アルファルファ種子:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Alfalfa Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 415 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693449

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

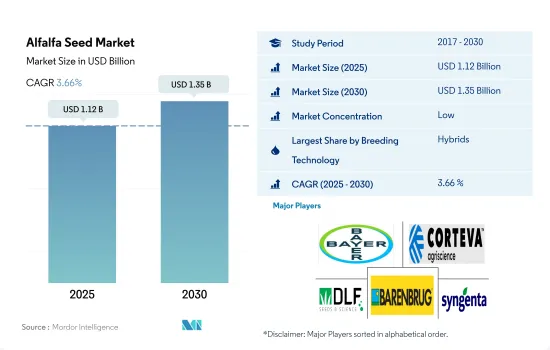

アルファルファ種子市場規模は2025年に11億2,000万米ドルと推定・予測され、2030年には13億5,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは3.66%で成長する見込みです。

耐病性などの改良された形質によるハイブリッド種子の採用増加が市場を牽引しています。

- 家畜人口は世界の様々な地域で増加しています。家畜頭数の増加には飼料栽培面積の拡大が必要であり、アルファルファは消化しやすい繊維質を提供しています。これらは、ハイブリッドと露地受粉アルファルファ種子市場の成長につながる主要因の一部です。

- ハイブリッド品種の採用が増加し、その利点についての認識が高まっているため、ハイブリッドセグメントがアルファルファ種子市場のトップに立っています。ハイブリッドアルファルファ種子市場規模は、予測期間終了までに約35.9%増加し、11億米ドルに達すると予測されます。これは、種子交換率の上昇と市場における改良品種の入手可能性によるものです。

- 干ばつ耐性や耐病性など、先進的なハイブリッド技術が生産者に受け入れられつつあることが、今後数年間のハイブリッドアルファルファ種子市場の成長に寄与すると予測されます。例えば、米国では2022年に業務用種子の栽培面積の99%をハイブリッド種子が占めるようになったが、これは高収量のハイブリッド品種が入手可能になったことと、Allied Seed LLC、Bayer AG、DLFといった人気企業が遺伝子組み換えアルファルファ品種を開発したことに起因しています。

- アフリカはOPVセグメントでCAGR 3.2%と最も急成長する市場になると予測されているが、これは同国の少数の農業従事者グループがハイブリッドよりもOPVを使用すると予測されているためです。OPVは肥料や農薬などの投入物が少なくて済み、価格も安く、小規模農業従事者や低所得農業従事者にとって手頃です。

- したがって、市販種子の栽培面積の増加や、より多くのタンパク質と消化可能な繊維を含む高品質の飼料に対する畜牛生産者の需要は、予測期間中にハイブリッド種子市場を押し上げると予測されます。

畜産業からのアルファルファ需要の増加と栽培面積の増加が市場を牽引しています。

- 欧州は世界最大のアルファルファ種子市場です。2022年には世界のアルファルファ種子市場の約41.1%を占め、アルファルファの栽培面積は320万ヘクタールでした。イタリアは最大の生産国であり、欧州におけるアルファルファ生産面積の大部分を占めています。より良質な食肉への需要が大きいため、家畜生産の増加はアルファルファのようなより良質な飼料作物への需要を生み出し、同地域のアルファルファ飼料種子市場を牽引すると考えられます。

- 2022年、北米はアルファルファ種子の世界市場において最大の市場であり、世界的に最も生産量が多く、気象条件、酪農業従事者による需要の増加により、世界市場の約29.0%のシェアを占めています。カナダは、飼料としての需要の増加、栽培面積の増加、収益性の高さから、この地域で最も需要が大きいです。

- アジア太平洋では、アルファルファは重要な飼料作物です。天候に恵まれ、高タンパク質飼料に対する需要がこの地域の家畜・牧畜業者から高まっているからです。同地域の市場シェアは2022年には16.5%であり、農業従事者の間でアルファルファの採用が増加していることから、予測期間中にCAGR 2.4%で増加すると予想されます。

- 南米は2022年に世界のアルファルファ種子市場の約6.5%を占めました。栽培面積は2017年の390万ヘクタールから2022年には440万ヘクタールに増加しています。この栽培面積の増加は、予測期間中にCAGR 3.0%で市場を牽引すると予測されます。

- 栽培面積の増加と飼料需要の増加が、アルファルファ種子市場の成長に寄与すると予測される主要因です。

世界のアルファルファ種子市場動向

北米とアジア太平洋が家畜の増加に伴いアルファルファの栽培面積を独占

- アルファルファは、家畜、特に牛に与える飼料加工産業からの高い需要により、世界的に栽培されている主要作物の一つです。アルファルファベースの飼料に対するこの高い需要を満たすため、アルファルファの栽培面積は2022年には3,150万ヘクタールとなり、2017~2022年の間に4.5%増加しました。さらに、この作物は2022年の飼料作物の栽培面積の39.2%を占めました。

- 北米は2022年のアルファルファの栽培面積が1,150万ヘクタールと多く、2017~2022年の間に5.5%増加しました。面積の増加は、同地域の飼料生産と家畜頭数を増加させるための投資とカナダ政府からの支援の増加に起因します。例えば、反芻動物の頭数は2017~2022年にかけて1.9%増加し、水牛と牛の頭数は同期間に1億5,510万頭から1億5,860万頭に増加しました。

- アジア太平洋では、アルファルファの栽培面積は2022年に640万ヘクタールとなりました。この地域の主要アルファルファ栽培国は中国、オーストラリア、インドです。中でも中国が主要な市場シェアを占めており、2022年のアジア太平洋アルファルファ栽培面積の76.8%を占めています。

- 中国政府は、酪農とアルファルファ生産を強化するための行動計画を策定しました。アルファルファの3万3,000ヘクタールを開発するための支援プログラムに7,130万米ドルを提供し、200ヘクタール以上のアルファルファ農場には1平方メートル当たり86.11米ドルの補助金を提供しました。このような措置により、同地域ではアルファルファの栽培が増加しています。

- 家畜の増加と乳製品需要の増加により、栽培面積は増加しています。

不利な気候条件下での高収量を目的とした、耐病性、幅広い適応性、耐乾性アルファルファ種子の採用増加

- 世界的に、アルファルファは主要な飼料作物として栽培されています。この作物で需要の高い形質は、耐病性、耐虫性、畜産業用の飼料/サイレージの品質を向上させるための幅広い適応性です。さらに、タンパク質含有量の増加、四季を通じた生育、リグニン含有量の低減といった他の形質も、将来的にフォレージの品質向上のために人気が高まると予想されます。

- より広い適応性は世界市場で最も採用されている形質であり、特に南米では2022年に35.4%を占めました。これは、農業気候条件の変化、圃場ストレス、異なる地域での作物栽培のために最も採用されました。Bayer、DLF、Barenbrugなどの開発企業は、英国でDKC 3218、DKC 3204、Debalto、Marcamoなどのさまざまなアルファルファ品種を開発してきました。これらの品種は、多様な環境条件に耐え、様々な土壌タイプに適応し、圃場ストレスや暑熱条件にも耐えることができます。さらに、EU委員会のREFORMAプロジェクト(2016~2020年)は、先進的育種技術を開発し、新しいアルファルファ品種を導入することを目指しています。

- 耐病性、高デンプン含量、干ばつ耐性も需要の高い形質です。Ampac Seed Company(Attention II)、Land O'Lakes(Round-up Ready)、KWS SAAT SE & Co.KGaG(HarvXtra、Standfast)、Bayerクロップサイエンス(DEKALB)、シンジェンタAG(NEXGROW)、DLF(Fortune)などが、コレトトリカム・トリフォリイやバーティシリウム・ウィルトなどの病害に対する抵抗性を持つ種子品種を提供している企業です。家畜飼料の改良需要の増加、耐病性などの多くの利点、収穫量の増加などの要因が、予測期間中の市場の成長を促進すると予想されます。

アルファルファ種子産業概要

アルファルファ種子市場は細分化されており、上位5社で39.27%を占めています。この市場の主要企業は、Bayer AG、Corteva Agriscience、DLF、Royal Barenbrug Group、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 地域

- アフリカ

- 育種技術別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- 日本

- ミャンマー

- パキスタン

- フィリピン

- ベトナム

- その他のアジア太平洋

- 欧州

- 育種技術別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他の欧州

- 中東

- 育種技術別

- 国別

- イラン

- サウジアラビア

- その他の中東

- 北米

- 飼育技術別

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米

- 南米

- 育種技術別

- 国別

- アルゼンチン

- ブラジル

- その他の南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ampac Seed Company

- Bayer AG

- Corteva Agriscience

- DLF

- KWS SAAT SE & Co. KGaA

- Land O'Lakes Inc.

- RAGT Group

- Royal Barenbrug Group

- S& W Seed Co.

- Syngenta Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92511

The Alfalfa Seed Market size is estimated at 1.12 billion USD in 2025, and is expected to reach 1.35 billion USD by 2030, growing at a CAGR of 3.66% during the forecast period (2025-2030).

The increased adoption of hybrid seeds due to their improved traits such as disease resistance are driving the market.

- The livestock population is increasing across various regions around the world. The increase in livestock population needs an expansion of the area under forages, and alfalfa offers easily digestible fiber content. These are some of the major factors leading to the growth of the hybrid and open-pollinated alfalfa seed market.

- The hybrid segment tops the alfalfa seed market due to the increased adoption of hybrid varieties and increasing awareness about their benefits. The hybrid alfalfa seed market value is projected to increase by about 35.9% and reach USD 1.1 billion by the end of the forecast period. This is due to the rise in the seed replacement rate and the availability of improved varieties in the market.

- Increasing acceptance of advanced hybrid technology by growers, such as drought tolerance and disease resistance, is projected to contribute to hybrid alfalfa seed market growth in the coming years. For instance, in the United States, hybrids occupied 99% of the area under commercial seeds in 2022, which is attributed to the availability of high-yielding hybrid varieties and the development of transgenic alfalfa varieties from popular companies such as Allied Seed LLC, Bayer AG, and DLF.

- Africa is forecasted to be the fastest growing market in the OPVs segment at a CAGR of 3.2% because a small group of farmers in the country is projected to use OPVs over hybrids as they require fewer inputs, such as fertilizer and pesticides and are less expensive and more affordable for small holding and low-income farmers.

- Therefore, an increase in the cultivation area under commercial seeds and the demand from cattle growers for quality forage with more protein and digestible fiber content is projected to boost the market for hybrid seeds during the forecast period.

The increasing demand for alfalfa from livestock industry combined with growing cultivation area driving the market.

- Europe is the largest alfalfa seed market in the world. It accounted for about 41.1% of the global alfalfa seed market in 2022, with 3.2 million hectares under alfalfa cultivation. Italy was the largest producer and occupied a large area of alfalfa production in Europe. As there is a significant demand for better-quality meat, increased livestock production is likely to create a demand for better forage crops such as alfalfa, driving the market for alfalfa forage seeds in the region.

- In 2022, North America was the largest market in the global alfalfa seed market, with a share of about 29.0% of the global market due to the highest production, globally, weather conditions, and increased demand by dairy farmers. Canada has the greatest demand in the region because of the increase in demand for crops as feed, the increase in cultivation area, and high profitability.

- In Asia-Pacific, alfalfa is an important forage crop as the weather is favourable and demand for high protein feed is more from the livestock and cattle rearers in the region. The market share of the region was 16.5% in 2022, which is expected to increase at a CAGR of 2.4% during the forecast period as the adoption of alfalfa is increasing among farmers.

- South America accounted for about 6.5% of the global alfalfa seed market in 2022. The area cultivated has increased from 3.9 million hectares in 2017 to 4.4 million hectares in 2022. This increase in cultivation area is anticipated to drive the market at a CAGR of 3.0% during the forecast period.

- The increasing area under cultivation and rising demand for forage are the major factors anticipated to help in the growth of the alfalfa seed market.

Global Alfalfa Seed Market Trends

North America and Asia Pacific dominated the area under cultivation of alfalfa with increased livestock population

- Alfalfa is one of the major crops cultivated globally due to the high demand from the feed processing industry to feed livestock, especially cattle. To meet this high demand for alfalfa-based feed, the area cultivated for alfalfa was 31.5 million hectares in 2022, which increased by 4.5% during 2017-2022. Moreover, the crop accounted for 39.2% of the area under cultivation of forage crops in 2022.

- North America has a higher area under cultivation of alfalfa in 2022, with 11.5 million hectares, which increased by 5.5% during 2017-2022. The increase in area is attributed to the increasing investments and support from the Canadian government to increase the region's feed production and livestock population. For instance, ruminant population increased by 1.9% from 2017 to 2022, with the number of buffaloes and cattle rising from 155.1 million to 158.6 million during the same period.

- In Asia-Pacific, the area under alfalfa cultivation was 6.4 million hectares in 2022. Major Alfalfa growing countries in the region are China, Australia, and India. Among these, China held the major market share, which accounted for 76.8% of the area under Asia-Pacific alfalfa cultivation in 2022.

- The government developed an action plan in China to enhance dairy and alfalfa production. It provided USD 71.3 million in support programs to develop 33.0 thousand hectares of alfalfa alongside a subsidy of USD 86.11 per square meter for alfalfa farms over 200 hectares. Thus, these measures increase the cultivation of alfalfa in the region.

- Due to an increase in livestock population and rising demand for dairy products, the cultivation area has been increasing.

Rising adoption of disease resistant, wider adaptability, and drought resistant alfalfa seeds for high yield during adverse climatic conditions

- Globally, alfalfa is a majorly cultivated forage crop. The high-demand traits of the crop are disease-resistant, insect-resistant, and wider adaptability for improving the quality of the feed/silage for the livestock industry. Furthermore, other traits such as increasing protein content, growing throughout the seasons, and reducing lignin content are expected to gain popularity in the future for increasing forage quality.

- Wider adaptability is the most adopted trait in the global market, especially South America, as it accounted for 35.4% in 2022 in the region. It was most adopted because of the changing agro-climatic conditions, field stress, and growing crops in different regions. Companies such as Bayer, DLF, and Barenbrug have developed different alfalfa varieties in the United Kingdom, such as DKC 3218, DKC 3204, Debalto, and Marcamo. These varieties can withstand diverse environmental conditions, adapt to various soil types, and withstand field stress and heat conditions. Furthermore, the EU Commission's REFORMA project (2016-2020) aims to develop advanced breeding techniques and introduce new alfalfa cultivars.

- Disease tolerance, high starch content, and drought tolerance are other traits in high demand. Ampac Seed Company (Attention II), Land O'Lakes (Round-up Ready), KWS SAAT SE & Co. KGaG (HarvXtra, Standfast), Bayer Crop Science (DEKALB), Syngenta AG (NEXGROW), and DLF (Fortune) are companies proving seed varieties that have resistance to diseases such as Colletotrichum trifolii, and verticillium wilt. Factors such as the increased demand for improving animal feed, many benefits such as disease resistance, and increasing yield are expected to drive the market's growth during the forecast period.

Alfalfa Seed Industry Overview

The Alfalfa Seed Market is fragmented, with the top five companies occupying 39.27%. The major players in this market are Bayer AG, Corteva Agriscience, DLF, Royal Barenbrug Group and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Breeding Technology

- 5.2.1.2 By Country

- 5.2.1.2.1 Egypt

- 5.2.1.2.2 Ethiopia

- 5.2.1.2.3 Ghana

- 5.2.1.2.4 Kenya

- 5.2.1.2.5 Nigeria

- 5.2.1.2.6 South Africa

- 5.2.1.2.7 Tanzania

- 5.2.1.2.8 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Breeding Technology

- 5.2.2.2 By Country

- 5.2.2.2.1 Australia

- 5.2.2.2.2 Bangladesh

- 5.2.2.2.3 China

- 5.2.2.2.4 India

- 5.2.2.2.5 Japan

- 5.2.2.2.6 Myanmar

- 5.2.2.2.7 Pakistan

- 5.2.2.2.8 Philippines

- 5.2.2.2.9 Vietnam

- 5.2.2.2.10 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Breeding Technology

- 5.2.3.2 By Country

- 5.2.3.2.1 France

- 5.2.3.2.2 Germany

- 5.2.3.2.3 Italy

- 5.2.3.2.4 Netherlands

- 5.2.3.2.5 Poland

- 5.2.3.2.6 Romania

- 5.2.3.2.7 Russia

- 5.2.3.2.8 Spain

- 5.2.3.2.9 Turkey

- 5.2.3.2.10 Ukraine

- 5.2.3.2.11 United Kingdom

- 5.2.3.2.12 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Breeding Technology

- 5.2.4.2 By Country

- 5.2.4.2.1 Iran

- 5.2.4.2.2 Saudi Arabia

- 5.2.4.2.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Breeding Technology

- 5.2.5.2 By Country

- 5.2.5.2.1 Canada

- 5.2.5.2.2 Mexico

- 5.2.5.2.3 United States

- 5.2.5.2.4 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Breeding Technology

- 5.2.6.2 By Country

- 5.2.6.2.1 Argentina

- 5.2.6.2.2 Brazil

- 5.2.6.2.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ampac Seed Company

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 DLF

- 6.4.5 KWS SAAT SE & Co. KGaA

- 6.4.6 Land O'Lakes Inc.

- 6.4.7 RAGT Group

- 6.4.8 Royal Barenbrug Group

- 6.4.9 S&W Seed Co.

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アルファルファ種子:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 415 Pages

- 納期

- 2~3営業日