|

市場調査レポート

商品コード

1692518

ヨーロッパ、中東、アフリカの二次副栄養素:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)EMEA Secondary Macronutrients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヨーロッパ、中東、アフリカの二次副栄養素:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

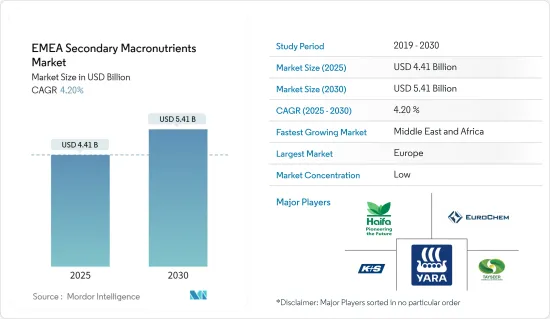

ヨーロッパ、中東、アフリカの二次副栄養素市場規模は2025年に44億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.2%で、2030年には54億1,000万米ドルに達すると予測されます。

ヨーロッパ、中東、アフリカ諸国の農法は、高品質の食品に対する消費者の需要の増加により進化してきました。肥料の多用により、土壌中の大栄養素レベルが低下しています。植物は少量の二次副栄養素を必要とするが、これらは一次栄養素では代替できないです。この必要性がヨーロッパ、中東、アフリカ諸国における二次副栄養素市場の成長を後押ししています。

マグネシウム(Mg)、硫黄(S)、カルシウム(Ca)からなる二次副栄養素は作物の成長に不可欠であり、欠乏すると植物の発育に支障をきたします。メーカー各社は、プレプラント、スターター、サイドドレス、施肥など、多様な施用方法を提供する二次栄養素肥料を製造しています。欧州では、ドイツはライ麦、オート麦、ジャガイモ、飼料用ビートの重要な生産国です。FAOSTATによると、ドイツのオート麦生産量は2021年の72万1,900トンから2022年には75万4,700トンに増加します。これらの二次副栄養素は、植物成長の最適化、土壌肥沃度の向上、栄養レベルバランス、土壌pH調整、水浸透と栄養吸収の改善など、複数の農業機能を果たします。農業分野では、これらの栄養素の有効性から液体製剤の採用が増加しています。この動向は、ヨーロッパ、中東、アフリカ諸国における穀物、果物、野菜の生産量の増加や健康志向の高まりと相まって、同地域の市場成長を牽引しています。

アフリカには大きな農業的潜在力があり、人口の大半は農業を主な生業としています。にもかかわらず、アフリカ大陸は依然として食糧輸入に依存しています。「フィード・アフリカ戦略」は、農業生産を増加させることを目的としており、マグネシウムベースの変種を含む一次および二次肥料の使用強化が重要な役割を担っています。マグネシウム肥料の施用により、さまざまな作物で測定可能な収量向上が実証されています。穀類は0.2~0.6トン/ヘクタール、ジャガイモ塊茎は1.5~3トン/ヘクタール、テンサイ根菜類は2~4トン/ヘクタール、トウモロコシ緑質量は2~6トン/ヘクタール、多年生草本乾草は0.4~0.7トン/ヘクタール、茶葉は0.5~1トン/ヘクタール増加しました。こうした収量向上の記録は、アフリカの農業におけるマグネシウム肥料施用の重要性を浮き彫りにしています。

さらに、同地域の主要企業は、単体硫黄、カルシウム、マグネシウムを他の肥料とブレンドして製品ラインを強化し、収量性能の向上を図っています。この開発により、同地域での二次副栄養素の採用が増加すると予想されます。

ヨーロッパ、中東、アフリカの二次副栄養素市場の動向

高品質作物の生産増加と持続可能な農業の必要性

ヨーロッパ、中東、アフリカ諸国の農業慣行は、高品質食品に対する消費者の嗜好の高まりとともに発展してきました。二次栄養素肥料の普及により、土壌中の多量栄養素レベルが低下しています。植物は最適な成長のためにすべての必須栄養素を必要とするため、ヨーロッパ、中東、アフリカ市場における二次副栄養素の需要を牽引しています。農業では、農家は土壌のマグネシウム欠乏に対処するために肥料としてマグネシウム塩を施用します。換金作物や野菜の栽培農家は特に、作物が適切に開発されるようマグネシウムの豊富な土壌に依存しています。また、植物園では鉢植え植物の成長をサポートするためにマグネシウム塩の需要が高いです。新興経済諸国における可処分所得の増加と相まって、ヨーロッパ、中東、アフリカ諸国の人口増加が食生活パターンの変化をもたらし、ヨーロッパ、中東、アフリカの二次副栄養素市場の成長を牽引しています。

二次副栄養素肥料はマグネシウム(Mg)、硫黄(S)、カルシウム(Ca)で構成されています。これらの栄養素が欠乏すると作物の生育が損なわれます。これらの肥料は、効率と効果を高めるため、液状で入手できます。生産者は、プレプラント法、スターター法、サイドドレス法、ファーティゲーション法など、柔軟な施用方法が可能な二次養分肥料を使用しています。カルシウムの一次供給源は世界的に石灰石であり、その他の供給源には塩基性スラグ、石膏、水和石灰、焼成石灰などがあります。欧州、中東・アフリカでは、硝酸カルシウム、一重および三重過リン酸塩、石膏が一般的なカルシウム肥料です。石膏は、欧州とアフリカで普及している落花生栽培には特に不可欠です。FAO(国連食糧農業機関)によると、アフリカの落花生生産量は2021年の1,680万トンから2022年には1,730万トンに増加し、世界の石膏肥料需要が増加する可能性を示しています。

欧州市場は主に、特にフランス、ドイツ、英国での穀物生産における二次副栄養素肥料の広範な使用によって牽引されています。この地域の健康志向の高まりと植物性食品の消費の増加が、多量栄養素の需要を支えています。2023年、EU委員会は、食料安全保障、持続可能な食料バリューチェーン、効果的な栄養管理を確保するため、Farm to Fork戦略を実施しました。この戦略は、窒素、リン、二次的多量栄養素に焦点を当て、2030年までに栄養素の損失を50%削減することを目標としています。さらに、土壌の肥沃度を維持しながら、欧州諸国全体で肥料使用量を20%削減することを目指しています。アラブ首長国連邦(UAE)の環境・水省(MOEW)とアブダビ環境庁によると、同国の土壌条件は世界的に見ても最も厳しく、そのため二次副栄養素の需要が高まっています。その結果、ヨーロッパ、中東、アフリカの二次副栄養素市場は、作物の収量を向上させ、果物や野菜などの高付加価値作物の需要増に対応する必要性によって牽引されています。

中東が市場をリード

アラブ首長国連邦、サウジアラビア、クウェート、エジプトなどの中東諸国は、栽培に不利な土壌条件のため、食糧供給を輸入に依存しています。アラブ首長国連邦環境水省(MOEW)とアブダビ環境庁によると、同国の土壌は農業にとって世界的に最も困難な状況にあります。こうした状況が、この地域の二次副栄養素市場の成長を後押ししています。

サウジアラビアは、食料安全保障と自給自足を達成するため、農業部門の発展を目指しています。作物の成長と収量を高めるための二次副栄養素の応用は、市場成長にとって不可欠となっています。サウジアラビアは、主にガス処理事業を通じて、世界の硫黄生産において重要な地位を維持しています。Saf Sulphur Factoryのような企業は、粉末、塊状、粒状など様々な形態の硫黄ベースの肥料を生産しています。硫黄とカルシウム肥料の大量生産により、同国は主要輸出国としての地位を確立しています。国連食糧農業機関(FAO)の統計によると、農業用硫酸カリウムの使用量は2021年の4,900トンから2022年には5,050トンに増加しています。この伸びは、作物の収量向上を求めるサウジアラビアの農家の間で、二次副栄養素肥料の需要が高まっていることを示しています。硫黄生産量の増加と食糧安全保障への関心の高まりが相まって、今後数年間は中東諸国全体で二次副栄養素の利用率が高まると予測されます。

ヨーロッパ、中東、アフリカの二次副栄養素産業の概観

ヨーロッパ、中東、アフリカの二次副栄養素市場は断片化されており、世界企業が高度に多様化した製品ポートフォリオで市場をリードしています。同市場には、AL-TAYSEER Chemical Industry、Yara International ASA、Eurochem Group AG、K+S Company、Haifa Groupなど、同地域で事業を展開する主要企業が名を連ねています。各社は製品の品質や販売促進で競争しているだけでなく、より大きなシェアを獲得し、獲得した市場規模を拡大するために、買収や事業拡大といった戦略的な動きにも注力しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 二次副栄養素による植物の健全な成長

- 主要企業のイニシアティブの高まり

- 地域における作物の多様化

- 市場抑制要因

- 一次栄養素肥料の使用量の増加

- ヨーロッパ、中東、アフリカ諸国における有機農業の需要増加

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 栄養素の種類

- 硫黄

- カルシウム

- マグネシウム

- 適用方法

- 固体

- 液体

- 作物タイプ

- 穀物

- 豆類と油糧種子

- 果物・野菜

- 芝・観葉植物

- その他の作物タイプ

- 地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- 中東

- アラブ首長国連邦

- サウジアラビア

- クウェート

- エジプト

- その他中東

- アフリカ

- 南アフリカ

- モロッコ

- ナイジェリア

- その他のアフリカ

- 欧州

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Al-tayseer Chemical Industry

- Yara International ASA

- Eurochem Group AG

- K+S Company

- Saudi United Fertilizer Company(al-asmida)

- ICL

- SAF Sulphur Company

- Haifa Group

- Trade Corporation International SA

第7章 市場機会と今後の動向

The EMEA Secondary Macronutrients Market size is estimated at USD 4.41 billion in 2025, and is expected to reach USD 5.41 billion by 2030, at a CAGR of 4.2% during the forecast period (2025-2030).

Farming practices in EMEA countries have evolved due to increasing consumer demand for high-quality food products. The extensive use of fertilizers has reduced macronutrient levels in soil, as most fertilizers lack these essential elements. While plants need secondary macronutrients in small quantities, these cannot be substituted with primary nutrients. This necessity drives the growth of the secondary macronutrient market in EMEA countries.

Secondary macronutrients, comprising magnesium (Mg), sulfur (S), and calcium (Ca), are essential for crop growth, and their deficiency can impede plant development. Manufacturers produce secondary nutrient fertilizers that offer versatile application methods, including pre-plant, starter, side-dress, and fertigation. In Europe, Germany is a significant producer of rye, oats, potatoes, and fodder beets. According to FAOSTAT, German oat production increased from 721,900 metric tons in 2021 to 754,700 metric tons in 2022. These secondary macronutrients serve multiple agricultural functions, including plant growth optimization, soil fertility enhancement, nutrient level balance, soil pH adjustment, and improved water infiltration and nutrient uptake. The agricultural sector increasingly adopts liquid formulations of these nutrients due to their effectiveness. This trend, combined with rising cereals, fruits, and vegetable production and growing health consciousness in EMEA countries, is driving market growth in the region.

Africa possesses significant agricultural potential, with agriculture being the primary occupation for most of its population. Despite this, the continent remains dependent on food imports. The Feed Africa Strategy aims to increase agricultural production, with enhanced usage of primary and secondary fertilizers, including magnesium-based variants, playing a crucial role. Magnesium fertilizer application has demonstrated measurable yield improvements across various crops: cereal crops increase by 0.2-0.6 metric tons/hectares, potato tubers by 1.5-3 metric tons/hectares, sugar beet root crops by 2-4 metric tons/hectares, corn green mass by 2-6 metric tons/hectares, perennial grass hay by 0.4-0.7 metric tons/hectares, and tea leaves by 0.5-1.0 metric tons/hectares. These documented yield improvements highlight the importance of magnesium fertilizer application in African agriculture.

Moreover, key players in the region are enhancing their product lines by blending elemental sulfur, calcium, and magnesium with other fertilizers to improve yield performance. This development is anticipated to increase the adoption of secondary macronutrients in the region.

EMEA Secondary Macronutrients Market Trends

Rising Production of High-Quality Crops and the Need for Sustainable Agricultural

Agricultural practices in EMEA countries have evolved with increasing consumer preference for high-quality food products. The widespread use of secondary nutrient fertilizers has reduced macronutrient levels in soil, as these fertilizers typically lack essential macronutrients. Plants require all essential nutrients for optimal growth, which drives the demand for secondary macronutrients in the EMEA market. In agriculture, farmers apply magnesium salt as a fertilizer to address soil magnesium deficiency. Cash crop and vegetable farmers particularly rely on magnesium-rich soil to ensure proper crop development. Plant nurseries also show a strong demand for magnesium salt to support potted plant growth. Population growth in EMEA countries, combined with increasing disposable income in developing economies, has led to changes in dietary patterns, driving the EMEA secondary macronutrient market growth.

Secondary macronutrient fertilizers consist of Magnesium (Mg), Sulfur (S), and Calcium (Ca). The deficiency of these nutrients can impair crop growth. These fertilizers are available in liquid form to enhance efficiency and effectiveness. Producers use secondary nutrient fertilizers due to their flexible application options, including pre-plant, starter, side-dress, and fertigation methods. Limestone serves as the primary global source of calcium, while other sources include basic slag, gypsum, hydrated lime, and burned lime. In Europe, the Middle East, and Africa, calcium nitrate, single and triple superphosphate, and gypsum are common calcium fertilizers. Gypsum is particularly essential for groundnut cultivation, which is prevalent in Europe and Africa. According to the Food and Agriculture Organization (FAO), groundnut production in Africa increased from 16.8 million metric tons in 2021 to 17.3 million metric tons in 2022, indicating a potential increase in global gypsum fertilizer demand.

The European market is primarily driven by the extensive use of secondary macronutrient fertilizers in cereal crop production, particularly in France, Germany, and the United Kingdom. The region's increasing health consciousness and rising consumption of plant-based foods support the demand for macronutrients. In 2023, the EU Commission implemented the Farm to Fork Strategy to ensure food security, sustainable food value chains, and effective nutrient management. This strategy focuses on nitrogen, phosphorus, and secondary macronutrients, targeting a 50% reduction in nutrient losses by 2030. Additionally, it aims to reduce fertilizer usage by 20% across European countries while preserving soil fertility. In the UAE, according to the Ministry of Environment and Water (MOEW) and Environmental Agency - Abu Dhabi, the country's soil conditions are among the most challenging globally, which has increased the demand for secondary macronutrients. Consequently, the EMEA secondary macronutrient market is driven by the need to improve crop yields and meet the growing demand for high-value crops, including fruits and vegetables.

Middle East Leads the Market

Middle Eastern countries, including the United Arab Emirates, Saudi Arabia, Kuwait, and Egypt, are import-dependent for food supplies due to unfavorable soil conditions for cultivation. According to the UAE Ministry of Environment and Water (MOEW) and Environmental Agency - Abu Dhabi, the country's soil is among the most challenging globally for agriculture. These conditions have driven the growth of the secondary macronutrients market in the region.

Saudi Arabia aims to develop its agricultural sector to achieve food security and self-sufficiency. The application of secondary macronutrients to enhance crop growth and yield has become essential for market growth. Saudi Arabia maintains a significant position in global sulfur production, primarily through gas processing operations. Companies like Saf Sulphur Factory produce sulfur-based fertilizers in various forms, including powder, lumps, and granular. The country's substantial production of sulfur and calcium fertilizers has established it as a major exporter. The Food and Agriculture Organization (FAO) statistics indicate that agricultural potassium sulfate usage increased from 4,900 metric tons in 2021 to 5,050 metric tons in 2022. This growth demonstrates the rising demand for secondary macronutrient fertilizers among Saudi Arabian farmers seeking improved crop yields. The combination of increased sulfur production and the focus on food security is projected to drive higher utilization of secondary macronutrients across Middle Eastern countries in the coming years.

EMEA Secondary Macronutrients Industry Overview

The EMEA secondary macronutrient market is fragmented with global players leading the market with a highly diversified product portfolio and several acquisitions and agreements taking place to gain a major share in the industry. Some of the major players in the market include AL-TAYSEER Chemical Industry, Yara International ASA, Eurochem Group AG, K+S Company, and Haifa Group are some of the major players who are operating in the region. The companies are not only competing based on product quality or product promotion but are also focused on other strategic moves, like acquisitions and expansions, to acquire a larger share and expand their acquired market size.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Secondary Macronutrients Ensure Healthy Plant Growth

- 4.2.2 Rising Key Players Initiatives

- 4.2.3 Crop Diversification in the Region

- 4.3 Market Restraints

- 4.3.1 Increasing Usage of Primary Nutrients Fertilizers

- 4.3.2 Increased Demand for Organic Agriculture In EMEA Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Nutrient Type

- 5.1.1 Sulfur

- 5.1.2 Calcium

- 5.1.3 Magnesium

- 5.2 Application Method

- 5.2.1 Solid

- 5.2.2 Liquid

- 5.3 Crop Type

- 5.3.1 Grains And Cereals

- 5.3.2 Pulses And Oilseeds

- 5.3.3 Fruits And Vegetables

- 5.3.4 Turfs And Ornamentals

- 5.3.5 Other Crop Types

- 5.4 Geography

- 5.4.1 Europe

- 5.4.1.1 Germany

- 5.4.1.2 United Kingdom

- 5.4.1.3 France

- 5.4.1.4 Italy

- 5.4.1.5 Spain

- 5.4.1.6 Russia

- 5.4.1.7 Rest of Europe

- 5.4.2 Middle East

- 5.4.2.1 United Arab Emirates

- 5.4.2.2 Saudi Arabia

- 5.4.2.3 Kuwait

- 5.4.2.4 Egypt

- 5.4.2.5 Rest of Middle East

- 5.4.3 Africa

- 5.4.3.1 South Africa

- 5.4.3.2 Morocco

- 5.4.3.3 Nigeria

- 5.4.3.4 Rest of Africa

- 5.4.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Al-tayseer Chemical Industry

- 6.3.2 Yara International ASA

- 6.3.3 Eurochem Group AG

- 6.3.4 K+S Company

- 6.3.5 Saudi United Fertilizer Company (al-asmida)

- 6.3.6 ICL

- 6.3.7 SAF Sulphur Company

- 6.3.8 Haifa Group

- 6.3.9 Trade Corporation International SA