アジア太平洋のトウモロコシ種子:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Maize Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 224 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693467

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

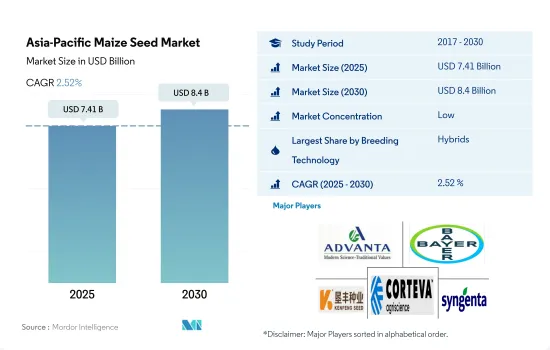

アジア太平洋のトウモロコシ種子市場規模は、2025年に74億1,000万米ドルと推定され、2030年には84億米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは2.52%で成長する見込みです。

病気に強い高品質種子品種への需要の高まりがアジア太平洋のハイブリッド種子を牽引

- アジア太平洋では、ハイブリッド種子が、露地受粉品種やハイブリッド派生品種と比較して、数量と金額でトウモロコシ種子市場を独占しています。2022年には、ハイブリッド種子がトウモロコシ種子市場の91.3%のシェアを占めました。この地域で生産されるトウモロコシのハイブリッド種子は、ウイルス性病害、細菌性病害、幅広い適応性、生物的ストレス耐性、色、高さ、穂軸あたりの粒数などの品質形質に耐性があります。

- ハイブリッド種子部門では、非遺伝子組み換えトウモロコシ種子が市場を独占し、2022年のシェアは83.3%でした。遺伝子組み換えトウモロコシの栽培は、中国、ベトナム、日本、パキスタンを除く多くの主要トウモロコシ生産国では承認されていないです。

- 2017~2022年にかけて市場は2.8%減少したが、これは中国やインドなどの主要国における栽培面積の減少や、同時期の不利な条件によるものです。例えば、中国とインドにおけるトウモロコシの栽培面積は、過去の期間にそれぞれ0.6%と2.6%減少しました。

- 2022年には、開放受粉品種とハイブリッド派生品種がトウモロコシ市場の8.7%を占め、ハイブリッド種子を下回りました。中国とインドが開放受粉品種の主要栽培国であり、葉腐病や細菌病などの病害に対する抵抗性が高くないため、同期間のシェアは67.8%です。さらに、開放受粉品種によるトウモロコシ栽培の大きな制約は、ハイブリッド品種に比べて収量が低く、生産性が低いことです。

- 高収量、病気に対する高い耐性、ハイブリッド化の増加といった主要因から、トウモロコシ市場におけるハイブリッド種子セグメントは予測期間中にCAGR 2.5%を記録すると予測されます。

中国は、ハイブリッド種子の採用率が高く、耕作面積が広いため、アジア太平洋のトウモロコシ種子市場で82.7%のシェアを占めました。

- トウモロコシはアジア太平洋で栽培されている主要作物の1つです。中国がこの地域のトウモロコシ種子市場をリードし、2022年には82.7%を占め、インド(4.4%)、インドネシア(3.7%)、フィリピン(2.2%)がこれに続きます。

- 中国では近年、黒龍江省、吉林省、河南省、内モンゴル自治区、山東省、河北省の主要生産省でトウモロコシの栽培面積が増加しています。2017年のトウモロコシ栽培面積は2,090万ヘクタールで、2022年には2,410万ヘクタールに増加しました。生産量は2017~2021年の間に2億5,700万トンから2億7,200万トン以上に増加しました。他の競合作物に比べてトウモロコシの採用が増加したため、同国ではトウモロコシ種子の需要が高まりました。

- インドはこの地域で2番目の主要トウモロコシ生産国です。インドでは、2021年のトウモロコシ生産量は3,016万トンを占め、商用ハイブリッドの高い使用率により前年比16.44%増となりました。同国で栽培されている一般的なハイブリッドは、P-3501、NK-6240、P-3396、JVM-421、African Tall、Narmada Moti、GM-6です。

- インドネシアの2021年のトウモロコシ生産量は1,200万トンです。ジャワ、スマトラ、スラウェシが同国の主要なトウモロコシ生産地域で、2022年の生産量の約90%を占めています。従って、これらの地域ではこれらの種子の販売がより多くなると推定されます。

- その他の主要なトウモロコシ生産国には、食品や飼料産業からの需要増加により、フィリピン、ベトナム、タイ、バングラデシュが含まれます。したがって、栽培面積の増加、ハイブリッドの採用率の上昇、加工産業からのトウモロコシ需要の増加が、トウモロコシ種子需要を牽引しています。このため、予測期間中、市場はCAGR 2.5%を記録すると予測されます。

アジア太平洋のトウモロコシ種子市場動向

工業用途、動物飼料と食品加工産業からの需要がトウモロコシ栽培を促進

- アジア太平洋は、世界的に主要なトウモロコシ生産地域の1つであり、各国の様々な加工食品産業で高い需要があります。2022年には、この地域のトウモロコシ栽培面積は6,760万ヘクタールに達しました。2022年の同地域のトウモロコシ栽培面積は、2021年と比較して1.1%増加しました。しかし、栽培面積は2017~2021年の過去に変動しました。この変動は、この地域の主要なトウモロコシ生産国のいくつかである中国、インド、インドネシアから生じた。

- 中国は、2022年のトウモロコシ栽培面積の64.7%を占め、主要なシェアを占めています。良好な気候条件と動物飼料としてのトウモロコシ需要の高さにより、この地域の主要国のひとつとなっています。さらに、トウモロコシの市場価格の上昇が、同国の農業従事者によるトウモロコシの採用を後押ししています。さらに、インドとインドネシアは、トウモロコシ栽培面積に関して中国に次ぐ主要国であり、2022年にはそれぞれ同地域の栽培面積の14.8%と5.2%を占めました。飼料、食品、エタノール工場などの加工産業からのトウモロコシの有利な市場価格が、これらの国々でのトウモロコシ栽培の採用を後押ししています。さらに、ガソリン混合におけるエタノール需要は、2019~20年の173兆リットルから2025~26年には1,016兆リットルに急増すると予測されています。その結果、エタノール需要全体は2019~20年の684兆リットルから2025~26年には1,500兆リットルに増加し、そのうち740兆リットルが穀物ベースのエタノールとなります。

- したがって、飼料用、食用、工業用トウモロコシの需要増は、予測期間中、同地域のトウモロコシ栽培面積を大幅に押し上げると予測されます。

干ばつ耐性、耐病性、幅広い適応性が、この地域の農業従事者が求める主要形質です。

- トウモロコシは高収益作物であるため、生産者によって栽培される重要な作物です。生産者は、雑草防除、穀物品質の向上、早熟、耐宿主性、耐病性、さまざまな地域や気候条件への適応性などの形質を強く好みます。例えば、BayerAG、BASF SE、シンジェンタなどの企業は、生産性を向上させ、初期腐敗病や葉の病気などの病気に対する抵抗性を高める形質を提供しています。これらの種子品種は、病害に抵抗するための他の散布剤や代替品が存在しないため、高い需要を目の当たりにしています。さらに、色、高さ、穂当たりの粒数といった他の主要形質も、生産者に高い利益をもたらすとして人気があります。

- 世界的に見て、中国はトウモロコシの主要生産国です。2022年は干ばつで水利用可能量が少なかったため、干ばつ耐性形質の需要が増加しています。したがって、予測期間中に干ばつに見舞われた国々の需要を満たすために、干ばつ耐性形質の需要が増加すると予想されます。さらに、生産者は土壌条件の変化や、ピンク茎虫、シュートフライ、斑点茎虫などの害虫からトウモロコシ作物を保護する需要により、より広い適応性、生物的ストレス耐性、耐虫性形質の採用も進めています。例えば、インドはアジア太平洋におけるとうもろこしの重要な生産国のひとつであり、この作物は害虫や生物的ストレスの影響を受け、さまざまな農業生態学的ゾーンで栽培されています。

- 気候条件による水不足、害虫、トウモロコシの成長に影響を与える病気などの要因は、新しい種子品種の導入と予測期間中の市場の成長に役立つと予想されます。

アジア太平洋のトウモロコシ種子産業概要

アジア太平洋のトウモロコシ種子市場はセグメント化されており、上位5社で28.84%を占めています。この市場の主要企業は、Advanta Seeds-UPL、Bayer AG、Beidahuang Kenfeng Seed、Corteva Agriscience、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 生産国

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Bayer AG

- Beidahuang Kenfeng Seed Co. Ltd

- Charoen Pokphand Group(CP Group)

- Corteva Agriscience

- DCM Shriram Ltd(Bioseed)

- Kaveri Seeds

- KWS SAAT SE & Co. KGaA

- Nuziveedu Seeds Ltd

- Syngenta Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92530

The Asia-Pacific Maize Seed Market size is estimated at 7.41 billion USD in 2025, and is expected to reach 8.4 billion USD by 2030, growing at a CAGR of 2.52% during the forecast period (2025-2030).

Increased demand for high-quality seed varieties with resistance to diseases is driving the hybrid segment in Asia-Pacific

- In Asia-Pacific, hybrid seeds dominated the maize seed market by volume and value compared to open-pollinated varieties and hybrid derivatives. In 2022, hybrid maize seeds held a 91.3% share of the maize seed market. Hybrid seeds produced in the region for maize are resistant to viral diseases, bacterial diseases, wider adaptability, abiotic stress tolerance, and quality traits such as color, height, and the number of grains per cob.

- In the hybrid seed segment, non-transgenic maize seeds dominated the market, with a share of 83.3% in 2022. The cultivation of transgenic maize is not approved in many major maize-producing countries, except China, Vietnam, Japan, and Pakistan.

- The market declined by 2.8% from 2017 to 2022 due to the decrease in the cultivation area in major countries such as China and India, as well as unfavorable conditions during the same period. For instance, the area of cultivation for corn in China and India decreased by 0.6% and 2.6% during the historical period, respectively.

- In 2022, open-pollinated varieties and hybrid derivatives accounted for 8.7% of the maize market, less than hybrid seeds. China and India are the major cultivators of open-pollinated varieties, with a share of 67.8% in the same period, as they are not highly resistant to diseases such as leaf rot and bacterial diseases. Moreover, a significant constraint in cultivating corn using open-pollinated seed varieties is that they provide lower yields and lower productivity than hybrids.

- Due to major factors such as high yield, high resistance to diseases, and an increase in hybridization, the hybrid seed segment in the maize market is projected to register a CAGR of 2.5% during the forecast period.

China dominated the Asia-Pacific maize seed market by accounting for an 82.7% share due to higher adoption of hybrids and a larger area under cultivation

- Maize is one of the major crops grown in Asia-Pacific. China leads the maize seed market in the region, accounting for 82.7% in 2022, followed by India (4.4%), Indonesia (3.7%), and the Philippines (2.2%).

- In China, there has been an increase in maize area in the major production provinces of Heilongjiang, Jilin, Henan, Inner Mongolia, Shandong, and Hebei in recent years. The acreage under maize cultivation was 20.9 million hectares in 2017, which increased to 24.1 million hectares in 2022. The production increased from 257 million metric ton to more than 272 million metric ton between 2017 and 2021. The increase in the adoption of maize compared to other competitive crops led to the rising demand for maize seeds in the country.

- India is the second major producer of maize in the region. In India, maize production accounted for 30.16 million metric ton in 2021, an increase of 16.44% compared to the previous year due to the high usage of commercial hybrids. The popular hybrids grown in the country are P-3501, NK-6240, P-3396, JVM-421, African Tall, Narmada Moti, and GM-6.

- Indonesia's maize production in 2021 was 12 million ton. Java, Sumatra, and Sulawesi are the major maize-growing areas in the country, which accounted for about 90% of production in 2022. Thus, the sales of these seeds are estimated to be higher in these areas.

- The other major maize-growing countries include the Philippines, Vietnam, Thailand, and Bangladesh due to the increasing demand from the food and feed industries. Therefore, the increase in the area, higher adoption of hybrids, and higher demand for maize from the processing industries drive the demand for maize seeds. Thus, the market is anticipated to register a CAGR of 2.5% during the forecast period.

Asia-Pacific Maize Seed Market Trends

Industrial applications, and the demand from animal feed and food processing industries are driving the maize cultivation

- Asia-Pacific is one of the major maize-producing regions globally, with a high demand in various processed food industries across its countries. In 2022, the region accounted for 67.6 million hectares of maize cultivation. The area under maize cultivation in the region observed an increase of 1.1% in 2022 compared to 2021. However, the acreage fluctuated during the historic period between 2017 and 2021. The fluctuation arose from China, India, and Indonesia, which are a few of the major maize-producing countries in the region.

- China occupied the major share of the area under maize cultivation, with 64.7% of the acreage in 2022. The favorable climatic conditions and the higher demand for maize as animal feed in the country have made it one of the major countries in the region. Moreover, the higher market prices for maize have driven its adoption by farmers in the country. Furthermore, India and Indonesia were the major countries after China concerning the area under maize cultivation, which accounted for 14.8% and 5.2% of the acreage in the region in 2022, respectively. The favorable market prices for maize from feed, food, and processing industries, such as ethanol plants, have driven the adoption of maize cultivation in these countries. Furthermore, the demand for ethanol in petrol blending is projected to surge from 173 crore liters in 2019-20 to 1,016 crore liters in 2025-26. Consequently, the overall demand for ethanol is set to rise from 684 crore liters in 2019-20 to 1,500 crore liters in 2025-26, with 740 crore liters being grain-based ethanol.

- Therefore, the increasing demand for corn for feed, human food, and industrial purposes is projected to drive the area under maize cultivation in the region significantly during the forecast period.

Drought tolerance, disease resistance, and wider adaptability are the major traits farmers seek in the region

- Corn is an important crop cultivated by growers because it is a high-profit crop. Growers have a high preference for traits such as weed control, improved grain quality, early maturity, lodging tolerance, disease resistance, and adaptability to different regions and climate conditions. For instance, companies such as Bayer AG, BASF SE, and Syngenta provide traits that help increase productivity and resistance to diseases such as early rots and leaf diseases. These seed varieties are witnessing high demand because no other sprays or alternatives exist to resist the diseases. Furthermore, other major traits, such as color, height, and the number of grains per cob, are popular for high returns for growers.

- Globally, China is a major producer of corn. The demand for drought tolerance traits is increasing because there was low water availability due to drought in 2022. Therefore, the demand for drought-tolerant traits is expected to increase to meet the demand of drought-affected countries during the forecast period. Moreover, the growers are also adopting wider adaptability, abiotic stress tolerance, and insect-resistant traits due to changes in soil conditions and demand for protecting corn crops from insects such as pink stem borer, shoot fly, and spotted stem borer. For instance, India is one of the significant producers of corn in Asia-Pacific, where the crop is affected by pests and abiotic stress and grown in different agroecological zones.

- Factors such as low water due to climatic conditions, pests, and diseases affecting the growth of corn are expected to help in the introduction of new seed varieties and the growth of the market during the forecast period.

Asia-Pacific Maize Seed Industry Overview

The Asia-Pacific Maize Seed Market is fragmented, with the top five companies occupying 28.84%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Beidahuang Kenfeng Seed Co. Ltd, Corteva Agriscience and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 Bangladesh

- 5.2.3 China

- 5.2.4 India

- 5.2.5 Indonesia

- 5.2.6 Japan

- 5.2.7 Myanmar

- 5.2.8 Pakistan

- 5.2.9 Philippines

- 5.2.10 Thailand

- 5.2.11 Vietnam

- 5.2.12 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Bayer AG

- 6.4.3 Beidahuang Kenfeng Seed Co. Ltd

- 6.4.4 Charoen Pokphand Group (CP Group)

- 6.4.5 Corteva Agriscience

- 6.4.6 DCM Shriram Ltd (Bioseed)

- 6.4.7 Kaveri Seeds

- 6.4.8 KWS SAAT SE & Co. KGaA

- 6.4.9 Nuziveedu Seeds Ltd

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アジア太平洋のトウモロコシ種子:市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 224 Pages

- 納期

- 2~3営業日