南米の種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

South America Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 435 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693472

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

南米の種子市場規模は2025年に87億8,000万米ドルと推定・予測され、2030年には119億4,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは6.33%で成長すると予測されます。

食品や飼料産業など、さまざまな用途で承認された遺伝子組み換え種子の数が最も多く、特にトウモロコシやアルファルファなどの連作作物の成長に貢献すると予想されます。

- 2022年、南米の種子市場ではハイブリッド種子が大きなシェアを占めています。生産者は高い利益と高い収量を得るためにハイブリッド種子を好むからです。南米では、トウモロコシ、ダイズ、アルファルファなどの高収益作物の栽培が承認されているため、遺伝子組み換えハイブリッド種子のシェアが大きいです。

- トウモロコシは高収益作物であり、生産者は栄養価の高い高収量と、異なる土壌や気象条件に素早く適応する種子を求めているため、ハイブリッド種子の中で最大の作物分野です。さらに、バイオ燃料生産における使用量の増加が、ハイブリッドトウモロコシ種子の採用に役立っています。

- 小麦は、ロシアとウクライナの戦争により欧州とアフリカの他の国々に輸出されているため、南米のハイブリッド種子市場においてCAGR 9.9%で最も急成長しているサブセグメントであると推定・予測されます。また、欧州諸国はピザのベースを作るために小麦を使用しています。そのため、小麦種子の需要はより速い速度で成長すると予想されます。

- アルファルファは、南米では遺伝子組換え種子と非遺伝子組換え種子の両方の栽培が承認されているため、予測期間中のCAGRは3.1%で、最も急成長している飼料セグメントの1つになると予測されます。高タンパク質で家畜が消化しやすいため、飼料として利用されています。また、除草剤耐性があり、雑草から保護することができます。従って、これらの用途はアルファルファの売上増加に貢献すると予想されます。

- ハイブリッド分野は、病気や害虫に対する耐性が高く、適応性が広いため、予測期間中のCAGRは6.6%と予想され、この地域で成長すると予測されています。

改良種子の入手可能性と作物増産のための新技術によりブラジルが南米の種子市場を独占

- 2022年、南米は世界の種子市場の11.1%を占めました。これは、この地域が豊富な天然資源、多様な気候、技術導入、世界の輸出の可能性を持っているためです。こうした需要の高まりが、同地域の種子市場を牽引しています。

- 2022年の南米の種子市場に占める保護栽培セグメントの割合はわずか0.01%に過ぎないが、これは中規模・小規模農家が高額な初期投資を行えないこと、南米諸国では新たな温室構造の設置に対する政府の支援がないことによる。そのため、予測期間中は保護栽培分野の成長が抑制される可能性があります。

- 南米では2023年から2030年にかけて、ハイブリッドの採用率が開放受粉種子品種よりも急速に伸びると推定されます。その理由は、ハイブリッドは収量を10%~15%増加させる能力があり、品質が良く、投資に対するリターンの質が高いからです。

- ブラジルは、改良種子の入手可能性、同国で栽培されるトウモロコシやトマトなどの収益性の高い作物、作物増産のための新技術により、南米をリードする国となっています。そのため、南米では予測期間中にCAGR 7.4%で市場が拡大すると予測されています。2022年、アルゼンチンは南米の種子市場の20.8%を占めました。アルゼンチンは農業の新興国であり、良質な作物を栽培する農家の需要を満たすために種子の需要が増加します。

- したがって、収量の増加、新技術、低金利で融資を提供する政府の取り組みなどの前述の要因は、予測期間中に南米の種子市場を増強すると予想されます。

南米の種子市場動向

油糧種子が南米の連作作物種子市場を独占し、大豆が主要な貢献者です。

- 南米では連作作物の栽培面積が圧倒的に多く、2022年には栽培面積の95%以上を占める。この地域で栽培されている主な連作作物は、大豆、トウモロコシ、小麦、豆類、アルファルファ、米です。2022年には、油糧種子が連作作物分野で44.1%の主要シェアを占める。さらに、列作物の栽培面積は、小麦、トウモロコシ、大豆の作付面積の増加により、2017年から2022年にかけて16.7%増加しました。世界的には、南米が最大の大豆生産国であり、大豆の作付面積は6,170万ヘクタール、2021年の生産量は1億9,680万トンでした。大豆の作付面積が大きいのは、輸出額の増加、石油加工産業からの世界の需要の高さ、他の主要生産国に比べて耕地が確保できること、利益率が高いことなどによる。

- ブラジルは、トウモロコシや大豆などさまざまな畑作物を栽培している主要国です。2022年には、この地域の連作作物栽培面積の53%を占めました。連作作物の栽培面積が増加しているのは、飲食品産業からの需要が増加していることと、トウモロコシを使ったバイオ燃料生成の需要が高いためです。さらに、トウモロコシはこの地域で栽培されている主要作物です。2022年には南米の連作作物栽培面積の27.6%を占めました。2017年から2022年にかけてトウモロコシの栽培面積は34.1%増加したが、これはトウモロコシが世界的に最も消費される作物のひとつであり、トウモロコシを利用した石油生成産業からの需要が増加したためです。

- 石油生成の需要、大豆を中心とする油糧種子の高い輸出ポテンシャル、世界市場におけるバイオ燃料生成の需要増加が、予測期間中に畑作物の栽培面積を増加させています。

南米では病害が作物の生産性と農業の持続可能性に大きな影響を与えるため、耐病性と除草剤耐性がトウモロコシと小麦の栽培で人気の形質です。

- トウモロコシと小麦は、南米地域で栽培されている主要な穀物です。これらの高収益作物は、国内消費と他国への輸出に利用されています。この地域、特にブラジルでは、除草剤耐性のトウモロコシ種子が広く栽培されています。これらの種子はグリホサートに耐性があり、広範囲の雑草を防除し、収量と品質を向上させる。バイエル、Limagrain、Corteva Agriscienceなどの大手企業は、このような除草剤耐性品種を提供しており、中でもDekalbはバイエルの人気ブランドです。除草剤耐性に加え、この地域の農家は、さまざまな生育条件に適応しやすいトウモロコシ品種を好みます。これらの種子は、穀物、飼料、初期腐敗病や葉の病気に対する耐性という2つの役割を果たします。

- 小麦もまた、南米で広く栽培されている主要な主食用穀物です。この地域の農家は主に、セプトリア、フザリウム、さび病などの病害に耐性のある小麦品種を栽培し、作物の損失を最小限に抑え、生産性の高い蘖(ひこばえ)と穂軸を確保しています。2020年、アルゼンチン政府は遺伝子組み換え(GM)小麦の栽培を承認し、2020年にはブラジルもGM小麦の栽培を承認しました。Bioceres社が開発したHB4干ばつ耐性品種は、アルゼンチンで55,000ヘクタールをカバーし、2021年の小麦栽培面積全体の0.85を占めました。

- この地域で人気のある他の小麦形質には、高い耕うん能力、様々な気候条件への適応性、高い製粉品質などがあります。したがって、輸出需要の増加と遺伝子組み換え品種の開発など育種技術の進歩により、2023~2030年の間に複数の形質を持つ小麦とトウモロコシの品種に対する需要が増加すると予測されます。

南米の種子産業の概要

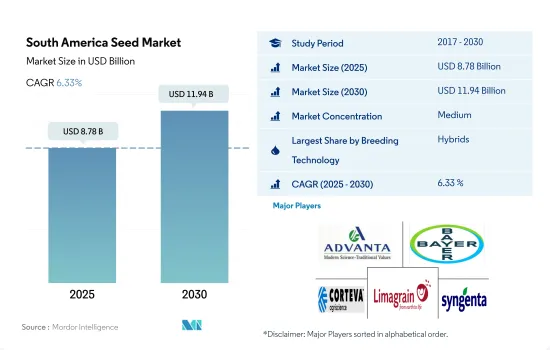

南米の種子市場は適度に統合されており、上位5社で40.76%を占めています。この市場の主要企業は以下の通りです。 Advanta Seeds-UPL, Bayer AG, Corteva Agriscience, Groupe Limagrain and Syngenta Group(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 野菜

- 最も人気のある品種

- トウモロコシと小麦

- タマネギ&レタス

- 大豆&アルファルファ

- トマト、カボチャ、スカッシュ

- 育種技術

- 畑作物および野菜

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 作物タイプ

- 畑作物

- 繊維作物

- 綿花

- その他の繊維作物

- 飼料作物

- アルファルファ

- 飼料用トウモロコシ

- 飼料用ソルガム

- その他の飼料作物

- 穀物・穀類

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物

- 油糧種子

- キャノーラ、菜種、マスタード

- 大豆

- ひまわり

- その他の油糧種子

- 豆類

- 豆類

- 野菜

- アブラナ

- キャベツ

- ニンジン

- カリフラワー&ブロッコリー

- その他のアブラナ

- ウリ科

- キュウリ・ガーキン

- カボチャ・スカッシュ

- その他ウリ科

- 根菜・球根

- ニンニク

- タマネギ

- ジャガイモ

- その他の根菜類

- ナス科

- 唐辛子

- ナス科

- トマト

- その他ナス科

- 分類されていない野菜

- アスパラガス

- レタス

- オクラ

- エンドウ豆

- ほうれん草

- その他分類されていない野菜

- 畑作物

- 生産国

- アルゼンチン

- ブラジル

- その他南米

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Corteva Agriscience

- DLF

- Groupe Limagrain

- KWS SAAT SE & Co. KGaA

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Sakata Seeds Corporation

- Syngenta Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92535

The South America Seed Market size is estimated at 8.78 billion USD in 2025, and is expected to reach 11.94 billion USD by 2030, growing at a CAGR of 6.33% during the forecast period (2025-2030).

Highest number of GM seeds approved with different applications such as food and animal feed industry is anticipated to help the growth of row crops, especially corn and Alfalfa

- In 2022, hybrids had a larger share in the South American seed market as growers prefer hybrids to earn high profits and obtain higher yields. South America has a larger share of transgenic hybrid seeds due to highly profitable crops such as corn, soybean, and alfalfa approved for cultivation in the region.

- Corn is the largest crop segment among hybrids as it is a high-profit crop, and growers want a higher yield with a high nutritional value and seeds that adapt quickly to different soil and weather conditions. Moreover, the higher usage in biofuel production is helping in the adoption of hybrid corn seeds.

- Wheat is estimated to be the fastest-growing sub-segment in the South American hybrid seed market at a CAGR of 9.9% during the forecast period as it is exported to other countries in Europe and Africa due to the war between Russia and Ukraine. European countries also use wheat to make pizza bases. Therefore, the demand for wheat seeds is expected to grow at a faster rate.

- Alfalfa is projected to be one of the fastest-growing forage segments at a CAGR of 3.1% during the forecast period, as both transgenic and non-transgenic seeds are approved for cultivation in South America. It is used as feed due to its high protein content and is easily digestible by livestock. It has herbicide tolerance that offers protection against weeds. Therefore, these uses are anticipated to help in increasing the sales of Alfalfa.

- The hybrids segment is projected to grow in the region, with an anticipated CAGR of 6.6% during the forecast period because of higher resistance to diseases and pests and wider adaptability.

Brazil dominates the South American seed market due to availability of improved seeds and new technology to increase the production of crops

- In 2022, South America accounted for 11.1% of the global seed market. This is because the region has abundant natural resources, diverse climates, technological adoption, and global export potential. This growing demand is driving the seed market in the region.

- The protected cultivation segment accounted for only 0.01% of the South American seed market in 2022 because medium-scale and small farmers cannot have a high initial investment, and there is no government support for setting up new greenhouse structures in South American countries. Therefore, it can restrain the growth of the protected cultivation segment during the forecast period.

- South America's adoption rate of hybrids is estimated to grow faster than open-pollinated seed varieties between 2023 and 2030 because of their ability to increase the yield by 10%-15%, good quality, and better quality return on investment.

- Brazil is the leading country in South America because of the availability of improved seeds, highly profitable crops such as corn and tomato grown in the country, and new technology to increase the production of crops. Therefore, it is anticipated that the market will increase during the forecast period in South America with a CAGR of 7.4%. In 2022, Argentina accounted for 20.8% of the South American seed market. Argentina is emerging in agriculture, which will increase the demand for seeds to meet the demand of farmers to grow good-quality crops.

- Therefore, the aforementioned factors, such as higher yield, new technologies, and government initiatives to provide loans at low-interest rates, are anticipated to augment the South American seed market during the forecast period.

South America Seed Market Trends

Oilseeds dominate South America row crops seed market, with soybean as the major contributor, driven by high export demand from oil processing as well as food and beverage industries

- In South America, row crops dominated the acreage under cultivation, accounting for more than 95% of the cultivated area in 2022. The major row crops cultivated in the region are soybean, corn, wheat, pulses, alfalfa, and rice. In 2022, oilseeds held a major share of 44.1% in the row crops segment. Additionally, the area under row crops increased by 16.7% from 2017 to 2022 due to increased wheat, corn, and soybean acreages. Globally, South America is the largest producer of soybeans, and the area under soybeans was 61.7 million hectares, with a production of 196.8 million metric tons in 2021. The major area under soybean is due to increased export value, high global demand from oil processing industries, availability of arable land compared to other major producing countries, and higher profit margins.

- Brazil is the major country cultivating different field crops, such as corn and soybeans. It accounted for 53% of the region's area used to cultivate row crops in 2022. The higher area under row crops is due to the increased demand from food and beverage industries and the high demand for bio-fuel generation using corn. Furthermore, corn is the major crop cultivated in the region. It accounted for 27.6% of South America's area for row crops in 2022. There was a 34.1% increase in the cultivated area for corn from 2017 to 2022 as it was one of the most consumed crops globally, and due to an increase in demand from corn-based oil-generating industries.

- The demand for oil generation, the high export potential of oilseeds, especially soybean, and the increasing demand for bio-fuel generation in the global market are increasing the area of cultivation for field crops during the forecast period.

Disease resistant and herbicide-tolerant are the popular traits in South America corn and wheat cultivation due to the significant impact of diseases on crop productivity and agricultural sustainability in the region.

- Corn and wheat are the major cereal crops grown in the South American region. These highly profitable crops are used for domestic consumption and export to other countries. In the region, especially in Brazil, herbicide-tolerant corn seeds are extensively cultivated. These seeds are tolerant to glyphosate, which helps control broad-spectrum weeds and improves yields and quality. Major companies like Bayer, Limagrain, and Corteva Agriscience offer such herbicide-tolerant varieties, with Dekalb being a popular brand from Bayer. In addition to herbicide tolerance, farmers in the region prefer corn varieties that are more adaptable to different growing conditions. These seeds serve dual purposes: grain, fodder, and resistance to early rots and leaf diseases.

- Wheat is another major staple cereal grain widely cultivated in South America. Farmers in the region mainly cultivate wheat cultivars resistant to diseases like Septoria, Fusarium, and rust to minimize crop losses and ensure productive tillers and panicles. In 2020, Argentina's government approved the cultivation of genetically modified (GM) wheat, and in 2020, Brazil also approved GM wheat cultivation. The HB4 drought-tolerant varieties, developed by Bioceres company, covered 55,000 hectares in Argentina and accounted for 0.85 of the total wheat cultivated area in 2021.

- Other popular wheat traits in the region include high tillering capacity, adaptability to various climatic conditions, and high milling quality. Therefore, with increasing export demand and advancements in breeding technology, such as the development of transgenic varieties, the demand for wheat and corn cultivars with multiple traits is projected to increase during 2023-2030.

South America Seed Industry Overview

The South America Seed Market is moderately consolidated, with the top five companies occupying 40.76%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Corteva Agriscience, Groupe Limagrain and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.1.2 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Corn & Wheat

- 4.2.2 Onion & Lettuce

- 4.2.3 Soybean & Alfalfa

- 4.2.4 Tomato, Pumpkin & Squash

- 4.3 Breeding Techniques

- 4.3.1 Row Crops & Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Type

- 5.3.1 Row Crops

- 5.3.1.1 Fiber Crops

- 5.3.1.1.1 Cotton

- 5.3.1.1.2 Other Fiber Crops

- 5.3.1.2 Forage Crops

- 5.3.1.2.1 Alfalfa

- 5.3.1.2.2 Forage Corn

- 5.3.1.2.3 Forage Sorghum

- 5.3.1.2.4 Other Forage Crops

- 5.3.1.3 Grains & Cereals

- 5.3.1.3.1 Corn

- 5.3.1.3.2 Rice

- 5.3.1.3.3 Sorghum

- 5.3.1.3.4 Wheat

- 5.3.1.3.5 Other Grains & Cereals

- 5.3.1.4 Oilseeds

- 5.3.1.4.1 Canola, Rapeseed & Mustard

- 5.3.1.4.2 Soybean

- 5.3.1.4.3 Sunflower

- 5.3.1.4.4 Other Oilseeds

- 5.3.1.5 Pulses

- 5.3.1.5.1 Pulses

- 5.3.2 Vegetables

- 5.3.2.1 Brassicas

- 5.3.2.1.1 Cabbage

- 5.3.2.1.2 Carrot

- 5.3.2.1.3 Cauliflower & Broccoli

- 5.3.2.1.4 Other Brassicas

- 5.3.2.2 Cucurbits

- 5.3.2.2.1 Cucumber & Gherkin

- 5.3.2.2.2 Pumpkin & Squash

- 5.3.2.2.3 Other Cucurbits

- 5.3.2.3 Roots & Bulbs

- 5.3.2.3.1 Garlic

- 5.3.2.3.2 Onion

- 5.3.2.3.3 Potato

- 5.3.2.3.4 Other Roots & Bulbs

- 5.3.2.4 Solanaceae

- 5.3.2.4.1 Chilli

- 5.3.2.4.2 Eggplant

- 5.3.2.4.3 Tomato

- 5.3.2.4.4 Other Solanaceae

- 5.3.2.5 Unclassified Vegetables

- 5.3.2.5.1 Asparagus

- 5.3.2.5.2 Lettuce

- 5.3.2.5.3 Okra

- 5.3.2.5.4 Peas

- 5.3.2.5.5 Spinach

- 5.3.2.5.6 Other Unclassified Vegetables

- 5.3.1 Row Crops

- 5.4 Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 DLF

- 6.4.6 Groupe Limagrain

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.9 Sakata Seeds Corporation

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

南米の種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 435 Pages

- 納期

- 2~3営業日