|

市場調査レポート

商品コード

1693664

アジア太平洋の燃料電池自動車:市場シェア分析、産業動向、成長予測(2025~2030年)Asia-Pacific Fuel Cell Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の燃料電池自動車:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 209 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

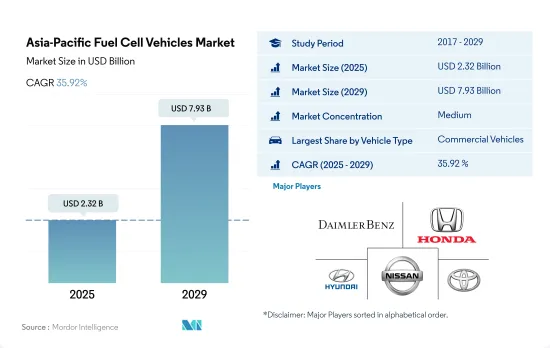

アジア太平洋の燃料電池自動車市場規模は、2025年に23億2,000万米ドルと推定され、2029年には79億3,000万米ドルに達すると予測され、予測期間中(2025~2029年)のCAGRは35.92%で成長する見込みです。

様々なタイプの車両に燃料電池技術を導入する同地域の先進的なアプローチを示し、輸送におけるクリーンエネルギー源としての水素の強い可能性を示す

- アジア太平洋は、サステイナブル輸送手段の急増を目の当たりにしており、それは多様なセグメントにわたる堅調な成長からも明らかです。乗用車から小型商用車、バン、中・大型トラック、バスに至るまで、この地域はグリーンモビリティを着実に取り入れています。特筆すべきは、乗用車セグメントにおける燃料電池電気自動車(FCEV)の販売台数の増加で、クリーン輸送の採用におけるこの地域のリーダーシップが強調されています。これらの販売台数は2017~2023年にかけて大幅に増加し、この動向は2030年まで続くと予測されます。

- 商用車セグメントでは、水素燃料電池技術への戦略的重点化によって、小型商用車と大型商用車の両セグメントが大幅な成長を遂げようとしています。小型商用車ピックアップトラックとバンの販売台数は、物流・輸送部門に合わせたゼロエミッション車へのシフトを示す顕著な急増を目の当たりにしています。この移行は、水素インフラへの投資と、二酸化炭素排出の抑制を目的とした政府のインセンティブによって後押しされています。

- FCEVを搭載したバスと並んで、中型と大型商用トラックも急速な成長軌道にあり、2030年までに販売台数は急増します。アジア太平洋におけるFCEVを取り巻く楽観論は、水素をベースとした経済への重要な動きを浮き彫りにしており、クリーンエネルギー導入の世界の先例を示しています。政府のイニシアティブ、技術的進歩、グリーン水素製造コストの低下は、この移行における極めて重要な要因であり、FCEVは商業輸送と旅客輸送の両方にとってますます魅力的なものとなっています。

アジア太平洋の燃料電池自動車市場は、特定の国が水素燃料技術採用に向けて先導しており、勢いを増しています。

- 輸送公害を抑制し、抑制するために、世界中の政府がグリーンエネルギーモビリティを採用するために行っているこれらのイニシアチブは、近い将来、燃料電池商用車市場を牽引すると予測される重要な要因の一つです。2019年11月、政府が支援する中国の企業で、トラック・バスメーカーのBeiqi Foton Motorは、燃料電池エンジンを含む代替エネルギー車に26億米ドルを投資すると発表しました。同社は2025年までに20万台の新エネルギー商用車を配備する計画です。

- いくつかの大手OEMメーカーは研究開発に多額の投資を行っており、商用車向けの技術を強化するために戦略的パートナーシップを結んでいます。2020年1月、日本の本田技研工業といすゞ自動車は、大型トラックの動力源として水素燃料電池を使用する研究を共同で実施すると発表し、ゼロエミッション技術を大型車に適用することで燃料電池の利用を拡大することを期待しています。このような開発は、アジア太平洋全域の電気商用車市場を強化すると予想されます。

- 2020年、韓国は電気自動車購入補助金を乗用車については2024年、バスとトラックについては2025年まで延長しました。ボーナスは価格上限と連動しています。6,000万ウォン以下のEVは全額補助を受けることができるが、6,000万ウォンから9,000万ウォンまでの車両は全額の50%しか受けることができないです。以前は1台当たり800万ウォンまで補助金が支給されていました。

アジア太平洋の燃料電池自動車市場動向

アジア太平洋の自動車ローン金利は各国の経済戦略を反映しており、景気刺激策を重視する国もあれば、より保守的な姿勢をとる国もあります。

- 過去数年間、これらの数字には顕著な変化がありました。インドネシアとインドは自動車ローン金利を顕著に引き下げたが、これは販売台数が変動する中で自動車部門を強化する潜在的な努力を示しています。日本は伝統に忠実に名目金利を維持したが、これは超金融緩和施策の持続を示す指標です。マレーシアは2021年に急落したが、2022年には足元を取り戻し、適応的な経済の再調整を示唆しました。一方、ニュージーランドとフィリピンは下降線をたどりました。タイは2020年に急落したが、2022年には再び上昇に転じた。オーストラリアの道のりは興味深く、毎年着実に上昇しているが、これはおそらく経済的回復力と戦略的乖離の融合を示しているのと考えられます。

- 2017~2023年にかけて、アジア太平洋は自動車ローンの金利変動のパノラマを見せた。インドネシアは、10%から11%の間で変動する最も急な金利で際立っており、その経済状況を明確に裏付けています。これとは対照的に、日本の金利は一貫して1%を下回っており、経済活動を促進するための長年の低金利施策を反映しています。オーストラリアとニュージーランドはより安定した動向で、2019年までに若干の引き上げが見込まれています。一方、フィリピンは、2017年に緩やかなベースからスタートしたもの、劇的な上昇を示し、2019年には7%を超えるピークに達しました。インドは安定したリズムを維持し、9~10%の範囲内にとどまり、マレーシアはわずかに上昇しました。逆にタイは緩やかな下降線をたどりました。

アジアにおける電気自動車(EV)需要の急増は、世界の自動車メーカーに新商品の投入を促し、EVとバッテリーパック市場の拡大をもたらしています。

- アジア太平洋における電気自動車(EV)需要の高まりを受け、多くの自動車メーカーが、この急成長する市場に合わせた革新的な製品を発表する戦略をとっています。2023年1月にシュコダが発表した、最先端の電気SUVをインドに導入する計画が重要な一例です。このクルマは82kWhという強力なバッテリーを搭載しており、1回の充電で500kmを超える航続距離を誇る。2023年後半に発売が予定されているシュコダの動きは、この地域を席巻している広範な動向を象徴しています。こうしたイントロダクションの導入は、EVの需要を喚起するだけでなく、アジア太平洋諸国におけるバッテリーパックの普及を促進することになります。

- アジア太平洋の都市生活において公共輸送がますます不可欠になるにつれ、新世代のメーカーが斬新でエコフレンドリーモデルをデビューさせる刺激となっています。2022年4月、インドを拠点とする新興企業の草分け的存在であるグリーンセル・モビリティは、電気モビリティ・バスのサービスブランド「NueGo」を発表しました。GreenCellは、インドの南部、北部、西部の3つの主要地域に750台のプレミアム電気バスを配備し、都市間通勤に革命を起こす計画です。初期段階では24都市に250台のバスを展開する予定だが、長期的なビジョンは、エコフレンドリー公共交通の強化に対する同社のコミットメントを強調するものです。このようなイニシアチブは、電気公共交通ソリューションの有望な急成長を示すものであり、今後数年間でアジア太平洋全域でより広範な採用が見込まれます。

アジア太平洋の燃料電池自動車産業概要

アジア太平洋の燃料電池自動車市場は、上位5社で60%を占めるほど、適度に統合されています。この市場の主要企業は、Daimler AG(Mercedes-Benz AG)、Honda Motor、Hyundai Motor Company、Nissan Motor、Toyota Motor Corporationなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 人口

- 一人当たりGDP

- 自動車購入のための消費者支出(cvp)

- インフレ率

- 自動車ローン金利

- シェアライド

- 電動化の影響

- EV充電ステーション

- バッテリーパック価格

- Xev新モデル発表

- 物流実績指数

- 中古車販売

- 燃料価格

- OEM生産統計

- 規制枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車種

- 商用車

- バス

- 大型商用トラック

- 小型商用ピックアップトラック

- 小型商用バン

- 中型商用トラック

- 商用車

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- タイ

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ballard Power Systems

- Daihatsu Motor Co. Ltd.

- Daimler AG(Mercedes-Benz AG)

- Dongfeng Motor Corporation

- Honda Motor Co. Ltd.

- Hyundai Motor Company

- Mazda Motor Corporation

- Nissan Motor Co. Ltd.

- Toyota Motor Corporation

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The Asia-Pacific Fuel Cell Vehicles Market size is estimated at 2.32 billion USD in 2025, and is expected to reach 7.93 billion USD by 2029, growing at a CAGR of 35.92% during the forecast period (2025-2029).

Demonstrates the region's advanced approach to implementing fuel cell technology in various vehicle types, indicating strong potential for hydrogen as a clean energy source in transportation

- The Asia-Pacific region is witnessing a surge in sustainable transportation, evident in its robust growth across diverse segments. From passenger cars to commercial vehicles, spanning light commercial pick-up trucks, vans, medium to heavy-duty trucks, and buses, the region is steadfastly embracing green mobility. Notably, the rising sales of fuel cell electric vehicles (FCEVs) in the passenger car segment highlight the region's leadership in adopting clean transportation. These sales saw a significant increase from 2017 to 2023, and the trend is projected to persist till 2030.

- In the commercial vehicle arena, both light and heavy-duty segments are poised for substantial growth, driven by a strategic emphasis on hydrogen fuel cell technology. Sales of light commercial pick-up trucks and vans have witnessed a remarkable surge, signaling a shift toward zero-emission vehicles tailored for the logistics and transportation sectors. This transition is bolstered by investments in hydrogen infrastructure and government incentives aimed at curbing carbon emissions.

- Medium and heavy-duty commercial trucks, alongside FCEV-powered buses, are also on a rapid growth trajectory, with sales volumes set to soar by 2030. The optimism surrounding FCEVs in the Asia-Pacific region underscores a significant move toward a hydrogen-based economy, setting a global precedent for clean energy adoption. Government initiatives, technological advancements, and the declining cost of green hydrogen production are pivotal factors in this transition, rendering FCEVs increasingly attractive for both commercial and passenger transportation.

The Asia-Pacific fuel cell vehicles market is gaining momentum, with specific countries leading the charge toward hydrogen fuel technology adoption

- These initiatives taken by governments across the world to adopt green energy mobility in order to curtail and curb transportation pollution are among the key factors that are projected to drive the fuel cell commercial vehicle market in the near future. In November 2019, the government-backed Chinese business, Beiqi Foton Motor, a truck and bus manufacturer, announced that it would invest USD 2.6 billion in alternative energy vehicles, including fuel cell engines. The company plans to deploy 200,000 new energy commercial vehicles by 2025.

- Several major OEM players are investing heavily in research and development, and they are entering strategic partnerships to enhance their technologies for commercial vehicles. In January 2020, Japan's Honda Motor and Isuzu Motors announced that they would jointly conduct research on the use of hydrogen fuel cells to power heavy-duty trucks, looking forward to expanding fuel-cell usage by applying zero-emission technology to larger vehicles. Such developments are expected to enhance the electric commercial vehicles market across Asia-Pacific.

- In 2020, South Korea extended the purchase subsidy for electric vehicles for passenger cars until 2024, and for buses and trucks, it was extended until 2025. The bonus is tied to a price cap. EVs priced below KRW 60 million are eligible for full subsidies, but vehicles priced between KRW 60 million and 90 million may receive only 50% of the full amount. Previously, up to KRW 8 million in subsidies were available per vehicle.

Asia-Pacific Fuel Cell Vehicles Market Trends

Asia-Pacific's auto loan interest rates reflected varying national economic strategies, with some countries emphasizing stimulation while others took a more conservative stance

- Over the past few years, there have been noticeable changes in these figures. Indonesia and India notably reduced their auto loan rates, signaling potential efforts to bolster the automotive sector in the face of fluctuating sales. Japan, adhering to its legacy, sustained its nominal rates, an indicator of its persistent ultra-loose monetary policy. Malaysia, after a sharp dip in 2021, seemed to regain its footing in 2022, hinting at an adaptive economic recalibration. New Zealand and the Philippines, meanwhile, navigated a descending path. Thailand, with a plunge in 2020, retraced some steps upward by 2022. Australia's journey was intriguing, with a steady climb each year, possibly indicating a blend of economic resilience and strategic divergence from its regional peers.

- During 2017-2023 period, Asia-Pacific showcased a panorama of fluctuating interest rates for auto loans. Indonesia stood out with the steepest rates oscillating between 10% and11%, clearly underlining its economic landscape. In stark contrast, Japan's rates remained consistently below 1%, reflecting its long-standing policy of low-interest rates to boost economic activity. Australia and New Zealand moved along a more stable trend with a slight increase by 2019. Meanwhile, the Philippines, though starting from a moderate base in 2017, marked a dramatic ascent, peaking over 7% in 2019. India maintained a steady rhythm, keeping within the 9-10% bracket, while Malaysia's course was slightly upward. Conversely, Thailand embraced a gentle downward slope.

The surging demand for electric vehicles (EVs) in Asia is prompting global automakers to introduce new offerings, thereby expanding the EV and battery pack market

- In response to the escalating demand for electric vehicles (EVs) in the Asia-Pacific region, numerous automakers are aligning their strategies to unveil innovative products tailored to this burgeoning market. One important instance is the announcement made by Skoda in January 2023, where it shared plans to introduce a cutting-edge electric SUV in India. This vehicle stands out due to its formidable 82-kWh battery, boasting an impressive range exceeding 500 kilometers on a singular charge. With its launch slated for late 2023, Skoda's move is emblematic of the broader trend sweeping across the region. Such introductions are poised to not only fuel the EV demand but also drive the proliferation of battery packs in various Asia-Pacific countries.

- As public transportation becomes increasingly integral to urban life in the Asia-Pacific, it is inspiring a new generation of manufacturers to debut novel, eco-friendly models. In a significant move in April 2022, the pioneering India-based startup, GreenCell Mobility, unveiled its electric mobility bus service brand, NueGo. GreenCell has plans to revolutionize intercity commutes by deploying 750 premium electric buses across three key regions in India, encompassing the South, North, and West. While the initial phase will witness the rollout of 250 buses across 24 cities, the long-term vision underscores the company's commitment to enhancing green public transportation. Such initiatives signal a promising surge in electric public transit solutions, setting the pace for broader adoption across Asia-Pacific in the coming years.

Asia-Pacific Fuel Cell Vehicles Industry Overview

The Asia-Pacific Fuel Cell Vehicles Market is moderately consolidated, with the top five companies occupying 60%. The major players in this market are Daimler AG (Mercedes-Benz AG), Honda Motor Co. Ltd., Hyundai Motor Company, Nissan Motor Co. Ltd. and Toyota Motor Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 GDP Per Capita

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.4 Inflation

- 4.5 Interest Rate For Auto Loans

- 4.6 Shared Rides

- 4.7 Impact Of Electrification

- 4.8 EV Charging Station

- 4.9 Battery Pack Price

- 4.10 New Xev Models Announced

- 4.11 Logistics Performance Index

- 4.12 Used Car Sales

- 4.13 Fuel Price

- 4.14 Oem-wise Production Statistics

- 4.15 Regulatory Framework

- 4.16 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Buses

- 5.1.1.2 Heavy-duty Commercial Trucks

- 5.1.1.3 Light Commercial Pick-up Trucks

- 5.1.1.4 Light Commercial Vans

- 5.1.1.5 Medium-duty Commercial Trucks

- 5.1.1 Commercial Vehicles

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Indonesia

- 5.2.5 Japan

- 5.2.6 Malaysia

- 5.2.7 South Korea

- 5.2.8 Thailand

- 5.2.9 Rest-of-APAC

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ballard Power Systems

- 6.4.2 Daihatsu Motor Co. Ltd.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Dongfeng Motor Corporation

- 6.4.5 Honda Motor Co. Ltd.

- 6.4.6 Hyundai Motor Company

- 6.4.7 Mazda Motor Corporation

- 6.4.8 Nissan Motor Co. Ltd.

- 6.4.9 Toyota Motor Corporation

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms