|

市場調査レポート

商品コード

1693422

アジア太平洋地域のアクリル接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Acrylic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のアクリル接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 215 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

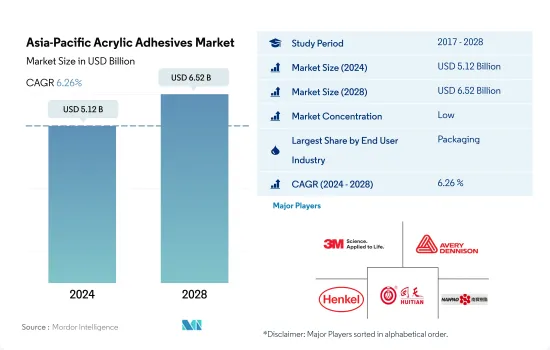

アジア太平洋地域のアクリル接着剤市場規模は、2024年には51億2,000万米ドルと推定され、予測期間中(2024-2028年)にCAGR 6.26%で成長し、2028年には65億2,000万米ドルに達すると予測されます。

アクリル接着剤の需要を促進する地域全体の電気自動車普及の高まり

- アクリル接着剤は、防水、耐候性シール、ひび割れシール、接着などの用途があるため、建設業界で広く使用されています。中国は、アジア太平洋地域で最も急成長している国であり、2022年から2028年のアクリル建築用接着剤の消費量のCAGRは5%です。同国は、2021年に金額ベースで4兆6,000億米ドルを記録し、前年比10%の伸びを示した建設生産高の増加により、建築・建設業界で使用されるアクリル接着剤の需要が最も高いことを記録しました。

- アクリル接着剤はまた、ガラス、金属、プラスチック、塗装面などの表面への適用性のため、自動車産業全体で広く使用されており、その特徴は、極端な耐候性、耐久性、長持ちなど、自動車産業で有用です。発展途上のアジアでEVエコシステムを開発することは、ASEAN諸国が消費者の普及を促進し、気候変動目標を達成するために不可欠です。明日のEVエコシステムの構築には、供給側と需要側の双方を後押しすることで、EVバリューチェーンを大幅に拡大することが必要です。アジア市場における電動4輪車の普及は、今後も著しいものになると思われます。絶対ベースでは、中国が最大のEV市場になると思われます。現在の軌道では、中国の普及率は60%に近づき、2030年までに世界のEV新車販売の40%以上を占めるようになると思われます。このため、予測期間(2022~2028年)にはアクリル自動車用接着剤の需要が増加します。

- アクリル接着剤はヘルスケア業界で医療機器部品の組み立てなどの用途に使用されています。アジア太平洋地域におけるヘルスケア投資の増加は、予測期間におけるアクリル接着剤の需要増加につながります。

世界の製造拠点である中国がアクリル接着剤の最大シェアを占める

- 2017年から2021年にかけて、アジア太平洋から生み出された需要は全地域の中で最も高かったです。この地域の接着剤需要のシェアは、すべてのエンドユーザー産業の製造能力が高いため、一貫して世界需要の38~40%程度を占めています。反応性、水系、溶剤系のアクリル接着剤がこの地域の需要の大半を占めています。

- 2017年から2019年にかけて、この地域の接着剤需要はCAGR 2.87%を記録しました。アクリル接着剤の需要が伸び悩んだのは、この地域における建設活動の減少と自動車生産の減少が原因です。この期間、これらのエンドユーザー産業からの需要はそれぞれ-1.68%と-1.65%のCAGRで減少しました。

- 2020年には、操業、労働力、原材料、サプライチェーン、その他の分野での制約により、地域全体のすべてのエンドユーザーからの需要が減少しました。この地域の全ての国の全ての産業の中で、オーストラリアの履物産業は最も大きな打撃を受け、数量ベースで前年比49.32%減少しました。経済の低迷による購買力の低下による内需の減少は、パンデミックの間、この産業に深刻な影響を与えました。

- 2021年には、貿易規制が緩和されたため、アクリル接着剤の需要は急速にパンデミック前の需要量に回復しました。インドの需要は数量ベースで前年比74.54%増と最も高い伸びを示しました。アジア太平洋地域全体の需要は、予測期間中に数量ベースでCAGR 5.13%を記録すると予想されます。この需要成長は、予測期間中、同地域の建設、包装、自動車産業によって牽引されます。

アジア太平洋地域のアクリル接着剤市場動向

発展途上国におけるeコマース産業の急成長により、業界は拡大する

- 包装は主に、保護、封じ込め、情報提供、実用性、プロモーションのために使用されます。そのため、包装はほとんどの産業にとって不可欠な要素となっています。2017年には、紙と板紙、プラスチック包装を含む包装の使用量は25億トンを占めました。2020年には、COVID-19の大流行により、サプライチェーンの混乱、包装資材の不足、商品の輸出入の制限、工場の低能力操業などにより、市場は7.4%のマイナス成長率を記録しました。

- 中国とインドネシアは海洋プラスチック廃棄物の第1位と第2位の排出国であるため、アジア各国の政府はプラスチックの使用を削減するための措置を講じています。中国は過剰包装に関する新たな規制を発表し、すべての食品・化粧品メーカーに対し、製品に比例して許容される包装の量を決定する特定のガイドラインを遵守するよう求めました。インドネシア政府による拡大生産者責任(EPR)規制は、生産者と小売業者に対し、リサイクル可能な材料の比率を高めるよう製品包装を再設計することを義務付けるものです。

- 2021年、市場は8%のプラス成長を記録し、27億トンの包装材料が様々な目的で使用されました。中間所得層の増加、サプライチェーンの改善、eコマース活動の活発化により、包装産業は今後も成長を続けると予想され、商品の出荷には特殊な包装が必要となるため、ここ数年で包装産業を大きく後押ししています。成長するアジア市場は包装の利用を促進し、予測期間中(2022-2028年)にCAGR 5.7%を記録することが期待されます。

インフラ活動拡大のための投資増が業界規模を拡大する

- アジア太平洋は、中国、日本、インドといった世界の主要経済国によって牽引されています。中国は継続的な都市化のプロセスを推進中であり、2030年の目標率は70%です。都市化の進展によって都市部で必要とされる居住空間が増加し、都市部の中間所得層が生活環境の改善を望むようになることで、住宅市場に影響を与え、それによって国内の住宅建設が増加する可能性があります。

- 非住宅インフラは大幅に拡大する可能性が高いです。中国政府は2019年に約1,420億米ドルに相当する26のインフラプロジェクトを承認し、2023年に完了する予定です。同国は世界最大の建設市場を有しており、全世界の建設投資の20%を占めています。2030年までに、政府は13兆米ドルを超える建設投資を計画しています。このため、建設市場は予測期間中(2022~2028年)に4.48%のCAGRで推移すると予想されます。

- 建設産業はアジア太平洋地域最大の産業の1つであり、2019年には有望な成長を記録しました。同地域はベトナム、マレーシア、インドネシア、タイ、その他の南アジア諸国など多くの新興諸国を構成しているため、同産業は成長を続けています。しかし、COVID-19パンデミックのために、建設部門は、インド、中国、日本、ASEAN諸国を含む発展途上国に深刻な影響を与えた地域全体の政府によるロックダウンのために大幅な減少を示しました。

- アジア太平洋地域でも、建設分野への海外投資家の関心が高まっています。発展途上諸国が投資家により良い利益と機会を提供するため、建設開発分野への外国直接投資(FDI)が増加しています。

アジア太平洋地域のアクリル接着剤産業の概要

アジア太平洋地域のアクリル接着剤市場は細分化されており、上位5社で15.23%を占めています。この市場の主要企業は以下の通りです。 3M, AVERY DENNISON CORPORATION, Henkel AG & Co. KGaA, Hubei Huitian New Materials and NANPAO RESINS CHEMICAL GROUP(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- 包装

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- ヘルスケア

- 包装

- その他のエンドユーザー産業

- テクノロジー

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水系

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co. Ltd

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Pidilite Industries Ltd.

- Sika AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Acrylic Adhesives Market size is estimated at 5.12 billion USD in 2024, and is expected to reach 6.52 billion USD by 2028, growing at a CAGR of 6.26% during the forecast period (2024-2028).

The rising adoption of electric vehicle across the region to foster the demand for acrylic adhesives

- Acrylic adhesives are widely used in the construction industry because of their applications, such as waterproofing, weather-sealing, cracks sealing, and bonding. China is the fastest-growing country in the Asia-Pacific region, with a CAGR of 5% during the period 2022 to 2028 in terms of consumption of acrylic construction adhesives. The country registered the highest demand for acrylic adhesives used in the building and construction industry owing to rising construction output which registered USD 4.6 trillion by value in 2021, showing 10% growth compared to the previous year.

- Acrylic adhesives are also widely used across the automotive industry because of their applicability to surfaces such as glass, metal, plastic, and painted surfaces, and their features are helpful in the automotive industry, such as extreme weather resistance, durability, and long-lasting. Developing an EV ecosystem in developing Asia is critical for ASEAN nations to expedite consumer adoption and meet their climate targets. Creating tomorrow's EV ecosystems entails significantly expanding the EV value chain by boosting both the supply and demand sides of the equation. The adoption of electric four-wheelers in the Asian markets will continue to be significant. In absolute terms, China will become the largest EV market. On its current trajectory, China's adoption rate will approach 60%, and the country will account for more than 40% of global new EV sales by 2030. This will increase demand for acrylic automotive adhesives in the forecast period (2022-2028).

- Acrylic adhesives are used in the healthcare industry for applications such as assembling medical device parts. The increase in healthcare investments across Asia-Pacific will lead to an increase in their demand in the forecast period.

Being a manufacturing hub of the world China holds largest acrylic adhesive share

- From 2017 to 2021, the demand generated from Asia-Pacific was the highest among all regions. This region's share of adhesive demand has consistently occupied around 38-40% of the global demand because of its high manufacturing capacity of all end-user industries. Acrylic adhesives with reactive, water-borne, and solvent-borne technologies account for most of the demand in the region.

- From 2017 to 2019, the demand for adhesives from this region recorded a CAGR of 2.87%. The slow growth in the demand for acrylic adhesives was due to a decrease in construction activities and a decrease in automotive production in the region. During this period, the demand from these end-user industries declined with a CAGR of -1.68% and -1.65%, respectively.

- In 2020, the demand from all end users across the region declined due to constraints in operations, labor, raw material, supply chain, and other areas. Among all industries from all countries in the region, the footwear industry in Australia took the worst hit, declining by 49.32% y-o-y in volume terms. The decrease in domestic demand because of low purchasing power resulting from a weak economy severely affected this industry during the pandemic.

- In 2021, the demand for acrylic adhesives quickly rebounded to pre-pandemic demand volumes as trade restrictions eased. The demand from India witnessed the highest y-o-y growth of 74.54% in volume terms. The overall demand from the Asia-Pacific region is expected to record a CAGR of 5.13% in volume terms during the forecast period. This demand growth will be driven by the region's construction, packaging, and automotive industries during the forecast period.

Asia-Pacific Acrylic Adhesives Market Trends

Fast paced growth of e-commerce industry in developing nations to augment the industry

- Packaging is mainly used for protection, containment, information, utility, and promotion. This makes packaging an integral part of most industries. In 2017, packaging usage accounted for 2.5 billion ton of packaging, including paper and paperboard and plastic packaging. In 2020, due to the COVID-19 pandemic, the market registered a negative growth rate of 7.4% due to disruptions in the supply chain, shortage of packaging material, restrictions on the import and export of goods, and factories operating at low capacity.

- Governments of different Asian countries have taken steps to reduce the use of plastic, as China and Indonesia are the first and second-largest contributors to plastic waste in the ocean. China has announced new restrictions on excessive packaging, requiring all food and cosmetics producers to adhere to specific guidelines determining the volume of packaging allowed in proportion to a product. The extended producer responsibility (EPR) regulation imposed by the Indonesian government will oblige producers and retailers to redesign their product packaging to include a higher proportion of recyclable material.

- In 2021, the market registered a positive growth of 8%, with 2.7 billion ton of packaging material used for various purposes. The packaging industry is expected to keep growing due to the rising middle-income population, improvement of supply chains, and rising e-commerce activities, which have significantly boosted the packaging industry in the past few years as special packaging is required for shipping goods. The growing Asian market is expected to boost packaging usage, enabling it to register a CAGR of 5.7% during the forecast period (2022-2028).

Raising investment to expand infrastructural activities will augment the industry size

- Asia-Pacific is driven by the world's major economies, such as China, Japan, and India. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increased living spaces required in the urban areas resulting from increasing urbanization and the desire of middle-income urban residents to improve their living conditions may impact the housing market and, thereby, increase the residential constructions in the country.

- Non-residential infrastructure is likely to expand significantly. The Chinese government approved 26 infrastructure projects worth approximately USD 142 billion in 2019, with completion due in 2023. The country has the largest construction market globally, accounting for 20% of all worldwide construction investments. By 2030, the government plans to spend over USD 13 trillion on construction. Thus, the construction market is expected to register a 4.48% CAGR during the forecast period (2022-2028).

- The construction industry is one of the largest industries in Asia-Pacific and recorded promising growth in 2019. The industry continues to grow as the region constitutes many developing countries such as Vietnam, Malaysia, Indonesia, Thailand, and other South Asian countries. However, due to the COVID-19 pandemic, the construction sector witnessed a significant decline owing to lockdowns by governments across the region, which severely affected developing countries, including India, China, Japan, and ASEAN countries.

- The Asia-Pacific region is also witnessing significant interest from international investors in the construction space. Foreign Direct Investment (FDI) in the construction development sector is increasing as developing countries provide better returns and opportunities for investors.

Asia-Pacific Acrylic Adhesives Industry Overview

The Asia-Pacific Acrylic Adhesives Market is fragmented, with the top five companies occupying 15.23%. The major players in this market are 3M, AVERY DENNISON CORPORATION, Henkel AG & Co. KGaA, Hubei Huitian New Materials Co. Ltd and NANPAO RESINS CHEMICAL GROUP (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.2 Regulatory Framework

- 4.2.1 Australia

- 4.2.2 China

- 4.2.3 India

- 4.2.4 Indonesia

- 4.2.5 Japan

- 4.2.6 Malaysia

- 4.2.7 Singapore

- 4.2.8 South Korea

- 4.2.9 Thailand

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV Cured Adhesives

- 5.2.4 Water-borne

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Hubei Huitian New Materials Co. Ltd

- 6.4.7 Kangda New Materials (Group) Co., Ltd.

- 6.4.8 NANPAO RESINS CHEMICAL GROUP

- 6.4.9 Pidilite Industries Ltd.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms