|

市場調査レポート

商品コード

1693445

ヒマワリ種子(播種用種子)-市場シェア分析、産業動向、成長予測(2025~2030年)Sunflower Seed (seed For Sowing) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヒマワリ種子(播種用種子)-市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 385 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

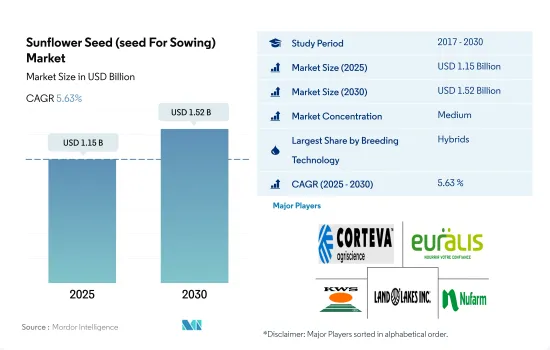

ヒマワリ種子(播種用種子)市場規模は2025年に11億5,000万米ドルと推定・予測され、2030年には15億2,000万米ドルに達し、予測期間(2025~2030年)のCAGRは5.63%で成長すると予測されます。

高収量、害虫抵抗性、高油分によりハイブリッド種子が主要シェアを占める

- ハイブリッド種子は干ばつに強く、異なる地域や気象条件への適応性が広く、ハイブリッド種子を使用することで高品質の油糧種子が生産されるため、2022年にはハイブリッド種子のシェアが開放受粉種子品種を上回りました。

- 予測期間中、ハイブリッド種子はより高い収量と害虫抵抗性を提供できるため、CAGRは5.7%と予測されます。世界全体では、2022年、非遺伝子組み換えハイブリッドヒマワリ種子市場は、ヒマワリハイブリッド種子市場の約100%でした。遺伝子組換えヒマワリは商業的に栽培されておらず、非遺伝子組換え食品を消費することの利点に関する人々の意識は高まっています。そのため、非遺伝子組み換えハイブリッドの需要が増加しています。

- ほとんどの地域では、開放受粉種子品種はハイブリッド種子品種に比べて使用量が少ないです。なぜなら、開放受粉種子品種は病害に対する抵抗性がなく、生物学的と生物学的要因の両方から攻撃を受けやすいからです。そのため、雑草や昆虫による作物の損失を最小限に抑えるため、生産者は耐病性や耐虫性といったハイブリッド種子の形質を利用しています。

- 開放受粉種子品種は、ハイブリッド種子よりも価格が安く、地域の条件に適応しやすいため、小規模生産者が開放受粉種子品種の使用を好むため、OPVによる播種が着実に増加しており、予測期間中にCAGR 3.4%を記録すると予想されます。

- したがって、高い収量や耐病性などの利点がハイブリッド種子セグメントの牽引役となるが、小規模農業従事者は作物投入コストを最小限に抑えることでより高い利益を得るために開放受粉種子品種を使用することになります。

ハイブリッド種子は、変化する気候条件への耐性と高収量を提供する能力により、世界のヒマワリ種子市場で最も急成長しているセグメントです。

- 南米は世界のヒマワリのトップ生産国のひとつです。2022年には、世界のヒマワリ種子市場金額で29.1%の市場シェアを占めました。南米で生産されるヒマワリは輸出価値が高く、油やオイルミックス用に加工されるからです。さらに、同地域の種子会社は、高油分と加工産業に適した品種を中心とした新しい種子のハイブリッドを発表しています。

- 南米では、ヒマワリの栽培面積は2022年に190万ヘクタールとなり、油や加工食品の需要増加により2020~2022年の間に8.7%増加しました。

- アルゼンチンでは、ロシア・ウクライナ戦争の影響でヒマワリとその油の生産需要が高まっており、世界最大のヒマワリ製品の生産・輸出国となっています。

- 欧州は、先進的技術が利用可能なため、予測期間中にCAGR約6.2%を記録し、成長を確認すると推定・予測されている地域です。米国農務省によると、欧州は理想的な気象条件に恵まれているため、予測期間中にヒマワリの生産量が増加する見込みです。

- アジア太平洋のヒマワリ栽培面積は、2022年には250万haと世界第2位であり、価格上昇とヒマワリ種子の需要により、さらに増加すると推定されます。

- ヒマワリの栽培に使用されるハイブリッド種子は、予測期間中にCAGR 5.7%を記録すると予想されます。なぜなら、ヒマワリ作物は気候条件に弱く、ハイブリッド品種は干ばつや洪水などの傾斜した気候条件に抵抗する能力を持っているからです。

- したがって、栽培面積の増加とヒマワリ油の高い需要が、予測期間中のヒマワリセグメントの成長を後押しする可能性があります。

世界のヒマワリ種子(播種用種子)市場動向

ヒマワリ種子子の需要増加によりヒマワリの栽培面積が増加しており、欧州が主要地域です。

- ヒマワリは世界中で栽培されている主要な油糧作物の一つです。世界全体では、ヒマワリの総栽培面積は2016~2022年の間に15.6%増加し、最も栽培面積の多い主要地域は欧州で(2,300万ヘクタール)、2022年には世界の75.5%を占めます。これは、良好な気候条件と世界の食用油需要の増加によるものです。ロシアは欧州で最も栽培面積が多く、1,020万ヘクタールで、2022年の世界面積の33.4%を占めました。同国の面積は2016~2022年の間に39.6%増加しました。面積の増加は、高い国内需要と輸出ポテンシャルによるものです。ヒマワリ種子の生産量では世界最大の国です。

- アジア太平洋は第2位の地域で、2022年には世界のヒマワリ作付面積の8.4%を占めます。しかし、2016~2022年の間に面積は10.9%減少しており、これは主にインドのような国々で農業従事者がトウモロコシや綿のような他の作物にシフトしたためです。例えばインドでは、2016~2022年にかけて、作付面積の44.3%が減少しました。中国はアジア太平洋の37.3%を占める主要生産国です。世界の生産量では中国は第4位で、2021年のヒマワリ種子生産量全体の4.7%を占めます。

- 2022年、アフリカは世界のヒマワリ栽培面積の7.8%を占め、2016年から4.1%増加しました。タンザニアはこの地域でヒマワリを栽培している主要国で、2022年にはこの地域のヒマワリ総栽培面積の44.9%を占めます。北米と南米は、2022年の世界のヒマワリ栽培面積のそれぞれ1.8%と6.2%のシェアを占めています。北米では、2016~2022年にかけてヒマワリの作付面積が14.5%減少したが、これは主にヒマワリ生産地域における干ばつの影響によるものです。

うどんこ病やフザリウム病などの病害の蔓延と油需要の高さから、耐病性、高オレイン酸、高リノール酸含有形質の需要が急増しました。

- ヒマワリは広く栽培されている主要な油糧作物のひとつです。米国では、2017年にヒマワリ生産量の10%~20%が殻付きカーネル、ホールシード、ヒマワリ種子を含むナッツと果実のミックスに使用されました。カーネルはグラノーラバーやパンなどの加工食品に使用されます。改良された形質を持つ種子品種に対する需要は、予測期間中に増加すると予想されます。さらに、オレイン酸とリノール酸含有量(必要性による)の高い油含有量(主要な収量属性特性)は、大きな需要があります。ヒマワリ油の需要は、大豆油の価格上昇とパーム油の禁止令の後に増加しています。このように、油分の含有量が多いため、ヒマワリのような作物への需要が高まり、高収入の収益が増加します。Corteva Agriscience、Groupe Limagrain、Syngenta AGによる65A25、P62LL109、LG 50760 CL、Xi Arkoなどの製品には、高オレイン酸含有形質が含まれています。

- 病害抵抗性形質は生産者に広く利用されており、べと病、フザリウム病、バーティシリウム病、スクレロチニア病、プラスモフォラ病などに対する抵抗性は非常に人気が高く、広く栽培されています。これらの病害は圃場条件下で大きな収量損失を引き起こすため、抵抗性品種は病害を回避し、生産性を向上させています。例えば、MG360やCP432Eはべと病に対する抵抗性を持つ品種です。

- その他、干ばつ耐性、宿根耐性、幅広い適応性、早生・中生、メチル系除草剤耐性、水分ストレス耐性など、高収量特性を持つ形質が世界的に利用されています。企業別、ウイルスに対する高い耐性を持つ新しいハイブリッド種子品種の導入や、加工産業による高い需要は、予測期間中のヒマワリ種子市場の成長を助けると予想される要因です。

ヒマワリ種子(播種用種子)産業概要

ヒマワリ種子(播種用種子)市場は適度に統合されており、上位5社で58.58%を占めています。この市場の主要企業は、Corteva Agriscience、Euralis Semences、KWS SAAT SE & Co. KGaA、Land O'Lakes Inc.、Nufarmなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 地域

- アフリカ

- 育種技術別

- 国別

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

- アジア太平洋

- 育種技術別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- ミャンマー

- パキスタン

- タイ

- その他のアジア太平洋

- 欧州

- 育種技術別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他の欧州

- 中東

- 育種技術別

- 国別

- イラン

- その他の中東

- 北米

- 育種技術別

- 国別

- カナダ

- メキシコ

- 米国

- 南米

- 育種技術別

- 国別

- アルゼンチン

- ブラジル

- その他の南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Corteva Agriscience

- Euralis Semences

- KWS SAAT SE & Co. KGaA

- Land O'Lakes Inc.

- Nufarm

- RAGT Group

- Royal Barenbrug Group

- S& W Seed Co.

- Syngenta Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92507

The Sunflower Seed (seed For Sowing) Market size is estimated at 1.15 billion USD in 2025, and is expected to reach 1.52 billion USD by 2030, growing at a CAGR of 5.63% during the forecast period (2025-2030).

Hybrids held the major share due to higher yield, pest resistance, and high oil content

- In 2022, hybrid seeds had more share than open-pollinated seed varieties because hybrid seeds are drought resistant, have wider adaptability to different regions and weather conditions, and high-quality oil seeds are produced by using hybrid seeds.

- During the forecast period, the hybrid segment is projected to register a CAGR of 5.7% due to its ability to provide higher yield and pest resistance. Globally, in 2022, the non-transgenic hybrid sunflower seed market was about 100% of the sunflower hybrid seed market. Transgenic sunflowers are not cultivated commercially, and the awareness among people about the benefits of consuming non-GMO food is increasing. Thus, the demand for non-transgenic hybrids is increasing.

- In most regions, open-pollinated seed varieties are used less compared to hybrid seed varieties because open-pollinated seed varieties are not resistant to diseases and can be attacked easily by both biotic and abiotic factors. Therefore, to minimize crop loss due to weeds and insects, growers use hybrid seed traits such as disease tolerance and insect resistance.

- Open-pollinated seed varieties are anticipated to register a CAGR of 3.4% during the forecast period owing to a steady increase in sowing under OPVs because small-scale growers prefer to use open-pollinated seed varieties as they are less expensive than hybrid seeds and easily adapt to local conditions.

- Therefore, the benefits, such as higher yield and resistance to diseases, will help drive the hybrid seed segment, but open-pollinated seed varieties will be used by small-scale farmers for higher profit by minimizing crop input costs.

Hybrids are the fastest-growing segment in the global sunflower seed market due to their ability to resist inclined climatic conditions and provide high yields

- South America is one of the top producers of sunflowers globally. In 2022, it held a market share of 29.1% in the global sunflower seed market value. This is because sunflowers produced in South America have high export value and are processed for oil and oil mixes. Additionally, the seed companies in the region have released new seed hybrids that are focused on high oil content and suiting processing industries.

- In South America, the cultivated area for sunflowers was 1.9 million hectares in 2022, which increased by 8.7% between 2020 and 2022 due to an increase in demand for oil and processed foods.

- There is a growing production demand for sunflower and its oil in Argentina due to the Russia-Ukraine War, as they are the largest producers and exporters of sunflower products globally.

- Europe is a region that is estimated to witness growth, registering a CAGR of about 6.2% during the forecast period due to the availability of advanced technology. According to the USDA, Europe has ideal weather conditions, due to which the production of sunflowers is expected to increase during the forecast period.

- Asia-Pacific has the second-largest cultivated area of sunflowers across the world, with 2.5 million ha in 2022, which is estimated to increase further due to rising prices and demand for sunflower seeds.

- Hybrid seeds used for the cultivation of sunflowers are expected to register a CAGR of 5.7% during the forecast period, as the sunflower crop is more vulnerable to climatic conditions, and hybrid varieties have the ability to resist inclined climatic conditions such as drought and flood.

- Therefore, the increasing cultivation areas and the high demand for sunflower oil may help boost the growth of the sunflower segment during the forecast period.

Global Sunflower Seed (seed For Sowing) Market Trends

There is an increased area under sunflower cultivation due to increased demand for sunflower seeds, with Europe being the major region

- Sunflower is one of the major oilseed crops cultivated all over the world. Globally, the total sunflower acreage increased by 15.6% between 2016 and 2022, with Europe being the major region with the highest cultivated acreage (23.0 million hectares), accounted for 75.5% of the global area in 2022. This is due to the favorable climatic conditions and increased demand for edible oil globally. Russia had the highest cultivated area in Europe, with 10.2 million hectares, accounting for 33.4% of the global area in 2022. The area in the country increased by 39.6% during 2016-2022. The increased area is due to high domestic demand and export potential. It is the largest country in terms of sunflower seed production globally.

- Asia-Pacific is the second-largest region, accounting for 8.4% of the world's sunflower acreage in 2022. However, the area decreased by 10.9% between 2016 and 2022, mainly due to farmers' shift to other crops like corn and cotton in countries like India. For instance, in India, from 2016 to 2022, 44.3% of the acreage declined. China is the major producer in the region, accounting for 37.3% of the area in Asia-Pacific. China ranks fourth in terms of global production, with 4.7% of total sunflower seed production in 2021.

- In 2022, Africa held 7.8% of the world's sunflower acreage, which increased by 4.1% since 2016. Tanzania is the major country cultivating sunflower in the region, accounting for 44.9% of the total sunflower acreage in the region in 2022. North America and South America held 1.8% and 6.2% share of the global sunflower area in 2022, respectively. In North America, sunflower acreage decreased by 14.5% between 2016 and 2022, mainly due to the impact of drought in sunflower-growing regions.

Prevalence of diseases, including downy mildew and Fusarium, and high demand for oil led to a surge in demand for disease resistance, high oleic and linoleic content traits

- Sunflower is one of the major oilseed crops that is widely cultivated. In the US, 10%-20% of sunflower production was used in shelled kernels, whole seeds, and nut and fruit mixes containing sunflower seed in 2017. Kernels are used in processed foods, such as granola bars and bread. The demand for seed varieties with improved traits is expected to increase during the forecast period. Moreover, high oil content (major yield attribute character), with oleic and linoleic content (based upon the need), have significant demand. The demand for sunflower oil is increasing after an increase in the prices of soybean oil and a ban on palm oil. Thus, the high oil content increases the demand for crops such as sunflower and increases the higher income returns. Products such as 65A25, P62LL109, LG 50760 CL, and Xi Arko by Corteva Agriscience, Groupe Limagrain, and Syngenta AG contain high oleic content traits.

- Disease-resistant traits are widely used by growers, and resistance to downy mildew, Fusarium, Verticillium, Sclerotinia, Plasmophora, and other diseases are very popular and widely cultivated. As these diseases cause significant yield losses during field conditions, resistant varieties avoid the diseases and increase their productivity. For instance, MG 360 and CP432E are the products that are resistant to downy mildew.

- Other traits, such as tolerance to drought, lodging, wider adaptability, early-medium maturity, tolerance to methyl herbicides, and tolerance to moisture stress, with high-yielding characteristics, are used globally. The introduction of new hybrid seed varieties by companies with higher resistance to viruses and high demand by processing industries are the factors expected to help in the growth of the sunflower seed market during the forecast period.

Sunflower Seed (seed For Sowing) Industry Overview

The Sunflower Seed (seed For Sowing) Market is moderately consolidated, with the top five companies occupying 58.58%. The major players in this market are Corteva Agriscience, Euralis Semences, KWS SAAT SE & Co. KGaA, Land O'Lakes Inc. and Nufarm (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Breeding Technology

- 5.2.1.2 By Country

- 5.2.1.2.1 Egypt

- 5.2.1.2.2 Ethiopia

- 5.2.1.2.3 Ghana

- 5.2.1.2.4 Kenya

- 5.2.1.2.5 Nigeria

- 5.2.1.2.6 South Africa

- 5.2.1.2.7 Tanzania

- 5.2.1.2.8 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Breeding Technology

- 5.2.2.2 By Country

- 5.2.2.2.1 Australia

- 5.2.2.2.2 Bangladesh

- 5.2.2.2.3 China

- 5.2.2.2.4 India

- 5.2.2.2.5 Indonesia

- 5.2.2.2.6 Myanmar

- 5.2.2.2.7 Pakistan

- 5.2.2.2.8 Thailand

- 5.2.2.2.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Breeding Technology

- 5.2.3.2 By Country

- 5.2.3.2.1 France

- 5.2.3.2.2 Germany

- 5.2.3.2.3 Italy

- 5.2.3.2.4 Netherlands

- 5.2.3.2.5 Poland

- 5.2.3.2.6 Romania

- 5.2.3.2.7 Russia

- 5.2.3.2.8 Spain

- 5.2.3.2.9 Turkey

- 5.2.3.2.10 Ukraine

- 5.2.3.2.11 United Kingdom

- 5.2.3.2.12 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Breeding Technology

- 5.2.4.2 By Country

- 5.2.4.2.1 Iran

- 5.2.4.2.2 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Breeding Technology

- 5.2.5.2 By Country

- 5.2.5.2.1 Canada

- 5.2.5.2.2 Mexico

- 5.2.5.2.3 United States

- 5.2.6 South America

- 5.2.6.1 By Breeding Technology

- 5.2.6.2 By Country

- 5.2.6.2.1 Argentina

- 5.2.6.2.2 Brazil

- 5.2.6.2.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Corteva Agriscience

- 6.4.3 Euralis Semences

- 6.4.4 KWS SAAT SE & Co. KGaA

- 6.4.5 Land O'Lakes Inc.

- 6.4.6 Nufarm

- 6.4.7 RAGT Group

- 6.4.8 Royal Barenbrug Group

- 6.4.9 S&W Seed Co.

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms