アジア太平洋のエポキシ接着剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Asia-Pacific Epoxy Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 2044259

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

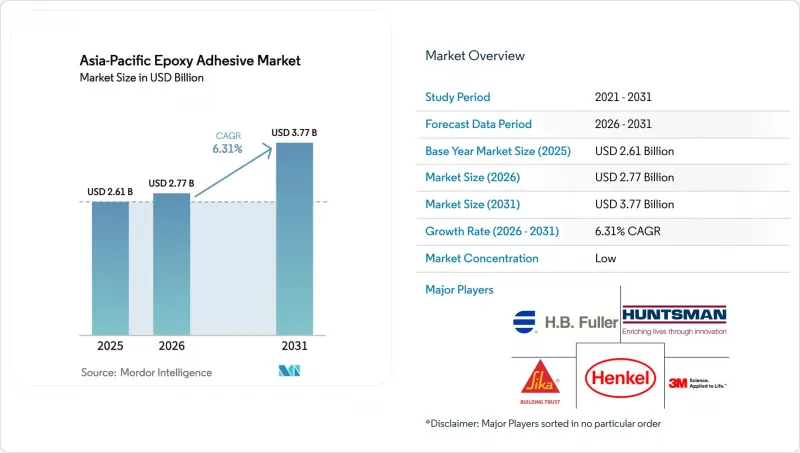

アジア太平洋地域のエポキシ接着剤市場規模は、2025年の26億1,000万米ドルから2026年には27億7,000万米ドルへと拡大し、2026年から2031年にかけてCAGR6.31%で推移し、2031年には37億7,000万米ドルに達すると予測されています。

輸送機器の着実な電動化、半導体パッケージングへの投資拡大、そして過去最高水準の都市インフラ支出が相まって、同地域全体で構造用接着剤の需要を押し上げており、これによりアジア太平洋地域のエポキシ接着剤市場は世界平均を上回る成長を遂げると見込まれます。自動車メーカーが溶接に代わって軽量複合材の接着を採用する中、2液型反応系製品は引き続き価格決定力を維持しています。一方、厳格な室内空気質規制により、建設プロジェクトでは常温に近い温度で硬化する低VOC硬化剤への移行が進んでいます。主要な化学メーカーは、電気自動車用バッテリー、フォトニクス・チプレット、高層ビルのファサードパネル向けの配合開発サイクルを短縮するため、地域研究所の規模を拡大しており、この変化により、現地のアプリケーションエンジニアリングに強みを持つ企業に競争上の優位性が傾いています。

アジア太平洋地域のエポキシ接着剤市場の動向と洞察

急増するEVおよび自動車の軽量化生産

アジア太平洋地域では、電気自動車(EV)の製造工場において、バッテリーモジュール、セル・トゥ・パック(CTP)システム、アルミニウム複合材ボディパネルなど、様々な部品向けに接着剤ソリューションの採用が拡大しています。この動向は、特に自動車メーカーが車両総重量を15~20%削減することを目指していることから、同地域のエポキシ接着剤市場を後押ししています。BYD、現代自動車、LGエナジーソリューションといった業界大手による大規模な投資が、数ギガワット時のバッテリー容量拡大を牽引しています。これらのバッテリーには、高い熱伝導率と急速な初期強度で知られる隙間充填用エポキシが採用されています。さらに、室温で最大6ヶ月間保存可能な、新たに商品化された銀ペーストエポキシは、炭化ケイ素パワーモジュールの製造に革命をもたらしています。従来の焼結工程を省くことで、この革新技術はインバーターの生産を効率化するだけでなく、エネルギー消費を最大40%削減します。

急速なインフラ整備と高層建築

2025年、アジア太平洋地域の各国政府は建設分野に5兆米ドル以上を投資しました。この都市化の急拡大により、ファサード用ガラス、アンカー用グラウト、補修用モルタルなどの需要が高まりましたが、これらはいずれも高靭性エポキシ樹脂に依存しています。さらに、5℃から10℃の範囲で硬化可能な新開発の低温硬化剤が、冬季のコンクリート打設に革命をもたらしています。この革新技術は、中国北部の建設現場やインドの高地鉄道プロジェクトにおいて特に有益であり、高価な加熱ブランケットの使用を不要にします。

ビスフェノールAおよびエピクロロヒドリン原料の価格変動

長期の樹脂契約を持たない中堅のコンパウンドメーカーは、四半期ごとの価格変動が20%を超えるため、利益率の圧迫に直面しています。この制約を克服するため、東南アジアのいくつかの加工業者はバイオベースのエポキシ樹脂への転換を進めています。ロジンやカルダノールを原料とするこれらのエポキシ樹脂は、価格が30%割高であるもの、230°Cを超えるガラス転移温度を誇ります。

セグメント分析

電子機器および半導体用途は、CAGR6.58%のペースで拡大しています。新竹やクリムを含む各地域でパワーデバイスやフォトニックモジュールの製造工場が出現していることから、このセグメントは自動車セクターを上回っています。しかし、自動車セクターは依然として最大の貢献源であり、23.18%のシェアを占めています。このセグメントにおけるアジア太平洋地域のエポキシ接着剤市場は、車体構造、バッテリーパック、パワートレインへの用途を牽引役として、成長を続けています。

高周波窒化ガリウムおよび炭化ケイ素デバイス分野は、体積熱伝導率が150 W/m-Kを超える銀充填エポキシ樹脂への需要を牽引しています。この動向により、化学品サプライヤーと基板メーカー間の研究開発(R&D)協力が強化されています。さらに、建設、エネルギー、船舶の各セグメントでは、総じて安定した需要が維持されています。インフラへの政府投資は、橋梁、風力発電用ブレード、船体の改修などのプロジェクトに重点が置かれており、これらはいずれも高弾性率の接着を必要としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EVおよび自動車の軽量化製造の急増

- インフラおよび高層建築への急速な投資

- 電子機器および半導体組立の拡大

- 国内の航空機プログラムでは、現地化された資格要件が採用されています

- アンチダンピング関税が後方統合を促進

- 市場抑制要因

- BPAおよびECH原料価格の変動

- 溶剤系製品に対する厳格なVOCおよび室内空気質(IAQ)規制

- 水性エポキシ樹脂の性能格差とコストプレミアム

- バリューチェーン分析

- 流通チェーン分析

- 規制情勢

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 流通チャネル分析

第5章 市場規模と成長予測

- エンドユーザー業界別

- 航空宇宙・防衛

- 自動車

- 船舶

- 電気・電子

- 建設

- エネルギー・電力

- その他の最終用途産業

- 技術別

- 反応性

- 溶剤系

- UV硬化型

- 水性

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Dow Inc.

- Dymax Corporation

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials(Group)Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日