アルミニウム鍛造- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Aluminium Forging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693687

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

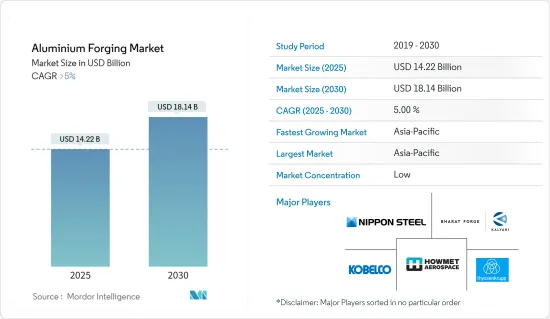

アルミニウム鍛造市場規模は、2025年に142億2,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは5%を超え、2030年には181億4,000万米ドルに達すると予測されています。

アルミニウム鍛造市場はCOVID-19による後退に直面しました。世界のロックダウンと厳しい政府規制により、生産拠点が広範囲にわたって閉鎖されました。しかし、市場は2021年に回復し、今後数年間は大幅な成長が見込まれます。

主要ハイライト

- 短期的には、産業セグメントでの軽量材料の使用拡大と自動車・輸送産業からの需要増加が、調査対象市場の需要を牽引する主要因です。

- しかし、アルミニウム価格の変動と厳しい品質基準が市場成長の妨げになると予想されます。

- 鍛造技術やシミュレーション技術の進歩は、同市場に新たな機会をもたらすと期待されています。

- アジア太平洋は、中国とインドからの需要が大半を占め、世界の市場を独占すると予想されます。

アルミニウム鍛造市場動向

自動車・輸送セグメントが市場を独占する

- アルミニウムは自動車セグメントで広く使用されています。エンジンラジエーター、ホイール、バンパー、サスペンション要素、エンジンシリンダーブロック、ギアボックスボディ、ボンネット、ドア、フレームを含むボディ部品などの部品に不可欠です。軽量性、耐久性、審美的な魅力で評価されるアルミニウムは、特に外装部品に好まれています。

- さらに、鍛造アルミニウム部品は自動車セグメントで極めて重要です。産業が燃費効率、軽量化、CO2排出量の抑制を重視する中、現代の自動車におけるアルミニウムの重要性は急上昇しています。アルミニウムを1kg使用するごとに車両重量が軽減されるため、自動車部品のアルミニウムへの依存度が高まり、市場の需要が高まっている

- アルミニウムの衝撃吸収能力は鋼鉄の2倍であるため、好まれる選択肢となっています。この効果により、メーカーはバンパーに一貫してアルミニウムを使用しています。さらに、アルミボディは安全性を高めています。アルミ部品が変形しても、全体の形態を維持するスチールとは異なり、変化は衝撃部分に局所化されるため、乗員の安全性が確保されます。

- 2023年、自動車産業は堅調な景気拡大と消費者の嗜好の進化に支えられ、大きな成長を遂げました。国際自動車製造者機構(OICA)のデータによると、乗用車と商用車を合わせた世界の自動車生産台数は約9,355万台でした。これは2022年の生産台数約8,483万台から顕著に増加し、成長率は約10.26%となります。

- 2023年には、アジア太平洋の商用車新車販売台数は2022年比で10.9%増加し、2022年の717万台に対して2023年には796万台が登録されました。

- しかし、インドでは、商用車(CV)販売台数は、24年度に2~5%の小幅な伸びを示した後、2024~25年度(25年度)は落ち込むと予測されています。ICRA(Investment Information and Credit Rating Agency of India Limited)のデータでは、25年度は4~7%の減少が見込まれています。

- 北米の2023年の自動車販売台数は1,919万台に達し、2022年の1,693万台から13.4%増加しました。その内訳は、乗用車が398万台、商用車が1,521万台、残りが大型トラック、バス、コーチです。

- さらに、欧州自動車工業会のデータによれば、2023年の欧州の新車登録台数は18.7%急増します。乗用車の販売台数は1,500万台、商用車は290万台に達し、それぞれ2022年の1,264万台、244万台から増加しました。

- 2024年第1四半期、英国の貿易産業は10万4,000件の商用車登録を記録し、前年同期比59%増という顕著な伸びを示しました。

- OICAのデータによると、ブラジルの2023年の小型商用車生産台数は42万2,000台で、前年比20%増となっており、市場の成長を裏付けています。

- さらに、サウジアラビアでは商用車市場の変革が見られます。経済の多様化とインフラの近代化に伴い、特にNEOMや紅海プロジェクトのようなメガプロジェクトが進行中で、先進的な商用車に対する需要が高まっている

- ビジョン2030の目標に向け、サウジアラビアの商用車セクタは急速に発展しています。米国・サウジアラビアビジネス評議会の予測によると、迅速なインフラ開拓と先進的物流ソリューションに対する需要の高まりにより、市場は2025年までに67億米ドルに達するといいます。

- このような力学を考えると、市場は予測期間中に大きく成長する準備が整っています。

アジア太平洋が市場を独占する

- アジア太平洋は、アルミ鍛造市場をリードし、予測期間中に最も急成長する地域となる見込みです。この急成長は、特に中国、インド、韓国、日本、様々な東南アジア諸国といった国々における、航空宇宙・防衛、自動車・輸送、産業機械、建設といったセグメントでの需要の高まりが主要因となっています。

- アルミニウム鍛造部品は高強度、軽量、耐食性に優れているため、高層ビルやオフィスタワーなどの高層建築物には欠かせないです。これらの部品は過酷な環境条件に耐えることができるため、メンテナンスや修理の必要性を最小限に抑えることができます。同地域の建設部門が拡大していることから、アルミニウム鍛造の需要は今後数年で増加するとみられます。

- 2030年までに都市化率70%を目指す中国の都市化推進は、住宅需要と中間層の生活水準向上への願望を強調しています。こうした動向は、住宅市場と住宅建設を活性化させ、アルミニウム鍛造市場に利益をもたらすことになります。

- 2024年、インドでは手頃な価格の住宅が70%増加すると予想されています。Invest Indiaによると、建設部門は2025年までに1兆4,000億米ドルの評価額を達成すると予測されています。2030年には人口の30%以上が都市居住者になるという予測もあり、2,500万戸以上の中級住宅と手頃な価格の住宅が急務となっています。不動産法、GST(物品サービス税)、REIT(不動産投資信託)などの最近の改革は、認可を迅速化し、建設産業を強化することを目的としており、市場の成長を促進しています。

- アルミニウム鍛造部品は航空宇宙セグメントで重要な役割を果たしており、機体、翼、制御面などの構造部品に使用されています。これらの部品は、エンジンや構造部品を軽量化することで、航空機や宇宙船の性能を高めています。この地域で航空宇宙部門が拡大するにつれて、アルミニウム鍛造の需要は伸びると予測されます。

- 中国は世界の航空宇宙セグメントで際立っており、航空機製造と国内航空旅行をリードしています。同国の航空機部品・組立部門は急速に拡大しており、200社以上の小規模部品メーカーを誇っています。

- 国際貿易局(ITA)のデータによると、中国は世界第2位の民間航空宇宙市場です。2024年1月現在、中国国家統計局と中国民用航空局の報告によると、民間航空機は7,351機で、2022年から550機以上増加しています。

- アルミニウム鍛造部品は、自動車の軽量化に極めて重要な役割を果たし、燃費を向上させ、排出ガスを抑制します。軽量化だけでなく、これらの部品は車体を軽量化し、シャーシを補強することで自動車の安全性を高めています。この地域での自動車生産が増加していることから、アルミニウム鍛造の需要は増加するとみられます。

- インドでは、インド自動車工業会(SIAM)のデータによると、2024年1月から3月までの乗用車、商用車、三輪車、二輪車、四輪車の生産台数は739万台に達しました。特に乗用車と商用車の販売台数は、それぞれ114万台と26万8,000台でした。

- アルミニウム鍛造は、その強度対重量比、耐食性、耐久性で珍重され、産業機械に広く応用されています。一般的な用途には、ギア、ギアボックス、ポンプ、バルブ、ベアリング、ブッシュなどがあります。産業機械の需要が増加するにつれて、アルミニウム鍛造の市場需要も増加すると考えられます。

- インド商務省のデータによると、2023会計年度の輸出額では、電気機械器具がトップで、酪農、食品加工、繊維用の産業機械が僅差で続き、80億米ドルを超えました。今後、電気機械設備の輸出は2024年度には124億米ドル近くに達すると予想されます。

- 鍛造アルミニウム部品は、軽量化とエネルギー消費の削減により、電子・計装部品の性能を向上させています。アジア太平洋ではエレクトロニクス部門が活況を呈しており、このセグメントにおけるアルミニウム鍛造の需要は拡大する傾向にあります。

- 日本電子情報技術産業協会のデータによると、日本のエレクトロニクス産業は2024年1月から6月までに5,452億5,600万円(約33億8,600万米ドル)相当の製品を生産し、前年同期比104.7%という著しい伸びを示しました。

- このような動態を考えると、アジア太平洋は予測期間中にアルミニウム鍛造需要が急増することになります。

アルミニウム鍛造産業概要

アルミニウム鍛造市場は細分化されています。主要企業(順不同)には、ハウメット・エアロスペース、バーラト・フォージ、ティッセンクルップAG、神戸製鋼所、新日本製鐵などが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 産業部門における軽量材料の使用拡大

- 自動車・輸送産業からの需要増加

- その他の促進要因

- 抑制要因

- アルミニウム価格の変動

- 厳しい品質基準

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 鍛造タイプ

- オープン型鍛造

- クローズダイ鍛造

- リングロール鍛造

- エンドユーザー産業

- 航空宇宙と防衛

- 自動車と輸送

- 産業機械

- 建設

- その他のエンドユーザー産業(電子・計測機器、エネルギーパワー、農業・農村)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Accurate Steel Forgings(INDIA)Limited

- Al Forge Tech Co., Ltd.

- All Metals & Forge Group

- Aluminum Precision Products

- Anchor Harvey

- Anderson Shumaker Company

- Bharat Forge

- Ellwood Group Inc.

- Howmet Aerospace

- ILJIN Co., Ltd.

- Kobe Steel, Ltd.

- Nippon Steel Corporation

- Norsk Hydro ASA

- Ramkrishna Forgings Ltd

- Scot Forge Company

- Thyssenkrupp AG

- Wheel India Limited

第7章 市場機会と今後の動向

- 先進鍛造技術とシミュレーション技術

- その他の機会

目次

The Aluminium Forging Market size is estimated at USD 14.22 billion in 2025, and is expected to reach USD 18.14 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The aluminum forging market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to see significant growth in the upcoming years.

Key Highlights

- Over the short term, the growing use of lightweight materials in the industrial sector and increasing demand from the automotive and transportation industries are the major factors driving the demand for the market studied.

- However, fluctuations in aluminum prices and stringent quality standards are expected to hinder the market's growth.

- Nevertheless, advanced forging techniques and simulation technologies is expected to create new opportunities for the market studied.

- Asia-Pacific region is expected to dominate the market across the world, with the majority of demand coming from China and India.

Aluminum Forging Market Trends

Automotive and Transportation Segment to Dominate the Market

- Aluminum is extensively used in the automotive sector. It's integral to components like engine radiators, wheels, bumpers, suspension elements, engine cylinder blocks, gearbox bodies, and body parts, including hoods, doors, and frames. Valued for its lightweight nature, durability, and aesthetic appeal, aluminum is especially favored for exterior components.

- Moreover, forged aluminum components are pivotal in the automotive realm. With the industry's emphasis on fuel efficiency, weight reduction, and curbing CO2 emissions, aluminum's significance in contemporary vehicles has surged. Every kilogram of aluminum reduces the vehicle's weight, prompting a growing reliance on aluminum for car parts and subsequently boosting market demand.

- Aluminum's shock-absorbing capabilities, being twice as effective as steel, make it a preferred choice. This efficacy has led manufacturers to use aluminum in bumpers consistently. Additionally, aluminum bodies offer enhanced safety; when aluminum parts deform, the change is localized to the impact area, unlike steel, which maintains the overall shape, ensuring passenger safety.

- In 2023, the automotive industry experienced significant growth, buoyed by robust economic expansion and evolving consumer preferences. Data from the Organisation Internationale des Constructeurs d'Automobiles (OICA) reveals a production of approximately 93.55 million units of vehicles worldwide, encompassing both passenger cars and commercial vehicles. This marked a notable uptick from the roughly 84.83 million units of vehicles produced in 2022, translating to a growth rate of about 10.26%.

- In 2023, the Asia Pacific region witnessed 10.9% increase in new commercial vehicle sales compared to 2022, with 7.96 million units registered in 2023, compared to 7.17million units in 2022.

- However, in India, commercial vehicle (CV) sales are projected to dip in the financial year 2024-25 (FY 25) after a modest 2-5% growth in FY24. As per the data from ICRA (Investment Information and Credit Rating Agency of India Limited) forecasts a 4-7% decline in FY25.

- North America saw motor vehicle sales reach 19.19 million units in 2023, a 13.4% rise from 2022's 16.93 million units, as reported by OICA. Of the total, passenger cars comprised 3.98 million units, commercial vehicles accounted for 15.21 million units, with the remainder being heavy trucks, buses, and coaches.

- Furthermore, as per the data from the European Automobile Manufacturers Association highlights an 18.7% surge in new motor vehicle registrations in Europe for 2023. Passenger car sales hit 15 million units, while commercial vehicles reached 2.90 million units, both up from 2022's 12.64 million and 2.44 million units, respectively.

- In the first quarter of 2024, the United Kingdom's trade industry recorded 104,000 commercial registrations, a notable 59% increase year-on-year, bolstered by the Ministry of Commerce's issuance of 65,363 permits in the same quarter of 2023.

- OICA data highlights Brazil's light commercial vehicle production at 422 thousand units in 2023, a 20% increase from the previous year, underscoring the market's growth.

- Moreover, Saudi Arabia is witnessing a transformation in its commercial vehicle market. As the nation diversifies its economy and modernizes its infrastructure, there's a growing demand for advanced commercial vehicles, especially with mega projects like NEOM and the Red Sea Project underway.

- Racing towards its Vision 2030 goals, Saudi Arabia's commercial vehicle sector is rapidly evolving. Projections suggest the market will reach USD 6.7 billion by 2025, driven by swift infrastructure developments and a rising demand for advanced logistics solutions, as per the U.S.-Saudi Arabian Business Council.

- Given these dynamics, the market is poised for significant growth during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is poised to lead the aluminum forging market, emerging as the region with the fastest growth during the forecast period. This surge is primarily fueled by rising demands in sectors like aerospace and defense, automotive and transportation, industrial machinery, and construction, particularly in nations such as China, India, South Korea, Japan, and various Southeast Asian countries.

- Owing to their high strength, lightweight nature, and corrosion resistance, forged aluminum parts are integral to high-rise buildings, including skyscrapers and office towers. These parts can endure harsh environmental conditions, minimizing maintenance and repair needs. With the region's construction sector expanding, the demand for aluminum forging is set to increase in the coming years.

- China's urbanization drive, targeting a 70% urban rate by 2030, underscores the demand for housing and the middle class's aspirations for improved living standards. These trends are poised to invigorate the housing market and residential construction, benefiting the aluminum forging market.

- In 2024, India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there's a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST (Goods and Services Tax) and REITs (Real Estate Investment Trusts), aim to expedite approvals and strengthen the construction industry, driving market growth.

- Forged aluminum parts play a crucial role in aerospace, being used in structural components like fuselages, wings, and control surfaces. These parts enhance aircraft and spacecraft performance by lightening engine and structural components. As the aerospace sector expands in the region, the demand for aluminum forging is projected to grow.

- China stands out in the global aerospace arena, leading in aircraft manufacturing and domestic air travel. The nation's aircraft parts and assembly sector is rapidly expanding, boasting over 200 small parts manufacturers.

- As per the data from the International Trade Administration (ITA), China is the second-largest civil aerospace market globally. As of January 2024, the National Bureau of Statistics of China and the Civil Aviation Administration of China reported 7,351 civil aircraft, an increase of over 550 airplanes from 2022.

- Forged aluminum parts play a pivotal role in reducing vehicle weight, which in turn boosts fuel efficiency and curtails emissions. Beyond weight reduction, these components enhance vehicle safety by lightening the body and reinforcing the chassis. Given the uptick in vehicle production in the region, the demand for aluminum forging is set to rise.

- In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three wheelers, two wheelers and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million and 268 thousand units, respectively.

- Aluminum forging finds extensive application in industrial machinery, prized for its strength-to-weight ratio, corrosion resistance, and durability. Common applications include gears, gearboxes, pumps, valves, bearings, and bushings. As demand for industrial machinery rises, so too will the market's demand for aluminum forging.

- Data from India's Department of Commerce highlights that in the 2023 fiscal year, electric machinery and equipment topped the export value charts, followed closely by industrial machinery for dairy, food processing, and textiles, exceeding USD 8 billion. Looking ahead, exports of electrical machinery and equipment are expected to reach nearly USD 12.4 billion in the 2024 fiscal year.

- Forged aluminum parts enhance the performance of electronic and instrumentation components by reducing weight and energy consumption. With the electronics sector booming in Asia-Pacific, the demand for aluminum forging in this domain is set to escalate.

- Data from the Japan Electronics and Information Technology Industries Association reveals that Japan's electronics industry produced goods worth JPY 5,452,56 million (~USD 3,386 million) from January to June 2024, marking a remarkable 104.7% growth compared to the same period the previous year.

- Given these dynamics, the Asia-Pacific region is poised for a surge in aluminum forging demand during the forecast period.

Aluminum Forging Industry Overview

The aluminum forging market is fragmented in nature. The major players (not in any particular order) include Howmet Aerospace, Bharat Forge, Thyssenkrupp AG, Kobe Steel, Ltd., and Nippon Steel Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Use of Lightweight Material in Industrial Sector

- 4.1.2 Increasing Demand from the Automotive and Transportation Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Fluctuations in Aluminum Prices

- 4.2.2 Stringent Quality Standards

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Forging Type

- 5.1.1 Open Die Forging

- 5.1.2 Close Die Forging

- 5.1.3 Ring Rolled Forging

- 5.2 End-User Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive and Transportation

- 5.2.3 Industrial Machinery

- 5.2.4 Construction

- 5.2.5 Other End-user Industries (Electronics and Instrumentation, Energy Power, Agriculture and Farming)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Accurate Steel Forgings (INDIA) Limited

- 6.4.2 Al Forge Tech Co., Ltd.

- 6.4.3 All Metals & Forge Group

- 6.4.4 Aluminum Precision Products

- 6.4.5 Anchor Harvey

- 6.4.6 Anderson Shumaker Company

- 6.4.7 Bharat Forge

- 6.4.8 Ellwood Group Inc.

- 6.4.9 Howmet Aerospace

- 6.4.10 ILJIN Co., Ltd.

- 6.4.11 Kobe Steel, Ltd.

- 6.4.12 Nippon Steel Corporation

- 6.4.13 Norsk Hydro ASA

- 6.4.14 Ramkrishna Forgings Ltd

- 6.4.15 Scot Forge Company

- 6.4.16 Thyssenkrupp AG

- 6.4.17 Wheel India Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advanced Forging Techniques and Simulation Technologies

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日