|

|

市場調査レポート

商品コード

1692128

希少疾患治療:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Rare Disease Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 希少疾患治療:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 131 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

希少疾患治療の市場規模は2025年に2,425億米ドルと推定され、予測期間(2025~2030年)のCAGRは11.93%で、2030年には4,260億3,000万米ドルに達すると予測されます。

市場を形成するメガトレンド:希少疾患治療市場は、希少疾患の世界の有病率の上昇と、新規治療薬の研究開発(R&D)への注力という2つのメガトレンドに牽引され、力強い成長を遂げています。これらのメガトレンドは、認知度の向上、有利な政府政策、新薬上市の急増によって支えられています。これらの要因が相まって、市場は前進し、希少疾患治療の展望が形作られています。

希少疾患患者数の増加:市場拡大の主な要因は、希少疾患の世界の流行です。GlobalGenes社によると、希少疾患の患者数は世界で4億人を超え、約7,000の疾患が知られています。このような患者数の多さは、特にこれらの疾患の80%が遺伝的なものであることから、専門的な治療に対する需要を高めています。年間250~280の新しい希少疾病が発見されていることは、市場範囲の拡大と治療アプローチにおける継続的な技術革新の必要性をさらに強調しています。

新規治療薬・薬剤の研究開発活動の活発化:研究開発は希少疾患治療市場の成長の核心です。資金提供の増加と戦略的な官民イニシアチブが技術革新を促進しています。例えば、米国食品医薬品局(FDA)は、希少疾患の臨床試験や研究ツールを支援するため、4年間で3,800万米ドルを超える資金を拠出しています。このような投資は、希少疾患患者のアンメット・メディカル・ニーズへの対応に不可欠であり、市場の大幅な成長を促進します。

新薬上市数の増加:FDAが承認した希少疾病治療薬の数は急速に増加しており、その多くが希少疾病治療薬に分類されています。酸スフィンゴミエリナーゼ欠損症(ASMD)の治療薬として開発されたゼンポザイムのような最近の承認動向は、希少疾患治療薬の開発に注力する同分野の姿勢を浮き彫りにしています。これらの新しい治療は、患者に希望を与えるだけでなく、希少疾患の患者特有のニーズに対応する選択肢を増やすことで、市場の拡大にも貢献しています。

有利な政府政策:政府のイニシアチブは、市場の成長を加速させる上で重要な役割を果たします。インドや米国のような国では、希少疾患の研究や治療を支援する政策を導入しています。例えば、インドは2024年8月、希少疾病中央技術委員会(CTCRD)の勧告を受けて、63の希少疾病を希少疾病国家政策に追加しました。同様に、米国FDAのARC(Accelerating Rare Disease Cures)プログラムは、希少疾患の治療法開発を迅速に進めることを目的としており、市場プレーヤーにとって有利な環境を作り出しています。

市場プレーヤーによる戦略的取り組み:戦略的提携、合併、買収が競合情勢を形成しています。アストラゼネカやCanSino Biologics Inc.のような企業は、中国における希少疾患の診断と治療へのアクセスを強化するために提携しています。このような取り組みにより、技術革新が促進され、市場範囲が拡大し、今後数年間で市場成長がさらに促進されると予想されます。

希少疾患治療市場の動向

生物製剤:希少疾患治療のイノベーションを推進

セグメントの概要:生物製剤は希少疾患治療市場を変革しており、現在の市場シェアの58%を占めています。タンパク質、抗体、ペプチドを含むこれらの複合療法は、これまで治療不可能と考えられていた遺伝性疾患や慢性疾患の治療に的を絞ったアプローチを提供します。

成長の原動力生物学的製剤の成長を牽引している要因はいくつかあります。個別化医療の発展とともに遺伝子研究の進歩が、高度に的を絞った治療法の創出を可能にしています。希少疾患の有病率の増加とその分子メカニズムに対する理解の深まりは、この分野の研究に拍車をかけています。さらに、希少疾病用医薬品の開発に対する規制上の優遇措置が企業に生物製剤への投資を促し、革新的な治療の強力なパイプラインを生み出しています。

競合情勢:生物製剤市場は激しい競争を特徴としており、各社は技術革新と提携に注力しています。製薬企業は、希少疾患の根本原因に取り組む生物学的治療法を開発するため、研究開発に多額の投資を行っています。製薬企業と研究機関の共同研究は一般的になりつつあり、新規生物製剤の開発を促進しています。遺伝子編集や細胞治療などの先端技術の利用は、既存の治療パラダイムを破壊し、生物学的製剤セグメントの今後の成長を促進すると予想されます。

アジア太平洋地域:希少疾患治療における新興大国

地域のダイナミクス:アジア太平洋地域は希少疾患治療の主要成長市場として台頭しており、2024年から2029年までの年間平均成長率(CAGR)は12%を超えると予測されます。同地域の急速な市場拡大は、世界の希少疾患治療の展望における同地域の可能性を浮き彫りにしています。

成長の触媒:アジア太平洋地域の成長を後押ししている要因はいくつかあります。政府のイニシアチブ、患者支援活動、ヘルスケアプロバイダーが先導する希少疾患に対する認識の高まりは、診断率を向上させ、治療需要を増大させています。アジア太平洋地域の各国政府は、希少疾患の管理を強化するための政策を導入しています。シンガポールの希少疾患基金やマレーシアのヘルスケア投資は、支援活動の顕著な例です。さらに、この地域のヘルスケア・インフラは拡大しており、特に新興国では高度な診断や治療へのアクセスが向上しています。

戦略的課題:アジア太平洋地域の急成長を活かそうとする企業は、同地域特有の遺伝的多様性を認識し、同地域で流行している希少疾患をターゲットとした治療に注力しています。国際的な製薬企業と現地のヘルスケア・プロバイダーとの提携は増加傾向にあり、臨床試験能力の向上とアジア人口の希少疾患に関する研究の拡大を目指しています。また、企業は遠隔医療や患者モニタリングプラットフォームなどのデジタルヘルス技術を活用し、希少疾患の管理をサポートしています。

今後の展望:アジア太平洋市場の堅調な成長により、投資と技術革新の増加が見込まれます。このダイナミックな市場における課題と機会に対処するためには、戦略的パートナーシップ、技術の進歩、規制当局の支援が鍵となります。新興技術を活用しながら、この地域の多様な規制環境とヘルスケア制度をうまく乗り切る企業は、成功に向けて有利な立場にあります。

希少疾患治療業界の概要

市場の優位性:世界の複合企業がリード

希少疾患治療市場は、ファイザー、ノバルティス、ロシュ、サノフィなどの世界製薬コングロマリットが市場の大部分を占めています。これらの企業が市場で強い地位を占めているのは、広範な研究開発能力と世界な展開によるものです。希少疾患のポートフォリオは、これらの企業の収益全体においてますます重要な役割を果たすようになっており、TAM(Total Addressable Market:対処可能な市場)の拡大により、さらなる拡大の機会が十分にあります。

主要企業革新と専門化が成功の原動力

ファイザー、ノバルティス、ロシュ、サノフィなどの主要企業は、イノベーションと専門性に重点を置いています。特に生物学的製剤と遺伝子治療における研究開発への多額の投資によって、市場でのリーダーシップは強化されています。ノバルティスの脊髄性筋萎縮症治療薬Zolgensmaやロシュの血友病A治療薬Hemlibraのような画期的な治療は、各社の先駆的な治療開発能力を示しています。世界なプレゼンスと資金力により、希少疾患治療薬開発の複雑さを克服し、この特殊な市場におけるリーダーとしての地位を確立しています。

市場成功のための戦略研究開発と提携

希少疾患治療市場における将来の成功は、研究開発努力の強化、戦略的提携、新技術の採用にかかっています。ゾルゲンマのような治療薬の承認が示すように、企業は遺伝子治療や個別化医療にますます力を注いでいます。研究機関や患者支援団体とのパートナーシップは、アンメットニーズを特定し、医薬品開発を加速させる上で不可欠です。例えば、バイオマリン・ファーマシューティカル社とアレン研究所による希少中枢神経系疾患の遺伝子治療に関する共同研究は、市場を形成する革新的パートナーシップの代表例です。さらに、創薬や臨床試験の最適化にAIやビッグデータを活用することは、競争優位性を高めるための重要な戦略になりつつあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 希少疾患患者数の増加

- 新規治療薬・新薬の研究開発活動の活発化、新薬上市数の増加、政府の好意的政策

- 市場抑制要因

- 希少疾患治療に関する認識不足

- 高い治療費

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 薬剤タイプ別

- 生物製剤

- 非生物製剤

- 治療領域別

- 遺伝子疾患

- 神経疾患

- 腫瘍

- 感染症

- 心血管疾患

- その他の治療領域

- 投与方法別

- 経口

- 注射

- その他の投与方法

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AbbVie Inc.

- AstraZeneca(Alexion Pharmaceuticals Inc.)

- Amgen Inc.

- Baxter

- Bayer AG

- Biomarin Pharmaceuticals

- Bristol-Myers Squibb Company

- Eisai Co. Ltd

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Pfizer Inc.

- Sanofi

- Teva Pharmaceuticals

- Vertex Pharmaceuticals

第7章 市場機会と今後の動向

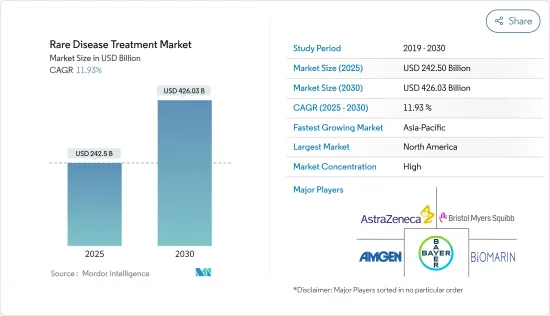

The Rare Disease Treatment Market size is estimated at USD 242.50 billion in 2025, and is expected to reach USD 426.03 billion by 2030, at a CAGR of 11.93% during the forecast period (2025-2030).

Megatrends Shaping the Market: The Rare Disease Treatment Market is experiencing robust growth, driven by two primary megatrends: the rising global prevalence of rare diseases and the intensifying focus on research and development (R&D) for novel therapeutics. These megatrends are supported by increasing awareness, favorable government policies, and a surge in new drug launches. Collectively, these factors are propelling the market forward and shaping the future of the rare disease treatment landscape.

Increase in the Number of Rare Disease Cases: A key driver for market expansion is the growing prevalence of rare diseases worldwide. According to GlobalGenes, more than 400 million people are affected by rare diseases globally, with approximately 7,000 known conditions. This substantial patient population drives demand for specialized treatments, especially since 80% of these diseases have genetic origins. The discovery of 250 to 280 new rare diseases annually further emphasizes the expanding market scope and the need for continuous innovation in treatment approaches.

Rising R&D Activities for Novel Therapeutics and Drugs: R&D is at the heart of growth in the rare disease treatment market. Increased funding and strategic public-private initiatives are catalyzing innovation. For example, the U.S. Food and Drug Administration (FDA) has committed over USD 38 million in funding over four years to support clinical trials and research tools for rare diseases. Such investments are critical in addressing the unmet medical needs of rare disease patients, fostering significant market growth.

Increase in the Number of New Drug Launches: The number of FDA-approved drugs for rare diseases, many of which are classified as orphan drugs, is growing rapidly. Recent approvals like Xenpozyme, designed for treating Acid Sphingomyelinase Deficiency (ASMD), highlight the sector's focus on rare disease drug development. These new treatments not only offer hope to patients but also contribute to market expansion by providing more options to address the specific needs of those affected by rare diseases.

Favorable Government Policies: Government initiatives play a crucial role in accelerating market growth. Countries like India and the United States are introducing policies that support rare disease research and treatment. For instance, in August 2024, India added 63 rare diseases to its National Policy for Rare Diseases, following recommendations from the Central Technical Committee for Rare Diseases (CTCRD). Similarly, the U.S. FDA's Accelerating Rare Disease Cures (ARC) Program is designed to fast-track the development of treatment options for rare diseases, creating a favorable environment for market players.

Strategic Initiatives by Market Players: Strategic collaborations, mergers, and acquisitions are shaping the competitive landscape. Companies like AstraZeneca and CanSino Biologics Inc. are partnering to enhance rare disease diagnosis and treatment access in China. Such initiatives are expected to drive innovation, expand market reach, and further stimulate market growth in the years ahead.

Rare Disease Treatment Market Trends

Biologics: Driving Innovation in Rare Disease Treatment

Segment Overview: Biologics are transforming the rare disease treatment market, accounting for 58% of the current market share. These complex therapies, including proteins, antibodies, and peptides, offer a targeted approach to treating genetic and chronic conditions previously considered untreatable.

Growth Drivers: Several factors are driving the growth of biologics. Advances in genetic research, alongside developments in personalized medicine, have enabled the creation of highly targeted therapies. The increasing prevalence of rare diseases, combined with greater understanding of their molecular mechanisms, is fueling research in this area. Additionally, regulatory incentives for orphan drug development are encouraging companies to invest in biologics, resulting in a strong pipeline of innovative treatments.

Competitive Landscape: The biologics market is characterized by intense competition, with companies focusing on innovation and collaboration. Pharmaceutical firms are investing heavily in R&D to develop biological therapies that tackle the root causes of rare diseases. Collaborations between pharmaceutical companies and research institutions are becoming more common, facilitating the development of novel biologics. The use of advanced technologies, such as gene editing and cell therapies, is expected to disrupt existing treatment paradigms and drive future growth in the biologics segment.

Asia-Pacific: Emerging Powerhouse in Rare Disease Treatment

Regional Dynamics: The Asia-Pacific region is emerging as a key growth market for rare disease treatments, with a projected Compound Annual Growth Rate (CAGR) of over 12% from 2024 to 2029. The region's rapid market expansion highlights its potential in the global rare disease treatment landscape.

Growth Catalysts: Several factors are propelling growth in Asia-Pacific. Increased awareness of rare diseases, spearheaded by government initiatives, patient advocacy, and healthcare providers, is improving diagnosis rates and increasing demand for treatments. Governments across the region are introducing policies to enhance rare disease management. Singapore's Rare Disease Fund and Malaysia's healthcare investments are notable examples of supportive efforts. Furthermore, the region's expanding healthcare infrastructure is improving access to advanced diagnostics and treatments, particularly in emerging economies.

Strategic Imperatives: Companies seeking to capitalize on Asia-Pacific's rapid growth are focusing on treatments targeting rare diseases prevalent in the region, recognizing its unique genetic diversity. Collaborations between international pharmaceutical firms and local healthcare providers are on the rise, aimed at improving clinical trial capabilities and expanding research on rare diseases in Asian populations. Companies are also leveraging digital health technologies, such as telemedicine and patient monitoring platforms, to support rare disease management.

Future Outlook: The Asia-Pacific market is expected to attract increased investment and innovation due to its robust growth. Strategic partnerships, technological advancements, and regulatory support will be key to addressing the challenges and opportunities in this dynamic market. Companies that navigate the diverse regulatory environments and healthcare systems in the region while leveraging emerging technologies are well-positioned for success.

Rare Disease Treatment Industry Overview

Market Dominance: Global Conglomerates Lead

The Rare Disease Treatment Market is dominated by global pharmaceutical conglomerates, with companies like Pfizer, Novartis, Roche, and Sanofi controlling a significant portion of the market. Their strong market positions are due to extensive R&D capabilities and global reach. Rare disease portfolios play an increasingly important role in these companies' overall revenue, with ample opportunities for further expansion due to the growing total addressable market (TAM).

Key Players: Innovation and Specialization Drive Success

Top players, such as Pfizer, Novartis, Roche, and Sanofi, share a focus on innovation and specialization. Their leadership in the market is bolstered by substantial investments in R&D, particularly in biologics and gene therapies. Breakthrough treatments like Novartis' Zolgensma for spinal muscular atrophy and Roche's Hemlibra for hemophilia A showcase the companies' ability to develop pioneering treatments. Their global presence and financial resources allow them to navigate the complexities of rare disease drug development, positioning them as leaders in this specialized market.

Strategies for Market Success: R&D and Collaboration

Future success in the rare disease treatment market will depend on intensified R&D efforts, strategic collaborations, and the adoption of emerging technologies. Companies are increasingly focusing on gene therapies and personalized medicine, as demonstrated by the approval of treatments like Zolgensma. Partnerships with research institutions and patient advocacy groups are vital in identifying unmet needs and accelerating drug development. For instance, BioMarin Pharmaceutical Inc. and the Allen Institute's collaboration on gene therapies for rare central nervous system diseases is a prime example of the innovative partnerships shaping the market. Additionally, the use of AI and big data for drug discovery and optimizing clinical trials is becoming a key strategy for enhancing competitive advantage.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in the Number of Rare Disease Cases

- 4.2.2 Rising R&D Activities for Novel Therapeutics and Drugs and Increase in the Number of New Drug Launches and Favorable Government Policies

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness Regarding Rare Disease Treatment

- 4.3.2 High Cost of Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - in USD)

- 5.1 By Drug Type

- 5.1.1 Biologics

- 5.1.2 Non-biologics

- 5.2 By Therapeutic Area

- 5.2.1 Genetic Diseases

- 5.2.2 Neurological Diseases

- 5.2.3 Oncology

- 5.2.4 Infectious Diseases

- 5.2.5 Cardiovascular Diseases

- 5.2.6 Other Therapeutic Area

- 5.3 By Mode of Administration

- 5.3.1 Oral

- 5.3.2 Injection

- 5.3.3 Other Modes of Administration

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AbbVie Inc.

- 6.1.2 AstraZeneca (Alexion Pharmaceuticals Inc.)

- 6.1.3 Amgen Inc.

- 6.1.4 Baxter

- 6.1.5 Bayer AG

- 6.1.6 Biomarin Pharmaceuticals

- 6.1.7 Bristol-Myers Squibb Company

- 6.1.8 Eisai Co. Ltd

- 6.1.9 Eli Lilly and Company

- 6.1.10 F. Hoffmann-La Roche Ltd

- 6.1.11 Novartis AG

- 6.1.12 Pfizer Inc.

- 6.1.13 Sanofi

- 6.1.14 Teva Pharmaceuticals

- 6.1.15 Vertex Pharmaceuticals