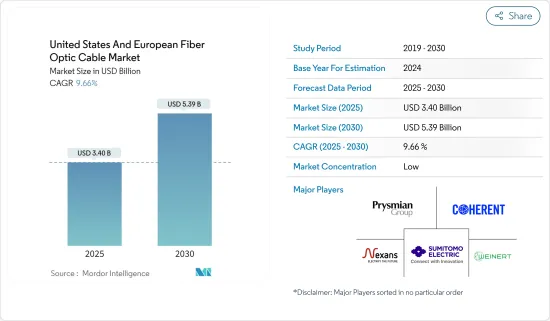

米国と欧州の光ファイバーケーブル市場規模は、2025年に34億米ドルと推定され、予測期間(2025~2030年)のCAGRは9.66%で、2030年には53億9,000万米ドルに達すると予測されています。

主要ハイライト

- 第5世代ネットワークと光ファイバーインフラの進化が、産業全体のデジタル変革を推進しています。光ファイバーケーブルは、銅線ケーブルよりもセキュリティ、信頼性、帯域幅、安全性に優れています。光ファイバーケーブルと銅線の違いは、光ファイバーケーブルが、銅線を通して情報を伝達する電子パルスではなく、光ファイバー線を通して情報を伝達する光パルスを利用することです。

- オンライン取引やバーチャル会議の増加に伴い、企業は競合を維持するために5Gと光ファイバーケーブルを必要としています。例えば、欧州中央銀行によると、消費者の非経常的な決済に占めるオンライン決済の割合は、2019年のわずか6%から2022年には17%に増加します。したがって、このような動向をサポートするためには、高速インターネットなどの堅牢なインフラが必要であり、これは調査対象市場に機会を創出すると予想されます。

- さらに、光ファイバケーブルは、照明や装飾、データ伝送、手術、機械検査など数多くの産業アプリケーションのためのコスト効率が高く、便利で簡単なソリューションです。また、在宅勤務やハイブリッド勤務モデルの増加も、米国と欧州全域でFTTHの必要性を高めています。

- データトラフィックの増加、特にインターネットプロトコル(IP)が、高ネットワーク帯域幅のニーズを急増させています。著名なサービスプロバイダは、6~9ヵ月ごとにバックボーンの帯域幅が倍増していることを記録しています。インターネットトラフィックの増加により、帯域幅は6~9ヵ月ごとに倍増しています。

- 米国と欧州市場における光ファイバー統合インフラの拡大も、特に電気通信産業における光ファイバーケーブルのニーズを非常に高めています。光ファイバーネットワークと光ファイバーワイヤも、ブロードバンド設備によって大幅に改善されました。これらのアーキテクチャには、FTTH、FTTP、FTTC、FTTBが含まれます。

- 発展途上国における光ファイバー生産者の接続ニーズの増加は、大きなビジネス展望を提供しています。しかし、ワイヤレスソリューション需要の増加や光ファイバーケーブルの敷設の困難さといった要因は、市場の成長にとっていくつかの運用上の困難をもたらします。

- また、米国と欧州の両地域がコビド後の景気後退に見舞われているように、マクロ経済的要因も調査市場の成長に大きな影響を与えます。さらに、ロシアとウクライナの戦争や米国と中国の紛争などの地政学的問題も、市場の持続的成長にとって厳しい環境を作り出しています。

米国と欧州の光ファイバーケーブル市場動向

光ファイバーと5G展開への投資増が市場を牽引

- 米国と欧州市場は、先進的な通信技術をいち早く導入した国の一つであり、現在もその傾向が続いています。発達したエコシステムの存在やデジタル技術の消費者浸透率の高さなどの要因が、光ファイバーや通信インフラへの投資を増やすよう産業利害関係者を後押ししています。例えば、通信サービスプロバイダのコーニングは最近、アリゾナ州初の光ファイバー網を2023年に設計する計画を明らかにしました。

- 例えば、CommScopeは光ファイバー技術革新のリーダー的存在であり、最も困難なネットワークのための高性能ファイバー接続の境界線を推進しています。同社は産業標準も設定しているため、同社の光ファイバー配線システムは常に要件を超越しています。

- 米国と欧州市場で5Gの導入が進んでいることも、調査された市場の成長を後押ししています。例えば、Ericssonは最近、2025年までにドイツで3.5GHz(5G)展開を行うと発表しました。3.5GHz帯の5Gネットワークは、2023年に予想されている42%から、2025年にはドイツ全体の43%を占めることになります。しかし、2025年にカバーされるのは、ドイツの地理的地域の7%に過ぎないと予想されています。

- 同様に、米国国立科学財団(NSF)は、米国の重要インフラや政府事業者がいつでもどこでも安全に通信できるよう、5Gソリューションの加速に注力しています。例えば、2022年9月、NSFは国防総省との提携を発表しました。1,200万米ドルの投資により、NSFは2022年のコンバージェンス・アクセラレータープログラムに16チームを選出しました。これらのチームは「Track G:Securely Operating Through 5G Infrastructure」に選ばれました。トラックGは、米国連邦政府と軍向けの5G通信を開発するための技術進歩を促進します。

- 米国を拠点とするネットワーク&通信ソリューションプロバイダであるアドトランは、パッシブ光ネットワーク技術を採用したフルファイバーネットワークの構築を可能にし、企業や家庭へのギガビット・アクセスやインフラのバックホールを提供しています。2023年1月、同社はSDX 6330 10Gビット/秒コンボパッシブ光ネットワークファイバーアクセスプラットフォームを発表しました。このプラットフォームにより、サービスプロバイダはコスト効率よく迅速に企業や家庭をファイバーベースのブロードバンドで接続できるようになります。この新しいソリューションは、産業で最も高いポート密度を提供し、400 Gbit/sのアップリンクを搭載した光回線端末の先駆けとなるものです。

- さらに、データ消費の増大は、データ接続をサポートする新しい光ファイバーケーブルネットワークへの投資を促進することによって、研究市場にも機会を生み出しています。例えば、2022年11月、スウェーデンの接続プロバイダ、Arelionは、メキシコと米国間のテキサスを通る2つの大容量光ファイバルートを作る計画を発表しました。新たな高密度波長分割多重ルートは、大容量でスケーラブルな帯域幅伝送に対する需要の高まりに対応し、米国、アジア、欧州のオーバー・ザ・トップ・サプライヤーのメキシコ国内市場へのアクセスを簡素化します。

通信エンドユーザー産業が大きな市場シェアを占める

- 光ファイバーケーブル(OFC)は通信インフラの重要なコンポーネントです。過去10年間、光ファイバーは、特に通信会社の強力な帯域幅ニーズに応えており、伝送媒体の選択肢となっています。調査対象地域には、AT& T、Verizon、Sprint、Vodafone Groupなどの大手通信会社が存在し、世界的・地域的プレゼンスを高めるために光ファイバーネットワークを継続的に拡大しています。

- インターネット、eコマース、コンピュータネットワーク、マルチメディア(音声、データ、ビデオ)など、さまざまなソースからのデータトラフィックの急増は、こうした膨大な量の情報を処理するために、より高い帯域幅を管理できる伝送媒体の必要性を示しています。Eurostatによると、欧州連合(EU)の1日当たりインターネット利用者の割合は、2028年には74.07%であったのに対し、2022年には84%に増加しています。比較的無限の帯域幅を持つ光ファイバー・ケーブルは、この問題に対する重要な解決策のひとつであるため、需要は今後も高水準で推移すると予想されます。

- 通信ネットワークでは、光ファイバーケーブルがセルタワー、データセンター、インターネットサービスプロバイダなどの異なるネットワークノードを接続し、異なる場所間で大量のデータをやり取りできるようにしています。光ファイバー・ケーブルは、高速インターネット接続や、ビデオ会議、オンラインゲーム、クラウドコンピューティングなどの先進的通信技術の開発にも適しています。従って、米国と欧州における5Gネットワークの拡大が、調査対象市場機会を促進すると予想されます。

- さらに、光ファイバーケーブルは、その安全性、拡大性、発生する膨大な量のバックホールトラフィックを処理する無制限の帯域幅の可能性により、リアルタイムのデータ収集と転送に大きく依存する5G、ビッグデータ、IoTなどの進化した技術に対応する帯域幅レベルをサポートするためにも選択されています。5Gの開始により、ネットワークの容量が向上し、遅延が短縮されると予測されています。

- インターネットは、光ファイバーケーブルがデータと通信産業で広く使用されているように、調査対象市場機会を促進している調査対象地域における著しい変革と急成長技術の1つです。例えば、Ericssonによると、調査対象地域ではスマートフォン1台当たりのデータトラフィックが増加し続けており、例えば北米ではスマートフォン1台当たりのデータトラフィックは2021年の13GB/月から2028年には58GB/月に増加すると予測されています。同様に、西欧では、2021年の16GB/月から2028年には56GB/月に成長すると予測されています。

米国と欧州の光ファイバーケーブル産業概要

米国と欧州の光ファイバーケーブル市場はセグメント化されており、Nexans SA、Prysmian Group、Weinert Industries AG、Coherent Corporation、Sumitomo Corporationなどの大手企業が参入しています。同市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、パートナーシップ、買収、合併などの戦略を採っています。

- 2023年3月-世界のネットワーク接続ソリューションのCommScopeは、米国全域のブロードバンド展開を加速し、より多くのコミュニティやサービスが行き届いていない地域を接続するため、光ファイバーケーブル生産の拡大を発表しました。同社によると、この取り組みにより米国内の光ファイバーケーブルの生産量が増加し、十分なサービスを受けていない地域へのブロードバンド展開が早まる。さらに、同社のHeliARC回線は、FTTH展開において年間50万世帯をサポートする見込み。

- 2023年3月-欧州連合は、デジタル10年のための2030年施策プログラムに沿って、建物に光ファイバーケーブルを敷設する義務を発表。新規制に基づき、新規契約ビルや大規模改修中のビルでは、パッシブインフラ(ミニダクト)とビル内光ファイバー配線(光ファイバーケーブル)をアパート/ユニット内のネットワーク終端点まで確保することが義務付けられます。EUはまた、「ファイバー・レディ(光ファイバーの準備が整っている)」ビルに対する認証の提供も計画しています。このような動向は、光ファイバーケーブルの需要を促進すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 主要マクロ経済テーマの影響

第5章 市場力学

- 市場の促進要因

- データトラフィックの増加が光ファイバーケーブルネットワークの需要を創出

- 光ファイバーと5G導入への投資の増加

- 市場課題

- ワイヤレスソリューションに対する需要の高まりと複雑な設置プロセス

第6章 市場セグメンテーション

- エンドユーザー産業別

- 通信

- 電力公益事業

- 防衛/軍事

- 産業

- 医療

- その他

- 国別

- 米国

- ドイツ

- オーストリア、スイス

第7章 競合情勢

- 企業プロファイル

- Nexans SA

- Prysmian Group

- Weinert Industries AG

- Coherent Corporation

- Sumitomo Corporation

- Corning Inc.

- Finisar Corporation

- Leoni AG

- Folan

- Molex LLC

- Fujikura Ltd

- Sterlite Technologies

- Furukawa Electric Co. Ltd

- Smiths Interconnect(Smiths Group PLC)

第8章 産業における光ファイバーの現状

第9章 市場の将来展望

The United States And European Fiber Optic Cable Market size is estimated at USD 3.40 billion in 2025, and is expected to reach USD 5.39 billion by 2030, at a CAGR of 9.66% during the forecast period (2025-2030).

Key Highlights

- The evolution of fifth-generation networks & fiber optic infrastructure has driven digital transformation across industries. Optic fiber cable presents better security, reliability, bandwidth, and security than copper cables. The distinction between a fiber optic cable and a copper wire is that the fiber optic cable utilizes light pulses to transfer information down the fiber lines rather than electronic pulses to transmit information through the copper lines.

- With increasing online transactions & virtual meetings, companies need 5G and optic fiber cable to remain competitive. For instance, according to the European Central Bank, online payments share in consumers' non-recurring payments increased to 17% in 2022 from just 6% in 2019. Hence, to support such trends robust infrastructure such as high-speed internet is required which is anticipated to create opportunities in the studied market.

- Furthermore, fiber optic cables are cost-effective, convenient, & easy solutions for numerous industrial applications, like lighting and decorations, data transmission, surgeries, and mechanical inspections. The growing work-from-home & hybrid work model also drives the need for FTTH throughout the United States and Europe.

- Data traffic growth, specifically Internet Protocol (IP), drives the surge in need for high network bandwidth. Prominent service providers registered bandwidth doubling on their backbones every six to nine months. Due to growing internet traffic, bandwidth doubles every 6 to 9 months.

- The expansion of fiber-integrated infrastructure in the US and the European market has also immensely raised the need for fiber-optic cables, particularly in the telecom industry. Fiber-optic networks and fiberoptic wires have also greatly improved owing to broadband installations. These architectures include FTTH, FTTP, FTTC, & FTTB.

- The increase in the need for connectivity in developing nations for fiber-optic producers offers significant business prospects. Yet factors like the advancement in wireless solution demand & the difficulty of deploying fibreoptic cables provide several operational difficulties for the market's growth.

- Macroeconomic factors also influence the studied market's growth significantly as both the United States and the European regions have been witnessing economic downturns post-covid. Furthermore, geopolitical issues such as the Russia-Ukraine war, and the US-China disputes also creates a challenging environment for an uninterrupted growth of the market.

US & European Fiber Optic Cable Market Trends

Rising Investment in Fiber Optic and 5G Deployment Drives the Market

- The US and European markets have been among the early adopters of advanced telecom technologies and continue to remain so. Factors such as the presence of developed ecosystems and higher consumer penetration of digital technologies support encourage the industry stakeholders to increase investments in fiber optic and telecom infrastructure. For instance, Corning, the telecom service provider, recently disclosed plans to design Arizona's first fiber network in 2023, anticipated to serve over 100,000 residences.

- Additionally, the studied regions also have the presence of some of the biggest fiber optic cable companies who continue to expand their regional presence; for instance, CommScope is among the leaders in fibreoptic innovation and drives the boundaries of high-performance fiber connectivity for the most challenging networks. Since the company also sets industry standards, its fiber-optic cabling systems always transcend requirements.

- The growing deployment of 5G in the US and European markets also favors the studied market's growth. For instance, Ericsson, recently stated that the 3.5 GHz (5G) roll-out will be conducted in Germany by 2025. The 3.5 GHz 5G network would constitute 43% of the total German population by 2025, up from 42%, which is anticipated in 2023. However, only 7% of the geographical region in Germany is expected to be covered in 2025.

- Similarly, the US National Science Foundation (NSF) concentrates on accelerating 5G solutions to support US critical infrastructure and government operators to communicate securely anytime and anywhere. For instance, in September 2022, NSF announced a partnership with the Department of Defense Office. With an investment of USD 12 million, NSF selected 16 teams for the Convergence Accelerator program in 2022. These teams were chosen for "Track G: Securely Operating Through 5G Infrastructure". Track G promotes technology advancement to develop 5G communications for the US federal government & military.

- Adtran, the US-based networking & communications solutions provider, enables the building of full-fiber networks employing passive optical network technologies that provide gigabit access to businesses and homes and for infrastructure backhaul. In January 2023, the company established its SDX 6330 10 Gbit/s combo passive optical network fiber access platform, which allows service providers to cost-effectively and quickly connect businesses & homes with fiber-based broadband. The new solution provides the highest port density in the industry and is the foremost optical line terminal incorporated with 400 Gbit/s uplinks.

- Furthermore, the growing data consumption is also creating opportunities in the studied market by driving investment in new optical fiber cable networks which supports the data connectivity. For instance, in November 2022, Arelion, a Swedish connectivity provider, unveiled a plan to create two high-capacity fiber optic routes through Texas between Mexico & the United States. The new dense wavelength division multiplexing routes will meet the increasing demand for high-capacity, scalable bandwidth transport & simplify access to Mexico's local markets for over-the-top suppliers in the United States, Asia, and Europe.

Telecommunication End-user Industry Holds Significant Market Share

- Optical fiber cable (OFC) is a vital building block in the telecommunication infrastructure. Over the last decade, fiber optics have been catering to forceful bandwidth needs, especially from telecommunication companies, and have become the choice of transmission medium. The Studied regions have the presence of some of the biggest telecommunication companies, such as AT&T, Verizon, Sprint, Vodafone Group, etc., who are continuously expanding their optical fiber network to increase their global and regional presence, which creates opportunities in the studied market.

- The eruption of data traffic from different sources, like the internet, e-commerce, computer networks, and multimedia (voice, data, and video), has shown the requirement for a transmission medium capable of managing higher bandwidth to handle such vast amounts of information. According to Eurostat, the share of daily internet users in the European Union had increased to 84% in 2022, compared to 74.07% in 2028. As fiber-optic cables, with comparatively infinite bandwidth, are among the key solutions to this problem, the demand is anticipated to remain high.

- In telecommunication networks, fiber optic cables join different network nodes, like cell towers, data centers, and internet service providers, allowing the exchange of extensive amounts of data between different locations. Fiber-optic cables also have suitable for developing high-speed internet connections & other advanced communication technologies such as video conferencing, online gaming, and cloud computing. Hence, the expanding 5G network footprint in the United States and the European region is anticipated to drive opportunities in the studied market.

- Moreover, owing to their security, scalability, and the unlimited bandwidth potential to handle the vast amount of backhaul traffic being generated, fiber-optic cables are also being selected to support the bandwidth levels catering to evolved technologies like 5G, Big Data and IoT that rely heavily on real-time data gathering and transfer. The launch of 5G is predicted to improve the capacity and lower latency straight to networks.

- The internet has been one of the significantly transformative and fast-growing technologies in the studied regions which is driving opportunities in the studied market as optical fiber cables are widely used in the data and the telecommunication industry. For instance, according to Ericsson, datatraffic per smartphone continues to grow in the studied regions, for instance, in North America, data traffic per smartphone is anticipated to growth from 13 GB/month in 2021 to 58 GB/month in 2028. Similarly, in Western Europe, it is anticipated to grow from 16GB/month in 2021 to 56GB/month by 2028.

US & European Fiber Optic Cable Industry Overview

The United States and European fiber optic cable market is fragmented, with major players like Nexans SA, Prysmian Group, Weinert Industries AG, Coherent Corporation, and Sumitomo Corporation. Players in the market are embracing strategies like partnerships, acquisitions, and mergers to enhance their product offerings and gain sustainable competitive advantage.

- March 2023 - CommScope, a global network connectivity solution, announced expansions to its fiber-optic cable production to accelerate broadband rollout across the U.S., connecting more communities and underserved areas. According to the company, this initiative will increase fiber-optic cable output in the U.S., hastening broadband deployment to underserved communities. Additionally, the company's HeliARC lines are expected to support 500,000 homes per year in FTTH deployments.

- March 2023 - European Eunion announced obligations to equip buildings with fiber-optic cables in line with its 2030 policy program for the digital decade. As per the new regulation, it will be mandatory to keep passive infrastructure (mini ducts) and in-building fiber wiring (fiber optic cables) in newly contracted buildings or buildings undergoing major renovations, up to the network termination point in the apartment/unit. EU is also planning to provide certification to the buildings that are 'fiber ready. Such trends are anticipated to drive the demand for fiber optic cables.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of Key Macro-economic themes

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The Increased Data Traffic Creates the Demand for Fiber Optic Cable Network

- 5.1.2 Rising Investment in Fiber Optic and 5G Deployment

- 5.2 Market Challenges

- 5.2.1 Rising Demand For Wireless Solutions and Complex Installation Process

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Telecommunication

- 6.1.2 Power Utilities

- 6.1.3 Defence/military

- 6.1.4 Industrial

- 6.1.5 Medical

- 6.1.6 Other End-user Industries

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Germany

- 6.2.3 Austria and Switzerland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nexans SA

- 7.1.2 Prysmian Group

- 7.1.3 Weinert Industries AG

- 7.1.4 Coherent Corporation

- 7.1.5 Sumitomo Corporation

- 7.1.6 Corning Inc.

- 7.1.7 Finisar Corporation

- 7.1.8 Leoni AG

- 7.1.9 Folan

- 7.1.10 Molex LLC

- 7.1.11 Fujikura Ltd

- 7.1.12 Sterlite Technologies

- 7.1.13 Furukawa Electric Co. Ltd

- 7.1.14 Smiths Interconnect (Smiths Group PLC)