|

市場調査レポート

商品コード

1698565

光ファイバーケーブル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Fiber Optic Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| 光ファイバーケーブル市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月10日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

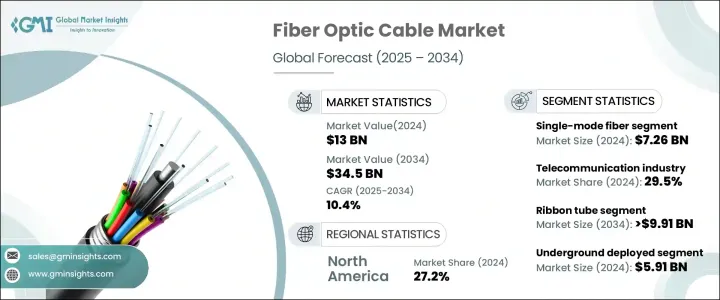

世界の光ファイバーケーブル市場は、2024年に130億米ドルと評価され、2025年から2034年にかけてCAGR 10.4%で成長すると予想されています。

高速接続に対する需要の高まり、5Gネットワークの拡大、データセンター展開の急増が、この成長の主な要因となっています。5G技術が世界的に拡大するにつれ、シームレスで低遅延の通信をサポートする堅牢なインフラの必要性が高まっています。ネットワークカバレッジを向上させるためにスモールセルの導入が増加していることから、効率的なバックホールとフロントホール接続を確保する光ファイバーケーブルの需要が高まっています。2030年までに56%を超えると予想される世界の5G普及率の上昇は、光ファイバーメーカーが最新の通信ネットワークをサポートするために、ケーブルの効率性、耐久性、トランスミッション速度を強化する原動力となっています。

データセンター事業の拡大も市場成長に貢献しており、通信会社やクラウドサービスプロバイダーは拡張性の高い広帯域インフラに多額の投資を行っています。光ファイバーケーブルは、データセンターが複雑なネットワーク需要を管理し、安全で高速な接続性を確保することを可能にします。電気通信とクラウドコンピューティングへの投資の増加に伴い、メーカーはハイパースケールデータセンターやエッジデータセンターの効率性と拡張性を高めるファイバー技術の革新に注力しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 130億米ドル |

| 予測金額 | 345億米ドル |

| CAGR | 10.4% |

市場はファイバータイプ別にシングルモードファイバーとマルチモードファイバーに区分されます。シングルモードファイバーは、優れた長距離データ転送機能を提供し、2024年には72億6,000万米ドルで市場をリード。マルチモードファイバはCAGR 8.5%で成長すると予測され、特にローカルエリアネットワークやデータセンターでの高速短距離通信用として人気を集めています。

産業別では、5Gネットワークにおける広帯域幅接続の需要増に牽引され、通信が2024年の市場シェアの29.5%を占め、優位を占めています。CAGR10.9%で拡大が予測される電力ユーティリティ業界では、スマートグリッドアプリケーション向けに光ファイバケーブルの採用が増加しています。市場シェア14.2%の防衛産業は、最新の通信システムやトランスミッションに不可欠な安全で高速なデータ伝送に光ファイバを利用しています。産業セグメントは、自動化とデジタルトランスフォーメーションイニシアチブの高まりに支えられて、2034年には73億4,000万米ドルを超えると見られています。CAGR8.2%の成長が見込まれる医療産業は、精密診断やイメージング技術に光ファイバを活用しています。

市場はケーブルタイプでも分類され、リボンチューブ光ファイバケーブルは、ファイバ密度が高いことから2034年には99億1,000万米ドルを超えると予測されています。ルースチューブケーブルは、2024年に43億5,000万米ドルで、長距離通信ネットワークに広く使用されています。一方、タイトバッファケーブルは、CAGR 9.8%で成長し、屋内アプリケーション向けに柔軟性が強化されています。2034年には41億9,000万米ドルに達すると予想される中央コアケーブルは、FTTH(Fiber-to-the-Home)やFTTB(Fiber-to-the-Building)の展開を通じてブロードバンドの拡大をサポートします。

配備の面では、地中光ファイバーケーブルが2024年に59億1,000万米ドルで首位に立ち、重要インフラに安全な接続性を提供しています。CAGR11.8%の成長が見込まれる水中セグメントは、大洋横断通信で重要な役割を果たしています。2034年には91億4,000万米ドルを超えると予測される空中配備は、コスト効率が高く、保守が容易なネットワーク拡張を提供します。

地域別では、北米が2024年に27.2%の市場シェアを占め、先進的なネットワーキング・ソリューションの急速な採用と、5Gインフラ整備を支援する政府の取り組みが牽引しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- ベンダー・マトリックス

- 利益率分析

- テクノロジーとイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- ブロードバンド普及率の増加

- 通信事業者の継続的拡大

- 高速インターネットへの需要の高まり

- データセンターの普及

- 5G技術の採用

- 業界の潜在的リスク&課題

- 高い導入・維持コスト

- 信号損失と減衰の克服

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:繊維タイプ別、2021年~2034年

- 主要動向

- シングルモードファイバー

- マルチモードファイバ

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- 地中

- 水中

- 空中

第7章 市場推計・予測:ケーブルタイプ別、2021年~2034年

- 主要動向

- リボンチューブ

- ルースチューブ

- タイトバッファード

- セントラルコア

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 通信業界

- 電力ユーティリティ

- 防衛/軍事

- 産業用

- 医療

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

- その他中東・アフリカ

第10章 企業プロファイル

- Belden Inc.

- Coherent Corporation

- CommScope Holding Company Inc.

- Corning Incorporated

- Encore Wire Corporation

- Finolex Cables Limited

- Fujikura Ltd.

- Furukawa Electric

- Hengtong Group Co., Ltd.

- Hexatronic Group AB

- LS Cable &System Ltd.

- Nexans S.A.

- Proterial Cable America Inc.(Proterial Ltd)

- Prysmian Group

- Sterlite Technologies

- Sumitomo Electric Industries Ltd

- Yangtze Optical Fiber and Cable Joint Stock Ltd Co.

The Global Fiber Optic Cable Market, valued at USD 13 billion in 2024, is expected to grow at a CAGR of 10.4% from 2025 to 2034. Rising demand for high-speed connectivity, the expansion of 5G networks, and the surge in data center deployments are key factors fueling this growth. As 5G technology expands worldwide, the need for robust infrastructure to support seamless, low-latency communication has intensified. The increasing adoption of small cell deployments for better network coverage has created a strong demand for fiber optic cables, which ensure efficient backhaul and fronthaul connectivity. The rise in global 5G penetration, expected to surpass 56% by 2030, is driving fiber optic manufacturers to enhance cable efficiency, durability, and transmission speeds to support modern telecommunication networks.

Expanding data center operations further contributes to market growth, with telecom firms and cloud service providers investing heavily in scalable, high-bandwidth infrastructure. Fiber optic cables enable data centers to manage complex networking demands, ensuring secure and high-speed connectivity. With increased investments in telecom and cloud computing, manufacturers are focusing on fiber technology innovations that enhance efficiency and scalability for hyperscale and edge data centers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13 Billion |

| Forecast Value | $34.5 Billion |

| CAGR | 10.4% |

The market is segmented by fiber type into single-mode and multi-mode fibers. Single-mode fiber led the market with USD 7.26 billion in 2024, offering superior long-distance data transfer capabilities. Multi-mode fiber, projected to grow at a CAGR of 8.5%, is gaining traction for high-speed, short-distance communication, particularly in local area networks and data centers.

By industry, telecommunications dominated in 2024, accounting for 29.5% of market share, driven by the growing demand for high-bandwidth connectivity in 5G networks. The power utilities sector, projected to expand at a CAGR of 10.9%, is seeing increased adoption of fiber optic cables for smart grid applications. The defense industry, with a 14.2% market share, relies on fiber optics for secure, high-speed data transmission, essential for modern communication and surveillance systems. The industrial segment is set to surpass USD 7.34 billion by 2034, supported by rising automation and digital transformation initiatives. The medical industry, expected to grow at a CAGR of 8.2%, leverages fiber optics for precision diagnostics and imaging technologies.

The market is also categorized by cable type, with ribbon tube fiber optic cables projected to exceed USD 9.91 billion by 2034 due to their high fiber density. Loose tube cables, valued at USD 4.35 billion in 2024, are widely used in long-haul telecom networks, while tight-buffered cables, growing at a CAGR of 9.8%, offer enhanced flexibility for indoor applications. Central core cables, expected to reach USD 4.19 billion by 2034, support broadband expansion through Fiber-to-the-Home (FTTH) and Fiber-to-the-Building (FTTB) deployments.

Deployment-wise, underground fiber optic cables led with USD 5.91 billion in 2024, providing secure connectivity for critical infrastructure. The underwater segment, expected to grow at a CAGR of 11.8%, plays a key role in transoceanic communication. Aerial deployments, forecasted to surpass USD 9.14 billion by 2034, offer cost-effective and easily maintainable network expansion.

Regionally, North America held a 27.2% market share in 2024, driven by the rapid adoption of advanced networking solutions and government initiatives supporting 5G infrastructure development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Vendor matrix

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increased broadband penetration

- 3.8.1.2 Continuous expansion of telecom companies

- 3.8.1.3 Growing demand for high-speed internet

- 3.8.1.4 Proliferation of data center

- 3.8.1.5 Adoption of 5G technologies

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High Implementation and maintenance cost

- 3.8.2.2 Overcoming signal loss and attenuation

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.10.1 Supplier power

- 3.10.2 Buyer power

- 3.10.3 Threat of new entrants

- 3.10.4 Threat of substitutes

- 3.10.5 Industry rivalry

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Fiber Type, 2021 - 2034 (USD Million)

- 5.1 Key Trends

- 5.2 Single-mode fiber

- 5.3 Multi-mode fiber

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 (USD Million)

- 6.1 Key Trends

- 6.2 Underground

- 6.3 Underwater

- 6.4 Aerial

Chapter 7 Market Estimates & Forecast, By Cable Type, 2021 - 2034 (USD Million)

- 7.1 Key Trends

- 7.2 Ribbon tube

- 7.3 Loose tube

- 7.4 Tight buffered

- 7.5 Central core

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Million)

- 8.1 Key Trends

- 8.2 Telecommunication

- 8.3 Power utilities

- 8.4 Defense/military

- 8.5 Industrial

- 8.6 Medical

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Belden Inc.

- 10.2 Coherent Corporation

- 10.3 CommScope Holding Company Inc.

- 10.4 Corning Incorporated

- 10.5 Encore Wire Corporation

- 10.6 Finolex Cables Limited

- 10.7 Fujikura Ltd.

- 10.8 Furukawa Electric

- 10.9 Hengtong Group Co., Ltd.

- 10.10 Hexatronic Group AB

- 10.11 LS Cable & System Ltd.

- 10.12 Nexans S.A.

- 10.13 Proterial Cable America Inc. (Proterial Ltd)

- 10.14 Prysmian Group

- 10.15 Sterlite Technologies

- 10.16 Sumitomo Electric Industries Ltd

- 10.17 Yangtze Optical Fiber and Cable Joint Stock Ltd Co.