|

市場調査レポート

商品コード

1692586

航空宇宙用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Aerospace Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空宇宙用接着剤とシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 329 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

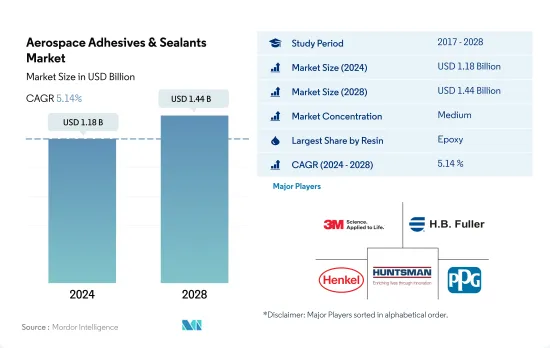

航空宇宙用接着剤とシーラント市場規模は、2024年に11億8,000万米ドルと推定され、2028年には14億4,000万米ドルに達すると予測され、予測期間(2024-2028年)のCAGRは5.14%で成長する見込みです。

コスト削減と効率向上のため、より重い組立継手の交換需要の高まりが市場需要を押し上げると予想される

- 接着剤とシーラントは、軽量航空機の組み立てにおいて重要な役割を果たします。そのため、制御システム、ナセルシステム、機体、エンジン部品など、多くの構造用途で使用されています。

- 航空宇宙用接着剤とシーラントは、2021年に数量ベースで7.45%の急成長を示しました。これは、景気回復、原材料の定期的な供給、米国、カナダ、ドイツ、中国を含む多くの国々での生産施設の再開によるもので、2020年に発生したCOVID-19の影響により、各国でのロックダウンが生産施設の停止を引き起こし、接着剤とシーラントの成長が世界中で減少しました。

- 航空宇宙用接着剤とシーラントは、様々な樹脂をベースにしており、エポキシ樹脂は、航空機メーカーの正確な要件を満たすその優れた構造特性により、航空宇宙用途で最も使用されている樹脂ベースの接着剤です。エポキシ接着剤は、機体構造に使用されるサンドイッチパネル、エッジ接着や空隙充填、ハニカム構造、その他多くの用途など、航空機の内外装部品の両方で使用されています。これらの接着剤の引張強度は、他のすべての接着剤の中で最も高い12000psi(82MPa)にまで達します。

- そのような航空機の重量を減らすために、メカニカルファスナー、ネジ、溶接継手などの重い組立継手の交換のための需要の高まりは、最終的に燃料コストを下げるのに役立ちます。航空会社による燃料費への支出は、過去10年間でほぼ40%削減されています。そのため、今後数年間は接着剤とシーラントの需要が高まると思われます。

炭素削減のための革新的技術開発が市場需要を押し上げる

- 欧州では、民間および軍用のヘリコプター、航空機、ジェット機、およびそれらの部品の製造と輸出が行われています。民間航空は欧州の航空宇宙産業で最大の分野です。欧州には3,000社以上の企業があり、88万人以上の従業員が働いています。フランス、ドイツ、イタリア、スペイン、英国には航空宇宙企業が集中しています。そのため、欧州は航空宇宙用接着剤とシーラントの消費量で第2位にランクされています。

- 近年、北米および世界の航空宇宙産業は、脱炭素化の圧力に直面しています。これは、炭素を削減するための革新的な技術開発によって実現できます。この移行は、予測期間である2022-2028年に新技術の適応に使用される航空宇宙用接着剤とシーラントの需要増加につながります。

- 前年比成長率が2021年に最も高くなるのは、2020年にCOVID-19が封鎖されたことで国際旅行と国内旅行が長期にわたって停止したため、パンデミック後にレジャー観光が盛り上がったためです。例えば、北米発着の国際線旅客数は2020年の4,100万人から2021年には5,900万人に増加します。この増加はMROビジネスと航空機アフターマーケットの増加につながり、これが2021年の前年比成長率が最も高い理由です。

- 2020年の航空宇宙用接着剤とシーラント需要の減少は、全国的な封鎖を引き起こしたCOVID-19パンデミックの影響、全体的な景気減速、国際・国内航空旅行の禁止によるものです。例えば、北米発着の国際線旅客数は2019年の1億5,900万人から2020年には4,100万人に激減しました。

世界の航空宇宙用接着剤とシーラント市場動向

民間航空と軍事航空の急成長が航空機生産を押し上げる

- 世界の航空宇宙産業は、北米、アジア太平洋、欧州に大きく支配されています。米国は、技術的に洗練された航空機、宇宙システム、軍用機の設計、開発、生産能力により、航空宇宙産業の世界的リーダーであると同時に地域的リーダーでもあります。2021年には、2020年の1,807機に対し、民間機、一般機、軍用機を含む合計約1,956機の航空機が同国に納入されました。2028年には2,269機の航空機が必要になると予測されています。

- アジア太平洋地域では、中国が民間航空宇宙および航空サービスの最大かつ最も急成長している市場です。2021年には航空機の納入が減少し、民間、一般、軍用の航空機の合計で約264機を記録し、2020年の367機と比較しました。しかし、2028年には回復し、969機に達すると予測されています。

- 欧州では、ドイツは最大級の航空宇宙産業を有し、相手先ブランド製造業者(OEM)、Tier I サプライヤー、システムインテグレーターが存在します。2021年には航空機の納入が増加し、2020年の98機に対し、民間機、一般機、軍用機の合計で約138機に達します。2028年には262機に達すると予測されています。2021年の航空宇宙産業の収益は314億ユーロでした。2020年と2021年には、民間航空が最も高い収益を上げる部門となり、2019年の320億ユーロに対し、両年とも約220億ユーロとなりました。しかし、市場が回復するのは2024年から2025年にかけてと予想されます。

- 上記の要因はすべて、予測期間中に世界の航空宇宙産業に影響を与えると予想されます。

航空宇宙用接着剤とシーラント業界の概要

航空宇宙用接着剤とシーラント市場は適度に統合されており、上位5社で58.97%を占めています。この市場の主要企業は以下の通り。 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and PPG Industries, Inc.(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- 中国

- EU

- インド

- インドネシア

- 日本

- マレーシア

- メキシコ

- ロシア

- サウジアラビア

- シンガポール

- 南アフリカ

- 韓国

- タイ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 樹脂

- アクリル

- シアノアクリレート

- エポキシ

- ポリウレタン

- シリコーン

- VAE・EVA

- その他の樹脂

- テクノロジー

- ホットメルト

- 反応性

- シーラント

- 溶剤系

- UV硬化型接着剤

- 水系

- 地域

- アジア太平洋地域

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他アジア太平洋地域

- 欧州

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他欧州

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- アルゼンチン

- ブラジル

- その他南米

- アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- Beacon Adhesives, Inc.

- Chemique Adhesives & Sealants Ltd

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Master Bond Inc.

- Permabond LLC.

- PPG Industries, Inc.

- Solvay

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Aerospace Adhesives & Sealants Market size is estimated at 1.18 billion USD in 2024, and is expected to reach 1.44 billion USD by 2028, growing at a CAGR of 5.14% during the forecast period (2024-2028).

The rising demand for the replacement of heavier assembly joints to reduce costs and improve efficiency is expected to boost market demand

- Adhesives and sealants play an important role in lightweight aircraft assemblies. Therefore, they are used in many structural applications, such as control systems, nacelle systems, fuselages, and engine parts.

- The aerospace adhesives and sealants have shown a sudden growth of 7.45% in terms of volume in 2021. This has happened due to the economic recovery, regular supply of raw materials, and reopening of production facilities in many countries, including the United States, Canada, Germany, and China, which were impacted by the COVID-19 outbreak in 2020 where lockdowns in countries caused the shutdown of production facilities and reduction in the growth of adhesives and sealants across the world.

- Aerospace adhesives and sealants are based on various resins, and epoxy resin is the most used resin-based adhesive in aerospace applications owing to its excellent structural properties, which fulfill the exact requirement of aircraft manufacturers. Epoxy adhesives are used in both interior and exterior parts of aircraft, such as sandwich panels used in fuselage construction, edge bonding and void filling, honeycomb structures, and many other applications. The tensile strength of these adhesives is up to 12000 psi(82 MPa) which is the highest among all other adhesives.

- The rising demand for the replacement of heavier assembly joints, such as mechanical fasteners, screws, and weld joints, to lower the weight of air vehicles will ultimately help in lowering fuel costs. It is seen that expenditure on fuel costs by airlines has been reduced by almost 40% over the last decade. Thus, it will drive the demand for adhesives and sealants in the coming years.

Demand for innovative technology development for reducing carbon to boost market demand

- European manufactures and exports both civil and military helicopters, aircraft, jets, and their components. Civil aviation is the largest segment in the European aerospace industry. Europe is home to over 3,000 companies with more than 880,000 employees. France, Germany, Italy, Spain, and the United Kingdom have a large concentration of aerospace companies. That is why Europe ranks second in the consumption of aerospace adhesives and sealants.

- In recent years, the aerospace industry in North America and worldwide has been facing pressure for decarbonization. This can be done through innovative technology development for reducing carbon. This transition will lead to an increase in demand for aerospace adhesives and sealants, which will be used for adapting new technology in the forecast period, which is 2022-2028.

- The year-on-year growth is highest in 2021 because of the post-pandemic boost in leisure tourism, as the lockdown in COVID-19 in 2020 put a long halt on international and domestic travel. For example, the number of international passengers traveling to and from North America increased from 41 million passengers in 2020 to 59 million passengers in 2021. This increase led to increasing in MRO business and aircraft aftermarket, which is the reason for the highest year-on-year growth in 2021.

- The decline in demand for aerospace adhesives and sealants in 2020 is due to the impact of the COVID-19 pandemic, which caused a nationwide lockdown, an overall economic slowdown, and a ban on international and domestic air travel. For example, the number of international passengers flying to and from North America fell drastically from 159 million in 2019 to 41 million in 2020.

Global Aerospace Adhesives & Sealants Market Trends

Rapid growth of civil and military aviation will boost the aircraft production

- The global aerospace industry is largely dominated by North America, Asia-Pacific, and Europe. The United States is both a global and regional leader in the aerospace industry due to its design, development, and production capabilities of technologically sophisticated aircraft, space systems, and military aircraft. In 2021, a total of around 1,956 units of aircraft, including civil, general, and military, were delivered to the country, compared to 1,807 units in 2020. It is forecast that the country may need 2,269 units of aircraft by 2028.

- In the Asia-Pacific region, China is the largest and fastest-growing market for civil aerospace and aviation services. In 2021, the country experienced a decline in aircraft deliveries, registering around 264 units of total aircraft in civil, general, and military, compared to 367 units delivered in 2020. However, it is forecast to recover and reach 969 units in 2028.

- In Europe, Germany has one of the largest aerospace industries, with the presence of original equipment manufacturers (OEMs), Tier I suppliers, and systems integrators. In 2021, the country saw an increase in aircraft deliveries, amounting to around 138 units of total aircraft in civil, general, and military, compared to 98 units in 2020. The market is projected to reach 262 units in 2028. In 2021, the aerospace industry's revenue stood at EUR 31.4 billion. In 2020 and 2021, civil aviation was the highest revenue-generating sector, amounting to around EUR 22 billion in both years, compared to EUR 32 billion in 2019. However, the market is not expected to recover until 2024-2025.

- All the abovementioned factors are expected to impact the global aerospace industry during the forecast period.

Aerospace Adhesives & Sealants Industry Overview

The Aerospace Adhesives & Sealants Market is moderately consolidated, with the top five companies occupying 58.97%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and PPG Industries, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV Cured Adhesives

- 5.2.6 Water-borne

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Singapore

- 5.3.1.8 South Korea

- 5.3.1.9 Thailand

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 United Kingdom

- 5.3.2.7 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Saudi Arabia

- 5.3.3.2 South Africa

- 5.3.3.3 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Beacon Adhesives, Inc.

- 6.4.5 Chemique Adhesives & Sealants Ltd

- 6.4.6 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International LLC

- 6.4.11 Illinois Tool Works Inc.

- 6.4.12 Master Bond Inc.

- 6.4.13 Permabond LLC.

- 6.4.14 PPG Industries, Inc.

- 6.4.15 Solvay

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms