|

市場調査レポート

商品コード

1693382

スペインの接着剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Spain Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインの接着剤:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

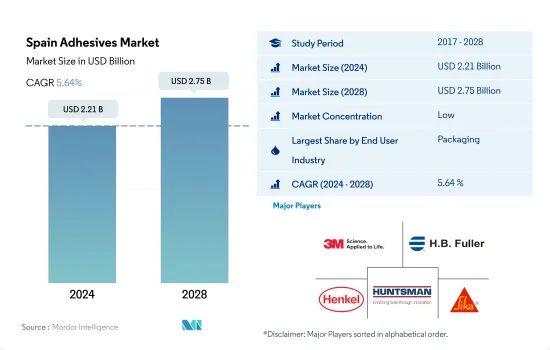

スペインの接着剤市場規模は2024年に22億1,000万米ドルと推定・予測され、2028年には27億5,000万米ドルに達し、予測期間中(2024~2028年)にCAGR 5.64%で成長すると予測されています。

軟質包装の新たな動向がスペインの接着剤消費を押し上げる見込み

- 接着剤は、様々な産業で使用される様々な基材を接着・接合する上で重要な役割を果たしています。これらの接着剤は、メーカーがコンポーネントやアセンブリの重量を軽減し、迅速、簡単かつ正確に接合を形成するのに役立ちます。2020年にCOVID-19が発生した結果、消費量は2019年と比較して8.91%減少しました。

- 2021年の接着剤消費量は、様々なエンドユーザー産業の包装用途の成長により、41万1,363トン以上増加しました。2020年のカートンボードの生産量は、いくつかの課題にもかかわらず32万1,600トンに達しました。さらに、スペインの食品包装量は2022年まで0.3%の割合でかなりの成長が見込まれます。包装された肉や魚介類、加工された果物や野菜の需要の増加、トマトペーストやピューレ用の液体カートンの普及といった要因が、今後数年間、軟包装における接着剤消費を促進すると予想されます。水性接着剤はコストが安く、これらの用途で必要とされる接着強度が高いため、産業で消費量が多いです。2021年には、国内の包装産業で20万1,000トン近くの水性接着剤が消費されると見られています。

- 現在進行中のいくつかのインフラプロジェクトが、国内の接着剤需要を押し上げています。2019年、Amazon Web Services(AWS)はスペインに新しいインフラ地域を立ち上げ、欧州で7番目の地域となりました。さらに、住宅建設は予測期間の後半にかけて大きく成長すると予想されています。スペイン国家統計局(INE)によると、2019~2025年にかけて、純世帯建設は毎年平均約13万5,000戸のペースで増加すると予想されています。これはスペインの接着剤市場に影響を与えると予想されます。

スペインの接着剤市場動向

プラスチックのリサイクル性の先進包装と飲食品産業からの需要で、プラスチック包装が包装産業をリードする

- 包装は、製品の安全性と長寿命を保護・強化するためのデザインと技術の面で、最も急成長している産業のひとつです。スペインの包装産業は、近年の飲食品産業の急成長によって大きく牽引されています。農業食品産業はスペインで最も有望なセグメントであり、欧州で4番目に大きい農業食品市場であり、30,000社以上の企業が存在します。自国ブランドの先進的プロモーションにより、スペインは世界の飲食品の主要輸出国としての地位を確立しています。

- COVID-19の大流行により、国を挙げての製造施設の閉鎖と一時的な操業停止は、サプライチェーンや輸出入の混乱など、いくつかの問題を引き起こしました。その結果、2020年の同国の包装生産量は前年比6%減となり、市場に大きな影響を与えました。同国の包装生産は主に紙と板紙が牽引しており、2021年に生産される包装の52%近くを占めます。しかし、プラスチックのリサイクル性が進んだことで、プラスチック生産部門は予測期間中にCAGR約4.27%の急成長を記録する可能性が高いです。

- スペインの包装産業の成長は、国内での生鮮食品需要の高まりと一致しています。パンデミック後の公衆衛生問題への関心の高まりは、全国的なeコマース活動の台頭とともに、食品加工産業の成長を後押しし、今後数年間の包装需要をさらに押し上げる可能性が高いです。

EV需要の増加と240億ユーロに相当する公的・民間Eモビリティ投資による自動車需要の増加

- スペインはドイツに次いで欧州第2位の自動車生産国です。スペインの自動車サプライヤーは2019年に358億2,200万ユーロ相当の製品を生産し、そのうち60%が欧州域内外に輸出されました。

- 同国の自動車生産はここ数年ほぼ一定しています。2019年、同国の生産台数は約2,822万2,355台で、2018年比0.1%の微々たる成長率を記録しました。2020年の同国の自動車生産台数は約226万8,185台でした。2020年の自動車生産台数は、COVID-19の大流行によりサプライチェーンが停止したため、18.6%減少しました。

- 2021年第1~3四半期の自動車生産台数は、2020年第1~3四半期比で4%増加し、159万2,277台に達しました。同国の自動車産業は、予測期間中、緩やかな需要となりそうです。しかし、2021年の同国の自動車生産台数は約209万8,133台で、2020年から8%減少しました。半導体チップ不足とサプライチェーンの制約が、同国の自動車生産台数に悪影響を及ぼしました。

- 自動車生産台数の不足は最近悪化しており、2022年には生産台数が18%増加し、力強い回復が見込まれます。スペインの電気自動車市場は、サプライヤーのeモビリティへのシフトを支援する次世代EU基金の恩恵を受けるはずです。さらにスペイン政府は、今後3年間で240億ユーロに相当する公的と民間のeモビリティ投資を発表しています。

スペイン接着剤産業概要

スペインの接着剤市場はセグメント化されており、上位5社で9.10%を占めています。同市場の主要企業は以下の通りです。3M、H.B. Fuller Company、Henkel AG & Co. KGaA、Huntsman International LLC、Sika AGなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- フットウェア皮革

- 包装

- 木工・建具

- 規制の枠組み

- スペイン

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- フットウェアと皮革

- 医療

- 包装

- 木工・建具

- その他

- 技術

- ホットメルト

- 反応性

- 溶剤系

- UV硬化型接着剤

- 水性

- 樹脂

- アクリル系

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- AC Marca

- AVERY DENNISON CORPORATION

- Beardow Adams

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Sika AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92437

The Spain Adhesives Market size is estimated at 2.21 billion USD in 2024, and is expected to reach 2.75 billion USD by 2028, growing at a CAGR of 5.64% during the forecast period (2024-2028).

Emerging trend of flexible packaging expected to boost the consumption of adhesives in Spain

- Adhesives play an important role in bonding and joining various substrates that are used across industries. These adhesives help manufacturers lower the weight of their components and assemblies and form joints quickly, easily, and accurately. As a result of the COVID-19 outbreak in 2020, consumption fell by 8.91% compared to 2019.

- Adhesive consumption increased by more than 411,363 ton in 2021 due to the growth of packaging applications among various end-user industries. In 2020, carton board production reached 321.6 thousand ton despite several challenges. Moreover, Spanish food packaging volume is expected to witness considerable growth at a rate of 0.3% through 2022. Factors such as rising demand for packaged meat and seafood, processed fruits and vegetables, and widespread usage of liquid cartons for tomato pastes and purees are expected to foster adhesives consumption in flexible packaging over the coming years. Waterborne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength which is required in these applications. It is seen that nearly 201 thousand tons of water-borne adhesives are consumed in the packaging industry of the country during 2021.

- Several ongoing infrastructure projects have boosted the demand for adhesives in the country. In 2019, Amazon Web Services (AWS) launched a new infrastructure region in Spain, making it its seventh region in Europe. Moreover, residential construction is expected to grow significantly over the later parts of the forecast period. According to Spain's National Statistics Institute (INE), net household construction is anticipated to increase at an average pace of around 135,000 units annually from 2019 to 2025. This is expected to influence the market for adhesives in Spain.

Spain Adhesives Market Trends

With the advancement in plastic recyclability and demand from the food and beverage industry, plastic packaging to lead the packaging industry

- Packaging is one of the fastest-growing industries in terms of design and technology for protecting and enhancing products' safety and longevity. The Spanish packaging industry has been majorly driven by the rapid growth of the food and beverages industry in recent years. The agri-food industry is the most promising sector in Spain and the fourth-largest agri-food market in Europe, with over 30,000 companies. Owing to the high-level promotion of country brands, Spain has positioned itself as a major exporter of food and drinks worldwide.

- Due to the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including disruptions in supply chains and imports and exports. As a result, the country's packaging production declined by 6% in 2020 compared to the previous year, significantly affecting the market. Packaging production is majorly driven by paper and paperboard in the country, which accounts for nearly 52% of the packaging produced in 2021. However, with the advancement of plastic recyclability, the plastic production segment is likely to register the fastest growth of around 4.27% CAGR during the forecast period.

- The growth of the packaging industry in Spain is in line with the growing demand for fresh food domestically. The growing interest in public health issues post-pandemic, along with the emerging e-commerce activities across the nation, is likely to boost the growth of the food processing industry and further drive the demand for packaging over the coming years.

Increasing EVs demand and government investment of public and private e-mobility investments worth EUR 24 billion to boost the automotive demand

- Spain is the second-largest automobile producer in Europe, after Germany. Spanish automotive suppliers produced EUR 35,822 million worth of products in 2019, of which 60% were exported inside and outside the European region.

- Automobile production in the country has been almost constant in the past few years. In 2019, the country produced about 28,22,355 units, registering a meager growth rate of 0.1% over 2018. The country produced about 22,68,185 units of vehicles in 2020. Automotive vehicle production contracted by 18.6% in 2020 as the COVID-19 pandemic halted the supply chain.

- In the first three quarters of 2021, automotive production increased by 4% over Q1-Q3 of 2020 and reached 1,592,277 vehicles. The country's automotive industry is likely to witness moderate demand during the forecast period. However, in 2021, the country produced about 2,098,133 vehicles, which was a decline of 8% from 2020. The semiconductor chip shortage and supply chain restrictions negatively affected the production of automotive vehicle units in the country.

- The automotive production shortfalls have recently worsened, and a strong rebound is expected in 2022, with output increasing by 18%. The Spanish electric vehicles market should benefit from the Next Generation EU fund, which supports suppliers in their shift toward e-mobility. Additionally, the Spanish government has announced public and private e-mobility investments worth EUR 24 billion over the coming three years.

Spain Adhesives Industry Overview

The Spain Adhesives Market is fragmented, with the top five companies occupying 9.10%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Spain

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Cyanoacrylate

- 5.3.3 Epoxy

- 5.3.4 Polyurethane

- 5.3.5 Silicone

- 5.3.6 VAE/EVA

- 5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 AC Marca

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Beardow Adams

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms