|

市場調査レポート

商品コード

1692438

欧州の精密農業:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Precision Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の精密農業:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

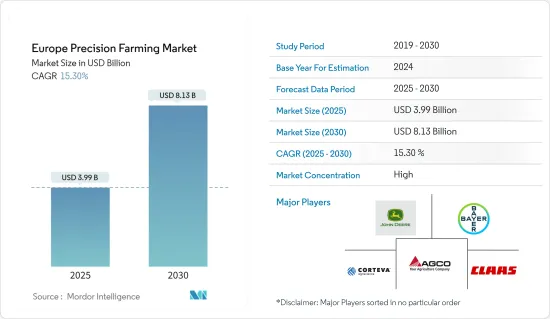

欧州の精密農業市場規模は、2025年に39億9,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは15.3%で、2030年には81億3,000万米ドルに達すると予測されます。

主なハイライト

- 欧州の精密農業市場は、技術の進歩と持続可能な農法への関心の高まりに後押しされて急成長を遂げています。農家は、GPS、ドローン、IoTデバイスなどのツールを活用して、作物の収量を向上させ、資源をより効率的に管理しています。

- 市場の拡大には、政府の支援が重要な役割を果たしています。欧州連合(EU)のホライゾン・欧州計画(2021~2027年)は、約1,040億米ドルの予算で、精密農業の導入を促進しています。このイニシアティブは、技術革新と協力を奨励し、地域全体の精密農業技術の開発と実施を促進しています。

- 同市場の主要技術には、ガイダンスシステム、リモートセンシング、可変レート技術が含まれます。これらのツールは、作物のモニタリング、土壌の健全性評価、農場の生産性を向上させる。リアルタイムのデータと高度な分析を統合することで、農家は特定の作物要件に合わせた、より多くの情報に基づいた意思決定を行うことができます。欧州連合(EU)の精密農業政策・導入見通し2023によると、この地域での精密農業の導入は英国がリードしており、英国内ではスコットランドが85%の導入率、次いでアイルランドの農家が43%となっています。ドイツとデンマークも、こうした技術の主要な採用国です。

- 持続可能な食糧生産に対する消費者の関心の高まりは、資源の効率的利用によって環境への影響を低減する精密農業の実践と一致しています。この動向は市場の需要に対応し、プレミアムで環境に優しい市場において農家にチャンスをもたらします。継続的な技術の進歩と持続可能な農業に対する強力な政策支援により、欧州における精密農業の将来は有望と思われます。

欧州の精密農業市場動向

労働力不足が欧州農業における精密農業の導入を促進

- 欧州連合(EU)の青果部門は、EU加盟国および非加盟国の労働力に大きく依存しています。ドイツ、イタリア、スペイン、フランス、ポーランドは、かなりの数の季節移民労働者を雇用しています。1億5,700万ヘクタールの農地に約910万戸の農場を持つEUは、移民政策の厳格化と季節労働者の減少により、労働力不足の深刻化に直面しています。こうした状況は、農業部門の効率性、生産性、持続可能性を向上させながら、労働力への依存を減らす自動化ソリューションを提供する精密農業技術の採用を加速させています。

- EUでは、特に農業が重要な経済的役割を担っている農村部において、労働力人口の減少が起きています。EUの農業労働力指数は約15.8%減少しており、利用可能な労働者数が全体的に減少傾向にあることを示しています。この人口動態上の課題により、作付け、収穫、加工などの作業に十分な労働力を確保することがますます難しくなっています。その結果、農家はこうした労働力不足に対処するため、精密農業技術の採用を増やしています。

- 2023年、欧州政府は農業と農村地域のデジタル化プログラムを開始し、農業におけるデジタル技術とデータ主導型アプローチの統合を推進しました。このイニシアティブは27万4,000以上の農場に恩恵をもたらし、高度なデジタルツールによる効率性と生産性の向上を目指しています。このプログラムは、GPS、センサー、データ分析などの精密技術の採用を奨励することで、欧州の精密農業市場の成長を直接支援しています。この自動化へのシフトは、労働力不足を解消するだけでなく、農業の効率性と持続可能性の向上にも役立ちます。

ドイツにおける精密農業の採用拡大

- ドイツの生産者による近代的農業技術の利用の増加は、精密農業への大きなシフトを浮き彫りにしています。ドイツは、2022年時点で約1,160万ヘクタールの農地を誇り、欧州最大の農業地域のひとつに位置づけられています。この広大な農業風景は、精密農業技術の導入に大きな機会を提供しています。さらに、多くの農家がGPSを利用した面積測定や土壌サンプリングなど、データ主導の手法を採用しているが、土地に応じた播種や施肥など、より高度な技術はまだ一般的ではないです。

- ドイツでは、特に500ヘクタールを超える農場では、精密農業が農業請負サービスの重要な一部となりつつあります。この技術は、土壌の状態や植物の健康状態をモニタリングし、生育管理の改善につなげる上で重要な役割を果たしています。特定の農地向けのドローン用途への関心の高まりは、モジュール式精密農業ツールの採用をさらに促進し、市場成長に寄与すると予測されます。ドイツのJKI(Julius Kuhn-Institut)は、専門的なノズルテストにおける厳格な基準で有名であり、同国では農業用ドローンに必須の認証となっています。例えば、DJI T30ドローンは、2022年にドイツで山間部のブドウ園の作業用として承認を受けました。

- 食糧安全保障とより良い養分管理への関心の高まりが、全国的に精密農業技術の普及を後押ししています。デジタル農業2025」プログラムなどの取り組みによって強化されたドイツの持続可能な農業へのコミットメントは、農業実践におけるデジタルツールの使用を加速させています。こうした進歩は、労働力不足や環境の持続可能性といった課題に対処するために不可欠であると同時に、土壌センサーやドローンといった技術の利用を通じて、作物の収量を向上させ、投入コストを削減します。

欧州の精密農業産業の概要

欧州の精密農業市場は非常に集中しています。Deere &Company、Bayer Crop Science、Agco corporation、CLAAS KGaA mbH、Corteva.が市場の主要企業です。欧州で事業を展開する企業は、技術革新やパートナーシップとともに、研究開発や製品投入に注力しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 政府の支援と補助金

- 技術の進歩

- 持続可能な農業に対する需要の増加

- 市場抑制要因

- 規制と標準化の課題

- 初期コストの高さ

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 技術

- 誘導システム

- 全地球測位システム(GPS)/全地球衛星航法システム(GNSS)

- 全地球情報システム(GIS)

- リモートセンシング

- 可変レート技術

- 可変レート肥料

- 可変率播種

- 可変レート農薬

- ドローンとUAV

- その他の技術

- 誘導システム

- コンポーネント

- ハードウェア

- ソフトウェア

- サービス

- アプリケーション

- 収量モニタリング

- 可変レートアプリケーション

- フィールドマッピング

- 土壌モニタリング

- 作物スカウティング

- その他のアプリケーション

- 地域

- ドイツ

- フランス

- 英国

- イタリア

- その他欧州

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- AGCO Corporation

- TopCon Corporation

- Corteva(Granular Inc.)

- CNH Industrial N.V.(Raven)

- Deere & Company

- Teejet Technologies

- CLAAS KGaA mbH(365FarmNet)

- AG Leader Technology Inc.

- Pottinger Landtechnik Gmbh group(MaterMacc)

- Bayer Cropscience AG

第7章 市場機会と今後の動向

目次

Product Code: 91048

The Europe Precision Farming Market size is estimated at USD 3.99 billion in 2025, and is expected to reach USD 8.13 billion by 2030, at a CAGR of 15.3% during the forecast period (2025-2030).

Key Highlights

- The precision farming market in Europe is experiencing rapid growth, propelled by technological advancements and an increased focus on sustainable agricultural practices. Farmers are utilizing tools such as GPS, drones, and IoT devices to improve crop yields and manage resources more efficiently.

- Government support plays a crucial role in the market's expansion. The European Union's Horizon Europe Programme (2021-2027), with a budget of about USD 104 billion, promotes the adoption of precision farming. This initiative encourages innovation and collaboration, facilitating the development and implementation of precision farming technologies across the region.

- Key technologies in the market include guidance systems, remote sensing, and variable rate technology. These tools enhance crop monitoring, soil health assessments, and farm productivity. Integrating real-time data and advanced analytics enables farmers to make more informed decisions tailored to their specific crop requirements. According to the European Union Precision Agriculture Policy & Adoption Outlook 2023, the United Kingdom leads in precision agriculture adoption in the region, with Scotland at 85% adoption within the UK, followed by 43% of Irish farmers. Germany and Denmark are also major adopters of these technologies.

- The growing consumer interest in sustainable food production aligns with precision farming practices, which reduce environmental impact through efficient resource use. This trend addresses market demands and presents opportunities for farmers in premium, eco-friendly markets. With ongoing technological progress and strong policy support for sustainable agriculture, the future of precision farming in Europe appears promising.

Europe Precision Farming Market Trends

Labor Shortages Drive Precision Farming Adoption in European Agriculture

- The European Union's fruit and vegetable sector relies heavily on non-national labor from both EU and non-EU countries. Germany, Italy, Spain, France, and Poland employ significant numbers of seasonal migrant workers. With about 9.1 million farms across 157 million hectares of agricultural land, the EU faces increasing labor shortages due to stricter immigration policies and declining availability of seasonal workers. This situation has accelerated the adoption of precision farming technologies, which offer automated solutions to reduce labor dependency while improving efficiency, productivity, and sustainability in the agricultural sector.

- The EU is experiencing a declining labor force, particularly in rural areas where agriculture plays a key economic role. The EU agricultural labor force index decreased by about 15.8%, indicating an overall downward trend in the number of available workers. This demographic challenge has made it increasingly difficult to find sufficient labor for tasks such as planting, harvesting, and processing. Consequently, farmers are increasingly adopting precision farming technologies to address these labor shortages.

- In 2023, the European government initiated a digitalization program for agriculture and rural areas, promoting the integration of digital technologies and data-driven approaches in farming. This initiative benefits over 274,000 farms, aiming to enhance efficiency and productivity through advanced digital tools. The program directly supports the growth of the Europe Precision Farming Market by encouraging the adoption of precision technologies such as GPS, sensors, and data analytics. This shift towards automation not only helps alleviate the labor shortage but also improves efficiency and sustainability in agriculture.

Growing adoption of precision farming in Germany

- The increasing use of modern farming techniques by German growers highlights a significant shift towards precision farming. Germany boasts about 11.6 million hectares of agricultural land as of 2022, positioning it as one of Europe's largest farming regions. This extensive agricultural landscape offers a significant opportunity for the adoption of precision farming technologies. Moreover, many farmers are adopting data-driven methods, such as GPS-based area measurements and soil sampling, although more advanced techniques like site-specific sowing and fertilizing are still less common.

- In Germany, precision farming is increasingly becoming a crucial part of agricultural contractor services, particularly on farms exceeding 500 hectares. This technology plays a significant role in monitoring soil conditions and plant health, leading to improved growth management. The rising interest in drone applications for specific farm areas is projected to further promote the adoption of modular precision farming tools, contributing to market growth. The German Julius Kuhn-Institut (JKI) is renowned for its stringent standards in professional nozzle testing, a certification that is mandatory for agricultural drones in the country. For instance, DJI T30 drones received approval in 2022 for mountain vineyard operations in Germany.

- The growing focus on food security and better nutrient management is driving the widespread adoption of precision farming technologies across the nation. Germany's commitment to sustainable agriculture, reinforced by initiatives such as the "Digital Farming 2025" program, is accelerating the use of digital tools in farming practices. These advancements are critical for addressing challenges like labor shortages and environmental sustainability, while also enhancing crop yields and reducing input costs through the use of technologies such as soil sensors and drones.

Europe Precision Farming Industry Overview

The European precision farming market is highly concentrated. Deere & Company, Bayer Crop Science, Agco corporation, CLAAS KGaA mbH and Corteva. are the key players in the market. The companies operating in Europe are focusing on R&D and product launches, along with innovations and partnerships.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Support and Subsidies

- 4.2.2 Technological Advancements

- 4.2.3 Increasing Demand for Sustainable Agriculture

- 4.3 Market Restraints

- 4.3.1 Regulatory and Standardization Challenges

- 4.3.2 High Initial Cost

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power Of Suppliers

- 4.4.2 Bargaining Power Of Buyers

- 4.4.3 Threat Of New Entrants

- 4.4.4 Threat Of Substitute Products And Services

- 4.4.5 Degree Of Competition

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Guidance System

- 5.1.1.1 Global Positioning System (GPS)/ Global Satellite Navigation System (GNSS)

- 5.1.1.2 Global Information System (GIS)

- 5.1.2 Remote Sensing

- 5.1.3 Variable Rate Technology

- 5.1.3.1 Variable Rate Fertilizer

- 5.1.3.2 Variable Rate Seeding

- 5.1.3.3 Variable Rate Pesticide

- 5.1.4 Drones and UAVs

- 5.1.5 Other Technologies

- 5.1.1 Guidance System

- 5.2 Components

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 Application

- 5.3.1 Yield Monitoring

- 5.3.2 Variable Rate Application

- 5.3.3 Field Mapping

- 5.3.4 Soil Monitoring

- 5.3.5 Crop Scouting

- 5.3.6 Other Application

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 United Kingdom

- 5.4.4 Italy

- 5.4.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 AGCO Corporation

- 6.3.2 TopCon Corporation

- 6.3.3 Corteva (Granular Inc.)

- 6.3.4 CNH Industrial N.V. (Raven)

- 6.3.5 Deere & Company

- 6.3.6 Teejet Technologies

- 6.3.7 CLAAS KGaA mbH (365FarmNet)

- 6.3.8 AG Leader Technology Inc.

- 6.3.9 Pottinger Landtechnik Gmbh group (MaterMacc)

- 6.3.10 Bayer Cropscience AG