|

市場調査レポート

商品コード

1692577

欧州のEVA接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe EVA Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のEVA接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 191 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

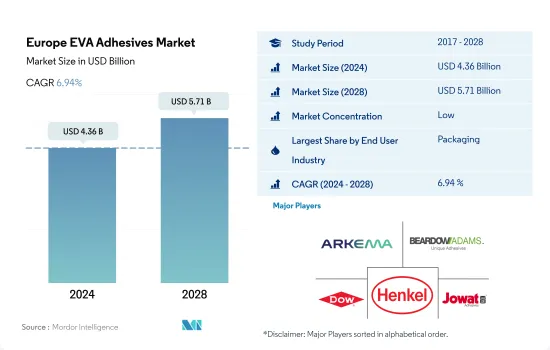

欧州のEVA接着剤市場規模は2024年に43億6,000万米ドルと推定・予測され、2028年には57億1,000万米ドルに達し、予測期間(2024-2028年)のCAGRは6.94%で成長すると予測されます。

パッケージングが最も急成長しているエンドユーザーであり、市場のポールポジションを維持します。

- EVA接着剤は、包装、自動車、木工・建具、建築・建設など、さまざまなエンドユーザー産業で応用されています。これらの接着剤は、紙、木材、プラスチック、ゴム、金属、皮革などの基材を接着することができます。EVA接着剤の主な用途としては、紙/カードストック箱、パッケージ・ラベリング、カートン・シーリング、組立、自動車内装、紙変換などが挙げられます。

- EVA接着剤の需要は2017年から2019年にかけて大きく伸びた。スペインの建築・建設業界は、この地域のすべての国のすべてのエンドユーザー業界の中で、需要の最も高い成長(2017~2019年のCAGR 11.07%)を示しました。住宅部門からの需要の増加がスペインでのこの成長を促進しました。

- 2020年、EVA接着剤の需要は、操業や貿易の制限、サプライチェーンの制約、COVID-19パンデミックによる労働力不足など様々な要因により、すべてのエンドユーザー産業から減少しました。自動車産業からの需要が最も苦しく、前年同期比19.16%減少しました。旅行活動の減少、原材料不足、その他の様々な要因もこの減少につながりました。COVID-19パンデミックによる規制が緩和されるにつれて、EVA接着剤の世界需要は2021年にはパンデミック前の水準まで回復しました。

- この成長動向は予測期間2022-2028年も続くと予想されます。数量ベースでは、すべてのエンドユーザー産業を合わせたEVA接着剤の需要は、予測期間中に3.61%のCAGRで推移すると予想されます。包装産業は、その速硬化特性のために他のものよりもEVA接着剤を好むため、需要の最も高いシェアを占めています。2022-2028年の予測期間中、最大のエンドユーザーであり続けると予想されます。

2022年、欧州の新設床面積は前年比4.10%増となり、EVA接着剤の需要を押し上げる

- EVA樹脂ベースの接着剤は、酢酸ビニルやその誘導体などのポリマーで作られています。これらのポリマーは優れた耐熱性を示すため、主にホットメルト技術に基づく接着剤として使用されています。これらの接着剤は、建築、自動車、電子機器など6つ以上の地域の産業で使用されています。これらの接着剤は、その不揮発性の性質が建設産業での使用に安全であるため、主に建築・建設産業で消費されています。同市場は建設業界の成長により成長を遂げており、欧州の建築物の新規床面積は2021年の73億平方メートルから2022年には76億平方メートルに達すると見られています。

- その他欧州の地域セグメントは、欧州のEVA樹脂系接着剤市場で大きなシェアを占めています。その他欧州は、スウェーデン、ノルウェー、ポーランド、オランダなどの国々で構成されており、EVA樹脂系接着剤は主に建設用途で消費されています。ポーランドの住宅建設は2021年に2020年比で30%増加し、これもEVA樹脂系接着剤の需要を押し上げると予想されます。

- ドイツは、建設、ヘルスケア、自動車産業の増加により、EVA樹脂系接着剤の主要な消費国となっています。EVA樹脂ベースの接着剤は、屋根の補修や自動車の組み立てなど多くの用途に使用できる強力な構造特性により人気があります。2020年には約20万5,000件のプロジェクトが完了し、自動車生産台数は2021年の330万台から2022年には2.94%増加すると予想されています。したがって、欧州のEVA接着剤市場は、2022年と2023年にそれぞれ数量ベースで6.90%と5.60%の成長率を記録すると予想されます。

欧州EVA接着剤市場動向

欧州における飲食品産業の著しい成長により包装産業が拡大

- 包装は欧州地域の主要分野の一つです。同地域は世界第2位の包装製品生産国で、アジア太平洋地域に次いで世界の包装生産量の約24%を占めています。ドイツ、ロシア、スペイン、英国は欧州における包装製品の主要生産国です。COVID-19パンデミックの影響により、2020年の包装生産は2019年に比べ7.14%減少したと見られます。この年、いくつかの国によって全国的な封鎖が行われ、この地域の生産設備は3~4ヶ月間停止しました。

- ロシアは包装製品の主要生産国で、2021年には2億1,380万トンを生産し、これは欧州で最高です。ロシアの包装産業は、近年の飲食品産業の急成長によって大きく牽引されてきました。ロシアは世界の食品の主要輸出国であり、様々な最終用途産業にわたる洗練されたパッケージングへのニーズを満たすために、パッケージング販売にさらなる影響を与えています。

- ドイツは欧州におけるプラスチック包装の主要生産国です。プラスチック包装は2021年に生産される包装の約79%を占める。プラスチック包装産業は、主に国内の飲食品産業の急成長によって牽引されています。同地域では、より多忙なライフスタイル、より大きな消費力、および関連要因の増加に伴い、素早く持ち運べるパッケージ製品の需要が増加しています。この動向は、今後数年間、欧州の包装製品で高まると思われます。

電気自動車を推進する政府の支援策が産業規模を拡大する

- 欧州の一人当たりGDPは3万4,230米ドルで、2022年の成長率は前年比1.6%です。自動車産業部門がGDP全体に占める割合は約2%です。2021年の欧州の自動車生産台数は、乗用車81%、商用車17%、その他2%です。

- 2020年には、ドイツ、イタリア、スペイン、ロシア、英国など多くの欧州諸国がCOVID-19パンデミックの影響を受けました。パンデミックはサプライチェーンの混乱、各国での操業停止、チップ不足をもたらし、欧州の自動車生産に影響を与えました。自動車の生産台数は2019年比で22%も激減しました。

- 米国は欧州から25.3%相当の自動車を輸入しており、2021年にはドイツが10.3%、英国が4.7%を占める主要輸入国のひとつとなりました。2022年初頭、ロシアによるウクライナ侵攻により新車販売が20.5%減少し、それが自動車生産にも反映されました。2022年第1四半期の欧州自動車市場は、前年同期比で10.6%減少しました。

- 自動車生産台数は、多くの欧州諸国が電気自動車に新たな投資を行っているため、期間中(2022~2027年)にCAGR 2.25%で成長する可能性が高いです。例えば、スペインは電気自動車生産に51億米ドルを投資する予定です。

欧州EVA接着剤産業の概要

欧州EVA接着剤市場は細分化されており、上位5社で10.12%を占めています。この市場の主要企業は以下の通りです。 Arkema Group, Beardow Adams, Dow, Henkel AG & Co. KGaA and Jowat SE(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- 包装

- 木工・建具

- 規制の枠組み

- EU

- ロシア

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 履物・皮革

- ヘルスケア

- 包装

- 木工・建具

- その他のエンドユーザー産業

- テクノロジー

- ホットメルト

- 溶剤系

- 水性

- 国名

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arkema Group

- Beardow Adams

- Dow

- Follmann Chemie GmbH

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- KLEBCHEMIE M. G. Becker GmbH & Co. KG

- Paramelt B.V.

- Soudal Holding N.V.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92414

The Europe EVA Adhesives Market size is estimated at 4.36 billion USD in 2024, and is expected to reach 5.71 billion USD by 2028, growing at a CAGR of 6.94% during the forecast period (2024-2028).

Packaging is the fastest-growing end-user and to remain as pole position in market

- EVA adhesives find applications in various end-user industries, including packaging, automotive, woodworking and joinery, and building and construction. These adhesives can bond substrates like paper, wood, plastics, rubbers, metals, and leather. Some major applications of these adhesives are paper/card stock boxes, package labeling, carton sealing, assembly, vehicle interiors, and paper conversion.

- The demand for EVA adhesives grew significantly from 2017 to 2019. The Spanish building and construction industry witnessed the highest growth (CAGR of 11.07% for 2017-2019) in demand among all end-user industries from all countries in the region. Increased demand from the residential sector fueled this growth in Spain.

- In 2020, the demand for EVA adhesives declined from all end-user industries because of various factors such as operational and trade restrictions, supply chain constraints, and labor shortages due to the COVID-19 pandemic. The demand from the automotive industry suffered the most, declining by 19.16% Y-o-Y. Reduced travel activity, shortage of raw materials, and various other factors also led to this decline. As the COVID-19 pandemic-induced restrictions eased, the global EVA adhesives demand rose back to pre-pandemic levels in 2021.

- This growth trend is expected to continue during the forecast period 2022-2028. In volume terms, the demand for EVA adhesives from all end-user industries combined is expected to record a CAGR of 3.61% during the forecast period. The packaging industry favors EVA adhesives over others because of their fast-curing properties and, thus, accounts for the highest share of the demand. It is expected to remain the largest end-user during the forecast period 2022-2028.

The rising new floor area in Europe by 4.10% y-o-y in 2022 to boost the demand for EVA adhesives in the coming years

- EVA resin-based adhesives are made of polymers such as vinyl acetate and their derivatives. These polymers show good thermal resistance, which is why they are mainly used as hot melt technology-based adhesives. These adhesives are used in more than six regional industries, including construction, automotive, and electronics. These adhesives are consumed mainly in the building and construction industry as their non-volatile nature makes them safe for use in the construction industry. The market is witnessing growth due to growth in the construction industry, with the new floor area of Europe constructions set to reach 7.6 billion square footage in 2022 from 7.3 billion in 2021.

- The Rest of Europe regional segment occupies a major share of the European EVA resin-based adhesives market. The Rest of Europe consists of countries such as Sweden, Norway, Poland, and the Netherlands, where EVA resin-based adhesives are primarily consumed for construction applications. Residential construction in Poland increased by 30% in 2021 compared to 2020, which is also expected to boost the demand for EVA resin-based adhesives.

- Germany is the prime consumer of EVA resin-based adhesives owing to the rising construction, healthcare, and automotive industries. EVA resin-based adhesives are popular due to their strong structural properties, which can be used in many applications, such as roof repairing and automotive assemblies. About 205 thousand projects were completed in 2020, and vehicle production was expected to increase by 2.94% in 2022 from 3.3 million units in 2021. Thus, the European EVA adhesives market is expected to register growth rates of 6.90% and 5.60% by volume during 2022 and 2023, respectively.

Europe EVA Adhesives Market Trends

Significant growth of food & beverage industry in Europe to escalate packaging industry

- Packaging is one of the major sectors of Europe region. The region is the second-largest producer of packaging products in the world, which holds about 24% of global packaging production after the Asia-Pacific region. Germany, Russia, Spain, and the United Kingdom are major producers of packaging products in Europe. It is seen that packaging production reduced by 7.14% in 2020 compared to 2019 due to the impact of the COVID-19 pandemic. During the year, a nationwide lockdown imposed by several countries halted the production facilities for three to four months in the region.

- Russia is a leading producer of packaging products producing 213.8 million tons in 2021, which is the highest in Europe. The Russian packaging industry has majorly been driven by the rapid growth of the food and beverages industry in recent years. Russia is a major exporter of food products worldwide, which further influences packaging sales to meet the need for sophisticated packaging across various-end use industries.

- Germany is the major producer of plastic packaging in Europe. Plastic packaging which nearly accounts for around 79% of the packaging produced in 2021. The plastic packaging industry is majorly driven by the rapid growth of the food and beverages industry in the country. With the rise in busier lifestyles, greater spending power, and related factors in the region, the demand for quick and on-the-go packaged products is increasing. This trend will rise in packaging products in the coming years in Europe.

Supportive government initiatives to promote electric vehicles will raise the industry size

- Europe has a GDP of 34,230 USD per capita with a growth rate of 1.6% y-o-y in 2022. The automotive industry sector contributes a percentage of around 2% of the total GDP. The European vehicle production comprises 81% passenger vehicles, 17% commercial vehicles, and 2% other vehicles in 2021.

- In 2020, many European countries were affected by the COVID-19 pandemic, including Germany, Italy, Spain, Russia, and the United Kingdom. The pandemic resulted in supply chain disruptions, lockdowns in the countries, and chip shortages which affected automotive production in Europe. The production of vehicles sharply declined by 22% compared to 2019.

- The United States imports 25.3% worth of cars from Europe and became one of the leading importers of the United States, where Germany accounted for 10.3% and the United Kingdom for 4.7% of total imports of vehicles in the country in 2021. At the beginning of 2022, the sale of the new vehicle dropped by 20.5% due to the invasion of Ukraine by Russia, which reflected in vehicle production as well. In the first quarter of 2022, the European automotive market was down by 10.6% compared to the same period last year.

- Vehicle production is likely to grow with a CAGR of 2.25% during the period (2022 to 2027) due to the new investments being made in electric vehicles by many European countries. For instance, Spain is going to invest USD 5.1 billion in electric vehicle production.

Europe EVA Adhesives Industry Overview

The Europe EVA Adhesives Market is fragmented, with the top five companies occupying 10.12%. The major players in this market are Arkema Group, Beardow Adams, Dow, Henkel AG & Co. KGaA and Jowat SE (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Solvent-borne

- 5.2.3 Water-borne

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arkema Group

- 6.4.2 Beardow Adams

- 6.4.3 Dow

- 6.4.4 Follmann Chemie GmbH

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Jowat SE

- 6.4.8 KLEBCHEMIE M. G. Becker GmbH & Co. KG

- 6.4.9 Paramelt B.V.

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms