|

市場調査レポート

商品コード

1693392

フランスのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)France Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| フランスのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 158 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

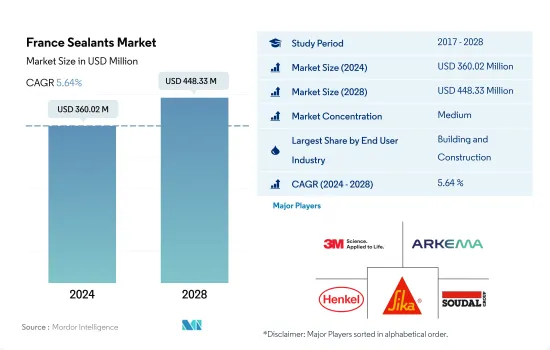

フランスのシーラント市場規模は2024年に3億6,002万米ドルと推定され、2028年には4億4,833万米ドルに達すると予測され、予測期間(2024年~2028年)のCAGRは5.64%で成長すると予測されています。

住宅建設の増加がシーラントの成長を促進

- フランスのシーラント市場は、シーラントの防水、耐候性シーリング、ひび割れシーリング、接合部シーリングの用途により、主に建設業界が牽引しています。フランスの建設産業は2021年に数量で10.5%急増し、シーラントの需要を増加させました。住宅の急成長と老朽化した住宅の維持管理は、予測期間中、フランスのシーラント需要を絶えず促進すると予想されます。

- その他のエンドユーザー産業セグメントは、電子・電気機器製造業におけるポッティングや保護材などの多様な用途により、フランスのシーラント市場で2番目に大きなシェアを占めると思われます。特に、センサーやケーブルのシールに使用されています。フランスのエレクトロニクス市場は、ここ数年安定した成長を記録しており、予測期間中もシーラントの需要を創出し続けることが予想されます。家庭用電化製品分野は、2027年までのCAGRが1.39%になる見込みです。また、持続可能でエネルギー効率に優れた用途として、機関車、海洋、DIY産業におけるシーラント需要の高まりが、予測期間中の市場シェアを押し上げると予想されます。

- シーラントはヘルスケアと自動車産業でかなりの用途があり、フランスは数十年にわたってこれらの分野で大きく発展してきました。ヘルスケアでは主に医療機器の組み立てやシールに使用されています。また、自動車分野では、ガラス、金属、プラスチック、塗装面など様々な基材にシーラントが使用されており、主にエンジンや自動車のガスケットに使用されています。これらの要因により、予測期間中、フランスにおけるシーラントの需要は増加すると予想されます。

フランスのシーラント市場動向

2024年のオリンピック開催がフランスの建設セクターを後押し

- フランスは欧州で2番目に大きな建設産業国です。同国の建設指数は緩やかな成長を示しており、過去数年間は業界売上高指数が緩やかに上昇しています。同国の建設産業は、8年もの長きにわたる衰退を経て、最近になって勢いを増しています。

- 2020年、建設部門は大幅な落ち込みを見せ、総建設生産高と新規受注高は大幅に減少しました。COVID-19パンデミックの深刻な影響により、フランスの建設産業の成長率は-12%以上低下しました。

- フランスの総建設生産高は、2021年第4四半期に2020年第4四半期比で0.2%減少し、前年同期比で1.2%減少しました。2021年12月の同国の建設業生産は前年同月比2.6%減、2021年11月比7%減となり、市場の需要が減少しました。

- しかし、フランス国内の総建設業生産は2022年第1四半期に2021年第1四半期比で0.9%増加し、前年同期比で2.6%増加しました。2022年4月の同国の建設業生産は、前年同月比1.5%増、2022年3月比1.2%増でした。パンデミックからの住宅建設セクターの回復と、来る2024年のオリンピックが、予測期間中の市場を牽引すると予測されます。

- したがって、上記のすべての要因は、調査された市場に影響を与えると予想されます。

2035年までの自動車排出量ネットゼロに加え、電気自動車登録台数の増加が自動車生産を促進する可能性が高い

- フランスの自動車産業は、欧州の他の主要国と比べてはるかに好調です。自動車生産台数は2018年まで継続的な成長を遂げたが、自動車市場がCOVID-19パンデミックの悪影響を受けたため、2019年にはさらに8.3%の減少を示しました。

- 2020年の自動車および小型商用車の生産台数は、2019年の217万5,350台に対して131万6,371台となり、39.5%の減少を記録しました。パンデミックにより、国内各地の製造部門は一時的な操業停止を余儀なくされました。原材料の供給が限られていたことも、自動車部門が直面する課題に拍車をかけた。

- 2021年には、同国のプラグイン電気自動車の新規登録台数は31万5,000台を超え、2020年比で62%の成長率を記録し、フランスにおける電気自動車セグメントの需要を高めました。それに伴い、2022年3月の電気自動車の市場シェアは前年同月比16.1%から21.4%に上昇しました。

- フランスの自動車業界は、2035年から内燃エンジン車の生産を禁止するという欧州議会の採決を全会一致で非難しました。同国は、2035年までに自動車排出量ネットゼロを達成する計画であり、予測期間中、同国の自動車市場を牽引する可能性が高いです。

フランスのシーラント産業概観

フランスのシーラント市場は中程度に統合されており、上位5社で43.64%を占めています。この市場の主要企業は以下の通りです。 3M, Arkema Group, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- フランス

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- ヘルスケア

- その他のエンドユーザー産業

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- CERMIX

- Dow

- Henkel AG & Co. KGaA

- ISPO Group

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

- Soudal Holding N.V.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92448

The France Sealants Market size is estimated at 360.02 million USD in 2024, and is expected to reach 448.33 million USD by 2028, growing at a CAGR of 5.64% during the forecast period (2024-2028).

Growing construction in residential sector to foster the growth of sealants

- The French sealants market is driven mainly by the construction industry due to applications of sealants waterproofing, weather-sealing, crack-sealing, and joint-sealing. The construction industry of France surged by 10.5% in 2021 in volume, which increased the demand for sealants. The rapid growth of residential dwellings and maintenance of aged housing are expected to constantly foster the demand for sealants in France over the forecast period.

- The other end-user industries segment will likely account for the second-largest share in the French sealants market owing to the diverse applications in the electronics and electrical equipment manufacturing industry for potting and protecting materials. They are used for sealing sensors and cables, among others. The French electronics market has registered steady growth over the few years, and it is expected to continue, creating demand for sealants over the forecast period. The consumer electronics segment will likely register a CAGR of 1.39% up to 2027. In addition, the rising demand for sealants in the locomotive, marine, and DIY industries for sustainable and energy-efficient applications is expected to boost the market share over the forecast period.

- Sealants have considerable applications in the healthcare and automotive industries, and France has developed significantly in these sectors over the decades. They are used in healthcare primarily for assembling and sealing medical devices. The automotive sector also exhibits significant application of sealants to various substrates, such as glass, metal, plastic, and painted surfaces, and is mainly used in engines and car gaskets. These factors are expected to augment the demand for sealants in France over the forecast period.

France Sealants Market Trends

Hosting the 2024 Olympics is likely to boost the construction sector in the country

- France has the second-largest construction industry in the European region. The construction index in the country witnessed slow growth, with a gradual increase in the industry turnover index over the past few years. The construction industry in the country recently gained momentum after eight long years of decline.

- In 2020, the construction sector witnessed a huge decline, with the total construction output and new orders declining considerably. The growth of the French construction industry fell by over -12% due to the severe impact of the COVID-19 pandemic.

- The total construction production in France declined by 0.2% in Q4 2021 compared to Q4 2020 and by 1.2% compared to the previous quarter in the same year. In December 2021, the country's production from the construction industry declined by 2.6% compared to the same month in the previous year and declined by 7% compared to November 2021, decreasing the demand for the market.

- However, the total construction production in France increased by 0.9% in Q1 2022 compared to Q1 2021 and by 2.6% compared to the previous quarter of the same year. In April 2022, the country's production from the construction industry increased by 1.5% compared to the same month in the previous year and increased by 1.2% compared to March 2022. The recovery of the residential construction sector from the pandemic and the upcoming 2024 Olympics are estimated to drive the market during the forecast period.

- Therefore, all the abovementioned factors are expected to impact the market studied.

In addition to net-zero vehicle emissions by 2035, electric vehicle registrations growth is likely to propel the automotive production

- The automotive industry in France has fared much better compared to other major European economies. Automotive vehicle production experienced continuous growth till 2018 and further exhibited a decline of 8.3% in 2019, as the automotive market was negatively affected by the COVID-19 pandemic.

- In 2020, the country produced 1,316,371 cars and light commercial vehicles compared to 2,175,350 vehicles produced during 2019, recording a decline of 39.5%, as production came to a halt in 2020 due to the COVID-19 pandemic. The pandemic forced the temporary shutdown of manufacturing units across different parts of the country. Limited raw material supply added to the challenges faced by the automobile sector.

- In 2021, the country's new plug-ins electric vehicle registration stood at over 315,000, registering a growth rate of 62% compared to 2020, enhancing the demand of the electric vehicle segment in France. Along with it, electric vehicles registered a 21.4% market share in March 2022, up from 16.1% Y-o-Y.

- The French car industry has unanimously condemned the European Parliament's vote to ban the production of combustion engine cars from 2035. The country plans to achieve net-zero vehicle emissions by 2035, which is likely to drive the automotive vehicle market in the country over the forecast period.

France Sealants Industry Overview

The France Sealants Market is moderately consolidated, with the top five companies occupying 43.64%. The major players in this market are 3M, Arkema Group, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 France

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 CERMIX

- 6.4.4 Dow

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 ISPO Group

- 6.4.7 MAPEI S.p.A.

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms