インドのトウモロコシ種子:市場シェア分析、産業動向、成長予測(2025~2030年)

India Maize Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693487

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

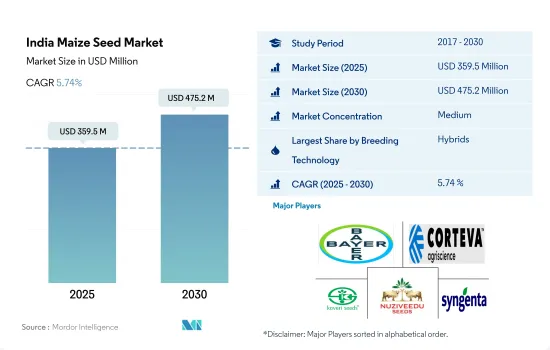

インドのトウモロコシ種子市場規模は2025年に3億5,950万米ドルと推定・予測され、2030年には4億7,520万米ドルに達し、予測期間(2025~2030年)のCAGRは5.74%で成長すると予測されます。

インドのトウモロコシ種子市場では、主にその高収量ポテンシャルと生物・生物的ストレス要因に対する回復力から、ハイブリッド種子が有力な選択肢として浮上しています。

- 2022年には、ハイブリッド種子がインドのトウモロコシ種子市場の65.8%を占め、残りの34.2%は開放受粉品種でした。ハイブリッド種子が好まれるのは、主にインドの大きな州で広く採用されているためです。

- ハイブリッドのトウモロコシは、2022年にはインドのトウモロコシ栽培面積の60%以上を占めました。このような高収量品種に対する需要の急増は、トウモロコシの家畜飼料としての利用の増加と、栄養強化食品に対する消費者の関心の高まりに後押しされています。

- インド商工会議所連合会(FICCI)によると、インドのトウモロコシ市場における交雑率は23%から100%です。ビハール州とタミル・ナードゥ州が100%のハイブリッド化率でリードしており、残りの地域では主に開放受粉の種子品種が栽培されています。

- ハイブリッドのトウモロコシは、均一な穂軸、病気、害虫、干ばつに対する抵抗性、優れた穀物品質、高い穂軸数など、いくつかの望ましい形質を示します。これらの特性は高い収量に貢献するため、ハイブリッドへの需要を牽引しています。

- Bioseedのような市場の主要企業は、需要の増加に対応するため、新しいハイブリッド品種を積極的に導入しています。2022年、Bioseedは最新のトウモロコシハイブリッド品種9792をインド市場に投入しました。

- 開放受粉品種は、ハイブリッド品種に比べて収量が低く、同じ種子の子孫が次のシーズンに使用されるため樹勢が低下するなどの制約があります。

- より高い収量、耐病性、ハイブリッド化の進行などを考慮すると、トウモロコシ市場におけるハイブリッド種子セグメントは予測期間中にCAGR 5.9%を記録すると予測されます。

インドのトウモロコシ種子市場の動向

良好な農業気候条件とトウモロコシ製品に対する旺盛な需要により、インドの栽培面積はアジア太平洋で第2位

- トウモロコシはインドの穀類作物ヒエラルキーにおいて、米、小麦に次いで第3位にランクされています。同国の食糧穀物生産の約10%を占めています。2021年には、インドは世界第5位のトウモロコシ生産国となり、世界生産量の2.6%に貢献しました。さらに、インドはアジア太平洋で2番目に大きなトウモロコシ栽培面積を有しており、同期間には1,000万ヘクタールがトウモロコシ栽培に充てられていました。トウモロコシ栽培は伝統的にカリフ期が中心だが、革新的な品種の台頭とエタノールなどトウモロコシ製品の需要急増により、冬期トウモロコシ栽培がますます現実的になっています。その結果、国内では2017~2022年にかけてトウモロコシ栽培面積が4.2%増加しました。

- 特筆すべきは、カルナータカ、マディヤ・プラデシュ、マハラシュトラ、ラジャスタン、ビハール、ウッタル・プラデシュ、テランガナ、グジャラート、タミル・ナードゥが2022年にインドの主要なトウモロコシ栽培地域に浮上し、合計でトウモロコシ総栽培面積の80%を占めるようになったことです。これらの地域の優位性は、トウモロコシ作物にとって良好な気象条件がトウモロコシ種子需要の高まりにつながったことに起因します。

- しかし、トウモロコシ栽培面積は40万ヘクタールの減少を経験し、2019年には900万ヘクタールに減少しました。このシフトは、生産者が大豆やキャノーラのような高収益作物に軸足を移したことが要因です。これらの油糧作物は悪天候に強く、石油加工産業からの需要が高まっているため、支持されました。

- 良好な農業気候条件とトウモロコシ製品に対する需要の高まりが、インドにおけるトウモロコシ栽培の拡大を後押ししています。この動向は今後数年間、同国におけるトウモロコシ種子販売を強化すると予想されます。

病害虫の蔓延が増加し、収量の大幅な減少につながることから、複数の形質を持つ改良型トウモロコシ品種へのニーズが高まっています。

- 生産者がトウモロコシの栽培を優先するのは、その収益性の高さと、特定の形質に対する需要のためです。これらの形質には、雑草防除、穀物品質の向上、早熟、宿根に対する耐性、葉巻病や初期腐敗病などの病害に対する耐性が含まれます。さらに、生産者は多様な農業気候条件への適応性を示すトウモロコシ品種を求めています。特筆すべきは、Bayer、BASF SE、シンジェンタといった企業が、耐病性と生産性を強化する形質を提供していることです。これらの種子品種は、耐病性のために利用可能な代替品や散布剤がないため、高い需要があります。

- インドではトウモロコシは重要な病害虫の課題に直面しており、主要病害虫は斑点茎立ち虫、ピンク茎立ち虫、シュート・フライ、秋期アーミーワームの4種類です。斑点カイガラムシは主にカリフ期に被害を受け、地域によって26%から80%の収量減につながります。同様に、ピンク色の茎虫はラビの季節に脅威となり、25.7%から78.9%の収量損失をもたらします。Corteva AgriscienceやBASF SEなどの企業は、これらの害虫に対抗するための害虫駆除製品を提供しています。

- 気象パターンの変化や宿根問題の増加に伴い、より広い適応性、宿根耐性、均一性、干ばつ耐性などの形質が支持を集めています。各社はこれに対応する新製品を積極的に投入しています。例えば、2023年には、DCMシュリラムの子会社であるバイオシードが、トウモロコシのハイブリッド 9792をインド市場で発売しました。

- 農業従事者は、損失を軽減し、収量を高め、病害虫に対する耐性を強化するために、改良された種子品種にますます目を向けるようになっています。

インドのトウモロコシ種子産業概要

インドのトウモロコシ種子市場は適度に統合されており、上位5社で56.72%を占めています。この市場の主要企業は、Bayer AG、Corteva Agriscience、Kaveri Seeds、Nuziveedu Seeds Ltd、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 州

- アンドラ・プラデシュ州

- ビハール州

- カルナータカ州

- マディヤ・プラデシュ州

- マハラシュトラ州

- ラジャスタン州

- タミルナドゥ州

- テランガナ

- ウッタル・プラデシュ州

- 西ベンガル州

- その他の州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Bayer AG

- Corteva Agriscience

- DCM Shriram Ltd(Bioseed)

- Groupe Limagrain

- Kaveri Seeds

- Nuziveedu Seeds Ltd

- Rasi Seeds Private Limited

- Syngenta Group

- VNR Seeds

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92550

The India Maize Seed Market size is estimated at 359.5 million USD in 2025, and is expected to reach 475.2 million USD by 2030, growing at a CAGR of 5.74% during the forecast period (2025-2030).

Hybrids have emerged as the dominant choice in the Indian maize seed market, primarily for their high-yield potential and resilience against biotic and abiotic stressors

- In 2022, hybrid seeds dominated the Indian maize seed market, accounting for 65.8% of its value, while open-pollinated varieties made up the remaining 34.2%. This preference for hybrids is primarily driven by their widespread adoption in larger Indian states.

- Hybrid maize occupied over 60% of India's total maize cultivation area in 2022. This surge in demand for high-yielding cultivars is fueled by maize's increasing use as animal feed and consumers' growing interest in nutritionally enhanced foods.

- According to the Federation of Indian Chambers of Commerce and Industry (FICCI), hybridization rates in the Indian maize market range from 23% to 100%. Bihar and Tamil Nadu lead the pack with 100% hybridization rates, while the remaining regions predominantly cultivate open-pollinated seed varieties.

- Hybrid maize exhibits several desirable traits, including uniform cobbs, resistance to diseases, pests, and drought, as well as superior grain quality and higher cob counts. These attributes contribute to their higher yields, thus driving the demand for hybrids.

- Key players in the market, like Bioseed, are actively introducing new hybrid varieties to meet the growing demand. In 2022, Bioseed launched its latest corn hybrid, 9792, in the Indian market.

- Open-pollinated varieties face limitations, such as lower yields compared to hybrids and reduced vigor, as the same seed offspring is used in subsequent seasons.

- Given their higher yields, disease resistance, and the ongoing trend of hybridization, the hybrid seed segment in the maize market is projected to register a CAGR of 5.9% during the forecast period.

India Maize Seed Market Trends

Owing to its favorable agro-climatic conditions and robust demand for corn products, India has the second-largest cultivation area in Asia-Pacific

- Corn ranks third in India's cereal crop hierarchy, after rice and wheat. It constituted approximately 10% of the country's food grain production. In 2021, India stood as the world's fifth-largest maize producer, contributing 2.6% to the global output. Additionally, India holds the second-largest maize cultivation area in Asia-Pacific, with 10 million hectares dedicated to maize in the same period. While the Kharif season traditionally dominates maize cultivation, the rise of innovative cultivars and surging demand for corn products, like ethanol, has made winter maize cultivation increasingly viable. Consequently, the country witnessed a 4.2% increase in maize cultivation area from 2017 to 2022.

- Notably, Karnataka, Madhya Pradesh, Maharashtra, Rajasthan, Bihar, Uttar Pradesh, Telangana, Gujarat, and Tamil Nadu emerged as India's primary maize-growing regions in 2022, collectively accounting for 80% of the total maize acreage. These regions' dominance is attributed to their favorable weather conditions for maize crops, leading to heightened demand for maize seeds.

- However, the maize cultivation area experienced a decline of 0.4 million hectares, dropping to 9 million hectares in 2019. This shift was driven by growers pivoting toward high-profit crops like soybean and canola. These oil crops gained favor due to their resilience in adverse weather and the rising demand from oil processing industries.

- Favorable agro-climatic conditions, coupled with the escalating demand for corn products, have been pivotal in driving the expansion of maize cultivation in India. This trend is expected to bolster maize seed sales in the country in the coming years.

The rising prevalence of pests and diseases, leading to significant yield losses, is fueling the need for enhanced maize varieties with multiple traits

- Growers prioritize cultivating corn due to its high profitability and their demand for specific traits. These traits include weed control, enhanced grain quality, early maturity, tolerance to lodging, and resistance to diseases like leaf curl and early rots. Additionally, growers seek corn varieties that exhibit adaptability to diverse agro-climatic conditions. Notably, companies like Bayer AG, BASF SE, and Syngenta offer traits that bolster disease resistance and productivity. These seed varieties are in high demand as there are no viable alternatives or sprays available for disease resistance.

- Maize faces significant pest challenges in India, with four major pests being the spotted stem borer, pink stem borer, shoot fly, and fall armyworm. The spotted stem borer predominantly affects crops during the Kharif season, leading to yield losses ranging from 26% to 80% across different regions. Similarly, the pink stem borer poses a threat during the Rabi season, causing yield losses between 25.7% and 78.9%. Companies like Corteva Agriscience and BASF SE offer insect control products to combat these pests.

- With changing weather patterns and an uptick in lodging issues, traits like wider adaptability, lodging tolerance, uniformity, and drought tolerance are gaining traction. Companies are actively introducing new products in response. For example, in 2023, Bioseed, a subsidiary of DCM Shriram, launched the corn hybrid 9792 in the Indian market.

- Farmers are increasingly turning to improved seed varieties to mitigate losses, boost yields, and enhance resistance against pests and diseases.

India Maize Seed Industry Overview

The India Maize Seed Market is moderately consolidated, with the top five companies occupying 56.72%. The major players in this market are Bayer AG, Corteva Agriscience, Kaveri Seeds, Nuziveedu Seeds Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 State

- 5.2.1 Andhra Pradesh

- 5.2.2 Bihar

- 5.2.3 Karnataka

- 5.2.4 Madhya Pradesh

- 5.2.5 Maharashtra

- 5.2.6 Rajasthan

- 5.2.7 Tamil Nadu

- 5.2.8 Telangana

- 5.2.9 Uttar Pradesh

- 5.2.10 West Bengal

- 5.2.11 Other States

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 DCM Shriram Ltd (Bioseed)

- 6.4.5 Groupe Limagrain

- 6.4.6 Kaveri Seeds

- 6.4.7 Nuziveedu Seeds Ltd

- 6.4.8 Rasi Seeds Private Limited

- 6.4.9 Syngenta Group

- 6.4.10 VNR Seeds

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

インドのトウモロコシ種子:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日